Peabody Energy - Buy of a lifetime!?

Seite 1 von 4 Neuester Beitrag: 04.04.17 23:11 | ||||

| Eröffnet am: | 16.06.15 11:57 | von: watchandlear. | Anzahl Beiträge: | 89 |

| Neuester Beitrag: | 04.04.17 23:11 | von: groundinspec. | Leser gesamt: | 41.255 |

| Forum: | Börse | Leser heute: | 6 | |

| Bewertet mit: | ||||

| Seite: < | 2 | 3 | 4 > | ||||

Wertentwicklung:

10 Tage: -27%

3 Monate: -60%

1 Jahr: -83%

5 Jahre: -94%

Einige Kennzahlen 2014 in Mio USD:

Umsatz: 6.133

Ergebnis: -787

Eigenkapital 2.900

akt. MK: 700

akt. Cash: 600 + 1,5 Mrd. aufgrund von Bankzusagen

Shortquote: 27%

Homepage:

http://www.peabodyenergy.com/

Akt. Unternehmenspräsentation:

https://mscusppegrs01.blob.core.windows.net/...tation_june%202015.pdf

Wikipedia:

https://en.wikipedia.org/wiki/Peabody_Energy

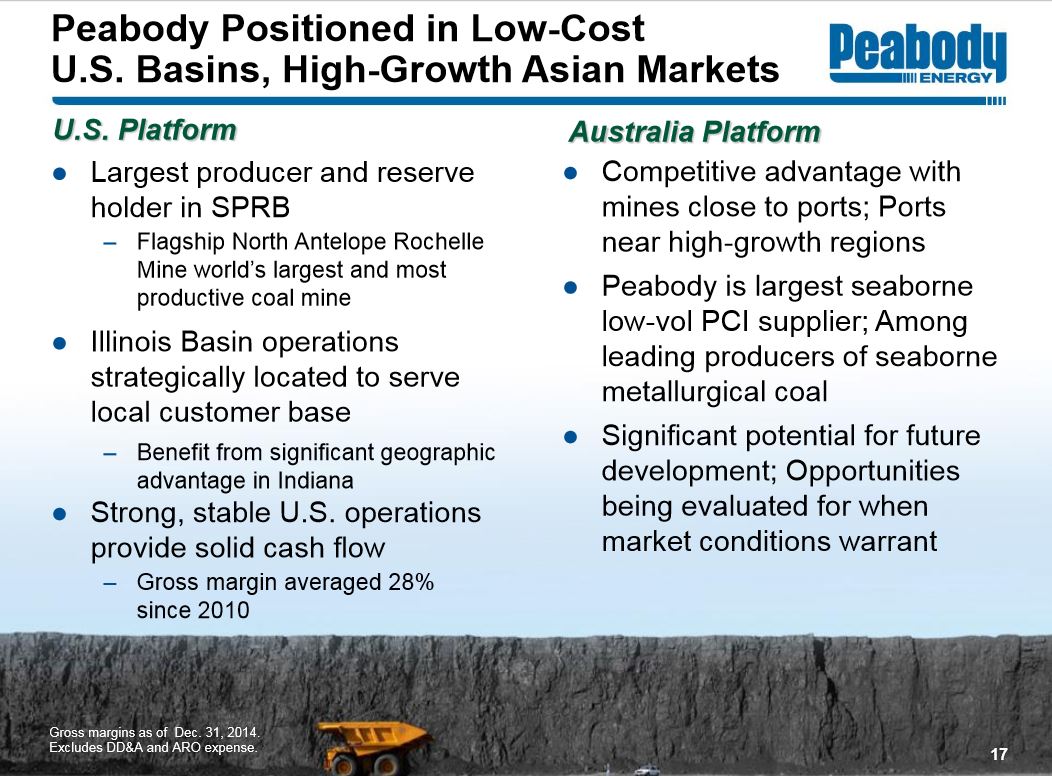

Peabody Energy ist das größte private Kohleunternehmen der Welt, welches 1883 in den USA gegründet wurde. Es deckt 10% der Stromversorgung in den USA und 2% in der ganzen Welt durch die Kohlelieferungen ab. In Summe betreibt das Unternehmen 26 Minen, welche sich in USA und Australien befinden. Herzstück der Firma ist die Mine Souther Powder River Basin (SPRB) in den USA. Hier werden aktuell 140 Mio Tonnen pro Jahr verkauft und die Reserven belaufen sich auf 3,1 Mrd Tonnen. In Summe verkauft Peabody pro Jahr 250 Mio Tonnen und die Gesamtreserven belaufen sich auf 7,6 Mrd Tonnen.

