against all odds

Seite 107 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 342.383 |

| Forum: | Börse | Leser heute: | 32 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 105 | 106 | | 108 | 109 | ... 117 > | ||||

http://www.tradingeconomics.com/united-states/corporate-profits

Optionen

Angehängte Grafik:

united-states-corporate-profits.png (verkleinert auf 69%)

united-states-corporate-profits.png (verkleinert auf 69%)

Optionen

Angehängte Grafik:

united-states-private-sector-credit.png (verkleinert auf 69%)

united-states-private-sector-credit.png (verkleinert auf 69%)

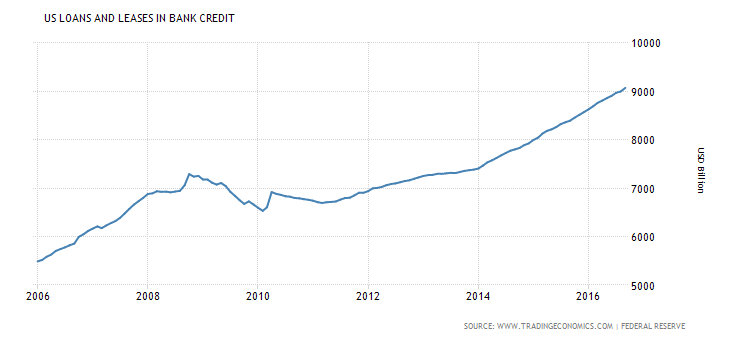

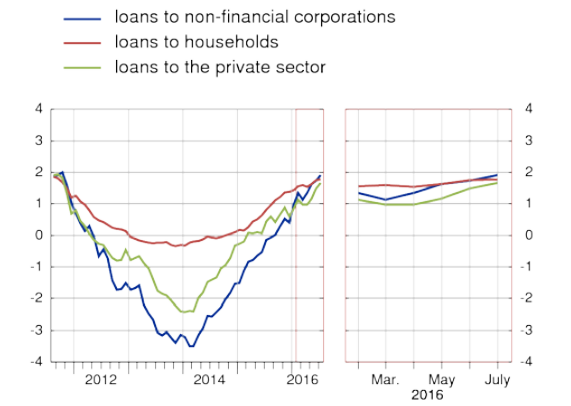

Bezogen auf den US-Markt sehen wir unter 1. eine sich moderat entwickelnde Blase im privaten Kredit, wobei beide Sektoren - Consuming und Business Investing - anziehen. Das Consumersentiment scheint 2. weitestgehend reif, es fehlt aber noch ein fröhlicher Schlenker nach oben, während Investoren sich im Sentiment wie gehabt per saldo neutral bewegen. Die Wachstumskennziffern tendieren 3. nachwievor moderat, während die Earnings zumindest nicht weiter toppen können. Der anziehende Privatkredit hat 4. noch keinen konstanten Upmove der Zinsen nach sich gezogen, auch wenn der auf der Symbolebene bereits vorbereitet wird.

Optionen

Optionen

Angehängte Grafik:

neg_yielding_bonds__chart_bloomberg__oct_18....png (verkleinert auf 52%)

neg_yielding_bonds__chart_bloomberg__oct_18....png (verkleinert auf 52%)

Optionen

Angehängte Grafik:

