against all odds

Seite 77 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 337.187 |

| Forum: | Börse | Leser heute: | 9 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 74 | 75 | 76 | | 78 | 79 | 80 | ... 117 > | ||||

The Constitution of the United States, drafted in the summer of 1787 in Philadelphia by some of the smartest men on this side of the Pond, proves this to be true. In that cherished document, the Founding Fathers demanded socialism. Section 8 of Article I, for example, empowers Congress "To establish Post Offices and post Roads." That same Section also authorizes Congress "To raise and support Armies," and even "To provide and maintain a Navy." Although the text does not preclude privatization of these public institutions — indeed, they continue to include entrepreneurial elements to this day — the Framers understood that they would certainly have public, social elements as well. Alexander Hamilton, James Madison, George Washington, Benjamin Franklin, and John Adams — among others — all signed this document. They agreed that the new national government would facilitate communication and defense through taxation. They agreed that these essential services would not have to be purchased on the open market. They agreed that these services would not be limited to those who could pay fair market value.

The author of the Declaration of Independence, Thomas Jefferson (who skipped the Constitutional Convention in favor of traipsing off to Paris during that hot summer in 1787), also supported the fledgling Nation"s foray into socialism. Perhaps the greatest of all of America"s socialized institutions, the Nation"s modern highway system, was begun in 1806 by then-President Jefferson"s authorization of the Cumberland (National) Road. Transportation, too, was deemed to be one of the Nation"s essential services that could not be relegated to private industry.

The Congress did President Jefferson one better. It socialized the great bulk of America"s navigable waterways in the late eighteenth and early nineteenth centuries. The founding generation recognized early on that the national government needed the power regulate interstate commerce—this was written into Article I of the 1787 Constitution—and waterways provided the most important channel of commerce. The national government, using this authority, opened America"s internal waterways to commerce. These immense "social" highways proved a boon to entrepreneurial activities (and perhaps saved the Nation).

Communication, transportation and mutual defense provide only the most obvious examples of the Founding Father"s interests in socialized institutions. Contrary to some popular reports, many in the founding generation had "republican," communitarian leanings. Our forefathers were not devout disciples of Adam Smith, let alone Herbert Spencer (who in the mid-nineteenth century infamously coined the phrase, "survival of the fittest"). They were pragmatists, capitalists and socialists, willing to try whatever was necessary to insure that the American experiment did not fail...'

http://jurist.law.pitt.edu/forumy/2009/10/...ist-founding-fathers.php

Optionen

Traditional decision theory distinguishes between risk and uncertainty. With risk, the probabilities of possible outcomes are known; with uncertainty, those outcomes are known, but not their probabilities. We introduce the concept of ignorance, a third, less tractable category. With ignorance, even the possible outcomes cannot be identified. Ignorance takes importance when high payoffs are associated with the unidentified outcomes. Thus we focus on consequential amazing developments, or CADs.

CADs spring upon societies as well as individuals. In the policy realm, the 2008 financial meltdown and the Arab Spring would represent CADs, major unanticipated events. For an individual, a CAD might be the discovery that a faithful spouse of many years has a secret second family, or that our trusted business partner has been pilfering corporate secrets all along. Authors depict the implications of consequential ignorance in some of the greatest of literary works: Hamlet’s ignorance of his father’s killer, Macbeth’s unawareness of outcomes when he attempts to seize the Scottish crown, Odysseus’s journey back to Ithaca involving a series of consequential adventures, all unknowable.

Consequential ignorance cannot be studied in a controlled laboratory setting, since its payoffs are high, its time delays often long, and merely introducing the subject tends to give away the game. Thus we study ignorance through great works of literature, from antiquity to the present day, positing that great writers understand how humans make decisions. We distinguish between unrecognized and recognized ignorance. In the latter category, we identify specific cognitive biases at work. We provide a formula for calculating consequential ignorance that incorporates the expected magnitudes and assessed base rates for CADs. Finally, we propose steps towards measured decision making under ignorance.

