Leser des Bären-threads

Seite 46 von 108 Neuester Beitrag: 25.04.21 00:14 | ||||

| Eröffnet am: | 23.02.08 10:39 | von: Rubensrembr. | Anzahl Beiträge: | 3.691 |

| Neuester Beitrag: | 25.04.21 00:14 | von: Katharinaqtrv. | Leser gesamt: | 366.546 |

| Forum: | Börse | Leser heute: | 29 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 43 | 44 | 45 | | 47 | 48 | 49 | ... 108 > | ||||

stimmt doch oder ???

das ist doch markverzerrung nach oben ...

Le nombre de permis de construire s'est effondré en France au 3e trimestre, chutant de 23,3% à 111.342 unités au cours du troisième trimestre par rapport à la même période de l'année dernière, tandis que le nombre de mises en chantier a reculé de 8,1% à 110.329 unités, selon un communiqué publié mardi par le ministère de l'Ecologie.

http://www.ft.com/cms/s/0/...dd-b4f5-000077b07658.html?nclick_check=1

Angehängte Grafik:

8.gif

8.gif

For nearly 50 years, this world-renowned index has served as the most widely recognized measure of global commodities markets. As a benchmark, the Reuters/Jefferies-CRB Index is designed to provide timely and accurate representation of a long-only, broadly diversified investment in commodities through a transparent and disciplined calculation methodology.

The history of the Reuters/Jefferies-CRB Index dates back to 1957, when the Commodity Research Bureau constructed an index comprised of 28 commodities that made its inaugural appearance in the 1958 CRB Commodity Year Book.

Since then, as commodity markets have evolved, the Index has undergone periodic updates to remain a leading benchmark for the performance of commodities as an asset class.

The Index was renamed the Reuters/Jefferies-CRB Index in 2005 when it underwent its tenth and most recent revision - as the collaborative effort of Reuters, the global information company, and Jefferies Financial Products, LLC - to maintain its continued accurate representation of modern commodity markets.

Angehängte Grafik:

crb_index.png

crb_index.png

Da wird es nicht mehr genügen, daß Paulson, Bush und Bernanke in wechselnder Besetzung und mit ernster Miene an das Publikum treten, wie es bisher immer die Börse beruhigt hat.

Bei Depression noch immer Luft nach unten

Allerdings kursieren wegen der Schwere der Kreditkrise in diesen Tagen auch immer wieder Befürchtungen, die Wirtschaft könne in eine Depression abdriften. Historisch gibt es dafür nur ein Beispiel: In den 30er Jahren, als sich dieses Desaster ereignete, sackte der Dow Jones zwischen 1929 und 1932 insgesamt um sage und schreibe 86 Prozent ab. So gesehen hätte in diesem Negativszenario die Wall Street trotz der bereits erlittenen enormen Verluste noch immer immenses Abwärtspotenzial.

Die Analysten von Ned Davis Research gehen derweil davon aus, dass im Falle einer Rezession ein Bodenbildung nahe sein könnte. Einschränkend heißt es dazu aber auch, dass die Charttechnik mit intakten Abwärtstrends noch keine Entwarnung gebe.

Selbst eine Depression schließt eine temporäre Kurserholung nicht aus

Wer der Situation selbst im Falle einer Depression noch etwas Gutes abgewinnen will, kann aus der Geschichte auch zumindest etwas Hoffnung schöpfen. Das riesige Kursminus der 30er Jahre wurde nicht mit einem Schlag eingefahren. Vielmehr wurde dieser Bärenmarkt von einer zwischenzeitlichen Bärenmarktrallye abgelöst.

Diese dauerte von November 1929 bis April 1930 und bescherte dem Dow Jones ein Plus von 48 Prozent, bevor es anschließend wieder abwärts ging. Wiederholt sich die Geschichte, besteht somit selbst im Falle einer Depression zumindest die Chance auf eine markante Gegenbewegung.

http://www.faz.net/s/...D8D~ATpl~Ecommon~Scontent.html?rss_googlefeed

aufgekauft und den Dax der Lächerlichkeit preisgegeben hätten. Zudem wird

kolportiert, dass Banken wie Goldman Sachs sich beim Shorten verspekuliert

hätten.

Wenn das stimmt, dann wäre das der eigentliche Skandal. Merkwürdiger-

weise regt sich aber keiner darüber auf. Kassierten diese Banken in den

USA doch riesige "Rettungspakete", um anscheinend selbst oder über liierte

Hedge-Fonds weiter ihren Zockergeschäften nachzugehen. Derweil klagt

die Wirtschaft darüber, dass ihr von den Banken nicht mehr ausreichend

Kredit gewährt wird.

Das Schlimme daran ist, dass sich das in Zukunft anscheinend auch nicht

ändern wird. Das hinter den Zockerbuden stehende renditegeile Kapital der

Globalisierungsclique verlangt vermutlich eine Verzinsung, die durch reelle

Geschäfte gar nicht eingefahren werden kann, bleibt also nur Zockerei,

Täuschung und Schädigung der realen Wirtschaft und der Öffentlichkeit

bis zum nächsten notwendigen Rettungspaket.

http://www.mmnews.de/index.php/200810291411/...durch-Zinssenkung.html

see:Commodities Report : Commodities: October 21, 2008 : Commodities [10-21-08 11:30 AM]

* Commodities: October 21, 2008

* October 2008

* Commodities Report

BNN chats with John Embry, chief investment strategist, Sprott Asset Management; and Michael Jones, president and CEO, Platinum Group Metals.

vorspulen aus 11:00 min

http://watch.bnn.ca/tuesday/#clip104603

Read why Galland is supporting gold and silver here:

In all countries and all civilizations, two commodities have been dominant whenever they were available to compete as moneys with other commodities: gold and silver.

