against all odds

Seite 84 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 342.664 |

| Forum: | Börse | Leser heute: | 15 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 81 | 82 | 83 | | 85 | 86 | 87 | ... 117 > | ||||

Jetzt wieder im Niemandsland und da können nur Daytrader arbeiten.

Optionen

tut mir leid, dass du ne doofe zeit hast... hold die ohren stibe

cheers und danke wie immer

Optionen

Optionen

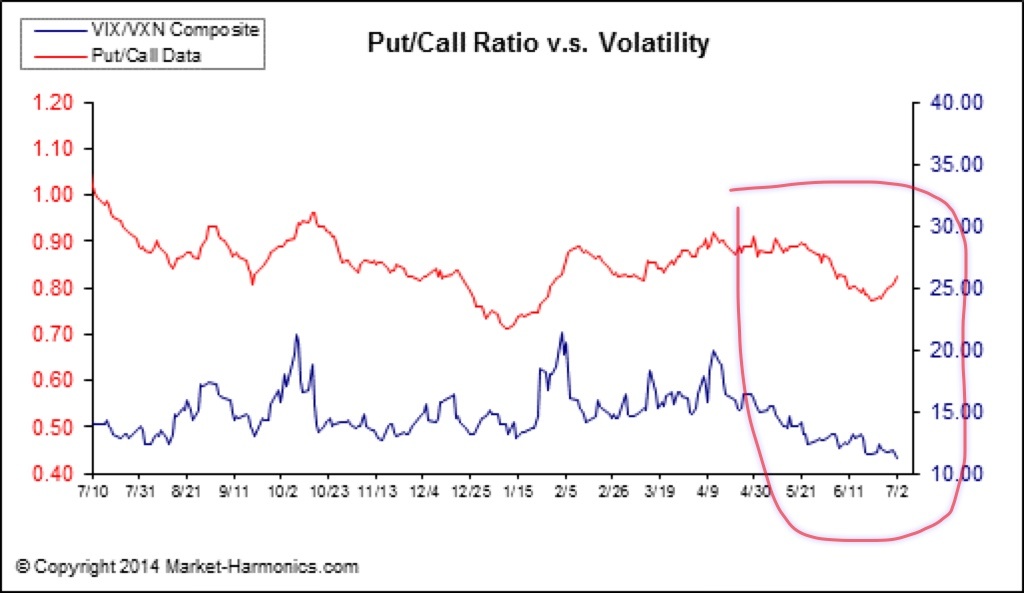

Angehängte Grafik:

image.jpg (verkleinert auf 49%)

image.jpg (verkleinert auf 49%)

Optionen

Optionen

Shorts habe ich zur Zeit keine mehr. Kurzfristig hatte ich versucht Priceline zu shorten, was ich jedoch schnell beendete. Die Zeit ist halt noch nicht reif, um die Big-Momentum Aktien anzugreifen.

