against all odds

Seite 91 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 328.602 |

| Forum: | Börse | Leser heute: | 36 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 88 | 89 | 90 | | 92 | 93 | 94 | ... 117 > | ||||

But this still doesn’t tell us why money exists. Why do you work such long hours to acquire pieces of paper or electronic credits in a bank account? Why do we stress and worry about money? It might help a bit to think of money as a theater ticket.

If the economy (and our access to goods and services) is the theater, then we can think of money as the ticket that gains us entry to the show. In a modern monetary system a specifically designated form of money is little more than something that gains you entry to be able to transact within that economy. And we work because of and stress about our ability to obtain money because our access to the goods and services that we need ultimately relies on obtaining this tool. At times in human history money has been many things, including unspoken bonds, sticks, rocks, precious metals, pieces of paper, or records on the Internet. Technically, many things can and do meet the various properties of money. These things generally represent something of a certain value that can be easily measured.

In other words we have developed a system of using items of particular value that represent the right to claim a certain amount of goods and services. It is, in essence, a way of recording a deferred promise. But we should be careful not to always think of money as a physical thing or something that has intrinsic value. Money represents a certain value, but the money thing itself (like a cash note) does not necessarily have intrinsic value.

Money in a modern society is largely made up of electronic records and numbers in computer systems. Your bank account exists primarily in a computer system as a record of account and not as a bar of gold in a vault. The electronic money system has come to dominate the way we transact and use this social tool. This brings us to our second crucial understanding about money:

2. Modern money is not necessarily a physical item or something with intrinsic value but is merely a medium of exchange and a record of account.

But what is the primary purpose of money? As I mentioned briefly earlier, the primary purpose of money is to provide us with a convenient medium of exchange for access to goods and services. That is, instead of toting around bars of gold to buy groceries at Walmart or relying on a barter system, we have created convenient ways to record our payments in order to obtain goods and services that we might desire. This gives us access to the ability to feed our families, send our children to school, maintain our health, enjoy ourselves, and so on.

Money, while important, should never be confused with true wealth. Remember, money is merely the medium of exchange. It is a tool like many other tools humans create, and it provides us with a means to an end. While the ticket gets you into the theater, what you want is not the ticket. The ticket simply gives you access to the show, which is the true end. Money is merely the means to that end. Although money is a necessary component of modern life, it is not a necessary component of acquiring true wealth.

Now, true wealth has different meanings to different people, but in most cases it involves the addition of companionship, good friends, good family, good health, access to food, access to water, security, et cetera. More money might make it more convenient to achieve certain things, but money and true wealth should not always be thought of as the same thing. Confusing money with true wealth is like confusing the theater ticket with the performance. Although we need some amount of tickets to enter the theater, the quality of that show is not necessarily dependent on the number of tickets we obtain throughout our lives. While money can certainly make it easier to obtain material goods, and perhaps even some level of happiness, it is always a means to some other end and should not be confused with the end.

This brings us to what might be the most important lesson we can learn about money:

3. Money is not necessarily true wealth.

Almost anything can serve as money. You could take toilet paper to the local pawnshop and trade it for something of equal value, assuming the pawn shop will find it valuable. More commonly we tend to see people view precious metals like gold as money. This is not incorrect. Anything can serve as a medium of exchange. It’s just that gold is a rather inconvenient form of money. It’s heavy, hard to value in real time, and not widely accepted as a medium of exchange. So it’s a fairly inconvenient means of purchasing goods and services.

Most of the money in a modern monetary system is what’s called fiat money. Fiat money is money that has no intrinsic value but is used as a medium of exchange because a specific government deems it so. In Latin fiat means “let it be.” Today’s monetary systems are designed as social systems that institutionalize and organize money under specific laws within specific societies. Governments regulate these monetary systems and identify the entities that may issue specific types of money.

The US government regulates the US monetary system, which is designed around the private banking system. You can think of the private banking system as the playing field upon which the US payments system works. The government is the referee (regulator), and we are the players trying to obtain balls (money) to score goals (consume and produce). But if you want to play on the field designated and regulated by the US government, then you must use the ball that it deems to be acceptable, and that means engaging the playing field that is the US banking system.

