against all odds

Seite 87 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 342.408 |

| Forum: | Börse | Leser heute: | 1 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 84 | 85 | 86 | | 88 | 89 | 90 | ... 117 > | ||||

Normalerweise trauen sich dann viele einen zweiten Versuch nicht mehr. Deshalb hier einen engen SL. geht es tiefer ist man mit begrenzten Verlust raus. Läuft der Wert dann doch wieder über den alten SL könnte man den zweiten Versuch starten. So ist mein Plan.

Optionen

Angehängte Grafik:

large.png (verkleinert auf 74%)

large.png (verkleinert auf 74%)

The bottom line is, I don’t know what the obsession with the monetary base is. Economists like to obsess over the central bank and the government because they view these entities as creating the real “money” in our economy. But this model almost always relies on a defunct money multiplier concept, misunderstandings of modern banking and ignores the fact that credit (bank created money) is indeed money. In fact, bank money isn’t just money, it’s the most important form of money that exists in our economy. Starting with the government and working out to the banking system is constructing a model of understanding that is entirely backwards. So starting with the Monetary Base as a foundation for understanding “inflation” is not just wrong in the common usage of the word, but almost certain to mislead you about the effects of this “money” creation. In essence, the Austrian definition of “inflation” is practically useless to anyone who wants to understand our monetary system as it actually exists....'

Read more at http://pragcap.com/about-that-inflation-defintion#w5Hd5j8yh7ltEbE8.99

Optionen

(2) both Post Keynesians and (at least some) Austrians have criticisms of the quantity theory of money; while the Austrians criticise the quantity theory on the basis of Cantillon effects, the Post Keynesian critique is much more radical;

(3) both Post Keynesians and Austrians reject rational expectations and think expectations are subjective;

(4) both Post Keynesians and Austrians stress the role of irreversible time and fundamental uncertainty in economics, and the limitations of probability theory in economic decision making (indeed some Austrians see Keynes’ and Mises’ views on probability as complementary);

(5) both Post Keynesians and Austrians have criticisms of the neoclassical theory of capital, though they part company on exactly what that the critique is.

http://socialdemocracy21stcentury.blogspot.de/...criticised_9471.html

Optionen

The theory was developed by Irving Fisher following the Wall Street Crash of 1929 and the ensuing Great Depression. The debt deflation theory was familiar to John Maynard Keynes prior to Fisher's discussion of it but he found it lacking in comparison to what would become his theory of liquidity preference.[1] The theory, however, has enjoyed a resurgence of interest since the 1980s, both in mainstream economics and in the heterodox school of Post-Keynesian economics, and has subsequently been developed by such Post-Keynesian economists as Hyman Minsky[2] and Steve Keen.[3]

Fisher's formulation[edit]

In Fisher's formulation of debt deflation, when the debt bubble bursts the following sequence of events occurs:

Assuming, accordingly, that, at some point in time, a state of over-indebtedness exists, this will tend to lead to liquidation, through the alarm either of debtors or creditors or both. Then we may deduce the following chain of consequences in nine links:

Debt liquidation leads to distress selling and to Contraction of deposit currency, as bank loans are paid off, and to a slowing down of velocity of circulation. This contraction of deposits and of their velocity, precipitated by distress selling, causes A fall in the level of prices, in other words, a swelling of the dollar. Assuming, as above stated, that this fall of prices is not interfered with by reflation or otherwise, there must be A still greater fall in the net worths of business, precipitating bankruptcies and A like fall in profits, which in a "capitalistic," that is, a private-profit society, leads the concerns which are running at a loss to make A reduction in output, in trade and in employment of labor.

These losses, bankruptcies and unemployment, lead to pessimism and loss of confidence, which in turn lead to Hoarding and slowing down still more the velocity of circulation. The above eight changes cause Complicated disturbances in the rates of interest, in particular, a fall in the nominal, or money, rates and a rise in the real, or commodity, rates of interest.