ps beschreib doch mal Deinen Silver Trade

Optionen

Optionen

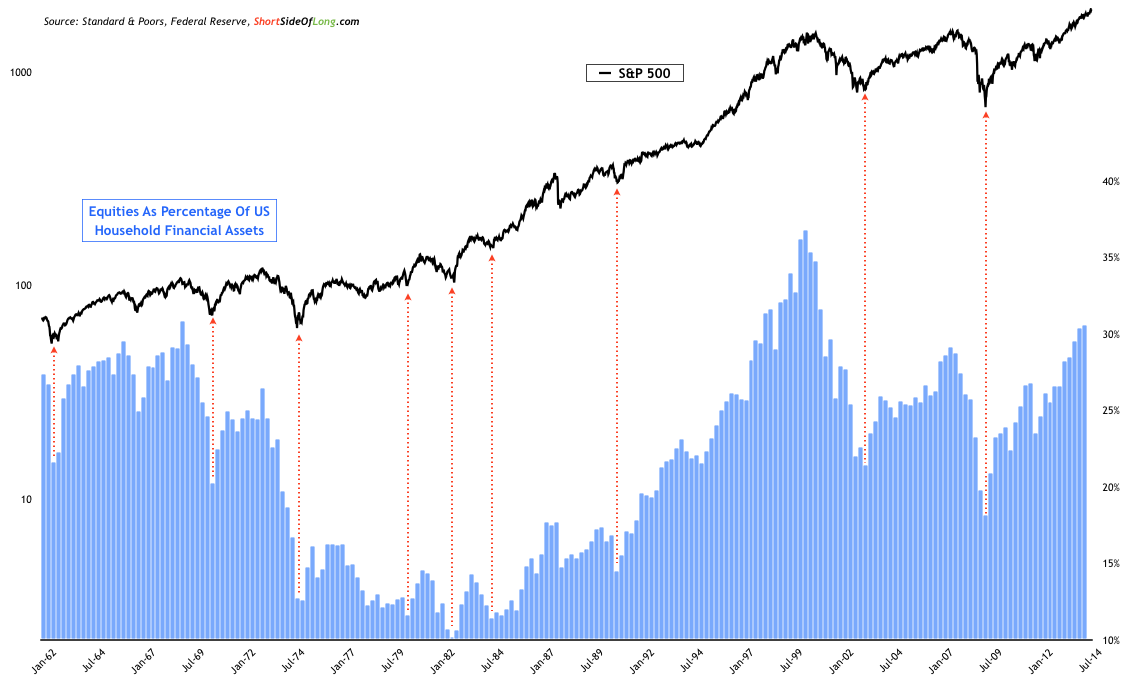

Angehängte Grafik:

equities-as-percentage-of-us-household-financial-....png (verkleinert auf 45%)

equities-as-percentage-of-us-household-financial-....png (verkleinert auf 45%)

Optionen

Angehängte Grafik:

pragcap.jpg

pragcap.jpg

Mission Statement - The best way to understand the workings of the economy is by understanding the way the human mind reacts and adapts to markets and the economy.

General view of the economy - The economy is complex, dynamic and uncertain and is being navigated by imperfect participants. Because of this it could be appropriate for government intervention at times.

How to fix the economy - Behavioralists don’t make specific policy recommendations, but generally believe that we can better understand the economy if we better understand human psychology as it pertains to money, markets and the economy.

What they love - Prospect theory, studying human biases and highlighting the fact that we’re totally ill-equipped to deal with money and markets.

What they hate - That their work is often rejected by mainstream economists as being something outside of the field of real economics.

Notable Pundits - Richard Thaler, Robert Shiller, Dan Ariely & Daniel Kahneman.

Famous Dead Economist Associated with School - George Katona & Amos Tversky.

Political Associations - No direct political associations.

Preferred form of communication - Well researched papers and books primarily. Behavioralists, not surprisingly, tend to be open-minded and well behaved.

Further Reading:

1- Prospect Theory: An Analysis of Decision under Risk – Kahneman & Tversky

2- Behavioral Economics – Thaler & Mullainathan

3 – Predictably Irrational - Ariely

Read more at http://pragcap.com/...ferent-schools-of-economics#gVvzHJ1yssZ3DLyX.99

Optionen

Optionen

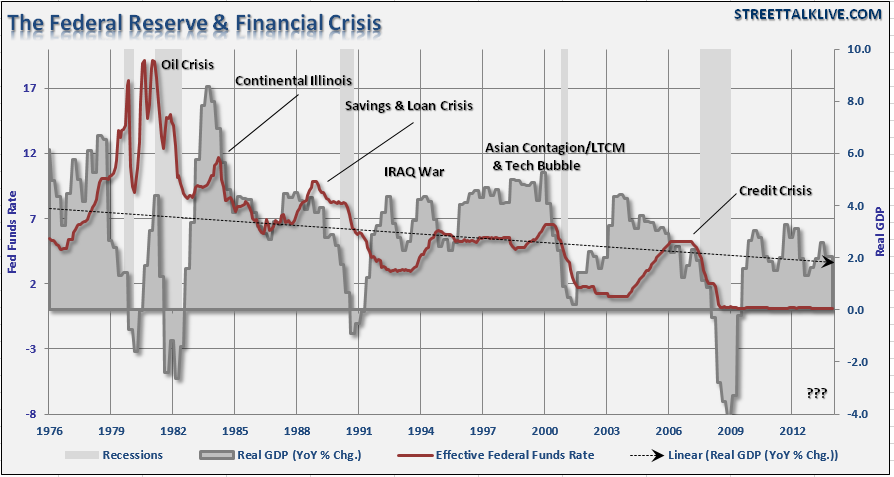

Angehängte Grafik:

fed-funds-crisis-062014.png (verkleinert auf 57%)

fed-funds-crisis-062014.png (verkleinert auf 57%)