https://research.hks.harvard.edu/publications/...Id=9136&type=WPN

Optionen

Optionen

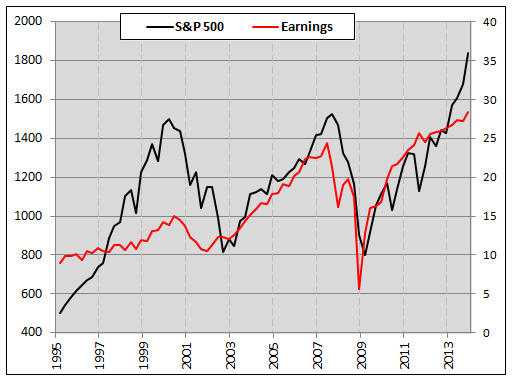

Angehängte Grafik:

spx-vs-corporate-earnings-historical-performance-....png (verkleinert auf 99%)

spx-vs-corporate-earnings-historical-performance-....png (verkleinert auf 99%)

Optionen

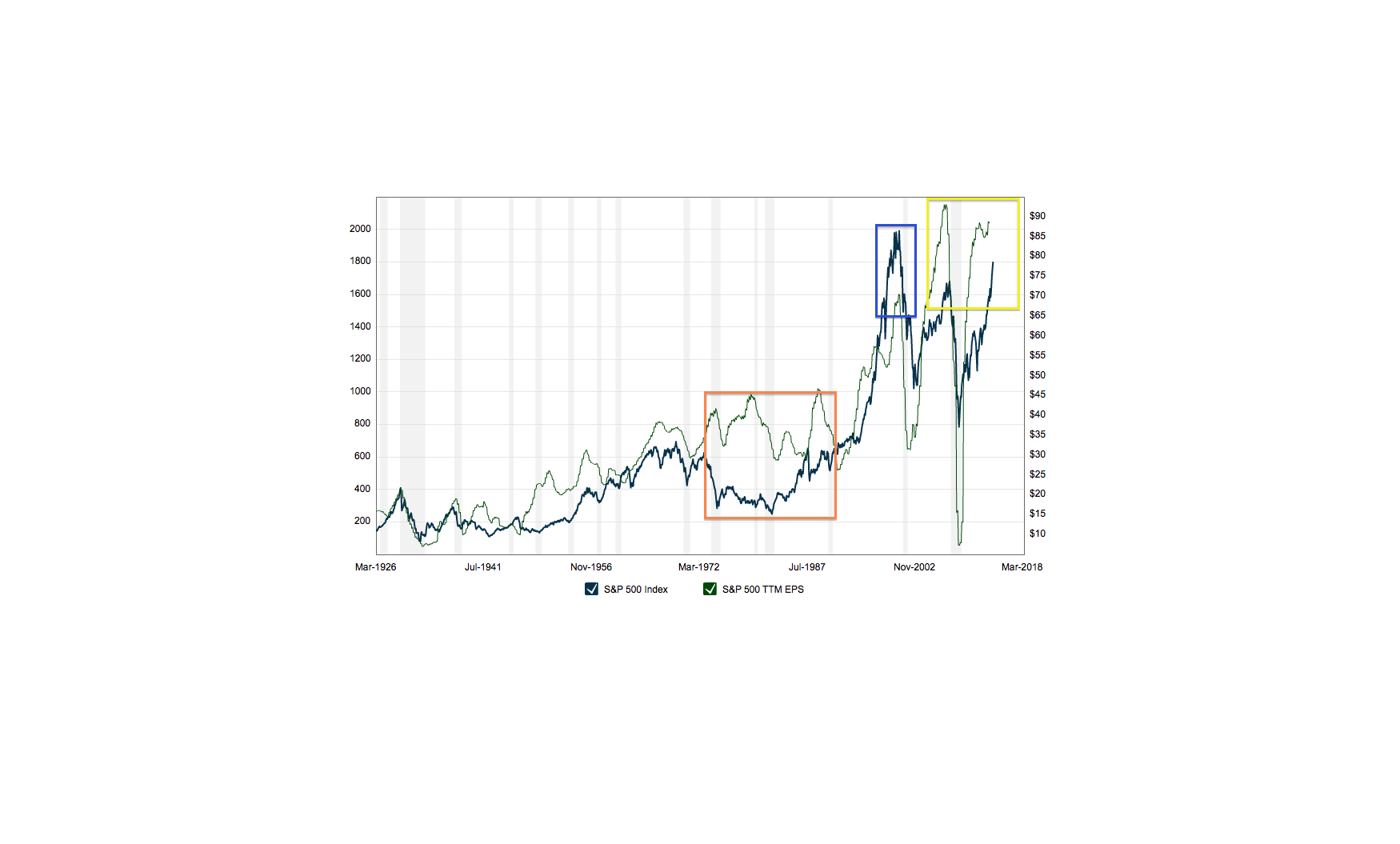

Angehängte Grafik:

nyse-margin-debt-spx-growth-since-1995.gif (verkleinert auf 56%)

nyse-margin-debt-spx-growth-since-1995.gif (verkleinert auf 56%)

Das werden wohl feuchte Bullenträume bleiben! Armer lehna!

Angehängte Grafik:

earnings.png (verkleinert auf 29%)

earnings.png (verkleinert auf 29%)

Optionen

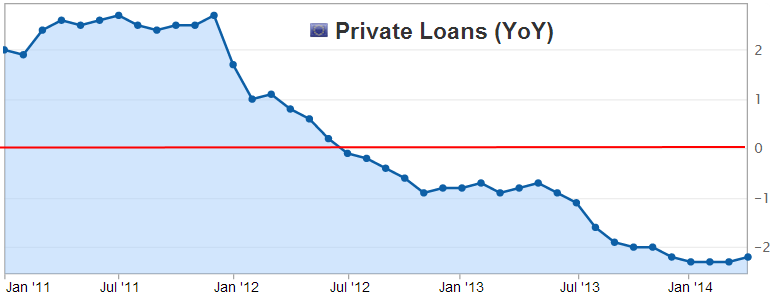

Angehängte Grafik:

private_loans.png (verkleinert auf 65%)

private_loans.png (verkleinert auf 65%)

Daraus folgt, dass die Bewegung der Margin Debt keinen Indikator für ein kritisches Niveau up- oder downside stellen kann. Jedenfalls nicht viel mehr als ein Kursindex selbst, denn steigende Kurse fallen notwendig mit einer Kreditexpansion zusammen (und umgekehrt). Es gilt nur grundsätzlich: Je höher die Kurse laufen, um so grösser das Rückschlagspotential - eben weil dann ein entsprechend grosses Kreditvolumen rückabgewickelt wird...

Optionen

da hätte sich der ek aber schön senken lassen... abprall von der ema 200 und mit schwung, das geht ja nun mal gern noch ein paar tage oder wochen so weiter, wenn die das machen...

ariva-sentiment ist mittlerweile wieder strong long, nachdem es letzte woche deutlich short unterwegs war... immerhin...

Optionen

Optionen

einen wunderschönen sommertag wünsch ich... bin am vertikutieren, meine nachbarn mögen es mir verzeihen.