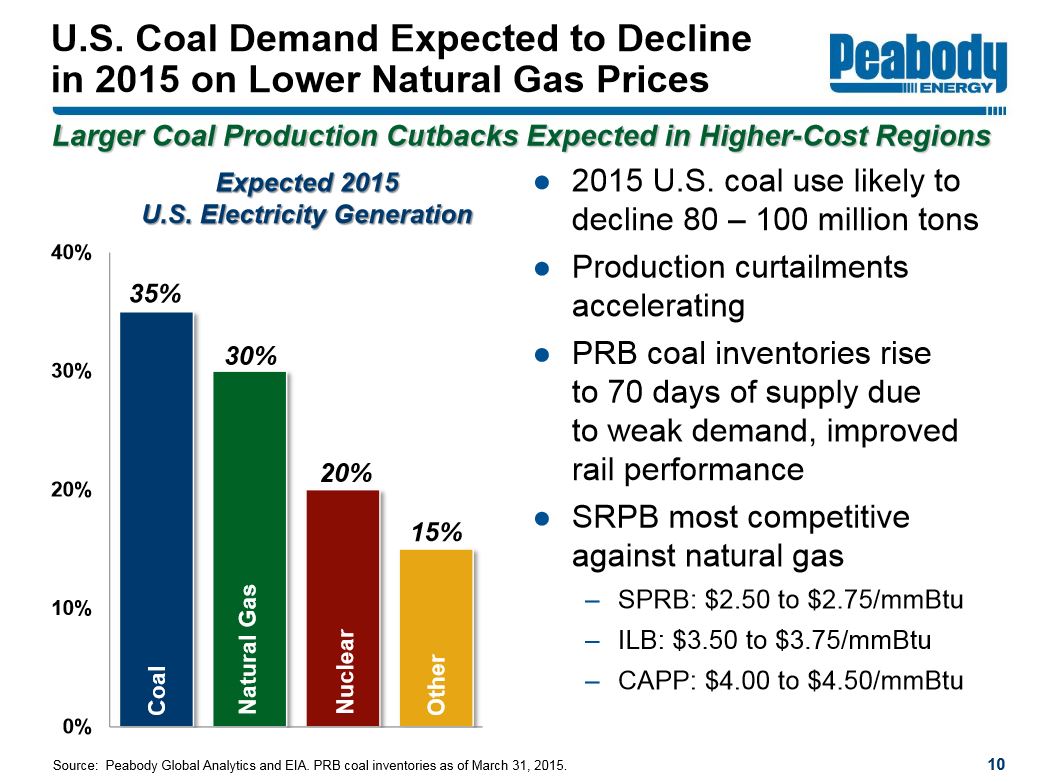

Der Kursrückgang lässt sich hauptsächlich damit erklären, dass durch das Fracking in den USA viele neue Gasvorkommen gefunden wurden, wodurch immer mehr Gas für die Energiegewinnung genutzt wird. Der Gaspreis ist aufgrund des großen Angebots auch ziemlich niedrig bei aktuell 2,90 USD. Viele Kohleproduzenten sind nicht mehr wettbewerbsfähig, haben hohe Schulden und stehen kurz vor der Insolvenz (z.B. Walter Energy, Arch Coal oder Alpha Natural Resources). Deren Hauptproblem ist vor allem, dass sie noch in diesem Jahr fällige Schulden nicht bedienen können. Peabody hat jedoch primär langfristige Schulden, welche teilweise erst in 4 Jahren fällig werden. Eine Insolvenz kann also die nächsten Jahre ausgeschlossen werden.