At first, gold and silver were highly prized only for their luster and ornamental value. They were always in great demand. Second, they were always relatively scarce, and hence valuable per unit of weight. And for that reason they were portable as well. They were also divisible, and could be sliced into thin segments without losing their pro rata value. Finally, silver or gold were blended with small amounts of alloy to harden them, and since they did not corrode, they would last almost forever.

Thus, because gold and silver are supremely "moneylike" commodities, they are selected by markets as money if they are available. Proponents of the gold standard do not suffer from a mysterious "gold fetish." They simply recognize that gold has always been selected by the market as money throughout history.

Generally, gold and silver have both been moneys, side-by-side. Since gold has always been far scarcer and also in greater demand than silver, it has always commanded a higher price, and tends to be money in larger transactions, while silver has been used in smaller exchanges.

Because of its higher price, gold has often been selected as the unit of account, although this has not always been true. The difficulties of mining gold, which makes its production limited, make its long-term value relatively more stable than silver.

http://www.commodityonline.com/futures-trading/...mmodities-8206.html

© ZEIT ONLINE 29.10.2008 - 12:49 Uhr

Der frühere Berater von US-Präsident Reagan warnt vor einer schweren Wirtschaftskrise in den USA. Sie werde mehr Zerstörung anrichten als jede andere, sagte er der ZEIT

Diese "tiefe und schwere" Rezession, so Martin Feldstein in einem Interview mit der ZEIT, "wird länger dauern als jede andere der Nachkriegszeit". Bereits jetzt befinde sich das Land in einer Rezession.

Angesichts der Krise rief der als konservativ geltende Wirtschaftswissenschaftler die Regierung in Washington zu einem staatlichen Ausgabenpaket zur Stützung der Konjunktur auf. "Wir brauchen zusätzlich ein massives Konjunkturprogramm. Die Präsidentschaftskandidaten sprechen über Programme in Höhe von etwa 60 Milliarden Dollar. Das ist nicht genug", sagte er.

Auch die vielfach angekündigten Steuererleichterungen wirkten dabei nicht, weil die Menschen das zusätzliche Geld sparten. "Wir müssen also sicherstellen, dass das Geld schnell ausgegeben wird. Am besten über öffentliche Ausgabenprogramme."

Der Ökonom kritisierte das Krisenmanagement von Finanzminister Henry Paulson und Notenbankchef Ben Bernanke. "Ich gebe ihnen keine guten Noten. Sie haben zu spät reagiert und teilweise die falschen Dinge getan". Man wüsste doch spätestens seit Mitte 2006, dass die Immobilienpreise irgendwann sinken würden. "Das sind doch alles kluge Leute in den Banken und in den Aufsichtsbehörden. Sie hätten sich rechtzeitig an einen Tisch setzen und nachdenken müssen", sagte Feldstein

>Auch der frühere Notenbankchef Alan Greenspan sei an der Krise schuld. "Die Federal Reserve hat die Zinsen zu lange zu niedrig gehalten. Das hat dazu beigetragen, dass sich am Immobilienmarkt eine Blase gebildet hat. Es geht aber nicht nur um die Zinspolitik. Die Fed - und die anderen Aufsichtsbehörden - hätte diese Blase durch regulatorische Eingriffe bekämpfen, die Kreditvergabe bremsen können."

©

Das vollständige Interview lesen Sie in der neuen Ausgabe der ZEIT. Ab morgen am Kiosk.

http://www.zeit.de/online/2008/44/feldstein-konjunkturprogramm

Gold might fall to $500s: Jon Nadler

Jon Nadler, Kitco’s well-known senior investment products analyst, elicits both criticism and acclaim for opinions that some characterize as contrarian. In this installment of an exclusive interview with The Gold Report, he brings his three decades of experience to bear (no pun intended) on the outlook for gold, promoting the precious metal as a key asset in a balanced portfolio, as well as for its intrinsic value and “insurance” attributes.

Get MCX/NCDEX Gold Futures prices here!

The Gold Report: Economic theory tells us gold should be taking off, given all the uncertainty in the marketplace. But we haven’t seen that happen. What is going on?

Jon Nadler: Well, as you may have heard, even Alan Greenspan found a glitch in his formerly "reliable" economic models during this crisis. Gold certainly will continue to have its volatile days, but the bigger trend is probably more important overall. To a certain extent, the metal got ahead of itself as a legacy of the huge infusion of speculative fund money that came into the commodities complex as a whole, and of course gold is part of that, aside from its role as money. This phenomenon goes back at least two years.

It accelerated last September when the Fed first started to cut rates, and then we got into a position between March and July where the ever-weakening U.S. dollar started things looking like a bubble of major proportion—not just in gold, but in most industrial metals and in oil. It got to the point where oil became so visible that regulators started making all sorts of unpleasant noises toward speculators.