Prior to his theory of debt deflation, Fisher had subscribed to the then-prevailing, and still mainstream, theory of general equilibrium. In order to apply this to financial markets, which involve transactions across time in the form of debt – receiving money now in exchange for something in future – he made two further assumptions:[4]

(A) The market must be cleared—and cleared with respect to every interval of time.

(B) The debts must be paid. (Fisher 1930, p.495)

In view of the Depression, he rejected equilibrium, and noted that in fact debts might not be paid, but instead defaulted on:

It is as absurd to assume that, for any long period of time, the variables in the economic organization, or any part of them, will "stay put," in perfect equilibrium, as to assume that the Atlantic Ocean can ever be without a wave.

He further rejected the notion that over-confidence alone, rather than the resulting debt, was a significant factor in the Depression:

I fancy that over-confidence seldom does any great harm except when, as, and if, it beguiles its victims into debt.

In the context of this quote and the development of his theory and the central role it places on debt, it is of note that Fisher was personally ruined due to his having assumed debt due to his over-confidence prior to the crash, by buying stocks on margin.

Other debt deflation theories do not assume that debts must be paid, noting the role that default, bankruptcy, and foreclosure play in modern economies.[5]

Debt deflation has been studied and developed largely in the Post-Keynesian school.

The Financial Instability Hypothesis of Hyman Minsky, developed in the 1980s, complements Fisher's theory in providing an explanation of how credit bubbles form: FIH explains how bubbles form, while DD explains how they burst and the resulting economic effects. Mathematical models of debt deflation have recently been developed by Australian post-Keynesian economist Steve Keen.

Initially Fisher's work was largely ignored, in favor of the work of Keynes.[6]

The following decades saw occasional mention of deflationary spirals due to debt in the mainstream, notably in The Great Crash, 1929 of John Kenneth Galbraith in 1954, and the credit cycle has occasionally been cited as a leading cause of economic cycles in the post-WWII era, as in (Eckstein & Sinai 1990), but private debt remained absent from mainstream macroeconomic models. James Tobin cited Fisher as instrumental in his theory of economic instability.

The lack of influence of debt-deflation in academic economics is thus described by Ben Bernanke in Bernanke (1995, p. 17):

Fisher's idea was less influential in academic circles, though, because of the counterargument that debt-deflation represented no more than a redistribution from one group (debtors) to another (creditors). Absent implausibly large differences in marginal spending propensities among the groups, it was suggested, pure redistributions should have no significant macroeconomic effects.

Bernanke's dismissal of debt deflation is criticized as improperly applying the theory of general equilibrium – in equilibrium, marginal redistribution of income produces no macroeconomic effects, but financial crises are characterized by not being in equilibrium and markets failing to clear – debt ceasing to grow and instead falling, debtors defaulting, rising unemployment – and thus, it is argued, equilibrium analysis is inapplicable and misleading.[4]

There was a renewal of interest in debt deflation in academia in the 1980s and 1990s,[7] and a further renewal of interest in debt deflation due to the financial crisis of 2007–2010 and the ensuing Great Recession.[6]

Debt-deflation theory has been studied since the 1930s but was largely ignored by neoclassical economists, and has only recently begun to gain popular interest, although it remains somewhat at the fringe in U.S. media.[8][9][10][11][12] In 2008, one legal journal wrote, "Bernanke has made sure that the second leg of a Fisherian debt deflation will not occur. But, past and present U.S. authorities have failed to adequately restore the balance sheets of over-leveraged banks, firms, and households."[13] In 2011, another law journal wrote, "the global economy has recently experienced a classic Minsky crisis - one with intertwined cyclical and institutional (structural) dimensions."[14]

Kenneth Rogoff and Carmen Reinhart's works published since 2009[15] have addressed the causes of financial collapses both in recent modern times and throughout history, with a particular focus on the idea of debt overhangs.

Similar theories[edit]

Debt deflation is not the only economic theory that cites credit bubbles as a key factor in economic crises; the most noted other theory is Austrian business cycle theory, which posits that economic crises are caused by excess credit growth and the malinvestment (misallocation of resources) that results, with these being caused by central bank monetary policy and the fractional-reserve banking system.