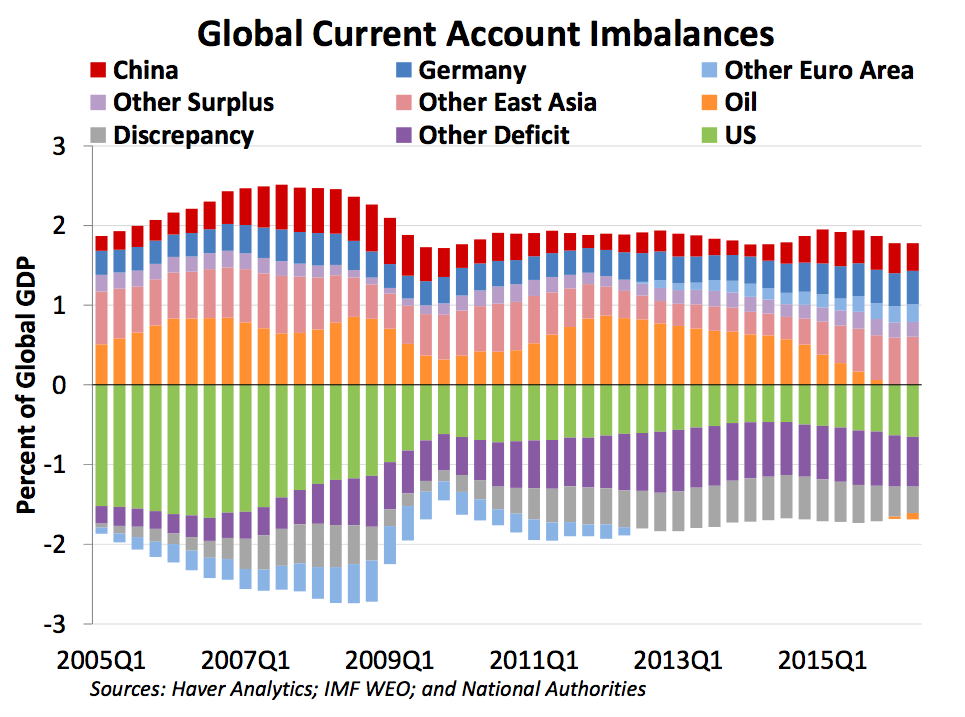

global_ca_imbalances__chart_ust_oct_2016_rep....png (verkleinert auf 52%)

global_ca_imbalances__chart_ust_oct_2016_rep....png (verkleinert auf 52%)

Optionen

Angehängte Grafik:

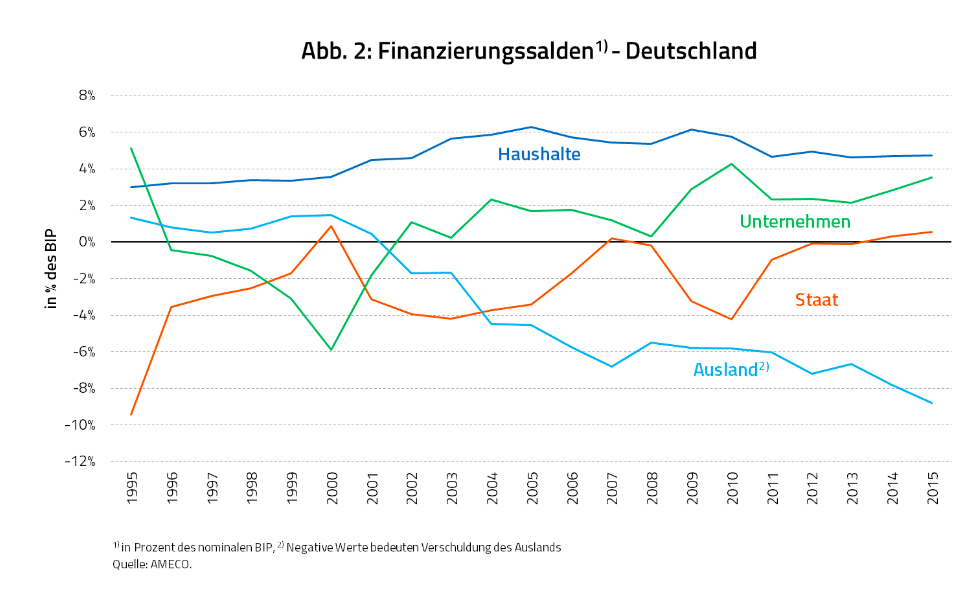

sectoral_balances_in_ger__chart_heiner_flassbe....png (verkleinert auf 52%)

sectoral_balances_in_ger__chart_heiner_flassbe....png (verkleinert auf 52%)

Optionen

Angehängte Grafik:

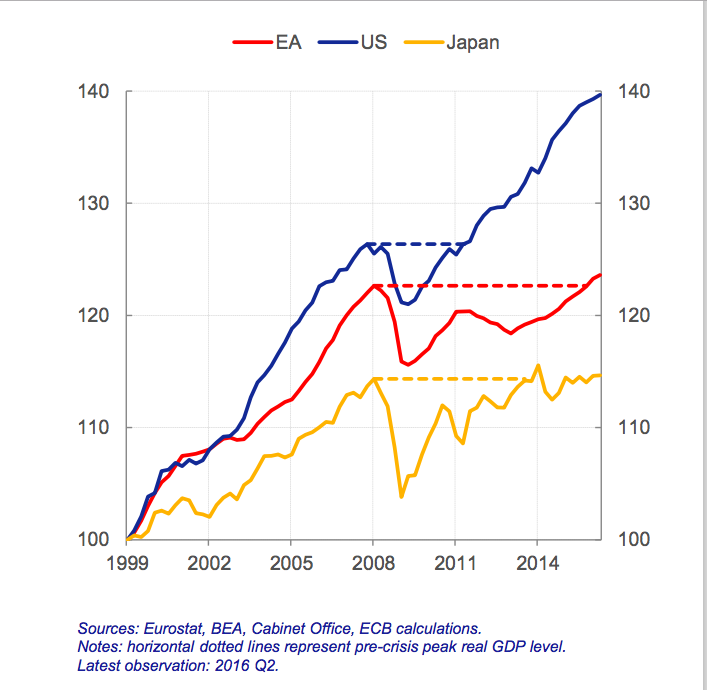

real_gdp_ea__chart_peter_praet__ecb__oct_6_....png (verkleinert auf 72%)

real_gdp_ea__chart_peter_praet__ecb__oct_6_....png (verkleinert auf 72%)

Optionen

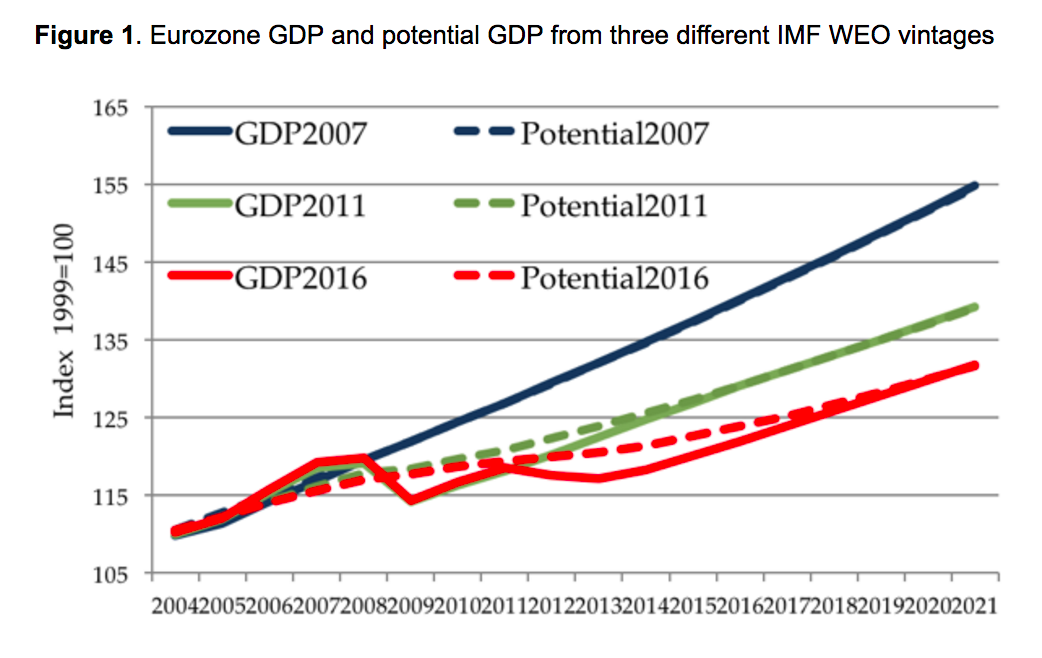

Angehängte Grafik:

ea_gdp_and_potential_gdp__chart_antonio_fata....png (verkleinert auf 48%)

ea_gdp_and_potential_gdp__chart_antonio_fata....png (verkleinert auf 48%)

Dieser zwiespältige Mix lanciert dann jenes übergeordnet pessimistische und bei Anlass sofort auf Krise gebürstete Sentiment unter Investoren, dass den Seitwärtsmarkt so stabil im Takt hält. Damit wäre nun auch klar, was zum nächsten grossen Bärenmarkt fehlt, nämlich ein Reboot insbesondere der Eurozone. Für diesen gibt es Anzeichen...

Optionen

That was one of the statistics tracked weekly by the Federal Reserve... The only people waiting in line at the Fed were a few messengers from the newspapers and some banks. Virtually no one else was interested in the currency in circulation. When we saw the number, we were shocked!

It had surged far beyond anything we had imagined. That was Thursday night. Roosevelt’s inauguration was going to be Saturday morning. We went home, plotted it on the chart and planned our strategy.