So we saw the exodus from the commodities complex of a good part of that hot money from hedge funds. Of maybe $300 billion that had come in, we don’t quite know how much got up and left. We certainly know that some $50 billion left oil, which had close to $60 billion in it. That’s a significant proportion just sucked out of those markets. Of course, prices collapsed in the wake of that, along with the credit crisis unfolding on the front burner. That piece of the puzzle really didn’t become visible untila few weeks ago, whereas the exit of hedge funds from commodities was well underway back in late June.

TGR: Are we now out of that exit phase?

JN: I think it is continuing because some of the funds simply failed, like Ospraie just last month. Ospraie had a lot of bad bets in oil and gas contracts. We see others with stock positions being wiped out in this debacle. If you have profitable positions in gold or oil, you’re going to be forced to sell them to raise cash to meet your equity margin call. To some degree, that continues. It has wiped some $200 off the gold price in the last 30 days alone.

TGR: If hedge funds and speculators are still exiting, when do you see that flushing itself through and gold reacting more as one would expect, given the financial turmoil?

JN: We may not see that for some time. If deflationary pressures really take hold, we may have a case of “reverse hedge” developing, whereby gold might still fall to the mid-$600s or even as low as the low $500s, but still fall less in percentage terms than other assets might. In that case, investors would still be better off holding some gold and lots of cash rather than equities or real estate and such. Hopefully we don’t head into that deflationary spiral because that could hurt a lot of higher-priced producers of gold. Certainly a lot of the mining companies would have to reconsider what projects to mothball if that happens.

If we don’t go into that vortex and confidence returns by whatever means, things could stabilize. Stability in gold would imply a trading range between $650 and $850. It’s definitely a blow to the doomsday newsletter writers, who thought the circumstances we are seeing now were the ideal scenarios they’d dreamt of as far back as we can recall. They know, however, that the world of $2,000 gold is not one they would want to live in.

The fact that in July gold had trouble surpassing $930, (not even matching the March highs when Bear Stearns failed), was definitely a big wake-up call as to what was going on. And of course what’s going on is that a lot of people had already bought gold starting at $252 and all the way up to $400 and $600. When this big crisis hit, if they spotted their 401(k) accounts off by 38% and their gold holdings ahead by 50% or 60% or much more, it wasn’t a hard decision to make. They liquidated that which was profitable in order to mitigate their losses. That’s why they'd bought their gold to begin with.

So the latecomers, those who were rushing in, having put off their gold purchases until it became a burning issue, basically got caught trying to buy into this “runaway train” scenario. The few people who tried cost-averaging higher-level purchases of $900 to $1,000-plus were the freshest of buyers during these past couple of weeks. The difference we spotted in retail transaction patterns is that this particular cycle in the gold market brought out quite a few sellers, along with new buyers. So there’s very good two-way activity going on in the physical market.

TGR: The gold bullion coins appear to have a very high premium over the gold spot price, so there still seems to be some fear out there, or is it shortages?

JN: Some issues in the physical market are really grossly misinterpreted. Observers are not doing anyone any favors. My perception is that we have a contingent of pundits who are extremely panicked that this is a very poor reaction by gold to the crisis, and it will make them look bad. It already has. Now they’re trying to manufacture this global stampede into gold by panicking investors and by scaring them with stories of supplies running out. No one will argue that there are higher levels of individual investor interest, but it’s nothing “unprecedented.” They’re trying to make it out as unprecedented, and that’s simply not the case. Perhaps it says more about how short a time such pundits have spent in these markets.

TGR: Just how real is the shortage in coins, then?

JN: Specifically, what’s going on with the coins is that most of the mints of the world do not operate on a “produce-then-wait-and-see” basis. They don’t pre-mint hundreds of thousands of coins and put them on the shelf waiting for buyers to materialize. They basically operate on a mint-to-demand policy.

Because of the prolonged bear market in the '80s and '90s, most of them had slimmed down to bare essentials and, in fact, a lot farm out some components of the coin manufacturing process, such as blanking. The U.S. Mint is one of them. They ran into some blank coin quality problems in silver back in March, with about half a million silver blank rejects. That put them behind the production schedules, and when demand indeed kicked in for physical small coins, they were unable to fulfill commitments on a timely basis. This does not mean they ceased production. In fact, most of these mints consider small-item production quite profitable, which implies that they have added shifts, are finding new suppliers of blanks and new refiners for material, and augmenting production to meet the demand. Inventory build-up is one of their top current priorities.

Look back in recent history at the classical gold rushes, if you will. During the first one, in that inflationary period in the late '70s and early '80s, some 16 million Krugerrands were sold globally. The market events of 1987 brought on the next wave of buying, and that is when the U.S. Mint sold more than 1.25 million ounces of gold. Nor should we lose sight of the fact that in the ’91 recession, just a few short years later, they only sold a quarter million ounces. And then we go to about 1999 before Y2K. Again, they suspended sales of certain products like silver rounds, which were being hoarded by people expecting the end of the world. Next would be May of 2006, with the North Korean and Iranian political tensions. Again, very good robust sales, but nothing of the magnitude of ’80 or ’87, and similar to what we’ve had since last year. But at best, I think this year the U.S. Mint will sell about 750,000 or 800,000 ounces. It’s not the level of 1987’s stampede or panic, so I don’t see why they’re trying to make it out to be something bigger than it is.