The first difference between these may be stated as debt-deflation being a demand-side theory, which emphasizes the period after the peak – the end of a credit bubble and contraction of debt causing a fall in aggregate demand – while the Austrian theory is a supply-side theory, which emphasizes the period before the peak – the growth of debt during the growth phase causing malinvestment. The theories may thus be seen as complementary, addressing different aspects of the issue, and are so-considered by some economists.[16]

In normative respects the theories are sharply different, with proponents of debt deflation generally arguing in the Keynesian, more precisely Post-Keynesian, tradition that government action can be beneficial, notably via debt forgiveness or engineering inflation (to reduce debt burden), or facilitating change in industries and investments, while Austrian economists generally argue that there is nothing to be done, the "malinvestments" needing to be "worked out of the system".

There have been other theories of economic crisis citing credit, discussed at the relevant section of Austrian business cycle theory.

Solutions[edit]

Fisher viewed the solution to debt deflation as reflation – returning the price level to the level it was prior to deflation – followed by price stability, which would break the "vicious spiral" of debt deflation. In the absence of reflation, he predicted an end only after "needless and cruel bankruptcy, unemployment, and starvation",[17] followed by "a new boom-depression sequence":[18]

Unless some counteracting cause comes along to prevent the fall in the price level, such a depression as that of 1929-33 (namely when the more the debtors pay the more they owe) tends to continue, going deeper, in a vicious spiral, for many years. There is then no tendency of the boat to stop tipping until it has capsized. Ultimately, of course, but only after almost universal bankruptcy, the indebtedness must cease to grow greater and begin to grow less. Then comes recovery and a tendency for a new boom-depression sequence. This is the so-called "natural" way out of a depression, via needless and cruel bankruptcy, unemployment, and starvation.

On the other hand, if the foregoing analysis is correct, it is always economically possible to stop or prevent such a depression simply by reflating the price level up to the average level at which outstanding debts were contracted by existing debtors and assumed by existing creditors, and then maintaining that level unchanged.

Later commentators do not in general believe that reflation is sufficient, and primarily propose two solutions: debt relief – particularly via inflation – and fiscal stimulus.

Following Hyman Minsky, some argue that the debts assumed at the height of the bubble simply cannot be repaid – that they are based on the assumption of rising asset prices, rather than stable asset prices: the so-called "Ponzi units". Such debts cannot be repaid in a stable price environment, much less a deflationary environment, and instead must either be defaulted on, forgiven, or restructured.

Widespread debt relief either requires government action or individual negotiations between every debtor and creditor, and is thus politically contentious or requires much labor. A categorical method of debt relief is inflation, which reduces the real debt burden, as debts are generally nominally denominated: if wages and prices double, but debts remain the same, the debt level drops in half. The effect of inflation is more pronounced the higher the debt to GDP ratio is: at a 50% ratio, one year of 10% inflation reduces the ratio by approximately to 45%, while at a 300% ratio, one year of 10% inflation reduces the ratio by approximately to 270%. In terms of foreign exchange, particularly of sovereign debt, inflation corresponds to currency devaluation. Inflation results in a wealth transfer from creditors to debtors, since creditors are not repaid as much in real terms as was expected, and on this basis this solution is criticized and politically contentious.

In the Keynesian tradition, some suggest that the fall in aggregate demand caused by falling private debt can be compensated for, at least temporarily, by growth in public debt – "swap private debt for government debt", or more evocatively, a government credit bubble replacing the private credit bubble. Indeed, some argue that this is the mechanism by which Keynesian economics actually works in a depression – "fiscal stimulus" simply meaning growth in government debt, hence boosting aggregate demand. Given the level of government debt growth required, some proponents of debt deflation such as Steve Keen are pessimistic about these Keynesian suggestions.[19]

Given the perceived political difficulties in debt relief and the suggested inefficacy of alternative courses of action, proponents of debt deflation are either pessimistic about solutions, expecting extended, possibly decades-long depressions, or believe that private debt relief (and related public debt relief – de facto sovereign debt repudiation) will result from an extended period of inflation.'

http://en.wikipedia.org/wiki/Debt-deflation

Optionen

Contrast with mainstream theory[edit]

The key distinction from mainstream economic theories of money creation is that circuitism holds that money is created endogenously by the banking sector, rather than exogenously by the government through central bank lending: that is, the economy creates money itself (endogenously), rather than money being provided by some outside agent (exogenously). Circuitism also models banks and other firms separately, rather than combining them into a representative agent as in mainstream neoclassical models.