...Most people might think that a bank holiday — easily the worst financial crisis in modern history — would be the harbinger of a further stock market decline and a signal to sell. We felt it was exactly the opposite. We believed that it was the climax of the whole deflation since 1929. The new President would have no choice but to close the banks, inflate the economy and pump up the stock market. Besides, at these low prices, major blue chips had great value. We had no intention of selling short. Our sole purpose was to buy. The next morning...

http://www.moneyandmarkets.com/...iumph-of-contrarian-investing-48652

Optionen

Angehängte Grafik:

image1.jpg

image1.jpg

1. Anecdotes. If you pay a lot of attention to specific stories and examples, give yourself -3. Illustrations can add color to conclusions, but when used as the basic level of analysis if is too easy to find supporting narratives.

2. Specific examples. Similar to #1 but probably even more common. How do you interpret information during earnings season? If you pay a lot of attention to news reports on specific companies, give yourself -3. (It does not matter whether the stories are positive or negative; -3 either way).

3. Symbols. If you find yourself drawn to colorful or graphic symbols of events – new paradigm, stall speed, stagnation, or anything similar pointing in any political direction – give yourself -2. If you completely reject analysis of data, take an additional -2.

4. Demonstrably biased data. Examples are things like ShadowStats, where there has been compelling and responsible refutation, without response, on several occasions. Or like the idea that over 90 million people in the U.S. are without work. There is a legitimate debate about some data, but a general rejection of this type indicates a preference for conclusions before evidence. Take -2 if you find these arguments credible.

5. Emphasizing unimportant data. Choosing to use data rather than stories is a good step. The problem is that there are so many indicators, and most of them have little significance. If you are looking at the Markit PMI (for Europe, China, or the U.S.), or regional diffusion indexes like Empire or Dallas, give yourself -1. There are so many of these that you can find anything you want, and none of them are established as really important.

6. Embracing biased interpretations. This happens so frequently that I can only give examples. Suppose that a source complains about seasonal adjustments one month, but not another. Or emphasizes sentiment measures only when pointing in the preferred direction. Or emphasizes some specific factor (birth/death adjustment, core measure versus headline) only when it fits their message. It is pretty easy to spot such sources if you look for them. If you find yourself in this camp, take another -1.

7. Relying upon biased or weak sources. Mr. Buffett said that you should not ask your barber if you need a haircut. Why ask a bond guy about stocks? Or an emerging market manager about bonds? Or a hedge fund manager, who is not really there to help you, about anything? If you do not have a high level of skepticism about sources, take another -1.

http://dashofinsight.com

Optionen

2. mit dem dadurch wieder expandierenden Welthandel erhält das Ami-Sentiment endlich die Bedingung, in prerecessive Regionen aufzusteigen und den nächsten grossen Bärenmarkt einzuleiten. Die Kapitulation der Permabären, sprich die langjährige Erfahrung, dass jeder Dip am Ende hochgekauft wird, wird das ihre dazu beitragen. Der Bärenmarkt wird die Eurozone in der besten aller Welten treffen, nämlich gerade dann, wenn neues Vertrauen in die Zukunft Fuss fassen konnte

Optionen

Angehängte Grafik:

capture118.png (verkleinert auf 89%)

capture118.png (verkleinert auf 89%)

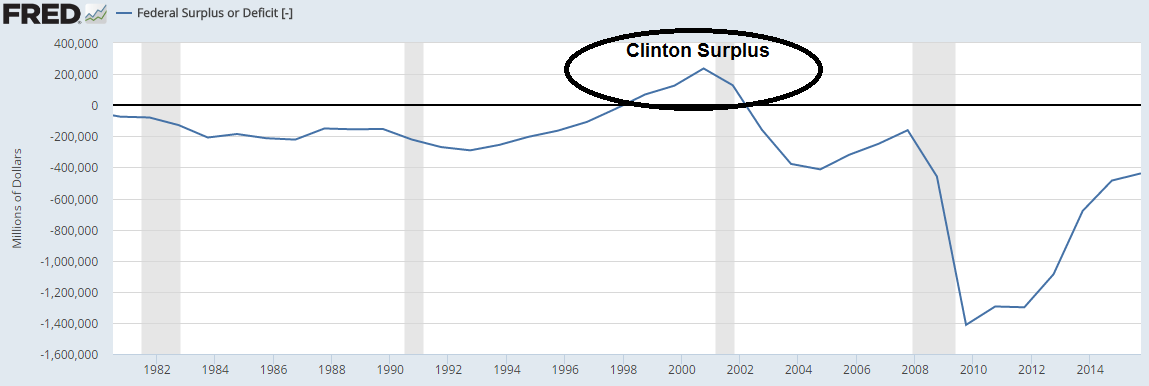

So, was the surplus, followed so closely by a sharp recession, just a coincidence? I suspect not. As Wynne Godley outlined back in the late 1990s, the fiscal position was never all that sustainable because, as a current account deficit country the flows were unsustainable. As I outlined in my popular paper, Understanding the Modern Monetary System, some sector of the economy has to be expanding its balance sheet in order for the economy to grow. If the private sector isn’t expanding its balance sheet (usually through borrowing) then the economy needs to make up for this drag via a government expansion in the deficit OR an expansion from the foreign sector. Since the foreign sector was...