Peabody hat bereits einige Sparmaßnahmen gestartet. So wird z.B. die Kohleförderung in Australien reduziert, da diese hochwertige Kohle auch mit die höchsten Förderkosten hat. Ebenso werden aktuell 250 Mitarbeiter entlassen und Filialen geschlossen.

Interessant ist auf jeden Fall, dass die Förderung von Peabodys größter Mine Souther Powder River Basin allerdings erhöht werden soll. Dies macht auch Sinn, da sich hier die Förderkosten umgerechnet auf den Gaspreis bei 2,50-2,75 USD liegen. Solange der Gaspreis also bei 3 USD liegt, wäre Peabody weiterhin konkurrenzfähig. Desweiteren sollte man bedenken, dass Peabody natürlich auch Stahlkonzerne beliefert, welche Kohle für die Stahlerzeugung benötigen. Dies ist völlig unabhängig von einem Gaspreis.

Aufgrund der starkten Währungs- und Rohstoffpreisschwankungen wird das Ergebnis und der Cash Flow von Peabody aktuell negativ stark beeinflusst. Peabody selbst hat bereits mitgeteilt, dass Anfang 2017 Hedgingpositionen auf Währung und Rohstoffe aufgelöst werden und es dadurch zu einer Ergebnis- und Cash Flow Verbesserung von ca, 685 Mio USD jährlich kommt! Ergänzt man noch die oben genannten Kosteneinsparungen, so könnte Peabody bei unveränderten Kohlepreis 2017 wieder eine schwarze Null schreiben. Sofern der Kohlepreis sogar bis dahin auch mal wieder steigen sollte, wäre das Unternehmen wieder deutlich in der Gewinnzone.

Die Analysten haben mal wieder sehr unterschiedliche Meinung… das niedrigste Kursziel liegt bei 2 USD von Goldman Sachs. Noch im Herbst 2014 hatten sie ein Kursziel von 13 USD und 2013 lag es noch bei 21 USD…. andere Analysten sagen akt. 4; 4,53 und 6 USD (alle von Juni 2015). Der Durchschnitt liegt akt. bei 7 USD Kursziel.

Ein kurzfristiger Rebound sollte auf jeden Fall möglich sein. Ob es aus langfristig gut läuft, wird die Zukunft zeigen.

Angehängte Grafik:

1.jpg (verkleinert auf 48%)

1.jpg (verkleinert auf 48%)

Angehängte Grafik:

3.jpg (verkleinert auf 48%)

3.jpg (verkleinert auf 48%)

Angehängte Grafik:

5.jpg (verkleinert auf 48%)

5.jpg (verkleinert auf 48%)

Hoffe persönlich noch auf den Bereich $2,00 - 1,80 und würde dann dort eine erste Long-Position eröffnen.

Noch 2-3 heftige Tage und wir sind dort...?!

Abwarten, sind demnächst beide schlauer:-)))

There is an old cliché often cited by traders that attempting to catch a falling knife is an extremely dangerous thing to do, but that doesn’t mean that picking one up off the ground isn’t occasionally worth the risk. The phrase “The U.S. coal industry is dead…” has been uttered so many times in the last six months that it has become conventional wisdom. Stocks in the industry have fallen in spectacular fashion, with those companies that have avoided bankruptcy so far losing over 90 percent of their value over the last five years or so. Peabody Energy (BTU) is no exception, but at these super depressed levels BTU may represent an opportunity for nimble traders with an appetite for risk.

The fact is that the coal industry, while undoubtedly in dire straits, is not dead yet, it’s just that stocks are priced that way. That doesn’t mean that coal has a bright future, it certainly doesn’t, but if conventional wisdom is put to one side it is hard to state that it has none at all. Coal still accounts for around 40 percent of the world’s electricity, and according to the IEA, overall demand will rise through at least 2019.

Coal prices, and stock in companies that produce it, have not tumbled without good reason, however. The big drop in oil prices last year dragged all energy prices with it but coal was particularly hard hit for many reasons. Firstly, the demand outlook for coal has worsened considerably. China has cut imports massively; the total imported fell 42 percent on an annual basis in the first quarter of this year. A political push to reduce emissions, cheaper natural gas and slowing growth in the economy have combined into a perfect storm for coal in what was, until recently, the world’s fastest growing economy. Those same factors have also reduced demand in the U.S. and most of the world…with one notable exception.