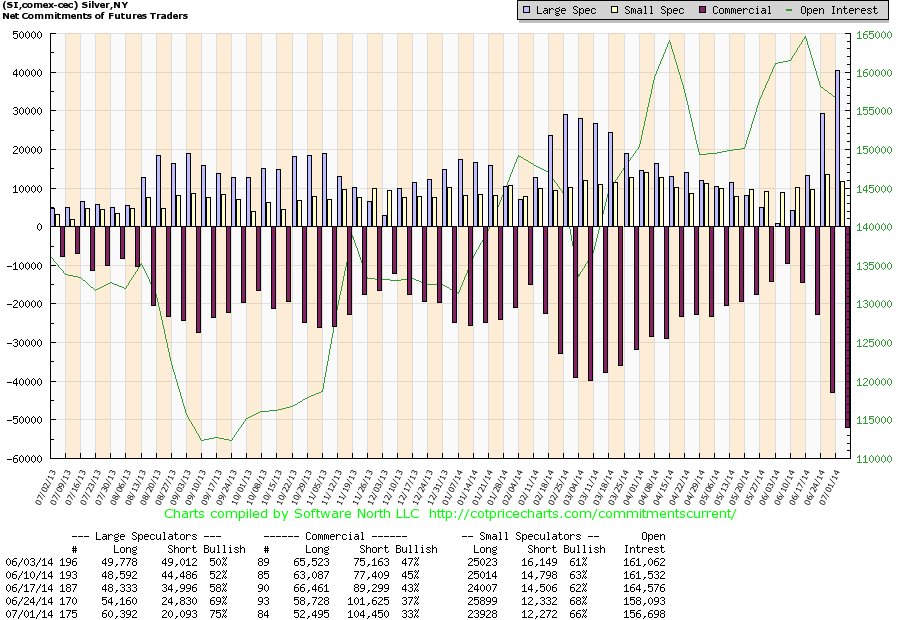

Im Grunde hat mich the Long side of.... darauf gebracht, durch die Analyse der Short-Positionierungen bei Silber. Dazu kam noch, dass ich den letzten Shortsqueeze auch schon erwischt hatte.

Der Chart hatte ein Tief gesehen mit einem Rebound über einen Widerstand, der als sehr markant zu bezeichnen ist. Beim Oval bin ich dann eingestiegen, auch weil es kaum Druck nach unten gab. Nach dem Squeeze bin ich ausgestiegen weil die Position zu groß war, um den Gewinn wieder in Frage zu stellen.

Seither beobachte ich Silber und bin eigentlich positiv für die weitere Entwicklung gestimmt, da anscheinend allgemein die Metalle zu kommen scheinen.

Angehängte Grafik:

silber.png (verkleinert auf 28%)

silber.png (verkleinert auf 28%)

Optionen

Angehängte Grafik:

si.png (verkleinert auf 56%)

si.png (verkleinert auf 56%)

2) The government is a user of bank money. When the government taxes Paul they take Paul"s bank money and redistribute it to Peter when they spend.

3) If the government runs a budget deficit (taxes less than it spends) then Paul buys a bond from the government and the government gives Paul"s bank deposit (which he used to buy the bond with) to Peter. Paul gets a bond which the government created in much the same way that a private corporation creates a bond when they issue corporate debt. If you want to say these entities "print" financial assets then fine. Corporations print stocks and bonds every day and you don"t hear the world exploding with hyperinflation rants because of it….

