der Euro/Dollar Long Thread

Seite 107 von 173 Neuester Beitrag: 25.04.21 10:13 | ||||

| Eröffnet am: | 15.05.04 15:07 | von: börsenfüxlein | Anzahl Beiträge: | 5.304 |

| Neuester Beitrag: | 25.04.21 10:13 | von: Mariejpgpa | Leser gesamt: | 238.203 |

| Forum: | Börse | Leser heute: | 81 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 105 | 106 | | 108 | 109 | ... 173 > | ||||

US-Industrieaufträge im November stärker als erwartet gestiegen

vom 04. Januar 2006 16:40

Washington, 04. Jan (Reuters) - Der Auftragseingang der US-Industrie ist im November stärker gestiegen als erwartet.

Die Zahl der eingegangenen Bestellungen nahm zum Vormonat um 2,5 Prozent zu nach einem Plus von 1,7 Prozent im Vormonat, wie das Handelsministerium am Mittwoch in Washington mitteilte. Analysten hatten mit einem Anstieg um 2,3 Prozent gerechnet. Die Industrieaufträge außerhalb des Rüstungsbereichs stiegen um 3,3 Prozent. Die Industrieaufträge ohne Berücksichtigung des Transportsektors blieben auf dem Vormonatsstand.

YUAN-Aufwertung ist, meiner Meinung nach, die große Unbekannte...da können dann die Würfel mit einem Schlag neu gemischt werden...und wer weiß: ? ; vielleicht wissen ja da einige böse Jungs mit ner Menge Kohle mehr als der Rest und Positionieren sich dementsprechend...

je ne sais pas...

im Grunde hat NRNF sicher recht...starke Supports/Resists suchen und dementsprechend danach handeln...mehr können wir Taschengeldtrader *g* ja sowieso nicht machen...

grüsse

füx

Für mich gesunde korrektur, und ich halte meine Long´s bis 1,225 und erst dann drehen wir.

According to IdeaGlobal currency strategist David Powell, the market had been "starved" of significant economic data -- and of liquidity -- in the last couple of weeks of December, and it seized on Tuesday's deluge of news to shake out long dollar positions.

But the euro, he noted, has not broken out of the $1.16 to $1.22 range it has been in since May of 2005.

"This is not the beginning of a new trend," Powell says. "We knew what the Fed's position had been since Dec. 13," and now the market will take its cues from the data.

For the time being, the dollar still remains supported by attractive yield differentials between U.S. rates at 4.25%, compared with the Europe Union's 2.25%, and Japan's at 0%.

And there's a chance that the dollar may surprise on the upside in the first quarter, should economic data and inflation come in stronger than expected, Powell says.

For the greenback, everything will indeed depend on whether, or rather how much, the U.S. economy will slow. The yields of short-term bonds surpassed of the yields of long-term bonds several times last week, signaling to some that there's economic trouble down the road.

In recent action, the yield of the two-year note stood at 4.31%, while that of a 10-year bond was at 4.36%.

[also keine invertierte Zinskurve mehr! - A. L.]

Quelle:

http://www.thestreet.com/_tscana/markets/marketfeatures/10260077.html

Also absehbares zinserhöhungsende in den usa + weiter steigende zisnen in euroland.

da kann der euro noch ein wenig laufen...

DR87X8

der juri

EUR/USD ist trotz der zahlreichen guten Daten aus der Eurozone in den Bereich von 1,2070 zurückgefallen. Die letzte Veröffentlichung wies einen Anstieg der Auftragseingänge in der deutschen Industrie im November um fulminante 13,5% im Jahresvergleich aus. Zuvor hatten bereits mehrere Stimmungsindikatoren ein deutlich aufgehelltes Bild gezeigt.