In the United States the dollar is the unit of account in which all money is denominated. Unit of account is the measuring stick we use for money. Much like the metric scale, money is measured according to its unit of account. So one dollar can buy you X number of sandwiches or whatever goods or services you desire. The unit of account is different in different countries, but the concept is always the same—a government has designated a specifically denominated money as the unit of account (for instance, the yen in Japan, euros in Europe, or pesos in Mexico), and the government regulates the playing field upon which that unit of

account is used. If you want to participate in the US economy, you must generally obtain money that is denominated in US dollars, which is the standard form of payment accepted for goods and services. In most cases that means participation in the US banking system using bank deposits denominated in dollars.

This brings us to the next important understanding about money:

4. Modern money is a specifically defined unit of account.

For the purposes of this book I will focus primarily on the economic purpose of money. At its most basic purpose, money is simply a medium of exchange, the tool that gains us access to goods and services. Today’s primary tool of exchange is bank deposits. The modern monetary playing field exists primarily within the banking system, which processes trillions of dollars in payments every single day. When you buy a sandwich with your debit card, your bank is processing a payment on your behalf. You are transferring bank deposits from your bank account to that of the seller. When you take money out of the ATM to make a purchase, you are drawing down a bank account in order to transact with physical money more conveniently.

All these transactions are centered around the banking system and the deposit system. Today’s monetary system exists primarily on spreadsheets as numbers in computers recorded by banks as bank deposits. Bank deposits are created when banks make loans; then these deposits are used as the primary means of transacting business at the point of sale. Modern money is both someone’s asset and someone else’s liability, existing primarily in computer systems as records of this basic accounting.

For instance, when a bank creates a loan, the loan generates four specific accounting entries. The loan is an asset for the bank; when the recipient of the loan deposits the money, the deposit creates a liability for the bank. For the borrower the loan is a liability and the deposit is an asset.

Understanding that most modern money is based on the electronic deposit system controlled by the banking system, and that this money is created as credit through the loan creation process, is crucial. This sophisticated banking system allows us to conveniently and efficiently exchange goods and services by establishing a money supply that is elastic. This means the money supply can expand and contract according to the needs of its users. This brings us to an essential understanding of modern money:

5. Most modern money is credit.

In today’s electronic money system most money exists as a record of account on spreadsheets as a result of the accounting relationship that created the money through the loan creation process.

http://www.pragcap.com/...on-page-what-is-money-the-basics-of-banking

Optionen

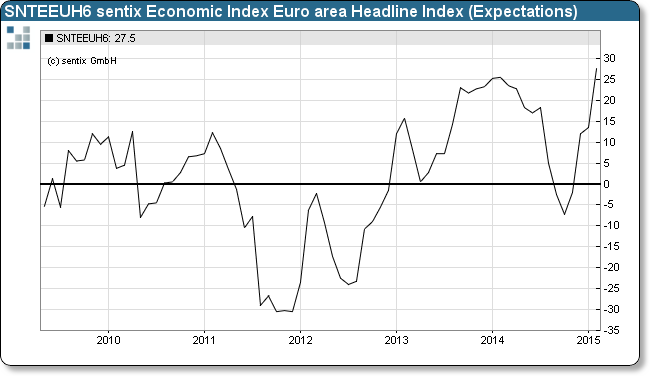

- Current situation -18.5 -19.5 -22.0 -16.5 -12.5 -2.5

- Expectations 0.0 -5.0 4.0 19.0 18.0 37.5

Individual investor

- Current situation -15.0 -20.5 -20.5 -15.5 -9.5 -1.0

- Expectations -5.0 -9.5 -8.0 5.0 9.0 17.5

Optionen

Angehängte Grafik:

default.png (verkleinert auf 78%)

default.png (verkleinert auf 78%)

Cash (+4.7%): Cash balances rose slightly to 4.7% from 4.5% in January. Typical range is 3.5-5%. BAML has a 4.5% contrarian buy level but we consider over 5% to be a better signal. More on this indicator here.

Equities (+57%): A net +57% are overweight global equities, a 7 month high. This is the 4th highest level since the bull market began. Over +50% is bearish. A washout low (bullish) would be under +15-20%. More on this indicator here.

Bonds (-55%): A net -55% are now underweight bonds, a small decline from -53% in January. For comparison, they were -38% underweight in May 2013 before the large fall in bond prices.

Regions:

US (+6%): Exposure to the US sank substantially to +6% overweight from +24% in January.

Europe (+56%): Exposure to Europe jumped massively to +56% overweight, the second highest in the survey's history.

