Ökonomen streiten über Verteilungsfrage

Seite 351 von 7846 Neuester Beitrag: 03.02.25 16:55 | ||||

| Eröffnet am: | 05.11.12 08:09 | von: permanent | Anzahl Beiträge: | 197.148 |

| Neuester Beitrag: | 03.02.25 16:55 | von: fws | Leser gesamt: | 37.174.908 |

| Forum: | Leser heute: | 29.882 | ||

| Bewertet mit: | ||||

| Seite: < 1 | ... | 349 | 350 | | 352 | 353 | ... 7846 > | ||||

Optionen

'In an internal document marked "strictly confidential," the IMF said it badly underestimated the damage that its prescriptions of austerity would do to Greece's economy, which has been mired in recession for the last six years.'

http://online.wsj.com/article/...887324299104578527202781667088.html#

Optionen

China's exports posted their lowest growth rate in almost a year in May while imports unexpectedly fell, government data showed on Saturday, underlining concerns about slowing growth in the world's second largest economy.

Evidence has mounted in recent weeks that the economy is fast losing growth momentum as sluggish domestic demand fails to make up for lethargic export sales.

The raft of weak figures has raised worries that China could be facing a weak second quarter. Data for may retail sales and industrial output, as well as inflation, are due on Sunday and could provide more evidence of a slowdown.

http://www.cnbc.com/id/100800314

Optionen

Trotzdem muss man lt. Hulbert im Laufe der nächsten Monate mit einer starken, übergeordenten Korrektur rechnen. Der Sommer würde sich seassonal ideal für die diese Dusche eignen.

image002.gif (verkleinert auf 68%)

.....The U.S. economy continues to heal, but economic escape velocity remains elusive. Europe is in recession and shows few signs of revamping its growth engines. Japan is still to announce growth-enhancing structural reforms. China has slowed. Some other large emerging countries (e.g., Brazil) are struggling to manage well their economies in the context of such a fluid global environment.

I worry that, rather than signal positive handoffs, recent changes are indicative of a gradual erosion in the trust that investors have placed in the power and effectiveness of central banks. It would be natural for this phenomenon to start in Japan as the country faces a difficult set of initial conditions and the lowest historical level of policy credibility.

Should this indeed be the case, look for central banks to be even more aggressive in the next few months as they try to regain control of the narrative. The Bank of Japan and the European Central bank would go further down the road of unconventional policies, and the Fed would not taper QE3 in its upcoming policy meeting as some expect.....http://finance.fortune.cnn.com/2013/06/03/el-erian-market-risk/

und zerohedge:....After all, money printing must lead to higher inflation at some point. The combination in Japan of a gigantic pile of accumulated debt, high running budget deficits, an old and aging population, near-zero interest rates and the prospect of rising inflation (indeed, that is the official goal of Abenomics!) are a toxic mix for the bond market. It is absurd to assume that you can destroy your currency and dispossess your bond investors and at the same time expect them to reward you with low market yields. Rising yields, however, will derail Abenomics and the whole economy, for that matter.

It is, of course, too early to tell. The whole thing could end up being just a storm in a tea cup. It could be over soon and markets could fall back in line with what the central planners prescribe. But somehow I doubt that this is just a blip – and interestingly, so does Mohamed El-Erian, Bill Gross’ colleague at PIMCO and the firm’s other co-chief investment officer.

If that is indeed the case it won’t be confined to Japan but will rapidly reverberate around the world. This is a much bigger story than a modest slowing of QE in the US. Could it be the beginning of the end?

I think the central bankers may not be sleeping so well now.

http://www.zerohedge.com/news/2013-06-07/...al-bankers-losing-control

Und nun der destruktive Teil der Übung: Vergesst den Scheiss.

Genau so wurmstichig sind Theorien, die überall Intrigen vermuten, wenn eigene Prognosen dann nicht eintreffen...