Dies erwies sich jedoch als nicht ausreichend, dem ohnehin bereits überkauften EUR/USD-Markt zu weiteren Gewinnen zu verhelfen, so dass Marktteilnehmer die Stopps an der Unterseite ins Visier nahmen. Wenn diese erst aus dem Markt sind, dürfte der Widerstand über 1,2100 leichter zu überwinden sein. Das bullische Bild eintrüben würde lediglich ein Rückgang unter die runde Marke von 1,2000.

Kaufaufträge liegen im Bereich von 1,2050 und 1,2000-20. Bei 1,2100 befinden sich auch Basen von Optionen, die im weiteren Handelsverlauf auslaufen, und bis dahin die Notierungen in Schach halten könnten. Gegen 13:10 Uhr CET notiert EUR/USD bei 1,2088. (th/FXdirekt)

Trotz zahlreicher guter Daten aus der Eurozone (die Auftragseingänge in der deutschen Industrie stiegen im November um sagenhafte 13,5% im Jahresvergleich und mehrere Stimmungsindikatoren zeigten ein deutlich aufgehelltes Bild) hat sich EUR/USD nicht über der Marke von 1,2100 halten können.

USD/JPY wurde zu Beginn des europäischen Handels am Donnerstag verkauft, Gerüchte um die Verteidigung einer Optionsbarriere bei 115,50 und Käufe japanischer Importeure stoppten jedoch die Talfahrt. Unterstützung brachten auch die Kommentare von Hiroshi Watanabe. Dieser hatte die Bewegungen von USD/JPY zum Jahresende 2005 als „derb“ bezeichnet und damit Missfallen des Finanzministeriums signalisiert.

EUR/GBP scheiterte mehrfach oberhalb von 0,6900, wobei der Anstieg im britischen CIPS-Einkaufsmanagerindex auf 57,9 Punkte im Dezember belastete. (th/FXdirekt)

Auf jeden Fall viel Glück!

Vorsicht allerdings, weil der Wert des OS nur aus dem Zeitwert besteht; er ist weit aus dem Geld!. Laufzeit ok. Und wenn der EUR nicht in die richtige Richtung läuft, er nur auf der Stelle verharrt, dann verliert er ständig an Wert. Wenn der EUR weitersteigt - das wäre schlecht. Mit dem Nachkaufen vorsichtig sein (alter Fehler von mir gewesen!).

Mit einem OS der DTE, der weit aus dem Geld war, habe ich mir schon mal ordentlich die Finger verbrannt (darüber gibt es auch einen Thread, aber ist ja Schnee von vorgestern). Wenn man im Verlust ist, und der Verlust wird größer und größer - dann bekommt man irgendwann so was wie Panik, man verkauft entnervt - UND DANN STEIGT DIE SCH.... Alles schon erlebt ... Insofern, wie man es macht, macht man es ....... Man soll aber auch nicht auf andere hören, es sei denn, es sind wirkliche Experten ... Ich bin es (noch) nicht ... Alles ohne Gewähr ...

Gruß Hotte

Was das für EUR/USD für Konsequenzen hätte, ist schwer zu sagen. Momentan bewegt sich das Paar immer noch parallel zu den Aktien-Indizes: Starke Börsen, (relativ) starker Euro. Bliebe es dabei, würde der Dow-Absturz mit einer Dollar-Rallye einhergehen.

-----------------

Market Features

Cult of the Bear, Part I

By Barry Ritholtz

1/5/2006 7:18 AM EST

www.thestreet.com/markets/marketfeatures/10260096.html

As 2006 begins, I'm at the bottom of the barrel, bringing up the rear, and the proverbial low man on the totem pole ... and I'm not talking about being in the doghouse with the Mrs. for excessive partying on New Year's Eve.

Rather, I refer to having the very lowest market prediction -- and by more than 2,000 Dow points (!) -- in the 2006 Business Week market forecasts.

In this column and one to follow, I'll describe my top down, macroeconomic process, and how I derived my improbable forecast. I'll also review some market history and explain how, after all the arguments have been made, these long-term charts reveal the most compelling reason to be cautious on U.S. equities into 2006.