India, the third largest importer of coal in the world, and now the fastest growing economy in the world according to the latest estimates, actually increased coal imports in 2014/5 by a respectable 19 percent. As India imports primarily from Australia and Asia, that is of little use to most U.S. producers, but once again with one notable exception…Peabody Energy. Around 40 percent of that company’s revenue comes from their Australian operations, so they are uniquely placed amongst U.S. producers to benefit from continued growth in India.

That alternative revenue source, combined with some aggressive action by management to cut U.S. costs earlier this month, makes Peabody a likely survivor as the industry collapses, and that, in turn, makes the 97 percent decline in the stock price look somewhat overdone. At around $2.40 at the time of writing, BTU looks like the risk reward ratio has swung in its favor. With over 30 percent of the total stock being sold short, simply a lack of bad news over the next few weeks could be enough to generate a significant rally. There is a downside, for sure, most notably if the current crisis forces a massive increase in insurance costs, but there is an awful lot of bad news priced in at these levels.

It should be stressed that this is a trade idea, not an investment. There is still an enormous amount of risk and a total loss is a possibility, so only capital set aside for high risk trading should be used. It seems, though, on examination of the evidence, that the market is overestimating the risk of bankruptcy for BTU. From a long term perspective investing in a coal company may seem like stupidity in the extreme, but this is not a long term trade. The idea is to benefit from an oversold position at these levels and a short squeeze that will almost certainly come at some point. On that basis a strong argument can be made that the knife that is BTU has already hit the floor, and picking it up here may be a smart thing to do.

By Martin Tillier of Oilprice.com

http://finance.yahoo.com/news/...-energy-btu-time-pick-221635809.html

Summary

- I bought Peabody stock as there is "blood on the streets" in the coal sector.

- The worries about the self-bonding program are overblown according to Vic Svec.

- I interview him to find out more about his company.

I have been following coal's downturn trying to anticipate when the bottom might be for a few years now. I wrote an Instablog post last year recommending the KOL (NYSEARCA:KOL) ETF, but to be honest I was using coal as an excuse to try to predict some of the Senate races. I am interested in politics, so the races intrigued me. I ended up predicting almost all of the Senate races correctly; the Republicans won the House and the Senate like I said. I never followed through on the actual investment in KOL personally as it was more of a possible idea than an actionable investment. At the end of the post I mentioned a risk factor which ended up proving to be true. I stated "The two biggest risks are that my election predictions are wrong and that the President may allow the EPA to go through with its policies without any regard for what the Congress believes." Unfortunately for coal stocks the administration's EPA has been strict on coal regulations.

It certainly has been tempting these past few years to pick a bottom in coal, but I have held back up until Wednesday. My reasoning for purchasing Peabody was I felt the lack of significant debt maturing until November of 2018 limits its bankruptcy risk. I think some investors believe the coal industry is dead which is turning a normal cyclical downturn into a black hole. Coal is not a dying technology which will be obsolete in 10 years. It is expected to power 40% of our energy usage in America next year.

The problems with coal have to do with market dynamics i.e. supply and demand. These issues generally work themselves out as companies cut production once prices decline. There was a similar decline in the late 90s as Peabody ended up being the subject of a leveraged buyout. After the stock went public again in 2001 it became one of the best performing stocks in the market. I fully expect this to happen once again. Some investors may claim "this time is different" as solar and wind power become more prevalent. This is faulty logic as coal will be heavily relied upon for decades.

The three main causes for Peabody's stock decline are regulations, competition from natural gas which has gotten much more competitive as its price has declined significantly, and declining demand from China. The argument in favor of Peabody is most of these situations will resolve themselves over time and can't get much worse. If Hillary Clinton gets elected the situation will remain the same. If a conservative Republican such as Rand Paul or Marco Rubio gets elected, we would see a significant loss of power at the EPA which would help ease the regulatory environment significantly. Most economists expect China to resume higher long term growth once its economy rebounds which would mean an increase in coal demand. Natural gas prices should move higher if America begins to export it. Natural gas supply is also being constrained as it is a byproduct of oil fracking and the rig count has declined by 60% as the price of crude has plummeted.