komplett http://www.pragcap.com/the-biggest-risk-of-a-clinton-presidency/

Optionen

Angehängte Grafik:

surp.png (verkleinert auf 44%)

surp.png (verkleinert auf 44%)

Optionen

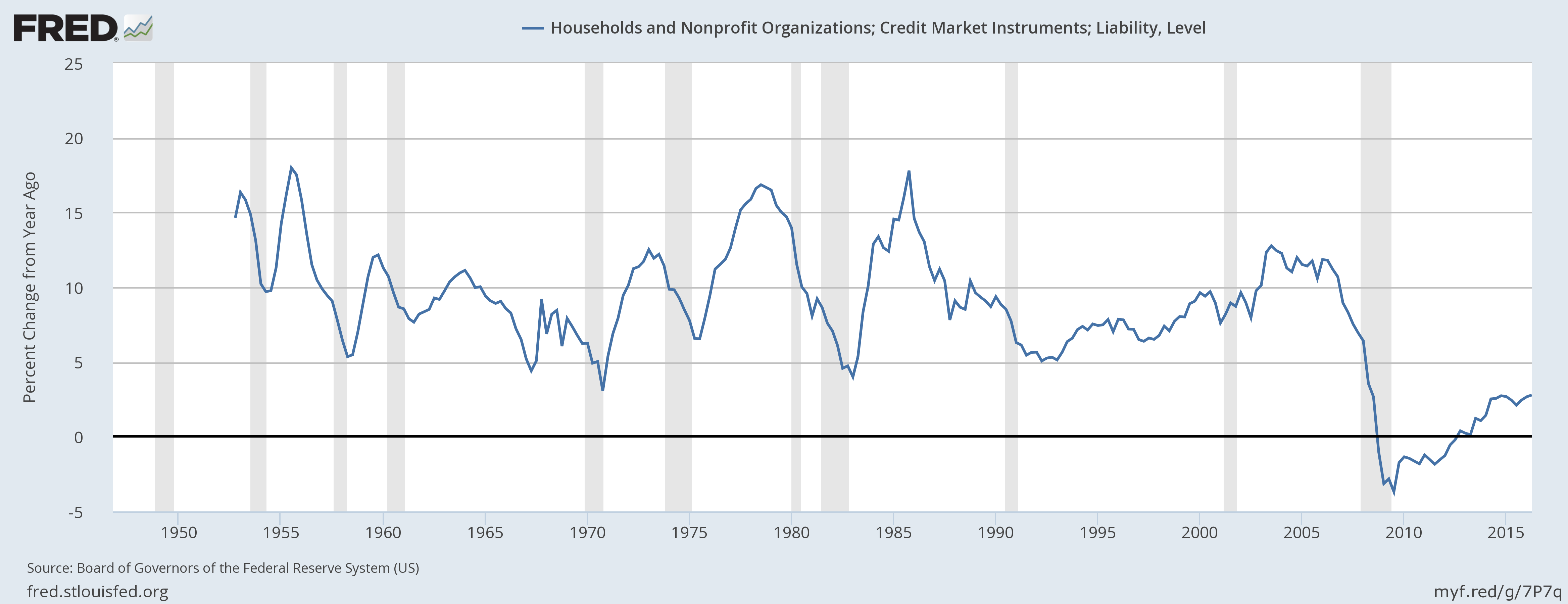

Angehängte Grafik:

fredgraph-9.png (verkleinert auf 10%)

fredgraph-9.png (verkleinert auf 10%)

