Vipshop Q1 Shows Triple-Digit Growth

China-based online discount retailer Vipshop Holdings (VIPS) reported first-quarter earnings after the market closed Wednesday that beat consensus estimates as it raised Q2 guidance.

Revenue rose 126% to $702 million in Q1 from the year-ago quarter, surpassing the consensus estimate of $652.2 million. Adjusted earnings per share of 63 cents rose 270%, beating the consensus estimates of 48 cents.

For Q2, Vipshop estimates revenue in the range of $780 million to $790 million, above the consensus view of $688 million, of analysts polled by Thomson Reuters.

Vipshop stock was up 2.5% to 150 in after-hours trading.

The company launched its IPO in March 2012. Priced at 6.50, the stock is up more than 2,100% since then.

Vipshop said active customers for the first quarter of 2014 rose 165% to 7.4 million from the prior year period. Total orders increased by 129% to 20 million.

First Quarter 2014 Highlights

Total net revenues increased by 125.9% over the prior year period to US$701.9 million, primarily attributable to a 165.1% increase in the number of active customers[1] to 7.4 million from 2.8 million and a 129.3% increase in total orders[2] to 20.2 million from 8.8 million over the prior year period.

Gross margin increased to 24.9% from 23.4% in the prior year period.

Non-GAAP income from operations[3] increased by 394.3% year-over-year to US$42.8 million from US$8.7 million in the prior year period. Non-GAAP operating income margin[4] increased to 6.1% from 2.8% in the prior year period.

Net income attributable to Vipshop's shareholders increased by 355.3% to US$26.6 million from US$5.8 million in the prior year period. Net income margin increased to 3.8% from 1.9% in the prior year period.

Non-GAAP net income attributable to Vipshop's shareholders[5] increased by 318.2% to US$37.7 million from US$9.0 million in the prior year period. Non-GAAP net income margin increased to 5.4% from 2.9% in the prior year period.

http://www.ariva.de/news/...st-Quarter-2014-Financial-Results-5038414

9%plus bei tradegate

The bullish trend continues

http://www.4-traders.com/VIPSHOP-HOLDINGS-LTD-AD-10246804/strategies/

Angehängte Grafik:

vips-consensus_revision_(last_18_months).png

vips-consensus_revision_(last_18_months).png

Vipshop’s strong 126% year-on-year revenue growth was driven by 1.6 times rise in active users and 1.3 times increase in orders, according to Deutsche Bank. Thanks to operating leverage, Vipshop’s operating margin improved by 1 percentage point to 6.1%, even as Lefeng, the discount makeup site that Vipshop recently bought, was incurring losses.

On a strong revenue outlook, we lift our FY14/15E revenue by 11%/12%, to Rmb3.4bn/5.3bn (+102%/54% YoY). We largely maintain our FY14/15E non-GAAP OPM of 5%/6.5% and increase EPS by 14%/6%. Our new US$191 TP (+8%) is based on an unchanged 1.0x PEG, against a 73% FY14-16E EPS CAGR (prior 76%).

http://blogs.barrons.com/emergingmarketsdaily/...deutsche-raises-tp/?

.... First Cramer says Vipshop dominates its category, which is growing at an explosive pace. "From 2012 through 2015 it's expected to expand at a 56.2% compound annual growth rate," Cramer said. That's significant opportunity.

Also, Cramer believes the Vipshop 'story' is still in early chapters with many more people likely to discover the site.

If VipShop were in the U.S., Cramer said, the company would have tons of bricks-and-mortar competition. Not so in China, however, where the company stands alone.Shares of VipShop are up 91% so far this year, but the company still only trades at 36 times earnings with a 58% growth rate. Cramer reminded viewers that VipShop is a Chinese Internet stock, which makes it highly speculative. But its continued growth means that for speculation it's certainly worth a look.

Vipshop is becoming a legitimate e-commerce company, and therefore, it's a growing threat to Alibaba and JD.com. With Vipshop's market cap being $10 billion, its valuation is relatively similar to JD.com's implied worth. However, a combined Vipshop and JD.com would create quite a power to battle Alibaba.