Wir werden also auch in Zukunft trotz Computerprogrammen und Hightech oft danebenliegen.

Weil der Markt stets bockig, eigenbrötlerisch, aufmüpfig und hinterhältig mit Fallgruben bestückt ist. Und das ist gut so.

PS: Äääähm...Optimisten wie ich suchen auch nach Omen....

Optionen

......Another uncomfortable fact for the efficacy of QE are the following facts. Since QE3 was launched last September, total bank reserves have grown by $244.1 billion and excess reserves by $239.4 billion – meaning that 99% of the funds remain idle. So no lending or investment is taking place as banks just take Fed liquidly in and simply earn the overnight interest rate. So, doing the same thing over and over again doesn't do the job of curing unemployment and growing the economy—just the illusion of it.

Main Street sees the stock market doing well which should stimulate more confidence if only people don"t look at the details of conditions.

Stocks rallied sharply out of the gate as headline data suggested more QE, which frankly is all markets have going for it beyond stock buybacks and reduced float.

The most oversold sectors experienced a rally and short squeeze while the overbought sectors were sold. Equity sectors leading markets higher included the major indexes which managed to close the volatile week green (These +/- 200 point days for the DJIA are a bit much even for the pros). Other oversold sectors in the rally included financials (XLF), consumer discretionary (XLY), energy (XLE), and tech (XLK). Still doing poorly, or at least not in the bullish flow, was India (EPI), Asia Ex-Japan (AAXJ), Emerging Markets (EEM), Australia (EWA) and China (FXI). Dividend areas were mixed with energy-related (AMLP) ETFs doing well, while Emerging Market dividend ETFs (DEM) were weaker.

The dollar (UUP) rallied slightly while gold (GLD) was hit hard once again as risk-off assets were shunned. Previously rising credit spreads narrowed as Treasury"s (TLT) fell and High Yield (HYG) outperformed. Commodity tracking ETF (DBC) was a little higher given its high energy weighting as crude oil (USO) rallied. Meanwhile, copper (JJC) continues to underperform which is generally taken as a poor sign of economic growth.

http://www.etfdigest.com/

dauer_unemployed.jpg (verkleinert auf 86%)

http://www.n-tv.de/wirtschaft/...sien-kopiert-EU-article10785711.html

damit ihre Theorie aufgeht. Es ist nämlich der Wunschtraum jeden Börsianers, durch Indizien von gestern das Morgen zu erkennen.

Man muss nur wissen auf welche Indizes und Statistiken die Großen schauen. Dies sind eben zumeist keine einfach erkennbaren Indizes, sondern eine Sammlung diverser Indikationen.

Das Hindenburg-Omen ist hierbei eines jener Indikatoren. Aber vermutlich glaubst du den Regierungen, Zentralbanken und der Frau Merkel, dass Alles wieder gut wird ;-)

Optionen

Oder ists für dich mit Abi einfach zu viel verlangt? ;-)

Optionen

Was die CBs tatsächlich leisten können beschreibt die Lender of the last Resort Funktion: Im Rahmen einer Recession den Zusammenbruch des Geldsystems überhaupt via Flutung und Garantien zu verhindern. Die CBs sind also fähig, einen tragfähigen Boden zu ziehen. Jedoch nicht, zyklische Bewegungen makro effektiv beeinflussen zu können...

Optionen

Aber Geld, dass nicht auf der eigenen Platte liegt sondern irgendwo im Internet (Kayman Inseln, usw.), ja wie nennt man das? Hmmm, wie wäre es mit "FIAT-Money"? Weil ich hoffe und glaube, dass das Geld dort sicherer ist als bei mir zuhause.