I bought Peabody (NYSE:BTU) because it is the world's largest private sector coal company. If I'm going to play a trend which has high risk, I'd rather do it with the highest quality company. It is a global coal company which gives it access to sell product from its mines in Australia to the fast growing Indian market.

There have been some questions about the self-bonding program recently which is the program which allows coal companies to economically insure their cleanup costs in the case of bankruptcy. I decided to do a phone interview Vic Svec, to have him explain where the market is wrong on this issue and others. According to his LinkedIn "Svec Vic is Senior Vice President of Global Investor and Corporate Relations for Peabody Energy, the world's largest private-sector coal company. Svec has executive responsibility for global advocacy, investor relations, corporate communications, reputation management, media relations, social media, crisis communications, employee communications and community relations. Svec has more than 30 years of experience in investor and public relations and joined Peabody in 1998. His previous employers include industry leaders Anheuser-Busch Companies and Brunswick Corporation."

It's a difficult thing to buy and recommend a stock which is down 97% from its peak even for a contrarian investor like myself. I felt his answers were able to quell my concerns.

Alex Pitti: My first question is about the self-bonding program. I was reading a Reuters article which stated you need a ratio of total liabilities to net worth of 2.5 times or less and a ratio of current assets to current liabilities of 1.2 times or greater. Chris Holmes, a spokesman for the Office of Surface Mining Reclamation and Enforcement was quoted as stating "Our team will examine all aspects of bonding and self-bonding." Explain why Peabody still qualifies for the program.

Vic Svec: Well Peabody's applicable subsidiaries are in full compliance with both federal and state requirements regarding self-bonding.

Alex Pitti: So why do you think there is so much investor angst about it?

Vic Svec: Well I think there's been some confusion and in some cases some intentional confusion that's been spread by misinformed stories that have been out there. Misinformed or perhaps agenda driven stories by those who those who may wish the industry ill. You also saw, I believe, a competitor who does not qualify for self-bonding and I think that created it.

Alex Pitti: Yeah kind of like a contagion effect.

Vic Svec: Yeah that's right.

Alex Pitti: Well there's a big public problem with coal. How are you trying to combat this? I saw on your website you had a "Fossil Fuels: A Moral Case" article. Have you heard of the book by Alex Epstein "The Moral Case for Fuels"?

Vic Svec: Yes. In fact Alex and I speak periodically. Peabody has launched a campaign about a year and half ago called the Advanced Energy for Life campaign. I encourage you, when you get a chance, to take a look at it. It's at AdvancedEnergyforLife.com. Essentially, it talks about the vital role that access to energy has in helping to eliminate poverty. The punishing effects of energy poverty. And then in the developed world, the vital importance of having access to low cost electricity. We have over 100 million people in the U.S. for instance that qualify for energy assistance. In this day and age that's a statistic that should alarm us and drive us all to action. Choice of fuels matter. Choice of policies matter. We believe that everything needs to be done to keep electricity abundant, reliable, and low-cost. Certainly coal fits that bill. Now I agree with you that I think the headlines have been punishing for coal, but they do ignore the fact that coal has been the fastest growing major fuel in the world over the last decade. Wood Mackenzie, the consultants, says that coal is likely to pass oil as the world's largest energy source by 2018. You have a new coal fueled plant built on average every 3 days, somewhere in the world that will provide good, low-cost electricity for years to come that have pulled hundreds of millions of people out of poverty.

Alex Pitti: The headlines are pretty terrible.

Alex Pitti: I was thinking that even though there may be a chance of a global economic recession, do you think it's possible it would spur some of the anti-coal policies to be ended because they're anti-consumer?

