against all odds

Seite 100 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 338.402 |

| Forum: | Börse | Leser heute: | 29 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 97 | 98 | 99 | | 101 | 102 | 103 | ... 117 > | ||||

Angehängte Grafik:

bildschirmfoto_2015-09-12_um_08.png (verkleinert auf 29%)

bildschirmfoto_2015-09-12_um_08.png (verkleinert auf 29%)

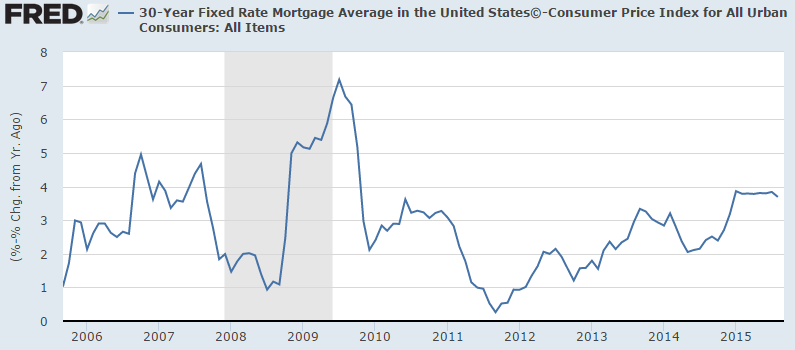

From an operational perspective the Federal Reserve controls an important interest rate. They control the price of money in the overnight market. As the monopoly supplier of reserves to the banking system the Fed is the price setter and not a price taker. But overnight rates are just one of many rates and while they’re important their price does not necessarily steer the future direction of the economy.

If we’ve learned one thing over the last 7 years it’s that reducing interest rates isn’t a very powerful policy mechanism. After all, one would think that 0% interest rates would be akin to “free money”. But interest rates really haven’t been as low as some people think. For instance, the rate that matters most to the housing market (arguably the most important asset market in the economy) has been pretty flat for most of the last 10 years.

And here’s the thing. Since the overnight rate is just a benchmark rate it has a rather imprecise impact on the rest of the economy. The fact that a bank can borrow in the overnight market for 0% does not have any meaningful impact on whether you can afford to buy a mortgage at 4%. And that’s the kicker. The Fed’s control of the short-term rate does not always translate into easing improvements at the long end of the curve structure. This is essentially Alan Greenspan’s great “conundrum”.

If we’ve learned anything over the last couple decades it’s that policy changes via the overnight rate are very imprecise and probably not as impactful as many think. But in many ways we focus on changes in the overnight rate as though they are world changing events. And in focusing so much on interest rates and treating the Fed like it has an Archimedean Lever over the economy, we lose sight of policies that might actually help us at times when we need it. When will we learn to stop focusing so much on policies that clearly aren’t as important as some would like to think?

Optionen

Angehängte Grafik:

fred1.png (verkleinert auf 64%)

fred1.png (verkleinert auf 64%)

Optionen

Angehängte Grafik:

real_domestic_demand__chart_peter_praet__ec....png (verkleinert auf 80%)

real_domestic_demand__chart_peter_praet__ec....png (verkleinert auf 80%)

The second one: newspapers aren’t going to tell you “we had 280 deaths on the roads today in America”. They’re going to tell you about the plane crash killing 14 people. So, you have misrepresentation of the math of risks. They are driven by the sensational. And the statistical and the sensational are not the same in our modern world.

https://larspsyll.wordpress.com/2015/09/29/newspapers-make-you-stupid/

Optionen

Optionen

Angehängte Grafik:

spxdef.jpg (verkleinert auf 51%)

spxdef.jpg (verkleinert auf 51%)

Optionen

Angehängte Grafik:

michigan-consumer-sentiment-index.gif (verkleinert auf 55%)

michigan-consumer-sentiment-index.gif (verkleinert auf 55%)

herkunft: postkeynesian

link: http://www.coppolacomment.com

license: Creative Commons Attribution 3.0 Unported License

about: Frances Coppola worked in banking for 17 years as a business analyst and project manager, running business and systems projects for (among others) RBS, Nat West, HSBC, Midland Bank and SBC Warburg (now UBS). Her banking experience encompasses retail and investment banking, front office, operations and settlement, but her particular area of expertise is financial control and risk management. She is particularly proud of the fact that RBS still produces its financial and regulatory reporting using a group consolidation system that she designed.