*kopfpatsch*

- As previously mentioned, I prefer to follow the monthly AAII asset class allocation. In the recent monthly survey, retail investors increased their equity exposure towards 65.2% of the portfolio, which is the highest for the investment cycle since the March 09 bottom. At the same time, investors decreased their cash levels to 16.7%, one of the lowest levels in over two years. I have previous wrote about the term consistently used by experts quoting that there is "plenty of cash on the sidelines", however the survey shows that cash levels are some of the lowest in over a decade and half. This is not a good time to be a buyer of equities, instead this is a good time to be holding a large amount of cash!

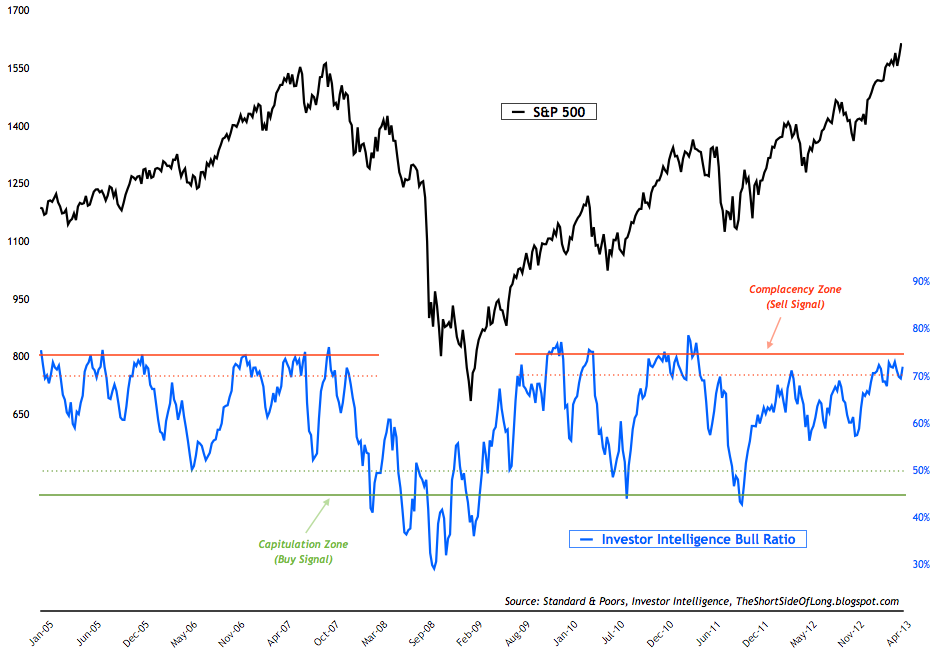

- Investor Intelligence survey levels came in at 46% bulls and 21% bears. Bullish readings fell by more than 6%, while bearish readings increased by a slight 1%. After giving a "sell signal" for quite a few weeks, the II bull ratio has recent fallen below the extreme territory as S&P 500 started correcting. For referencing, recent chart of the II bull ratio chart can be seen by clicking clicking here.