Japan (+35%): Managers are +35% overweight Japan, unchanged from last month. Funds were -20% underweight in December 2012 when the Japanese rally began.

EEM (-1%): Managers increased their EEM exposure to -1% underweight from -13% in January.

Commodities (-20%): Managers commodity exposure remained low at -20% underweight. With the exception of August, it has been less than -15% since early 2013. Low commodity exposure goes in hand with low sentiment towards EEM.

Macro: 51% expect a stronger global economy over the next 12 months, unchanged from January. January 2014 was 75%, the highest reading in 3 years. This compares to a net -20% in mid-2012, at the start of the current rally.

Optionen

Optionen

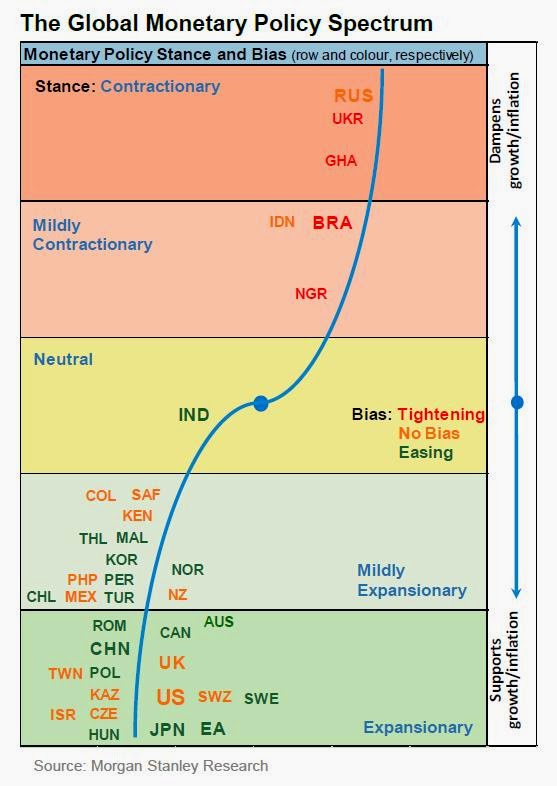

Angehängte Grafik:

the_global_monetary_policy_spectrum__graph_m....jpg (verkleinert auf 91%)

the_global_monetary_policy_spectrum__graph_m....jpg (verkleinert auf 91%)

Optionen

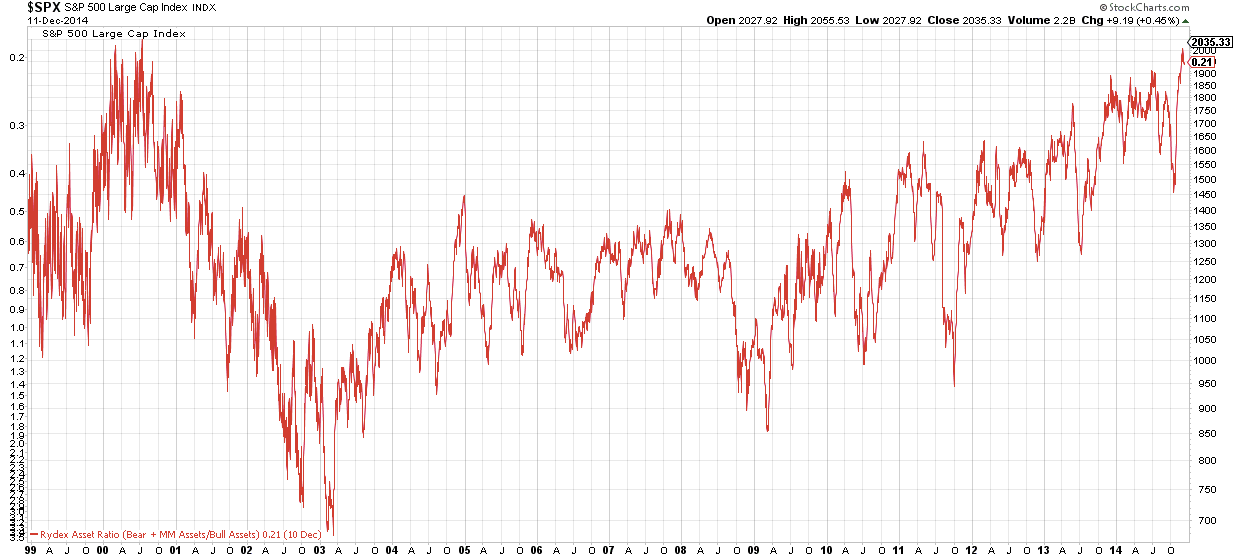

Angehängte Grafik:

rydex.png (verkleinert auf 40%)

rydex.png (verkleinert auf 40%)