TGR: Why is there such a premium, though? Just because they’re undersupplied?

JN: Yes, once the retail shops saw the Mint selling coins on an allocation basis, with some restrictions to build up inventories, the retailers started raising premiums on coins that they couldn’t basically get to fulfill previously sold orders. They raised their bids; they also raised their offer. It’s really limited to items like the silver rounds and some of the smaller fractional coins.

But in terms of Kitco getting supplies, basically we took the attitude that if we could not get a commitment from our distributors and suppliers as to a firm premium and/or a delivery date or both, we simply removed the items from the order pages in the online store. Those order pages are limited to items we are confident we can deliver at a decent price within a decent number of days. I know that the list is looking pretty slim, but we do have product to sell, and our pool accounts have never had any shortage of underlying material to secure; namely, 1,000-ounce bars of silver and 400-ounce bars of gold. We continue to offset 100% of all pool account purchases for the peace of mind of our clients.

And we’re adding back a lot of the items that had been removed. For instance, we just got several tens of thousands in gold coins and about a quarter million in silver coins from the Royal Canadian Mint. We’re getting Austrian gold and silver coins in very soon, and I’m sure that the U.S. will restart its sales to distributors once they switch dates on the coins to 2009. This is, coincidentally, the period when mints cease producing old (current year) dating and start with the new ones, and the switchover generally creates a bit of a glitch, too. At any rate, there will be product. We have eggs, thus we will have the omelet as well.

TGR: So it would be prudent to wait a bit.

JN: Absolutely. People are not good consumers if they go out and pay $5 over spot on $10.50 silver just to secure something that they think they’re going to have to barter at the grocery store. First of all, that likelihood is not there. Second, the liquidity of such items for such a situation would be questionable. When the supplies do come out, they will be priced at the previous norm. The Mint is not selling the New Olympic Silver Maple Leaf at more than the $1.50 they normally charge. That means they shouldn’t retail for more than $2.50 anyway. If people want to go on eBay and pay $5—well, as I said, try to be a good consumer.

Another thing some of our clients have done is that if they like a particular price that gold or silver reaches on a given day, they simply lock in that price and buy ounces of gold or silver in the Kitco or Royal Canadian Mint pool accounts, and then plan to take advantage of a conversion to physical coins or bars when their supplies and premiums return to earth. It could be just a matter of a few weeks overall.

TGR: Earlier you suggested that in a deflationary period or one just slightly inflationary, gold might be somewhere in the $500-$600 range. But over the longer term, you think it is more likely to stabilize somewhere between $650 and $850?

JN: I think that’s what we’re looking at in order to reflect current levels of supply and demand, basically make the mining community reasonably happy and keep India buying, which it’s currently not. Anything over $850 is just too much as far as they’re concerned, and they’ve demonstrated that stance for most of this year.

We’re in Indian Festival season and they’re lamenting about very poor sales. We just learned in mid-October, for instance, that the World Gold Council is apprehensive about sales levels of bullion in India, the largest consuming nation of the metal. Not only did they change their gold promotion campaign roughly in June or July, the campaign was switched to something very emotional, with raw appeal to long-standing cultural concepts. They really came down to the nitty-gritty to remind Indians that this is part of their cultural and spiritual life. The previous campaign had a happy, luxurious, light-hearted approach. But more than that, they launched a program whereby people can actually buy gold coins through India’s post offices. It’s a huge distribution network, particularly well-suited to sales in very small increments, such as one gram or five gram coins. They recognize that urban buyers are not very gold-friendly anymore and that rural buyers continue to be the ones looking at gold as an alternate form of savings.

So your little one gram coin for $30 or so provides direct access to a lot of people. It’s a brilliant marketing scheme in terms of convincing the refiners to make small material. I think in part that’s one of the things that delayed supplies from Valcambi, one of the refiners in Switzerland, which is probably trying to focus on ramping up to send a gazillion one gram coins throughout India. Let’s see how it’s received; hopefully all these little grams will add up to something real in terms of overall tonnage. So far, the 800 or 900 or 1,000 tons that experts estimated for India to take from the market this year is definitely not there. It wasn’t there last year; it’s not there this year.

TGR: Any other significant factors at play in that scenario?

JN: Investment demand, robust as it may have been, has really been competing with a fairly healthy supply of scrap metal from secondary sources. In fact, last year it ended up almost a wash, where scrap suddenly had amounted to 1,000 tons in the market and investment was about 1,200 tons. So again, at high prices, gold finds its way into the market and we haven’t seen this sort of global man-in-the-street stampede to gold. It’s still competing with cash at this point, where people are really nervous about what they do with the money they take out of the bank.

TGR: Given that, if we’re looking at gold as insurance against the financial markets and cash, why wouldn’t gold go up? Why would it stabilize around $650 to $850?