These theoretical differences lead to a number of different consequences and policy prescriptions; circuitism rejects, among other things, the money multiplier based on reserve requirements, arguing that money is created by banks lending, which only then pulls in reserves from the central bank, rather than by re-lending money pushed in by the central bank. The money multiplier arises instead from capital adequacy ratios, i.e. the ratio of its capital to its risk-weighted assets.[2] It also emphatically rejects the neutrality of money, believing instead that the money supply and its growth or decline are critical to the functioning of the economy.

Circuitism is easily understood in terms of familiar bank accounts and debit card or credit card transactions: bank deposits are just an entry in a bank account book (not specie – bills and coins), and a purchase subtracts money from the buyer's account with the bank, and adds it to the seller's account with the bank.

Transactions[edit]

As with other monetary theories, circuitism distinguishes between hard money – money that is exchangeable at a given rate for some commodity, such as gold – and credit money. Unlike mainstream monetary theory, it considers credit money created by commercial banks as primary (at least in modern economies), rather than derived from central bank money – credit money drives the monetary system. While it does not claim that all money is credit money – historically money has often been a commodity, or exchangeable for such – basic models begin by only considering credit money, adding other types of money later.

In circuitism, a monetary transaction – buying a loaf of bread, in exchange for dollars, for instance – is not a bilateral transaction (between buyer and seller) as in a barter economy, but is rather a tripartite transaction between buyer, seller, and bank. Rather than a buyer handing over a physical good in exchange for their purchase, instead there is a debit to their account at a bank, and a corresponding credit to the seller's account. This is precisely what happens in credit card or debit card transactions, and in the circuitist account, this how all credit money transaction occur.

For example, if one purchases a loaf of bread with fiat money bills, it may appear that one is purchasing the bread in exchange for the commodity of "dollar bills", but circuitism argues that one is instead simply transferring a credit, here with the issuing central bank: as the bills are not backed by anything, they are ultimately just a physical record of a credit with the central bank, not a commodity.

Monetary creation[edit]

In circuitism, as in other theories of credit money, credit money is created by a loan being extended. Crucially, this loan need not (in principle) be backed by any central bank money: the money is created from the promise (credit) embodied in the loan, not from the lending or relending of central bank money: credit is prior to reserves.

When the loan is repaid, with interest, the credit money of the loan is destroyed, but reserves (equal to the interest) are created – the profit from the loan.

In practice, commercial banks extend lines of credit to companies – a promise to make a loan. This promise is not considered money for regulatory purposes, and banks need not hold reserves against it, but when the line is tapped (and a loan extended), then bona fide credit money is created, and reserves must be found to match it. In this case, credit money precedes reserves. In other words making loans pulls reserves in (assuming that the regulatory need for bank reserves exists), instead of reserves being pushed out as loans which is assumed by the mainstream model.

The failure of monetary policy during depressions – central banks give money to commercial banks, but the commercial banks do not lend it out – is referred to as "pushing on a string", and is cited by circuitists in favor of their model: credit money is pulled out by loans being extended, not pushed out by central banks printing money and giving it to commercial banks to lend....'

http://en.wikipedia.org/wiki/Monetary_circuit_theory

Optionen

Ist nicht schön, aber passiert. Weiter beobachten!

Und das wo alle Welt auf die Korrektur wartet!

Commodities funktionieren anders als die Indizes und vielleicht brauch ich etwas mehr Hintergrund.