That’s not because fixed income traders are stupid. It’s because fixed income traders are hedging against the risk of being on the wrong side of the trade. In other words, the futures curve slopes up to hedge against being wrong. And anyone who was devising policy based on this sort of an expectations based market model has basically been wrong as well because they don’t understand how traders and markets actually work. Scott Sumner loves to say that we should keep finance out of macroeconomics, but his lack of understanding of finance is actually the cause of so many of his misunderstandings about macroeconomics.

All of this can be filed under the folder of “Economics is often a Political Theory Masquerading as a Reflection of Reality”. And it’s a big problem because an economist who can’t accurately understand how markets operate in reality will totally misunderstand the application of many of their ideas. Theory is nice and all, but only when it meshes well with reality.

http://www.pragcap.com/why-expectations-based-econ-models-dont-work

Optionen

Like the government, banks are also money issuers but not issuers of private sector net financial assets. That is, banking transactions always involve the creation of a private sector asset and a liability. Banks create loans independent of government constraint (aside from the regulatory framework). As I will explain, banks make loans independent of their reserve position with the government, rendering the traditional money multiplier deeply flawed.

The monetary system in the developed world is designed specifically around a competitive private banking system. The banking system is not a public-private partnership serving public purpose, as the central bank essentially is. The banking system is a privately owned component of the system run for private profit. The thinking behind this design was to disperse the power of money creation away from a centralized government and put it into the hands of nongovernment entities. The government’s relationship with the private banking system is more a support mechanism than anything else. In this regard I like to think of the government as being a facilitator in helping to sustain a viable credit-based money system.

It’s important to understand that banks are not constrained by the government (outside the regulatory framework) in terms of how they create money. Business schools teach that banks obtain deposits and then leverage those deposits ten times or so. This is why we call the modern banking system a fractional reserve banking system. Banks supposedly lend a portion of their reserves. There’s just one problem here: banks are never reserve constrained. Banks are always capital constrained. This can best be seen in countries such as Canada, which has no reserve requirements. Reserves are used for two purposes—to settle payments in the interbank market and to meet the Fed’s reserve requirements. Aside from this, reserves have little impact on the day-to-day lending operations of banks in the United States. This was recently confirmed in a paper from the Federal Reserve:

“

Changes in reserves are unrelated to changes in lending, and open market operations do not have a direct impact on lending. We conclude that the textbook treatment of money in the transmission mechanism can be rejected.

This is an important point because many people have assumed that various Fed policies in recent years (such as quantitative easing) would be inflationary or even hyperinflationary based on the flawed concept that an expansion of the monetary base (reserves) would lead directly to bank lending and higher inflation. Because banks are not reserve constrained, that is, they don’t lend their reserves or multiply their reserves, this doesn’t necessarily lead to more lending and will not result in the private sector’s being able to access more capital.

The concept of “reserves” sometimes confuses people, but reserves can be thought of as the bank deposits for banks. If we think of the banking system that we use then our deposits are primarily created by banks when they make new loans. But the banking system also has a banking system – the Federal Reserve system. And every bank must maintain an account with the Federal Reserve. This is the market where banks settle interbank payments (payments across different banks). You can think of the reserve system as a big clearinghouse for all the banks to settle payments with. This is always done in reserve deposits so banks are required to maintain a certain amount of reserves at all times. But we shouldn’t think of this clearinghouse as the center of the monetary system or even the point where loans are “multiplied”. That is, the fact that banks must maintain some level of reserves does not mean that they are constrained in their loan making by the quantity of reserves they hold.

That banks are not reserve constrained can mean only one thing—banks lend when credit-worthy customers have demand for loans (assuming the banking system is healthy and banks are engaging in the business they are designed to transact). Loans create deposits, not vice versa. In the loan creation process banks will make loans first (resulting in new deposits) and will find necessary reserves after the fact (either in the overnight market or through the Federal Reserve).