JN: By and large it has already proven its insurance attributes by virtue of the fact that it outperformed the S&P just sitting around stable. It basically functions that way. If it stays in the $845 and $945 range, as it has this year—the overshoot was a blip—maintenance of these levels has already enabled those who hold some percentage of gold to mitigate the under-performance of the S&P and the Dow and everything else in their mutual funds. In that sense, it’s certainly done its job. Gold doesn’t need to go to $1,200 or $2,200, as all of the doomsayers were saying, to prove itself. That would be more like proof that something has gone extraordinarily wrong in the global system and it’s a scenario you really don’t want to wish for. Should it come to that, you can pretty much be assured that other assets have totally vanished—not just a major damage hit, but you can write them off. That’s not desirable and the G7 and G12 seem prepared to do anything at their disposal to prevent a scenario where you would see both the Dow and gold at $4,000. That’s not what people are gearing up for, obviously, considering the social disruption and violence and all that it might engender. So stability is preferable.

Yes, I think some things are not going to go smoothly. There will be more pain, and more banks will still fail, and you will have occasional runs and blips where gold takes off out of the gate, but the bigger picture really says that this is about it. There’s no valid reason for it to really go up much, much, higher because a lot of the pressure now is on the deflationary side. With all the money that's been thrown into the system, there are many people expecting a Weimar Republic-style hyper-inflation to become the necessary result. However, as in many previous instances, a lot of this excess liquidity is expected to be mopped up out of the system on an orderly basis when things stabilize.

Among the unknowns, of course, are the effects of de facto partial bank nationalization by the U.S., and issues such as which types of participants will be able to play in the commodity markets, and to what extent. Reading between the lines of what Bernanke said in mid-October, it’s pretty clear that they don’t intend to have asset bubbles going forward because of the pain involved in deflating these bubbles. So I think values will not be allowed to get out of hand once again. I’m not talking about gold price suppression here. Far from it. I’m just saying that asset bubbles in general that make for these kind of outcomes probably will be regulated away, or at least in large part..TGR: So do you see anything pleasant on the horizon?

JN: Not exactly. We can expect another two years of real turmoil in terms of difficulties in GDP and retail sales, and consumer spending. It’s going to be a difficult proposition for the industrial metals to make a good go of it—silver, platinum, palladium—because their primary users are: a) unable to get credit or b) scaling back production on lower expectations of demand or c) like the automakers, who are at best, willing to buy only a little bit for inventory because they still have unsold inventory to address first. We’ve seen copper take a big hit, just based on global demand destruction expectations. Same with oil, which is definitely reflecting the same demand versus supply situation.

TGR: Gold is something that can react on fear. Do you anticipate fear to drive it up?

JN: The way to avoid that is probably to not be focused so much on price performance, because most people ought to be buying gold as the allocation device that it really is, and then mobilize it only when absolutely needed, rather than buying because they think they’ll “make money.” That’s not in the cards, really. If you try to trade these markets, you get chopped up. We’ve seen that clearly. Anybody who has tried to trade these gold markets recently was just chewed up and spat out. It was impossible. When you have to stand in the way of these runaway trains that fund liquidations present, or one-off stampedes that some other funds might present on a given day when they set their mind to buying, that’s just not going to work for the smaller trader. The long-term 10% life-insurance type of allocation is the key here for many.

TGR: What’s your thinking about the U.S. dollar these days?

JN: The dollar still has surprises left in it, obviously, because everybody had called for its demise about a year ago. By March they had also buried it and sang its last rites. And sure enough, after July when push came to shove, a lot of people said, “You know what, okay, I’ll sit on dollars.” And there you had your shortage of dollars.

Not everything is fathomable today. We have elections in the U.S. in November, which could mean some interesting change in the national psyche as to which way we go forward, what programs get put into place, who’s the new Fed chairman or Treasury boss. A lot of questions are still unanswered. One of the fundamentals—one that readers shouldn’t ignore—is that whatever the government has put into motion in recent weeks may take upwards of 14 months to really show up. People expect instant gratification, and part of the wild swings is just frustration. “Where is the immediate result? How come we’re not roaring ahead?” These are not easy-going, fast-result types of processes.

TGR: You offer a logical, level-headed perspective that should be of some comfort to our readers in these highly emotional times.

JN: If I tried to convince you that it’s a one-way street and it can only go that way and buy now, beat the rush, two years from now you might not want to talk to me. I would have lost credibility. It’s not about being right on price forecasts, although I don’t think I’m too far off on those either. It’s not about making hype out of it; at the end of the day that’s really going to smell like you have an agenda. It’s more about seeing what’s going on in the underlying market and gauging the consumers’ pulse.

Jon Nadler, an oft-quoted industry spokesman in financial media worldwide, is Senior Investment Products Analyst for Kitco Bullion Dealers. Jon has devoted some 30 years to the precious metals market and on its related investment products. A graduate of UCLA, he established and ran precious metals operations at major financial institutions (Deak-Perera, Republic National Bank, and Bank of America) and has consulted on marketing and product development issues to government mints, precious metals retailers, and trade and membership organizations such as the World Gold Council.