Optionen

Optionen

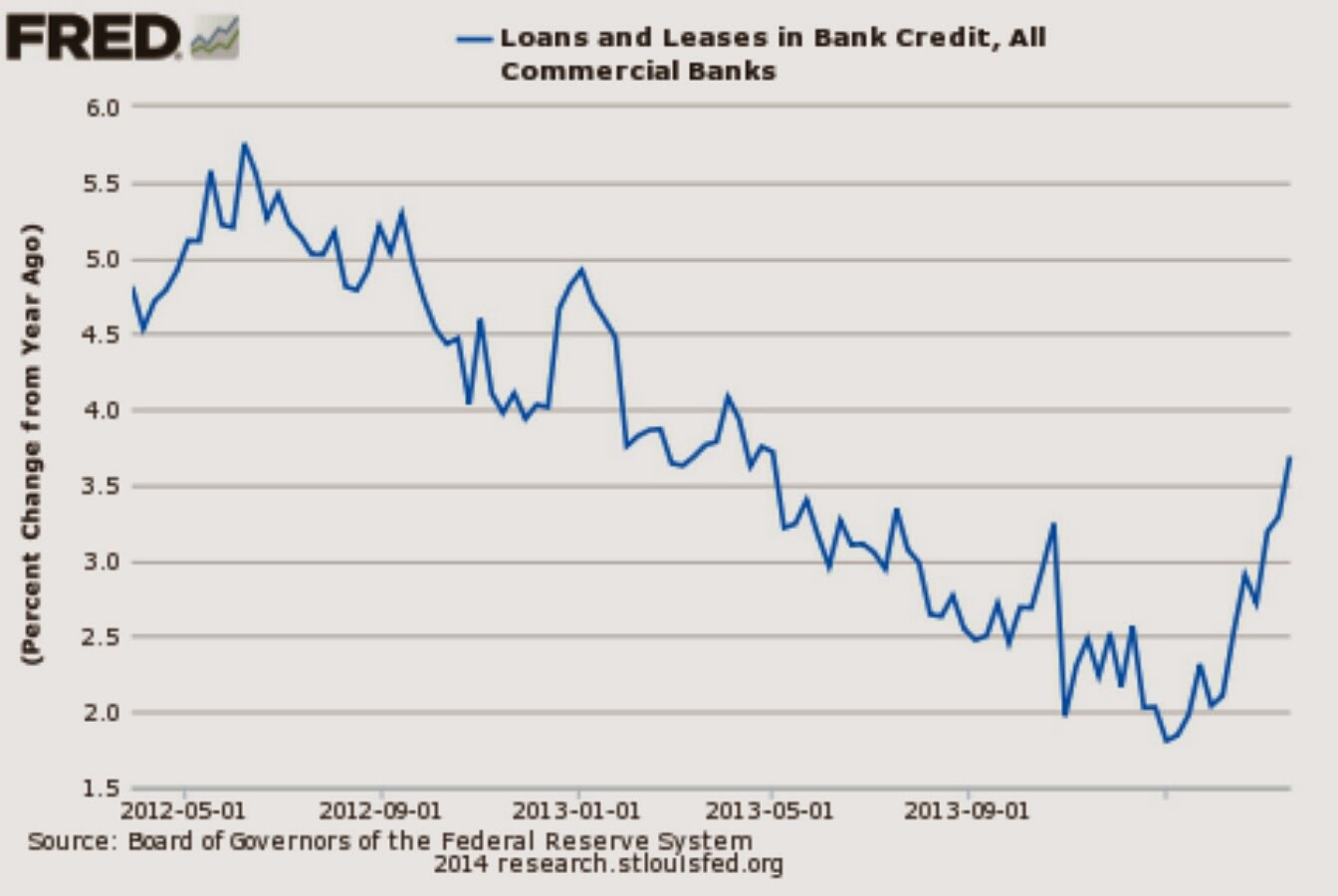

Angehängte Grafik:

loans_and_leases.jpg (verkleinert auf 37%)

loans_and_leases.jpg (verkleinert auf 37%)

(1) classical loanable funds theory, with time preference explaining the interest rate;

(2) Wicksell’s natural rate of interest;

(3) neutral rates of interest;

(4) rational expectations;

(5) the belief that real world market economies can be modelled with single representative agent models where agents maximise utility;

(6) Ricardian equivalence;

(7) belief in a real world tendency to general equilibrium;

(8) belief that money is neutral (whether in the short or long run, or in the long run);

(9) the quantity theory of money;

(10) the law of demand as a universal law;

(11) the law of diminishing marginal utility as a universal law;

(12) the law of diminishing marginal productivity;

(13) the belief that firms equate price with marginal cost or move price towards marginal cost;

(14) the belief that agents maximise utility in the neoclassical sense;

(15) the belief that involuntary unemployment is fundamentally caused by inflexible wages.

(16) the idea that macroeconomics needs rigorous microfoundations.

(via Lord Keynes)

Optionen

fillorkill am 02.08.13

wie war das noch mit dem beige book und dem terminus weather? als saisonale schwäche weggewunken...

Optionen

Optionen

mein bärenherz sagt also: gute prognose, wie immer, fill.

gruß