Frances is now a writer and commentator on banking, finance and economics. Her blog Coppola Comment is widely read and her writing has featured on the Financial Times, City AM, The Economist. The Guardian and a range of online publications. She also writes for the online magazine Pieria and occasionally for the ICAEW, and she is a frequent commentator on banking matters for the BBC.

Frances has an MBA from Cass Business School with a specialism in finance and risk management. And since financial people can be creative too, Frances is also a professional singer and singing teacher. She has a B.Mus from London University and is an Associate of the Royal College of Music. She also has two teenage children and not much time to do the garden any more!

Optionen

Optionen

Angehängte Grafik:

nu_(1).gif (verkleinert auf 84%)

nu_(1).gif (verkleinert auf 84%)

Bin ja, wie bereits beschrieben schon seit ca. einem Jahr in Brasilien investiert. Mit den entsprechenden Buchverlusten. Vorgestern habe ich eine Position Aeroflot gekauft.

Ich spekuliere auf ein Ende der Konfrontation zwischen Russland und dem Westen. Gerade, da Europa ein Problem mit den Flüchtlingsströmen hat, kann es seine Haltung gegenüber Russland nicht aufrecht erhalten.

Wie wir beide am eigenen Laib im "Bekloppte reden über Verteilungsfragen" Thread

erfahren haben, dürfte die europäische Politik den Eindruck haben, dass dumpfes, rechtes Gedankengut ein paar Plätze im Parlament kosten könnte.

Russland spielt seine Position mM nach sehr gezielt und verdient aus strategisch-theoretischen Überlegungen meinen Respekt. Menschlich sieht die Welt wiederum anders aus.

Der Finanzindustrie sollte klar sein, dass die aktuellen Assetpreise in den EM's absolute Schnäppchenpreise sind. Wäre ich Finanzmaffia, würde ich schon seit längerem auf Einkaufstour sein und jetzt gezielt an einem Comeback der EM's arbeiten.

Ein schwächerer Dollar und wieder mehr Direktinvestitionen würden den Bärenmarkt beenden und die Assetpreise erheblich heben. Der Konsum in diesen Ländern würde wieder steigen und die Weltwirtschaft beleben.