4) When the Fed performs quantitative easing they perform open market operations (just like they have for decades) which involve a clean asset swap where the bank essentially exchanges reserves for t-bonds. The private sector loses a financial asset (the t-bond) and gains another (the reserves or deposits). The result is no change in private sector net financial assets. QE is a lot like changing your savings account into a checking account and then claiming you have more "money". No, the composition of your savings changed, but you don"t have more savings.

5) Cash notes like the ones you have in your wallet are created by the US Treasury and are issued to the Federal Reserve upon demand by member banks. This cash is literally "printed" by the Treasury, but serves primarily as a way for banks to service their customers. In other words, if you have a bank account you can exchange your bank deposit for cash from the ATM or the bank teller. Cash is preceded by the dominant form of money, bank money. But it doesn"t get printed off the presses and fired into the economy as some would have us believe.

Read more at http://pragcap.com/...-the-money-printing-madness#20WxXt3SqiX6qre3.99

Optionen

Optionen

Angehängte Grafik:

image.jpg (verkleinert auf 49%)

image.jpg (verkleinert auf 49%)

Optionen

Truly dark liquidity can be collected off-market in dark pools. Dark pools are generally very similar to standard markets with similar order types, pricing rules and prioritization rules. However, the liquidity is deliberately not advertised—there is no market depth feed. Such markets have no need of an iceberg-order type. In addition, they prefer not to print the trades to any public data feed, or if legally required to do so, will do so with as large a delay as legally possible—all to reduce the market impact of any trade. Dark pools are often formed from brokers' order books and other off-market liquidity. When comparing pools, careful checks should be made as to how liquidity numbers were calculated—some venues count both sides of the trade, or even count liquidity that was posted but not filled.

Dark liquidity pools offer institutional investors many of the efficiencies associated with trading on the exchanges' public limit order books but without showing their actions to others. Dark liquidity pools avoid this risk because neither the price nor the identity of the trading company is displayed.[6]

Dark pools are recorded to the national consolidated tape. However, they are recorded as over-the-counter transactions. Therefore, detailed information about the volumes and types of transactions is left to the crossing network to report to clients if they desire and are contractually obligated.[7]

Dark pools allow funds to line up and move large blocks of equities without tipping their hands as to what they are up to. Modern electronic trading platforms and the lack of human interaction have reduced the time scale on market movements. This increased responsiveness of the price of an equity to market pressures has made it more difficult to move large blocks of stock without affecting the price.[8]

Dark pools are run by private brokerages which operate under fewer regulatory and public disclosure requirements than public exchanges.[9] Tabb Group estimates trading on the dark pools accounts for 32% of trades in 2012 vs 26% in 2008.[9]

Price discovery[edit]

For an asset that can be only publicly traded, the standard price discovery process is generally assumed to ensure that at any given time the price is approximately "correct" or "fair". However, very few assets are in this category since most can be traded off market without printing the trade to a publicly accessible data source. As the proportion of the daily volume of the asset that is traded in such a hidden manner increases, the public price might still be considered fair. However, if public trading continues to decrease as hidden trading increases, it can be seen that the public price does not take into account all information about the asset (in particular, it does not take into account what was traded but hidden) and thus the public price may no longer be "fair".

Yet when trades executed in dark pools are incorporated into a post-trade transparency regime, investors have access to them as a part of a consolidated tape. This can aid price discovery because institutional investors who are reluctant to tip their hands in lit market still have to trade and thus a dark pool with post-trade transparency improves price discovery by increasing the amount of trading taking place.[10]

Market impact[edit]

Whilst it is safe to say that trading on a dark venue will reduce market impact, it is very unlikely to reduce it to zero. In particular the liquidity that crosses when there is a transaction has to come from somewhere—and at least some of it is likely to come from the public market, as automated broker systems intercept market-bound orders and instead cross them with the buyer/seller. This disappearance of the opposite side liquidity as it trades with the buyer/seller and leaves the market will cause impact. In addition, the order will slow down the market movement in the direction favorable to the buyer/seller and speed it up in the unfavourable direction. The market impact of the hidden liquidity is greatest when all of the public liquidity has a chance to cross with the user and least when the user is able to cross with ONLY other hidden liquidity that is also not represented on the market. In other words, the user has a tradeoff: reduce the speed of execution by crossing with only dark liquidity or increase it and increase his market impact.