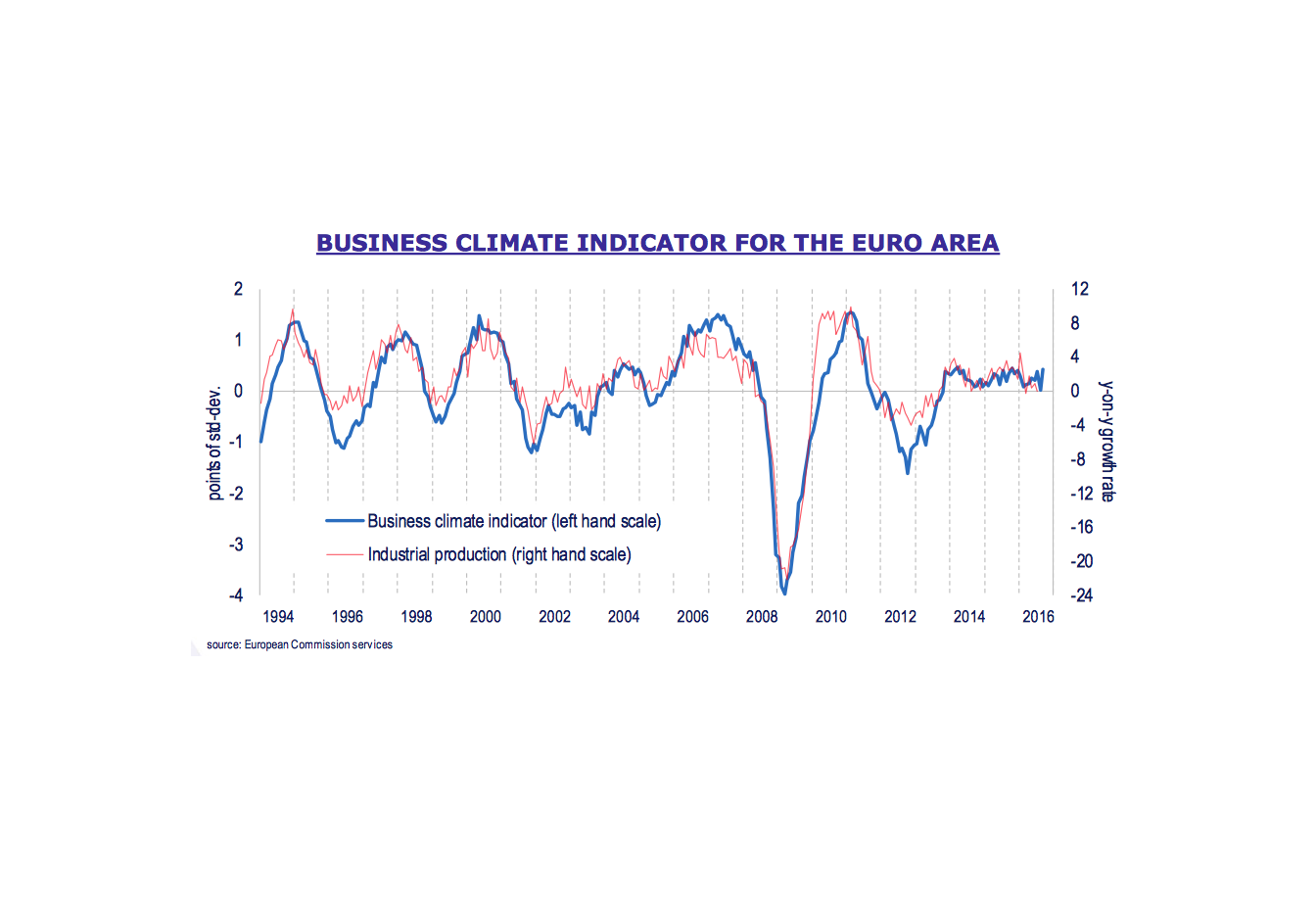

Ich könnte mir vorstellen, dass ein Anstieg auf Bärenmarktlevel nach der langen Krise in der Eurozone relativ schnell sein könnte. Es fehlte nur ein passender Trigger.

Angehängte Grafik:

business_sentiment.png (verkleinert auf 37%)

business_sentiment.png (verkleinert auf 37%)

Angehängte Grafik:

usd_jpy.png (verkleinert auf 41%)

usd_jpy.png (verkleinert auf 41%)

Optionen

A new working paper, “Lost in Fiscal Space,” coauthored by myself and Arjun Jayadev, suggests that, on the contrary, the functional finance and the conventional approaches can be understood in terms of the same analytic framework. The claim that fiscal policy can be used to stabilize the economy without ever worrying about debt sustainability sounds radical. But we argue that it follows directly from the standard macroeconomic models that are taught to undergraduates and used by policymakers.

Here’s the idea...

http://equitablegrowth.org/equitablog/...nce-vs-conventional-finance/