But there’s a more important point here. The idea that the Fed is financing the deficit implies that the US Treasury could not otherwise sell the bonds at the current rates. I find this very hard to believe given that demand for US Treasury bonds actually INCREASED before QE was implemented during the financial crisis and the fact that inflation has remained extremely low in the USA. Could there come a time when inflation is spiraling out of control and demand for US government bonds declines to a point where the Fed must intervene just to bolster demand? Of course. But that time is not now and hasn’t occurred in the last five years. So, until then, I am inclined to say that QE in the USA is just a big time version of monetary policy and not a direct financing of US government spending...'

http://pragcap.com/does-qe-finance-government-spending

Optionen

b Saldenmechanik verstehen - die Veränderung einer Variablen ist mit der Veränderung anderer identisch

c Ideologische Narrative als Driver der Marktoberfläche und ihre je nach dem Stand im Zyklus unterschiedliche Wirkweise verstehen

d Basic Uncertainty, irrational Expectation, basic Disquilibrium und Animal Spirits als kausale psychologische Driver verstehen

e Sentimentindikationen relativ zum Stand im Zyklus zu einem Gesamtbild zusammen fügen

f wasserdichte Ideologieresistenz - je dominanter die Ideologie, desto grösser der mentale Abstand

g der eigenen Intuition vertrauen - es gibt nichts, was smarter wäre

Optionen

Philip Pilkington: Monetary Economics quite consciously departs from the neoclassical paradigm while at the same time setting itself the high task of producing concise and coherent models. So, let’s start from the beginning: why did you and Godley feel the need to depart so forcefully from the neoclassical paradigm? To tear yourselves away from it in such black and white terms as stated in the introduction to the book suggests to me that you and Godley found it lacking at a very fundamental level. Could you explain why this is?

Marc Lavoie: Having dealt with real world economics, through his position at the British Treasury until 1970, Wynne was convinced that mainstream macroeconomics just did not make any sense, whether it was monetarism or the standard Keynesian IS/LM model of the time; in fact he could not understand how any reasonable person, not yet brainwashed by courses in mainstream economics, could grant any credibility to the textbook and to the sophisticated models of mainstream economics. So it is clear that Wynne wished to depart from neoclassical economics, and start from scratch, which is what he did to some extent already when Wynne and his colleague Francis Cripps wrote a highly original book that was published in 1983, Macroeconomics. This book was written because Wynne got convinced that the Keynesians of all strands were losing their battle against Milton Friedman and the monetarists, because Keynesians could only provide very convoluted answers to simple questions such as: “Where does money come from? Where does it go? How do the income flows link up with the money stocks? How is new production financed?”

Our book Monetary Economics also tries to provide appropriate answers to these questions. We agonized for a while between trying to engage in a constructive dialogue with our mainstream colleagues and targeting a non-mainstream audience, or perhaps trying to achieve both goals. In the end, we figured that it would be very difficult to please both audiences, and we chose to focus on a heterodox audience. In any case, I have spent most of my academic career trying to develop alternative views and alternative models of economics – what is now called heterodox economics; this is the literature we know best. So we took our book as a formal contribution to this heterodox literature and more specifically as a contribution to post-Keynesian economics.

PP: I know it’s a rather general question, but what did you and Wynne feel were the most fundamental weaknesses of neoclassical/monetarist theory? In the book you put a lot of emphasis on dynamism and change, was this a major point of departure from the mainstream?

ML: Well, that is a rather grandiose question! Critics of neoclassical economics, and of Friedman’s monetarism, have written dozens of books and thousands of pages about this topic. To start with, I suppose that Wynne objected to basic demand-pull explanations of inflation, where the excess supply of money generates excess aggregate demand and hence inflation. Wynne thought that the money supply is endogenous, brought about by the requirements of the economy, mainly by the time taken by the production process, which involved unfinished goods and goods not yet sold, the production of which had to be financed by credit. Wynne also rejected the mainstream explanation of inflation because his work on pricing theory led him to believe that prices were based on normal unit costs, with no clear relationship between higher output and this normal unit cost, nor between higher output and the markup. So any relationship that could be found between prices and money was likely to be due to a reversed causality. Indeed, Wynne never believed in the concept of the natural rate of unemployment, the NAIRU, or the associated vertical Phillips curve; and the most sophisticated econometric analysis, meta-analysis, has proved him right.