Adverse selection[edit]

One potential problem with crossing networks is the so-called winner's curse. Fulfillment of an order implies that the seller actually had more liquidity behind their order than the buyer. If the seller was making many small orders across a long period of time, this would not be relevant. However, when large volumes are being traded, it can be assumed that the other side—being even larger—has the power to cause market impact and thus push the price against the buyer. Paradoxically, the fulfillment of a large order is actually an indicator that the buyer would have benefitted from not placing the order to begin with—he or she would have been better off waiting for the seller's market impact, and then purchasing at the new price.[11]

Another type of adverse selection is caused on a very short-term basis by the economics of dark pools versus displayed markets. If a buy-side institution adds liquidity in the open market, a prop desk at a bank may want to take that liquidity because they have a short-term need. The prop desk would have to pay an Exchange/ECN access fee to take the liquidity in the displayed market. On the other hand, if the buy-side institution were floating their order in the prop desk's broker dark pool, then the economics make it very favorable to the prop desk: They pay little or no access fee to access their own dark pool, and the parent broker gets tape revenue for printing the trade on an exchange. For this reason, it is recommended that when entities transact in smaller sizes and do not have short-term alpha, do not add liquidity to dark pools; rather, go to the open market where the short-term adverse selection is likely to be less severe.

http://en.wikipedia.org/wiki/Dark_liquidity

Optionen

Optionen

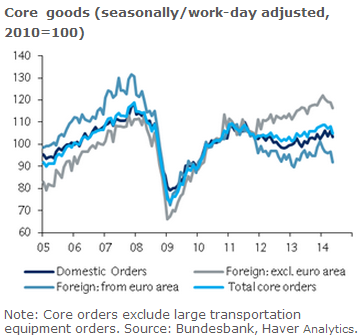

Angehängte Grafik:

core_goods_orders.png

core_goods_orders.png

Optionen

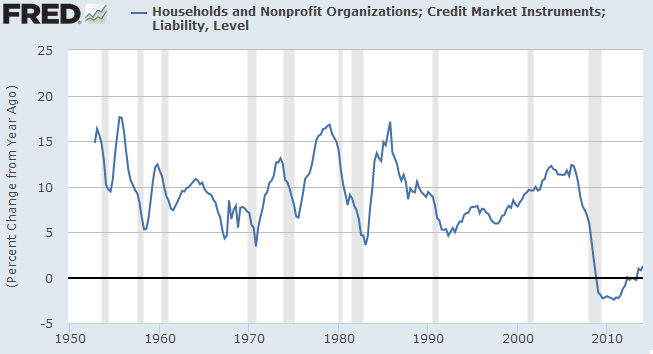

Angehängte Grafik:

cmdebt.png (verkleinert auf 78%)

cmdebt.png (verkleinert auf 78%)

Optionen

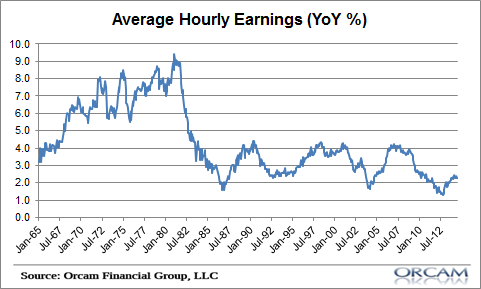

Angehängte Grafik:

ahetpi.png

ahetpi.png

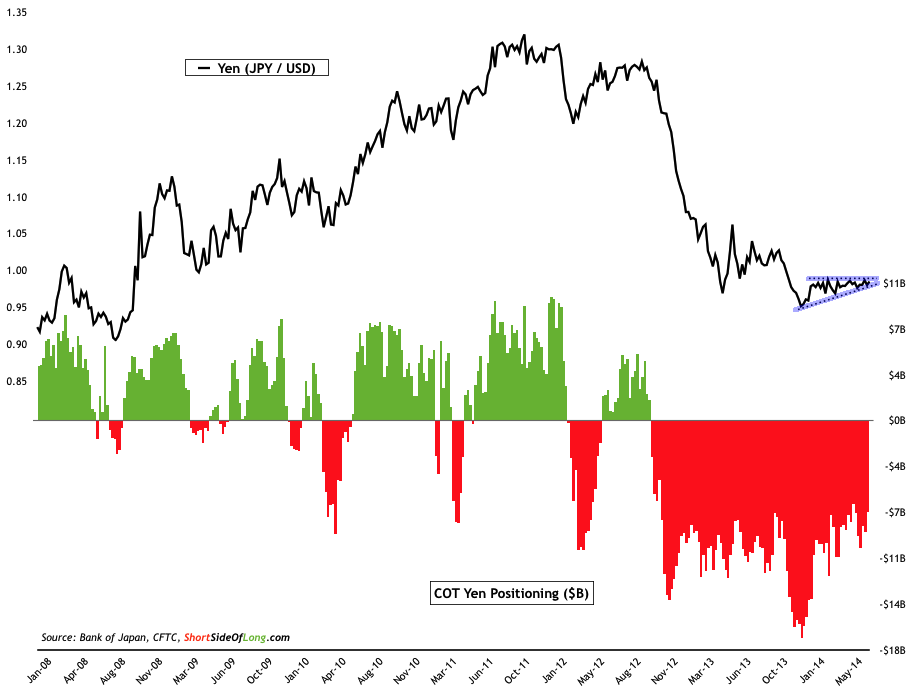

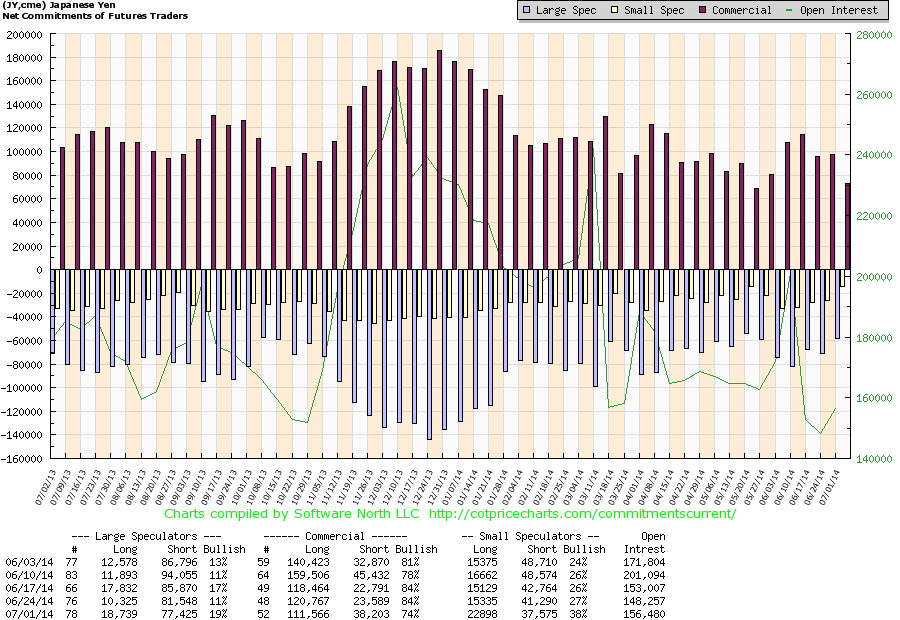

wird - die Spinstory, derzufolge der monetär neutrale Asset-Swap der BOJ den Yen kausal unter Druck setzen soll das Short-Sentiment bei der Stange. Aber es ist nur eine Frage der Zeit, bis irgendwo bei irgendwem der Geduldsfaden reisst. Denke, ich werd mir morgen einen Schein raussuchen...

Optionen

Angehängte Grafik:

japanese-yen-cot.png (verkleinert auf 55%)

japanese-yen-cot.png (verkleinert auf 55%)

Angehängte Grafik:

jy.png (verkleinert auf 56%)

jy.png (verkleinert auf 56%)