{kind=link}

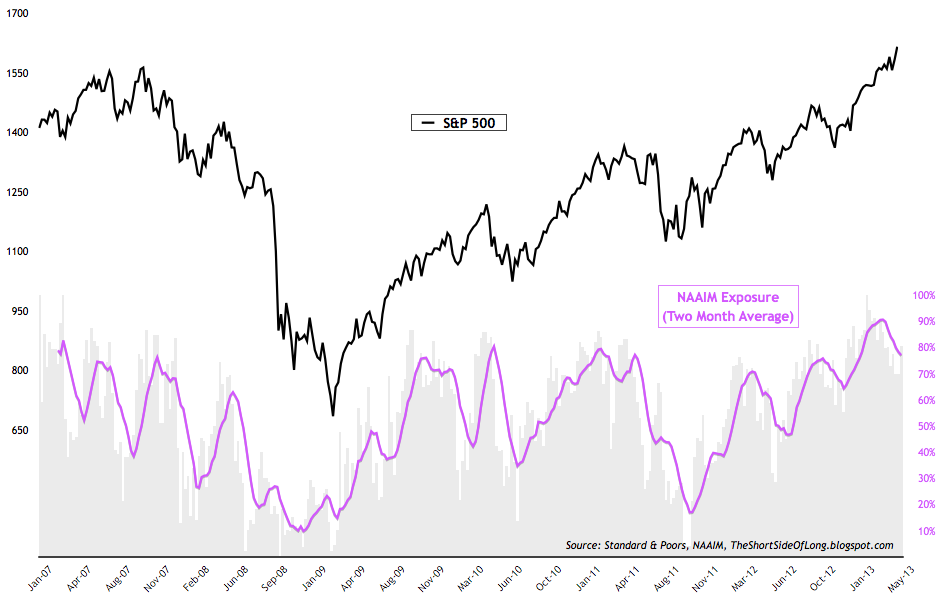

- NAAIM survey levels came in at 52% net long exposure, while the intensity came in at 75%. This is a first time in months that the net long exposure has fallen below extremely bullish readings. It definitely looks like the recent drop in price is changing the market conditions and fund manager exposure. For referencing, recent NAAIM sentiment chart can be seen by clicking here.

{kind=link}

- Other sentiment surveys still remain in the "sell signal" territory. Consensus Inc survey & Market Vane survey remain at or near extremely elevated level associated with previous market tops. The same can be said for the Hulbert Newsletter Stock Sentiment surveys, which remain very close to the frothy levels seen few weeks ago. For referencing, recent Consensus Inc survey chart can be seen by clicking here.

{kind=link}

Optionen

Ein Konjunkturprogramm hingegen wäre Deficit Spending, also eine via Pump geschaffene zusätzliche staatliche Nachfrage, die den Ausfall der privaten kompensiert und überkompensiert. Davon kann aber mit Ausnahme Japans nicht die Bohne die Rede sein. Tatsächlich kürzen die Amis ihr Spending an allen nur denkbaren Ecken und haben so ihr Deficit inzwischen mehr als halbiert. Genau dies wird die Profits drücken und damit eine bearishe Indikation liefern...

Fill

Optionen

meterhohe Botinewände, Flutlichttürmir und Selbstschussanlagen vermögen die Flut mittelloser US-Flüchtlinge ins Gelobte Land Mexico nur zu bemsen. Diese rein wirtchschaftlche Ilegalen auf Scuche nach Esssensresten und Trinkwsser., von unterqualifizierten Härtefellen, stets von Rückabwicklung in die heruntergewirtschafteten Regionen des Nordens bedroht, sich nach harter Arbeit für wenig Lohn, aber in echtem Geld (dem Peso) sehnend - sind ein kleinwenig pessistisches Omen für das, was danoch kommen mag, Der mexicanische Innenmimister unter dem tosenden Applaus von Medien und Stammtischen; "Was dazukommt, ist, dass wir ihnen eine Einreisesperre für eine bestimmte Zeit auferlegen, damit sie am nächsten Tag nicht wiederkommen können."Wenn die dann irgendwo aufgegriffen werden, dann kann man ohne großes Federlesen sie wieder rausschmeißen, und das ist das Entscheidende."

Dies folgende Graphik zeit nur die Trandumkehr. Der Status quo ist wesentlich arlamierender:

Optionen

s22-infografik-mexiko-thickbox.jpg

Der Problem wird in Zukunft nach einem Crash sein, dem aktuellen QE noch eins drauf zu setzen, sonst ist es ja kein heilsamer Schock. Nichts wäre nach einem Crash verheerender als ein "Weiter so, wird schon wirken" seitens der FED.