Reversed causation also affected the link between investment and saving: for Keynesians, investment drives saving, whereas the neoclassical view is that saving allows investment. The importance of getting this causality right is clear nowadays: a true neoclassical author would argue that households need to save more so as to provide firms with the funds they need to invest; but if households reduce their consumption expenditures, with firms selling less, why would they want to invest more? Neoclassical macroeconomics is essentially supply-led; this to us is its fundamental weakness: capitalist economies, most of the time, are demand-led. They generally suffer from a lack of effective demand, not from a lack of capacity or a lack of labour resources. Thus we mostly focus on the variables that determine aggregate demand. I used to believe that only advanced economies had spare capacity; but then I read a 1983 book of Lance Taylor, showing the peculiar features of less-developed economies and how they should be modelled: he also assumed spare capacity!

It is also true as you point out that in our book we emphasize the transition from the starting position towards the new equilibrium – that is we go beyond comparative statics, beyond comparing the initial state to the final new state of the model. In part, this is because the short-run results of a change may turn out to be opposite of the long-run impact. For instance, in one of our more sophisticated models, the desire of households to borrow a greater percentage of their personal income has a favourable impact on consumption and GDP in the short-run, but it has a negative impact on these two variables in the long-run. This we do with simulations; but of course, with fancy enough mathematics, you can also show this with the help of algebra, provided the model is not overly complicated.

more http://www.nakedcapitalism.com/2012/06/...ith-marc-lavoie-part-i.html

Optionen

Optionen

http://www.elgaronline.com/view/journals/roke/2-3/roke.2014.03.04.xml

Optionen

Optionen

Angehängte Grafik:

fig1.gif (verkleinert auf 77%)

fig1.gif (verkleinert auf 77%)

Der Konflikt in der Ukraine wird von den Amis genutzt, um einen der Großen Player gegen den Dollar (Russland) unter Druck zu setzen. Gelingt bisher auch ganz gut. Das könnte unter anderem auch wieder zu guten Tradinggelegenheiten bei russischen Assets führen.

Nur wie weit es diesmal nach unten geht ist kaum absehbar, weil die Kontrahenten bisher nicht den Eindruck machen, dass einer nachgeben will, wobei Russland eigentlich keine guten Karten hat. Aber hier geht es auch um den Machtstatus eines Diktators und da spielen Argumente, wie sie in einer Demokratie gelten würden keine Rolle.

Putin wird diesen Kampf annehmen und wenn die russische Wirtschaft erst einmal den Bach runter geht wird es ihn nicht sonderlich kratzen. Hauptsache er bleibt an der Macht!

Russland setzt auf den amerikanisch / westlich dominierten Weltmarkt, weil es sich als Rohstoffproduzent in dessen Abhängigkeit gebracht hat, also überhaupt keine Alternative mehr als Partizipation existiert. Ru's Bockigkeit ist vielleicht ärgerlich, aber keine echte Bedrohung und schon gar kein Gegner des Westens. Sein Pech ist es aber, mit dieser Bockigkeit das Material bereitgestellt zu haben, an dem die Frage, wer in Europa das Sagen hat, ausgefochten wird. Investieren würde ich jetzt da nun nicht gerade...