If I were a weatherman, my forecast would be 50% chance of heavy showers --- despite the "sunshine" that greeted investors on the first trading day of 2006.

War Games

As part of their strategic planning, the Pentagon plays out various military scenarios: A land war in Europe, a U.S. invasion of Iraq, a revolution in South America. During the Cold War, Strategic Analysis Simulation was the mother of all war games, modeling nuclear confrontation between the U.S. and U.S.S.R.

These exercises allow for multiple variables and outcomes: Winning was less important than teasing out how different scenarios could unfold. Strategic planners wanted to learn how decisions were made in the field, where surprises may develop, how unforeseen events could cause a "domino effect."

I used similar war-gaming techniques to consider what might happen next year. Only instead of nuclear conflagration, I think about consumer spending, corporate expenditures and hiring. What might happen to real estate prices, and how will that impact other elements? Will the demand for commodities continue to increase? Will Asian growth stay strong? What will Congress do: taxes, spending, deficits, politics? What are the political wild cards? I wonder how inflation will impact all of it, and what the Federal Reserve might do, including the expected -- and the unexpected.

While doing all this war-gaming, one scenario kept coming up repeatedly: The slow-motion slowdown. It starts with the consumer, who after years of spending, finally tires. Soon, it infects corporate revenue and profits. Slowly, it cascades its way across different sectors: housing, durable goods, discretionary spending, entertainment. Eventually, the decay spooks the markets.

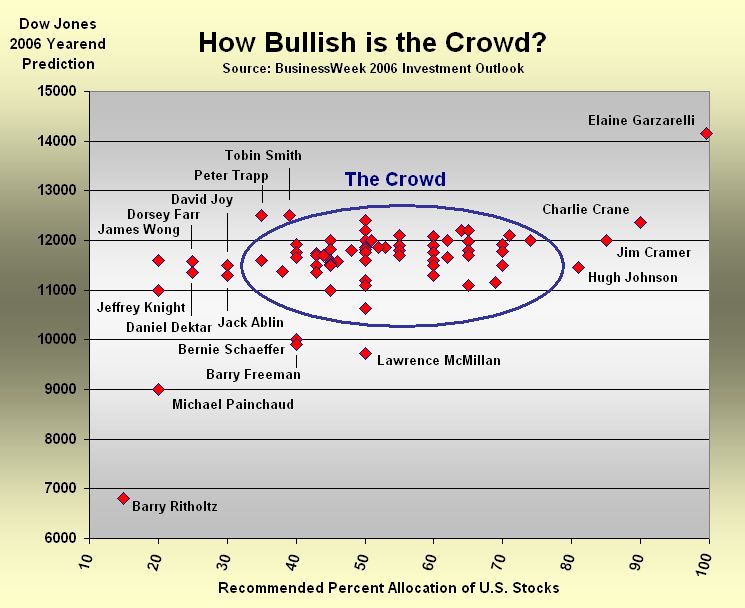

The Crowd Is Bullish

There is a lot of anecdotal chatter about sentiment , but I prefer to stick with quantitative data. I hear too many people say, "All my colleagues/friends/brother-in-laws are (fill in the blank)." That's meaningless.

The Business Week survey reveals one group of bullishness. When I made my guess, I never figured I would be the outlier to the downside. Silly me.

One alternative to conjuring up various scenarios would be to simply extrapolate this year into next. I suspect that's why so many forecasters cluster around the same numbers. Most of the surveyed group is clustered between 11,000 and 12,000 (about plus 5%-10%) on the Dow, while advising a 40% to 75% U.S. equity exposure.

But its not just the Pros: Other surveys reveal a similar bullishness. A WSJ.com poll of more than 5,000 people taken on Dec. 30 shows 46% expect the same thing in 2006 as the market gurus: between Dow 11,000-12,000. Another 12% think we end up at more that 12,000. About 22% expect to end 2006 unchanged. Only 9% expect we will see the Dow between 10,000 and 10,500 -- a mild correction of less than 10%. Just 11% believe the Dow will drop below 10,000.