For Alibaba, Vipshop would give it access to an e-commerce channel that is growing rapidly, including its flash-sales model, which also provides access to more than 350 brands that may be willing to discount aggressively.

The final scenario is an Amazon take-over. Already, plans have been discussed of Alibaba and JD.com entering U.S. markets. Hence, Amazon acquiring Vipshop would give it a growing channel and a presence in China, perhaps even a hedge against Alibaba and JD.com.

http://www.fool.com/investing/general/2014/05/17/...t-lead-to-vi.aspx

....Dangdang looks like a lame duck next to its e-commerce peer Vipshop (VIPS), which reported first-quarter earnings too. Unlike Dangdang, Vipshop’s revenue growth went well ahead of analyst expectations.

Investors punish more than reward these days. Shares of Dangdang slumped 15.9% this morning. Vipshop rose 5.2%.

User growth at Dangdang is also unimpressive compared to Vipshop. Dangdang had appromixately 8.6 million active customers, a 16% increase from a year ago. Total orders for the first quarter were about 16.4 million, an 11% rise. Vipshop saw a 1.6 times rise in active users and 1.3 times increase in orders.

wenn ich hier über Vipshop angefangen habe zu posten,dann nur weil ich denke ,dass einige der chinesischen oder auch russischen Internetwerte eine gute Zukunft vor sich haben.DangDang erschien mir schon früher etwas problematisch

Sie stehen bei mir noch auf der Watchlist

Baidu (BIDU), Vipshop Holdings (VIPS): "I like Baidu, Alibaba when it comes public and Vipshop. Those are my 3 Chinese stocks for 2014."

http://seekingalpha.com/article/...-3-chinese-stocks-for-2014-5-22-14

.........

Improving growth outlook for Vipshop

Vipshop reported Q1 earnings that blew past analyst estimates, as the strong growth momentum keeps its top and bottom line growing in triple digits. In fact, revenue growth accelerated in Q1 after three consecutive quarters of slowing growth. The company also guided FY 2014 revenue $100 million higher than the analyst consensus at the time. The growth in expectations caused Vipshop's forward valuation to only rise slightly despite a 52% rise in its share price from late February. We should see continued strong growth in the rest of 2014, and further margin expansion as a consequence of increased scale and the integration of the Lefeng acquisition, where the company will take advantage of cross selling opportunities and benefit from synergies which will lower the combined operating expenses.

I expect that Vipshop will continue to grow ahead of expectations and I believe that there might be further upside for FY 2014 earnings and revenue, which will lead to a higher share price going forward.---

Vipshop Holdings (NYSE:VIPS) is in a consolidation with a 182.10 buy point. The stock has been digesting gains since early March. Vipshop has perked up in the past couple of weeks and its up/down volume ratio, a demand gauge, has climbed back above 1.0. On a down note, the stock is in a late-stage pattern.

Earlier this month, the Chinese online retailer blew by views with a 271% surge in Q1 earnings. Another triple-digit gain is expected in the current quarter.At the end of the first quarter, 251 funds owned shares, up from 125 two quarters before that. T. Rowe Price New Horizons , a leading growth fund, has a position. But it trimmed its holdings in the latest reported quarter.

Read More At Investor's Business Daily: http://news.investors.com/...2342-vipshop-has-solid-profit-growth.htm

Vipshop shares recently broke resistance at $160.

Coming off strong second quarter earnings and guidance.

JPMorgan raised price target for stock to $210......

....P/E Ratio: A current P/E ratio of over 113 may come across as rather alarming. However, with the projected growth, that figure is soon to drop dramatically. Assuming the company merely meets earnings expectations for the final three quarters this year, full year EPS of $2.87 would leave the stock with a current P/E value of under $60. Meanwhile, full year 2015 earnings are expected to come in at $4.54....

Read More At Investor's Business Daily: http://news.investors.com/technology/...ation-slows.htm#ixzz3Ghub1O9L

http://finviz.com/quote.ashx?t=vips

Die Firma hat eine Eigenkapitalrendite von 35%? Wow . . .