Understanding the business of banking is rather simple. It’s best to think of banks as running a payments system that helps us all transact within the economy. In addition to helping manage this payments system, banks issue money in the form of loans. Banks earn a profit from transacting business when their assets are less expensive than their liabilities. In other words banks need to run this payments system smoothly but will seek to do so in a manner that doesn’t reduce their profitability.

Banks don’t necessarily use their deposits or reserves to create loans, however. Banks make loans and find reserves after the fact if they have to. But since banking is a spread business (having assets that are less expensive than liabilities), the banks will always seek the least expensive source of funds for managing their payment system. That just so happens to be bank deposits. This gives the appearance that banks fund their loan book by obtaining deposits, but this is not necessarily the case. It is better to think of banking as a spread business in which the bank simply acquires the least expensive liabilities to sustain its payment system and maximize profits. Banks need funding sources to run their businesses, but they do not necessarily need reserves or deposits to make those loans.

To illustrate this point I will briefly review the change in balance sheet composition between banks and households before and after a loan is made. Since banks are not constrained by their reserves, the banks do not need to have X amount of reserves on hand to create new loans. But banks must have ample capital to be able to operate and meet regulatory requirements.

http://www.pragcap.com/the-basics-of-banking

Optionen

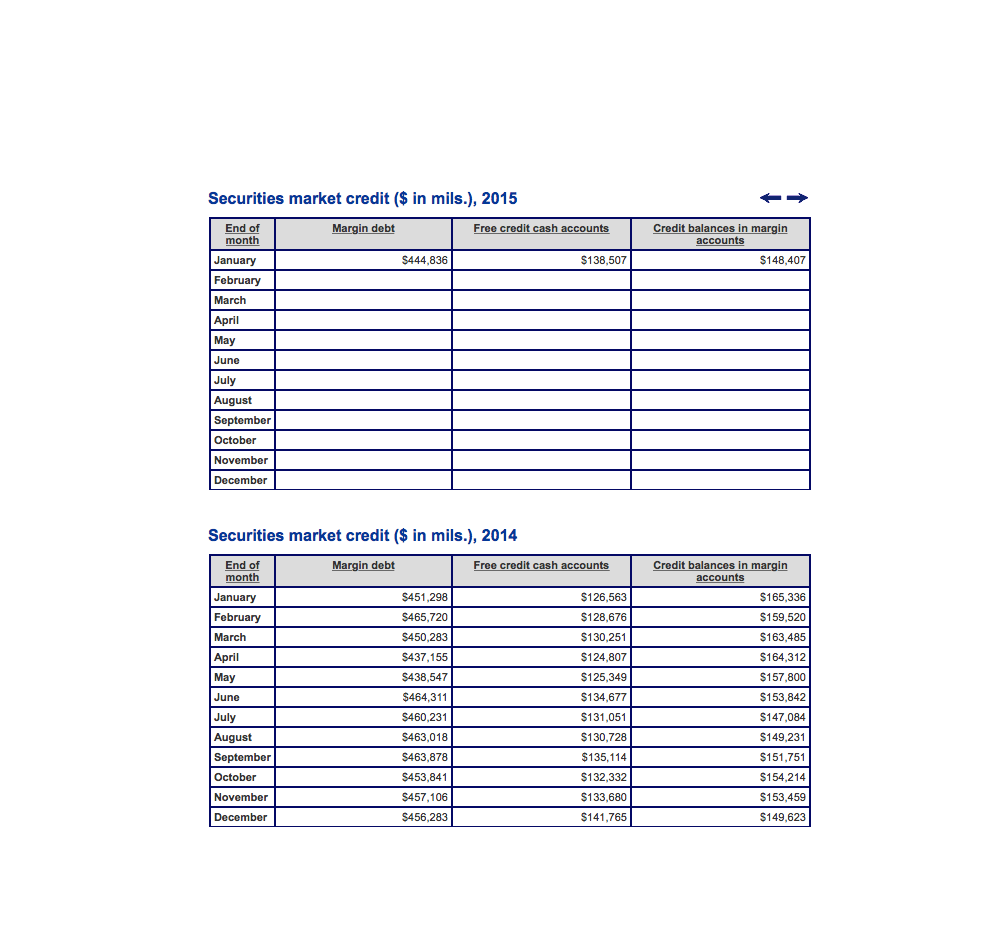

Angehängte Grafik:

bildschirmfoto_2015-03-02_um_13.png (verkleinert auf 50%)

bildschirmfoto_2015-03-02_um_13.png (verkleinert auf 50%)