www.theaureport.com

Peter Schiff - (Former Ron Paul Economic Advisor) Versus Art Laffer (Former Ronald McReagan Economic Advisor) - August 28, 2006 - Peter Schiff [Pimp]

http://www.youtube.com/watch?v=IU6PamCQ6zw

http://club.ino.com/trading/

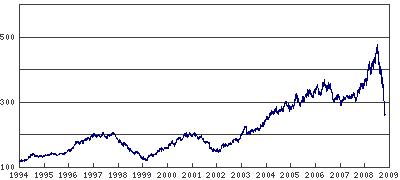

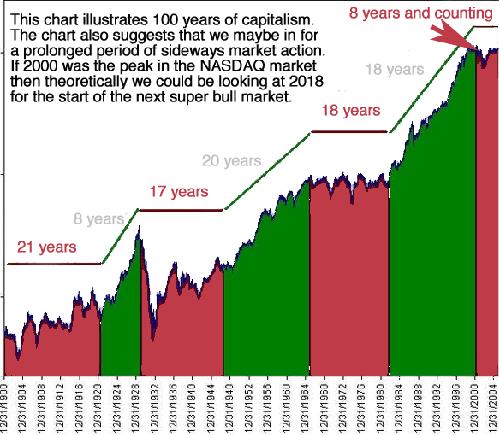

As many baby boomers are facing retirement, this recent meltdown in the stock market has put many in a precarious position. Money they had counted on for their golden years has quickly disappeared and will not likely return anytime soon.

To illustrate this point, a friend of mine recently sent me a chart which I would like to share with you. This charts shows that we may be going into a prolonged period of no growth in the overall stock market. The NASDAQ peaked at 5,132.52 on March 10th, 2000. The NASDAQ market is in many ways more important than the DOW, and should be considered more of a leading indicator. If that is truly the case, then we have been in a bear market for the last eight years.

If many stocks have lost 50% of their value, they must now go up 100% just to get back to where they were. If we are to assume that the stock market grows by 10% a year (and that is not a good assumption), then it’s going to take at least 10 years for many of these stocks to reach the heights they once were at. Many stocks will never come back. I don’t think we will ever see Yahoo trade anywhere close its all time intraday high of $500.13 (set January 4, 2000).

I expect to see a prolonged economic climate that is not conducive for stocks to move higher. However, there will be pockets of opportunity where certain markets and sectors will move higher.

All in all, this is not a rosy picture for either the US economy or the world economy. As I have said many times on this blog, these are trading markets and not markets to hold long-term. Witness our General Motors blog, and the fact that General Motors (NYSE_GM) is a scrambling to either avoid bankruptcy or to find a partner. The latest rumor is that they’re looking at Toyota (NYSE_TM).

Trading throughout the balance of this decade and into the early part of the next decade is going to be the key to survival and for recovering the profits in your portfolio. We strongly recommend that you approach these markets with some level of expertise and knowledge of technical trading.

The future is going to be the future and we need to take advantage of every moment and prepare ourselves to be the very best we can be in whatever business or endeavor we are pursuing.

Angehängte Grafik:

sideway_min_8yrs.jpg

sideway_min_8yrs.jpg

wie lange brauchen wellen bis zu uns???

http://www.iht.com/bin/printfriendly.php?id=17366633

Layoffs sweep from Wall St. across New York region

By Patrick Mcgeehan

Thursday, October 30, 2008

A broad array of businesses across the New York region have begun eliminating jobs by the thousands as the pain of the financial crisis spreads well beyond Wall Street.

Companies as varied as Yahoo, American Express, Time Inc. and Swissport Cargo Services at Kennedy International Airport say they are preparing to lay off employees, including online ad sales representatives, magazine editors and baggage handlers, in the coming weeks.

Economists and labor-market analysts predict that the cuts will be part of a large wave of pink slips that is expected to drive up the city's unemployment rate and strain the state's unemployment insurance fund. In the week that ended Oct. 11 — the latest week for which data are available — New York led all states with an increase of 5,224 first-time unemployment claims.

Law firms are shrinking and publishing companies, which employ about 54,000 people in the city, announced layoffs of about 880 employees this week. Other service businesses, like consulting, catering and tourism, are almost certain to follow suit, said James Brown, who analyzes the city's job market for the New York State Department of Labor.

"The professional fields are going to feel the impact of falling corporate profits," Brown said. "We have a lot of firms in professional services and they sell to corporations nationally and internationally. With corporate profits dropping, their business is weakening. I expect them to start losing jobs soon."

Those cuts would come on top of the layoffs of tens of thousands on Wall Street, which is in the midst of its most wrenching changes in decades.

Despite large cutbacks at some of the city's most venerable banks, city and state unemployment rates have risen only gradually this year, with each holding at 5.8 percent from August to September. But that is expected to change: The number of New Yorkers filing claims for unemployment benefits has been rising at an accelerating pace, in part because layoffs are spreading beyond Wall Street.

In the first nine months of this year, about 60,000 New York City residents collected unemployment checks, according to the Labor Department. That was an increase of about 7,000, or 13 percent, from the first nine months of 2007. Financial services accounted for the biggest share of that rise, but every other sector in the economy also saw increases in unemployment claims. The number of unemployed city residents who used to work in the media, for instance, rose by about 20 percent to more than 2,800, according to the department's figures.

Those numbers did not include the seven employees of Wenner Media, the publisher of Rolling Stone magazine, who were laid off this week, or the 600 jobs that Time Inc. said it planned to eliminate during a reorganization announced on Tuesday. But among them may have been some of the 270 people whose jobs were eliminated in the last three months at McGraw-Hill, which owns BusinessWeek magazine and the Standard & Poor's debt-rating agency.

