against all odds

Seite 99 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 342.352 |

| Forum: | Börse | Leser heute: | 1 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 96 | 97 | 98 | | 100 | 101 | 102 | ... 117 > | ||||

Wenn man es bemerkt, ist es in der Regel mal Zeit Feierabend zu machen.

Optionen

Mein Bauch sagt zur Zeit klar Long, mein Senti-HS noch nicht. Also halte ich die Füsse still. Wird schon seinen Sinn haben. Bislang hatte es das zumindest.

Wenn es sich die nächsten Tage tatsächlich in diese Richtung weiter bewegt, könnten wir vielleicht endlich eine negative Stimmung erreicht haben, die für eine Bodenbildung notwendig wäre.

www.daxtrend.blogspot.de

Optionen

Most people think QE is powerful because it adds “money” to the private sector, but as I’ve explained repeatedly QE is really just an asset swap. The more “money” is only stimulative to the extent that swapping a savings account with a checking account is stimulative. So, we have our other six transmission mechanisms.

The interest rate channel is weak because QE doesn’t have a strong impact on long rates unless the Central Bank explicitly sets long rates. Otherwise, long rates float with market expectations. The financial crisis channel works best when markets are panicked and liquidity is low. The asset price effect is highly questionable and not likely as powerful as some believe.

The expectations channel can’t possibly be as powerful as some assert because of the multi-temporal problem I’ve discussed before (basically, expectations of a boost in growth now is offset by expectations of a contraction in policy later). The credit channel isn’t powerful because the central bank doesn’t directly control demand for debt. And the exchange rate channel is only powerful if the central bank explicitly targets exchange rates. So, the short story is, QE isn’t really as “easing” as many believe.

So, the clear conclusion here is that domestic QT can’t be “tightening” unless you believe that QE is a powerful form of “easing”. The evidence on that is weak at best.

At an international basis the term Quantitative Tightening is equally misleading. For instance, China does not control the quantity of dollars that exist in the financial system at any given time. They can influence their domestic economy’s quantity of Yuan, but they do not control foreign currency quantities. Remember, China buys US T-Bonds primarily because they are a net importer of US Dollars due to their trade position. The People’s Bank of China does not control this position.

The cause (trade inflows) and effect (PBoC T-Bond purchase) is not properly referred to as “easing” since the PBoC is not implementing this policy in an independent attempt to ease policy. Likewise, any unwind of this balance sheet will not reduce global liquidity, but rather, will likely be implemented as an attempt to boost domestic demand and further positively influence trade inflows into China.

Like Quantitative “Easing”, Quantitative “Tightening” likely isn’t as relevant as many will make it out to be.

Optionen

Link: http://www.imf.org/external/pubs/ft/survey/so/2015/res083115a.htm

...With respect to outside, the issue I have been struck by is how to indicate a change of views without triggering headlines of “mistakes,’’ “Fund incompetence,’’ and so on. Here, I am thinking of fiscal multipliers. The underestimation of the drag on output from fiscal consolidation was not a ``mistake’’ in the way people think of mistakes, e.g., mixing up two cells in an excel sheet. It was based on a substantial amount of prior evidence, but evidence which turned out to be misleading in an environment where interest rates are close to zero and monetary policy cannot offset the negative effects of budget cuts. ..To take a familiar example, I believe that, in the context of the Greek program discussions, it made good sense to argue for debt relief first in private. We did. And when we thought our argument was not getting through, it made good sense to then go public.

komplett s.o.

Optionen

Optionen

Angehängte Grafik:

nyse-margin-debt-spx-growth-since-1995.gif (verkleinert auf 56%)

nyse-margin-debt-spx-growth-since-1995.gif (verkleinert auf 56%)

Optionen

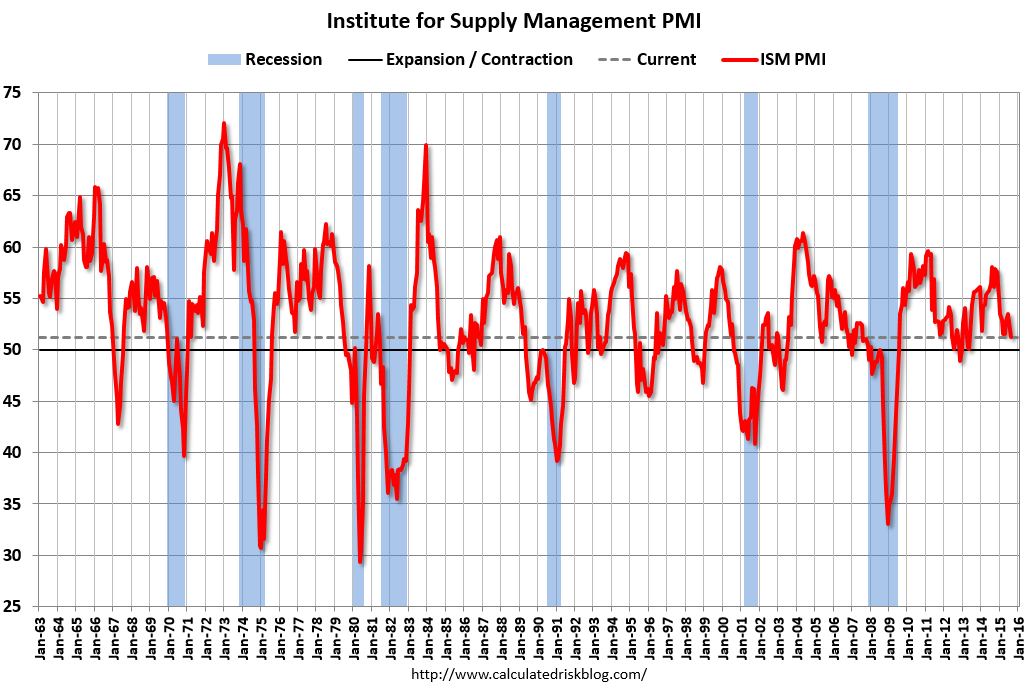

Angehängte Grafik:

ismaug2015.png (verkleinert auf 49%)

ismaug2015.png (verkleinert auf 49%)