Optionen

Optionen

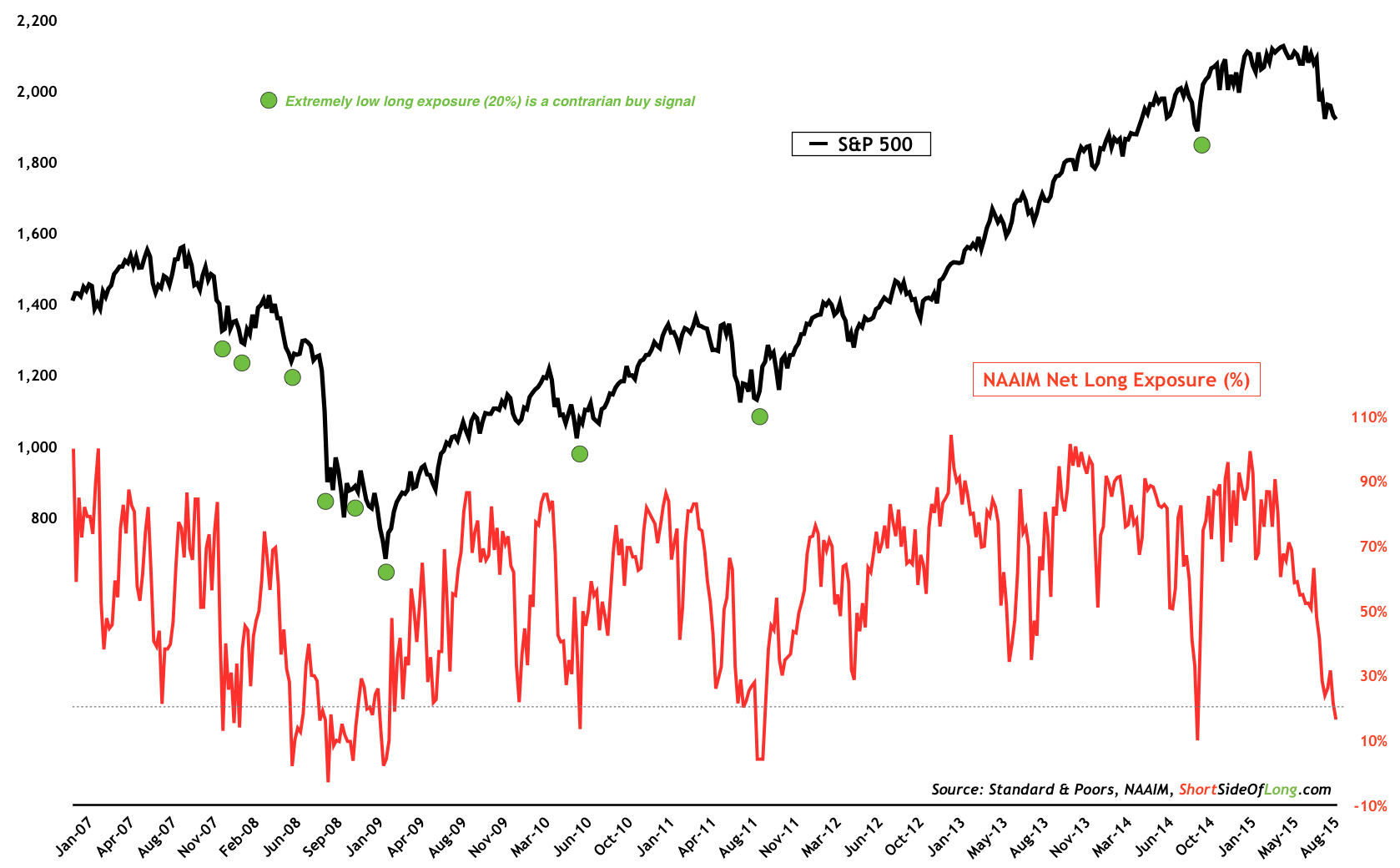

Angehängte Grafik:

naaim-net-long-exposure.png (verkleinert auf 30%)

naaim-net-long-exposure.png (verkleinert auf 30%)

'net financial assets'

Autor: http://www.interfluidity.com/v2/6174.html

Every financial asset is also some entity’s liability. The sum of all financial positions is by definition zero. So we can write:

NET_WORLD_FINANCIAL_POSITION = 0

Suppose that, quite arbitrarily, we divide the world into a “foreign” and a “domestic” sector. Then we have:

NET_FOREIGN_FINANCIAL_POSITION + NET_DOMESTIC_FINANCIAL_POSITION = NET_WORLD_FINANCIAL_POSITION = 0

NET_FOREIGN_FINANCIAL_POSITION + NET_DOMESTIC_FINANCIAL_POSITION = 0

Suppose that, again arbitrarily, we decompose the domestic economy into a public and private sector:

NET_PRIVATE_DOMESTIC_FINANCIAL_POSITION + NET_PUBLIC_DOMESTIC_FINANCIAL_POSITION = NET_DOMESTIC_FINANCIAL_POSITION

Substituting into our previous expression, we get

NET_FOREIGN_FINANCIAL_POSITION + NET_PRIVATE_DOMESTIC_FINANCIAL_POSITION + NET_PUBLIC_DOMESTIC_FINANCIAL_POSITION = 0

We can also write this in terms of changes or flows. Since the sum above must always be zero, it must be true that any changes in one sector are balanced by changes in another:

ΔNET_FOREIGN_FINANCIAL_POSITION + ΔNET_PRIVATE_DOMESTIC_FINANCIAL_POSITION + ΔNET_PUBLIC_DOMESTIC_FINANCIAL_POSITION = 0

Two of the flows in the equation above have conventional names, so we can rewrite:

CURRENT_ACCOUNT_DEFICIT + ΔNET_PRIVATE_DOMESTIC_FINANCIAL_POSITION + CONSOLIDATED_GOVERNMENT_SURPLUS = 0

Rearranging…

ΔNET_PRIVATE_DOMESTIC_FINANCIAL_POSITION = -CURRENT_ACCOUNT_DEFICIT + -CONSOLIDATED_GOVERNMENT_SURPLUS

ΔNET_PRIVATE_DOMESTIC_FINANCIAL_POSITION = CURRENT_ACCOUNT_SURPLUS + CONSOLIDATED_GOVERNMENT_DEFICIT

Optionen

Optionen

Angehängte Grafik:

fig2.png (verkleinert auf 81%)

fig2.png (verkleinert auf 81%)