The digital media, a bright spot in the Bloomberg administration's efforts to reduce the city's economic dependence on Wall Street, may be the next to scale back. Yahoo, which is based in California but has much of its ad sales force in Manhattan, is preparing to eliminate at least 1,500 jobs before the end of the year, the company announced last week. Analysts predicted that some of those layoffs would be in New York, but Kim Rubey, a Yahoo spokeswoman, declined to say how many there would be.

Kevin Ryan, the chief executive of Alleycorp, which owns six start-up online companies, said that even a relatively robust industry like his would have to cut back if the downturn is prolonged.

"Almost every industry's going to be impacted," Ryan said. "There will be less financing available. Already, a lot of conversations about consolidation are happening. I think it's going to happen pretty rapidly."

The traditional advertising agencies of Madison Avenue, he said, are due for some significant layoffs because of the faster decline of printed publications. But much of that cutting might be put off until after the busy fourth quarter.

"The interesting moment's going to come early next year" in the advertising and retail businesses, Ryan said. "I think a lot of it's going to come in January."

The outlook for the metropolitan area has darkened quickly in the last several weeks. Moody's Economy.com, a research firm, raised its projection of job losses in financial services by two-thirds this month, to 100,000 from 60,000, which, it said, would put the region into recession before the end of the year.

In recent weeks, each new forecast of the fallout has been bleaker than the one before. Two weeks ago, the office of the city comptroller raised its estimate of job losses on Wall Street to 35,000 from 25,000. On Tuesday, Governor David Paterson raised the estimate again, to 45,000, and projected that the state's unemployment rate would climb to 6.5 percent. He also said his administration was projecting that the state would lose 160,000 private sector jobs by the end of next year.

On Wednesday, Governor Paterson told Congress that the state expected 90,000 laid-off workers who have been out of work for six months to exhaust their 13 weeks of additional emergency benefits by Dec. 31.

So far, investment banks, brokerage and other securities firms have accounted for almost all of the jobs lost in financial services in the city. But that, too, is about to change. American Express, the giant credit card company, has been hinting that a large layoff would be part of a restructuring plan that it expects to unveil in the next few weeks. A spokeswoman for the company, which is based in Lower Manhattan, declined to say how many of the layoffs would be in the metropolitan area.

While the number of jobs in all professional services in the city was still higher last month than it had been a year before, the legal business is smaller than it was a year ago, Brown said. Law firms are suffering from the sharp drop in transactions on Wall Street, as well as the softening real estate market, Brown said.

Heller Ehrman, a firm with a big presence in Manhattan (with Lehman Brothers as a client), went out of business this month. This week, the managing partners of Thelen, a law firm with about 300 employees in New York, recommended that the firm be dissolved by the end of next month. A spokesman said approval of the shutdown was a "formality."

At Kennedy International, Swissport is considering eliminating 97 of 128 jobs in its baggage-handling operation by the end of next month because of the impact of the slowing economy on airline traffic, according to documents filed with the state labor department. Swissport, which is based in Zurich, handles luggage for several airlines at Kennedy, said Stephan Beerli, a spokesman for the company. Beerli declined to discuss details of the layoff plan, saying that no "official" notice had been given to employees.

"We are right now in a phase where everybody's preparing contingency plans," Beerli said.

http://www.faz.net/s/...796E0~ATpl~Ecommon~Scontent.html?rss_finanzen

In the first nine months, the city's exports bound for the United States, where the ongoing global financial crisis started, grew only 11.6 percent, a decline of 12.9 percentage points from the same period last year. Growth of exports to Hong Kong also slowed to 6.3 percent, down 18.3 percentage points.

But exports to emerging markets including countries in the Association of Southeast Asian Nations and Latin America jumped 30.8 percent and 41.9 percent respectively.

http://news.xinhuanet.com/english/2008-10/30/content_10279486.htm

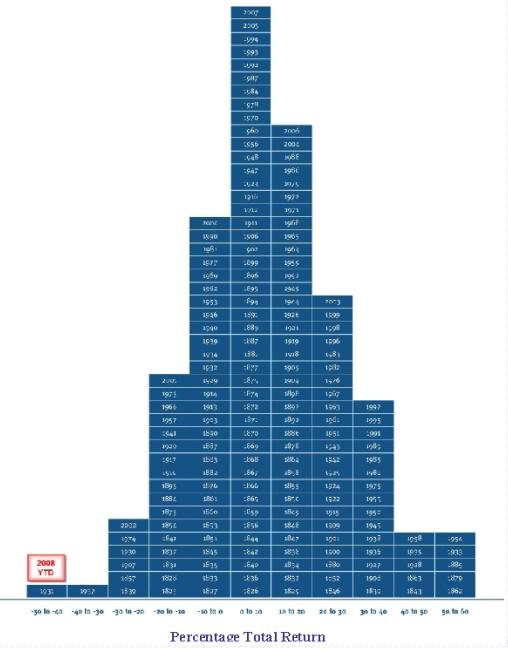

http://www.investmentpostcards.com/2008/10/30/...-1825-to-2008/print/

Angehängte Grafik:

s_p_index_from_1825_to_2008.jpg

s_p_index_from_1825_to_2008.jpg

Mittwoch, 29. Oktober 2008

Die Zentralbank sorgt per Zinssenkung, wie seit Greenspan üblich, für eine neue Blase. Wahrscheinlich die letzte vor dem Untergang des Finanzsystems US-amerikanischer Prägung.