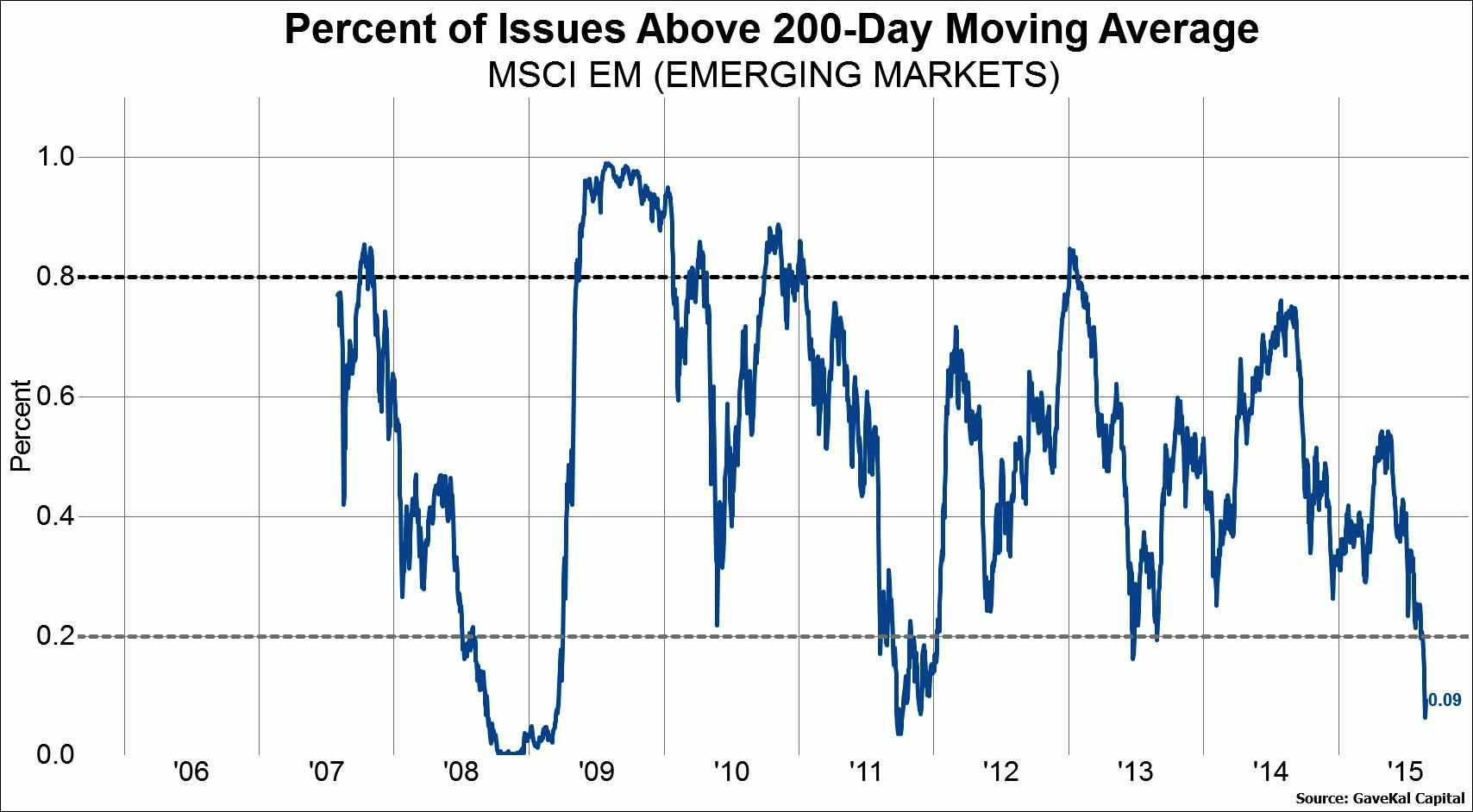

Interessanter finde ich indes, dass das Sentiment immer noch sehr bärisch ist, obwohl der Dax in der Spitze über 30% abgegeben hatte. Da wimmerten die Bären, dass es schon zu lange keine 10% Korrektur gegeben hatte und erwarten nun (wie immer) nichts geringeres als Armageddon.

Zudem sind die EM's samt China derart abgerutscht, dass die Bären eigentlich völlig überfressen in ihren Höhlen liegen müssten. Scheint allerdings nicht so zu sein.

Angehängte Grafik:

brl.png (verkleinert auf 43%)

brl.png (verkleinert auf 43%)

Bin schon in Brasilien investiert, leider zu früh mit entsprechenden Buchverlusten.

Nun suche ich nach einem besseren Einstieg, um nachzufassen.

Angehängte Grafik:

msci-em-breadth.jpg (verkleinert auf 29%)

msci-em-breadth.jpg (verkleinert auf 29%)