This means 89% of these WSJ readers do not believe 2006 will be a substantially down year.

Note that the crowd isn't extremely bullish, however. It will take one more rally toward 11,000 to get investors to breathlessly embrace the market. Then the trap door gets sprung.

I understand why the crowd is so bullish. The past few years have seen terrific data points: S&P 500 earnings have grown by double digits for 14 consecutive quarters. Companies are awash in cash; they have been buying back shares at the most rapid rate we've seen since the late 1990s; more than $456 billion worth in 2005, according to TrimTabs Investment Research. Since the dividend tax rate was slashed to 15%, the number of companies issuing dividends has increased, and pre-existing yield-payers have upped their dividends significantly. That's before we get to the record-setting M&A activity last year.

Despite all of these elements, the markets are essentially unchanged. Look at any U.S. index for the past one or two-year period -- or even four or five -- and there's been very little progress made. Except for the pre-Iraq war selloff and subsequent snapback, and the rally from the October 2005 lows, there hasn't been much of a market gain. Aren't you curious as to why that is?

Source: TheMessThatGreenspanMade

I'd be a lot more bullish about prospects for U.S. equities if companies were plowing that half a trillion dollars back into R&D, hiring and spending. Instead, I am bewildered at the dearth of innovation in much of America's corporate suites. (Thank goodness for Google (GOOG:Nasdaq) and Apple (AAPL:Nasdaq) !)

Reality vs. Headlines

I've discussed this repeatedly: The economic data are actually far more discouraging than the headlines would have you believe:

# Unemployment has fallen to 5% primarily due to labor pool dropouts (3.5 million at the peak; now 2.3 million) -- and not a surge of people getting jobs, as detailed here;

# Private sector job growth has been 0.8% since the recession ended. At this point in prior recoveries, job growth averaged about 8.8% -- and has never been less than 6.0% before, according to the Economic Policy Institute.

# Inflation appears more benign than it actually is. Putting aside the foolishness of the "core" rate, the key reason is Owners Equivalent Rent. If housing were appropriately calculated, then CPI would be closer to 5.3%, as detailed here.

# GDP and consumer spending have been propped up by mortgage equity withdrawal (MEW); Typically, MEW accounts for 0.25 to 0.50 GDP points. Over the past four years, the MEW accounted for about 90% of GDP -- between 2.5 and 3.5%, according to the blog Calculated Risk Without MEW, GDP isn't 4.3% -- it's less than 1%.

Big Old Jet Airliner [Schöne Metapher!, A. L.]

Imagine the markets as a four-engine jet. Let's name the four engines M&A, buybacks, dividends and earnings growth.

Our jet is cruising along at ... oh, let's say 10,847 feet. All four engines are at full throttle. Yet for some reason, the plane cannot seem to make any altitude. Every time it gets near 11,000 feet, it seems to stall. Once or twice, it even swoops down to gain some speed but still cannot seem to break that altitude.

Mind you, all four engines are working at peak efficiency, and have been burning high-priced jet fuel prodigiously. The pilot and crew are experienced, and everyone wants the jet to go higher.

Yet it cannot seem to make any upwards progress. Odd, isn't it?

Now consider this: What happens if something goes wrong? What if one of the engines flames out? What if we start running low on fuel? Or if there's a human error? This doesn't mean the plane will plow into the ocean -- but it is likely to lose some altitude.

That's the situation we have found ourselves in. Despite the many positives we have seen in the market, we have been unable to make any progress. And, if any of the positives falter slightly, markets will feel the impact in a big way.

FORTSETZUNG MORGEN (falls Interesse besteht, dann:)

Tomorrow: Long-term cycles, trading ranges, and P/E mean reversion.

Angehängte Grafik:

30101.jpg (verkleinert auf 68%)

30101.jpg (verkleinert auf 68%)