Kommentar der Börsen-Zeitung

Es kommt einem ja irgendwie bekannt vor: Eine geplatzte Asset-Preis-Blase, global einbrechende Aktienkurse, die amerikanische Wirtschaft droht abzuschmieren - und die US-Notenbank Federal Reserve (Fed) senkt den Leitzins auf 1%.

So wie die Währungshüter um Fed-Chef Ben Bernanke den Schlüsselzins gestern erwartungsgemäß um 50 Basispunkte gesenkt haben, schleuste das Gespann um Bernankes Vorgänger Alan Greenspan das Zinsniveau im Juni 2003 ebenfalls auf nur 1 Prozentpunkt oberhalb der Nulllinie herab.

Damals war es eine Reaktion auf die geplatzte Dot-Com-Bubble und die Verschärfung der Finanz- und Wirtschaftskrise nach den Terroranschlägen vom September 2001. Derzeit sind die US-Immobilienkrise sowie der Beinahe-Zusammenbruch des globalen Finanzsystems nach der Lehman-Pleite im September dieses Jahres die Auslöser der Krise.

Angesichts dieses Déjà-vu-Erlebnisses überraschen die Bewertungen kaum. Die Börsen reagieren - mit zeitlichem Vorlauf - zunächst erfreut. Stabilitätsorientierte Ordnungspolitiker warnen dagegen, dass mit der radikalen Zinssenkung bereits die nächste Spekulationsblase genährt werde.

Wer aber hat recht? Keiner von beiden. An den Aktienmärkten wird bald Ernüchterung einkehren, weil die Zinssenkungen der Fed verpuffen, solange der Bankensektor nicht wieder in die Spur zurückfindet und die Talfahrt am Immobilienmarkt endet.

Aber auch die Anhänger der Hypothese der liquiditätsgetriebenen Spekulationsblasen irren. Nicht die Reaktion der Fed auf die Blasenimplosion des Jahres 2001 hat die Immobilien-Hausse ausgelöst. Die laxe Kreditvergabepraxis an Gläubiger schlechter und schlechtester Bonität wog schwerer.

Aber selbst wenn man für das Liquiditätsargument empfänglich ist, waren es nicht die Zinssenkungen, die die Krise heraufbeschworen haben, sondern das zu lange Festhalten am niedrigen Zinsniveau, nachdem sich die Wirtschaft schon wieder auf dem Wege der Besserung befand. Für die Beantwortung der Frage, wann die Zinsen wieder erhöht werden müssen, ist im jetzigen Zyklus noch viel Zeit.

Die Krise hat das Zeug, das Finanzsystem und die Realwirtschaft über Jahre zu schwächen. Die Geldpolitik kann derzeit dagegen nur sehr wenig ausrichten. Das Einzige, was sie tun kann, ist, dem System billiges Geld zumindest anzubieten. Der Schritt der Fed war daher ohne Alternative.

http://www.mmnews.de/index.php/200810291419/...m-letzten-Gefecht.html

http://www.ftd.de/boersen_maerkte/aktien/...ose-drastisch/432558.html

Von Thomas Göhler

Donnerstag, 30. Oktober 2008

Sicher kennen Sie die Geschichte vom tapferen Schneiderlein, welches mit seiner Fliegenklatsche Sieben auf einen Streich erwischte. Offenbar geht dieser Handwerker verstärkt im Finanzsystem auf Beute.

Während in der letzten Oktoberwoche gleich 6 Banken auf einmal „gerettet“ werden mussten ( beachte Orwellschen Neusprech: „gerettet“ hieß früher „pleite“), so gab sich der Schneider im Oktober nicht mehr damit zufrieden, sondern schlug nun in einem Monat gleich bei Staaten zu (ich habe bis heute 11 gezählt), welche „gerettet“ werden müssen.

Gerade nimmt sich unser Schneider eine neue Herausforderung vor: Währungen. Dabei hat er schon den Blick auf eine weitere Fliegenart: Versicherungen und Hedgefonds. Er steigert sich in seinem Gemetzel immer weiter hinein und wird in einigen Monaten nur noch wahllos um sich schlagen und keiner ist mehr vor ihm sicher. Ich denke, wenn er sich erst größere Firmen vor nimmt, benötigt er weitere Gesellen.

Aber eines verschont er noch, um die Spannung zu erhalten: Staatsanleihen. In diese retten sich derzeit Anleger. Dabei kommen diese nun auch verstärkt in Not, da durch die vielen staatlichen Rettungspakete nun eine Überzahl an Bonds auf den Markt kommen, was sozusagen zur Inflation dieser Anlageform führt. Die Folge sind schnelles Absinken der Attraktivität und wieder Flucht aus diesen, was die jeweiligen Länder weiter destabilisieren wird. In den vergangen Wochen haben sich diese Auswirkungen schon durch fallende Renditen und sinkende Kurse bemerkbar gemacht, wie auch das Handelsblatt berichtete. So kauft ja auch die US-Notenbank verstärkt solche auf (2007 nahm die FED bereits 20% dieser in Gewahrsam). Sie kann diese auch noch recht leicht hoch einkaufen, was das AAA-Rating noch einige Zeit erhält. Das wird aber mit fortschreitender Inflationierung dann zu einem zügigen Absturz führen.

http://www.mmnews.de/index.php/200810301420/...res-Schneiderlein.html