Optionen

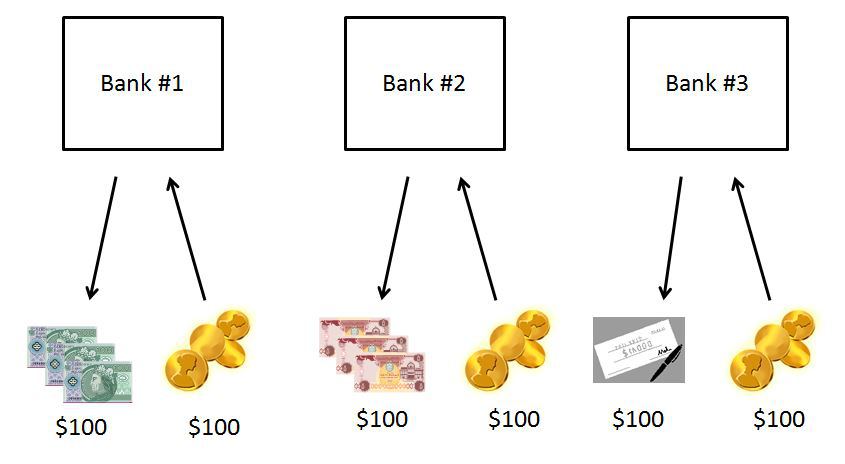

Of course, I’ve argued that this is wrong and that we have a truly endogenous system in which we can all create money and banks hold a special importance because of their centrality to the payment system we all use. The “moneyness” of the item they create is unique in ways that outside money is not in regard to playing a crucial role in everyday economic activity. In other words, when understanding the monetary system it is best to start from the inside out, not from the outside in. In addition, we’ve discovered that the money multiplier is a myth, that banks don’t lend reserves, QE doesn’t create high inflation and the impact of increasing quantities of outside money is pretty muted.

As technology advances the banks are actually taking an even stronger hold over the system. They are making outside money increasingly less important. And they are exposing the reality that our monetary system is not constructed around outside money, but indeed revolves around the stability and strength of our banking system. Some might find that alarming, but that’s how the system has always been designed. The corporations rule the day and the government bends over backwards to service their needs. The construction of our payment system is no different really.

http://pragcap.com/the-death-of-outside-money

Optionen

After that, I"m going to explain how the market settles on an interest rate in a fractional-reserve free banking system. I"m then going to explain how fractional-reserve central banking works on a gold standard, to include a discussion of the use of reserve requirements and base money supply expansion and contraction as a means of controlling bank funding costs and aggregate bank lending. Finally, I"m going to refute two misconceptions about the Gold Standard–first, that it caused the Great Depression (it categorically did not), and second, that its reign in the U.S. ended in 1971 (not true–its reign ended in the Spring of 1933).

full: http://www.philosophicaleconomics.com/

Optionen

Angehängte Grafik:

bank2.jpg (verkleinert auf 60%)

bank2.jpg (verkleinert auf 60%)

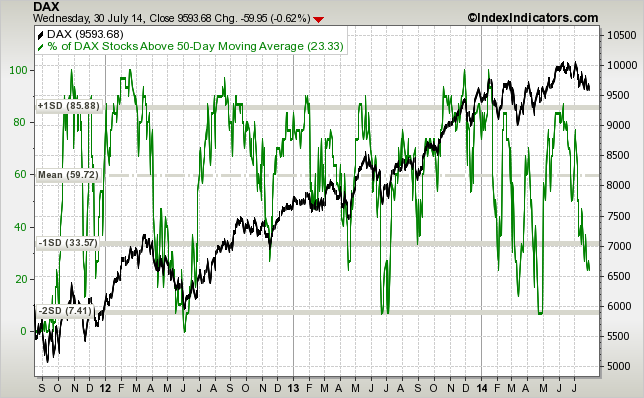

Nun sieht es doch nach einer Korrektur aus, wobei jetzt die Frage im Raum steht wie weit diese gehen kann. Für die Bullen spräche nur aus Sicht der EMA 50 im Dax, dass mit dem heutigen Tage dieser Indikator wohl so ziemlich am Boden ist.

Schaue ich mir die Tageskerze an, sollte zumindest eine technische Gegenreaktion drin sein.

Hab mal eine Spielposition Long gekauft.

Angehängte Grafik:

ema_50_31.png (verkleinert auf 79%)

ema_50_31.png (verkleinert auf 79%)

Optionen

Angehängte Grafik:

indexpc.gif

indexpc.gif