Dass QE eine Nullnummer ist, gilt nicht ausschließlich, weil nicht alle Anleihen in die Bilanz der FED wandern. QE ist weitestgehend ein Stützungsprogramm, um die Bondpreise oben zu halten und dem Staat somit zu niedrigen Zinsen Geld zu beschaffen. Sobald jedoch Zweifel an de Solvenz der USA kommen (und das wäre nach einem konjunkturbedingten Crash der Fall) dürfte es auch zum Dollarcrash kommen. Einen Bondcrash halte ich für ziemlcih ausgeschlossen, weil die FED zur Not QE hochfahren würde und die großen Stillhalter in Bonds ncht verkaufen werden (was sollten sie für die freigesetzten Dollars sonst kaufen?)

Die aktuellen Zahlen zeigen nun ungschminkt das ganze Dilemma.

""Die Zahlen zeigen die wirkliche Situation des chinesischen Exports", sagte Shen Jianguang, der asiatische Chefvolkswirt der japanischen Bank Mizuho der Nachrichtenagentur Bloomberg. Die Lage sei wegen der schwachen externen Nachfrage und der zuletzt deutlichen Aufwertung des Yuan trüb./seu/DP/zb "

http://www.ariva.de/news/...-Mai-schwach-strengere-Kontrollen-4554024

Mal sehen: Konjunktur schwach aber die CT und die vermeintlich QE-Psychologie wird'S richten?

Da hab ich anno 2000 bessere Argumente für Rekordkurse gehört, z.b. dass die Produkte der Unternehmen gefragt wie nie wären. Das wäre auch in meinen Augen das einzige Argument was steigende Börsen gesund und nachhaltig steigen lassen würde. Denn dass QE alleine seit April nicht mehr als Bullenargument zieht hat sich wohl nicht zu jedem Börsenbriefschreiber rumgesprochen.

Fragt sich, warum die Leute jetzt richtig liegen sollten, wenn sie schon im Mai komplett daneben lagen.

fireshot_pro_screen_capture__005_-... (verkleinert auf 91%)

chart_month_btceurbitcoineuro.png (verkleinert auf 93%)

The average investor misses out in a bull market due to "shell shock" and poor investing habits; however, I would support getting in at these levels, even if a premium has to be paid up front for that privilege instead of waiting around for a better entry point. If a correction takes place, and you have conviction in stocks you are holding or on your watchlist, then do not be afraid to pull the trigger and stay invested in the long run.

"Investing, when it looks the easiest, is at its hardest. When just about everyone heavily invested is doing well, it is hard for others to resist jumping in. But a market relentlessly rising in the face of challenging fundamentals-recession in Europe and Japan, slowdown in China, fiscal stalemate and high unemployment in the U.S.- is the riskiest environment of all."--Seth Klarman

-Naturwissenschaftler betrachten den Markt analytisch ohne Emotionen und können zu Gewinnern werden

-Normalbürger der gesellschaftlichen Mitte machen sich nicht stets tiefe Gedanken und handeln so oft instinktiv richtig

-Gesellschaftswissenschaftler, Poitologen, Sozialwissenschaftler können schön reden, halten sich für überlegen und zahlen die Rechnung für die Naturwissenschafter und Normalbürger an der Börse. Der Gedanke der eigenen Überlegenheit führt ins Verderben.

ave

Optionen

Wendezeit in der Geldpolitik

Die Anleiherenditen steigen. Grenzen der Geldpolitik werden immer häufiger erkannt - so wie die erhebliche Rolle funktionierender Banken und Finanzmärkte für das Wohlergehen einer Wirtschaft. Und die öffentliche Bewertung expansiver Finanzpolitik wirkt nur scheinbar konfus und widersprüchlich. Mehr

Optionen

Selbst Duckmäuser und Hasenfüße müssen also aufs Glatteis, wenn sie nicht permanent verlieren wollen.

Und eine Hausse gedeiht immer dann am besten, wenn genügend Kohle im Umlauf ist, die von der realen Wirtschaft nicht abgegriffen wird. Auch das dürfte in Euroland wohl weiter der Fall sein...

Man kann natürlich immer auf Korrektur spekulieren-- aber Trendwende kann ich bei dem Umfeld nicht erkennen...