Optionen

| Boardmail an "Bursar" |

Wertpapier: Vipshop Holdings Ltd AD |

Vipshop (VIPS)

Online retailer Vipshop had a rough debut on the New York Stock Exchange in 2012, and that is putting it lightly. It raised 39% less than its IPO target, dropped 15% on its first day of trading and by six months after going public had gained just 0.5%.

Last year, things began to turn around for the company, and both George Soros and Chase Coleman have reaped the benefits.

Coleman's Tiger Global got its feet wet with the investment in the first quarter last year, purchasing 850,000 Vipshop shares and selling them off during the next quarter. In the fourth quarter last year, it came back around on the stock, buying up 1.46 million shares.

As of the second quarter this year, Tiger Global owns 2.43 million shares, nearly double.

Soros, on the other hand, bought into Vipshop in the third quarter last year with the purchase of 101,000 shares. As of the second quarter this year, he holds 475,000 shares

On this one, the proof is in the numbers: Both billionaires have gained more than 100% on their Vipshop investments in less than a year.

http://www.thestreet.com/_nasdaq/story/12932245/1/...EE&cm_ite=NA

“In our view, an established reputation and strong supply chain management capabilities position Vipshop well to benefit from the rapidly growing online flash sales market in China. We expect Vipshop’s marketing and big data investments to foster strong new active customer growth and enhance customer experience. Mobile leadership with 46% revenue contribution. Stronger-than-peer growth profile and better earnings visibility.,” the firm’s analyst commented......

Traders bought 2,281 put options on the stock. This represents an increase of 145% compared to the average daily volume of 930 put options.

Vipshop Holdings Ltd – (NASDAQ:VIPS) last released its earnings data on Wednesday, August 13th. The company reported $0.72 earnings per share for the quarter, beating the analysts’ consensus estimate of $0.64 by $0.08. The company had revenue of $829.40 million for the quarter, compared to the consensus estimate of $791.55 million. Analysts expect that Vipshop Holdings Ltd – will post $2.97 EPS for the current fiscal year. ......

http://sleekmoney.com/...-from-analysts-at-morgan-stanley-vips/50770/

Die Zukunft hat begonnen 4.0!

Ist den Investierten seit meinem Einstieg allerdings längst bekannt.Müsstest du als Langfrist Anleger eigentlich auch längst wissen, oder!?

Auf steigende Kurse..

Chinese online fashion retailer Vipshop Holdings Ltd. (VIPS) rose to a record in New York as concern waned that Alibaba Group Holding Ltd. (BABA) will lure investors away from smaller rivals.

Vipshop surged 4.3 percent to $229.29 on Oct. 31, capping an 11-week stretch that saw the company’s American depositary receipts lose 26 percent of their value leading up to and immediately after Alibaba’s $25 billion initial public offering, before rallying 34 percent to an all-time high.-----

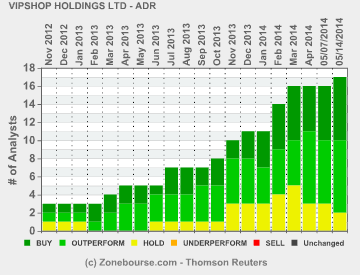

Of 24 analysts covering the company, 21 have buy recommendations, the highest number since the company’s March 2012 IPO. While Vipshop’s sales will increase at a slower pace next year, net income growth will accelerate, according to the mean of 21 analyst estimates compiled by Bloomberg.

Henry Guo, senior analyst at JG Capital Corp. in San Francisco, said by phone on Oct. 31. “Vipshop is a leader in a niche market. Although Alibaba has a similar service, those segments have not gained any traction yet. Alibaba is not a meaningful competitor for Vipshop in the near term.”

solch ein Unfug so ein Gerücht in die Welt zu setzen,einfach unzulässig!

Nur so kann Marktwirtschaft und Unternehmensbewertung funktionieren!

Ich war vor vielen Jahren bei der Übernahme von Netscape durch AOL dabei.Da ging es innerhalb Sekunden von 10 DM auf 400DM..

Wenn Substanz an den Mann gebracht werden muss,gelten häufig keine Gesetze an der Börse!

Und genau das ist hier der Fall.Wirst sehen!