Vic Svec: Well I certainly think every time that we go through an economic downturn it's a reminder of how vital a fundamental staples are. Everyday items. Food, shelter, clothing, energy need to be reliable, need to be abundant, need to be abundant, need to be low-cost. That's for businesses, that's for people on fixed incomes. It's for people really across all political stripes. The concept that we could somehow do without fossil fuels would be laughable were it not for the earnestness of some of the people who advocate this. They're small, but they're very vocal. Unfortunately what they've proposed serious and would be extremely damaging to the economy, to jobs, and to individuals.

Alex Pitti: There is a small group of loud people, but the problem is that they've moved the conversation to be negative towards coal. The Chinese economy isn't looking too great. What do you predicting? Because their problems with the numbers and how reliable they are. So what do you seeing from China?

Vic Svec: Well we see China longer term. China has clearly has had some slack what has other been an economic juggernaut in recent years. There's no doubt that there's been some slack in the system there. Having said that we think China continues to have tens or maybe hundreds of millions of people move to cities, move to the middle class in coming decades and they're being joined by the Asean countries in Southeast Asia, by India itself which has passed up China as the largest, fastest growing coal importing nation. You continue to have hundreds of millions and billions of people that lack basic access to electricity and coal field electricity is a major part of that. I would also add that metallurgical coal which is a fundamental staple of steel making in the world certainly remains essential and will also help Peabody overtime.

Alex Pitti: I read that 80% of the Chinese coal plants are not profitable. You think that will continue?

Vic Svec: That may have been the actual coal producers. I think what that says is that these very low seaborne are unlikely to sustain over time. We have already seen some stabilization of seaborne prices for both metallurgical coal and thermal coal in recent days. That's largely as a result of supply having come off line to help what has been slower demand growth. As demand picks up you're likely to see peak trough kind of cycle continue to evolve on the seaborne market.

Alex Pitti: I've read on some blog sites that people are worried that even if one of your competitors goes bankrupt that they still won't be lowering their production. Do you think if your competitor goes bankrupt the supply demand/balance would become more in line?

Vic Svec: It's probably not appropriate for me to talk about competitors. Having said that, we have seen coal supply come down this year and we would expect that to continue given some of the cost pressures that are facing certainly producers that are in regions that are on the higher end of the cost curve. We would point to Appalachia for example as a region where the coal seams are very thin. The cost to get the coal out are very high and the prices are leading to a fair amount of supply cutbacks.

Alex Pitti: You're debt is trading at significantly below par value. Do you plan on buying some of it back?

Vic Svec: We'll continue to evaluate our options and deleveraging is a longer term goal for us. We're focused most immediately on cash and liquidity and we do have deleveraging as an objective overtime. We have a new CEO at the company Glenn Kellow. He's identified four major areas of emphasis. One of those is financial which goes to the point we were just discussing. One is portfolio management which is looking at sale of non-core assets. The other two areas are in SG&A and a leaner organization. You've seen us take quick recent actions on that. Then finally operational. Safe, low-cost operations we've continued to drive down capital and operating expenses and we look to do more.

Alex Pitti: Personally I wasn't following coal in the late 90s, but I was reading that from 1997-2000 was a difficult time for coal, so could you compare this time period to today?

Vic Svec: Well you're exactly right. In fact in 1998 we had a leveraged buyout of Peabody. We were heavily leveraged. The coal markets were difficult for a couple of years. And then in classic trough to peak structure, you saw the coal markets improve pretty dramatically over a short amount of time.

Alex Pitti: So how long a time would you say that was?

Vic Svec: Well I would say literally over probably a 6, 12, 18 month period you saw the markets turn fairly dramatically. While clearly Peabody stock has been very challenged over the last couple of years. In the last decade we have also been among the top 25 performers of our S&P 500 group several times during that decade showing that we can been significant outperformers at times, in addition to of course doing through some cyclical downturns.

Alex Pitti: For me as an investor, I thinking that it's a typical peak to trough scenario, but it's being exaggerated because of anti-coal media.

Vic Svec: Yeah. I think that's true and you have significant short interest in some of the coal equites as well which lead to people intentionally looking to intentionally trying to exaggerate any points of challenge out there, so we through it. At the end of the day, coal is an essential product. Peabody is the world's largest private sector coal company. We have a tremendous asset base. We got an approach towards the business that we believe will lead to longer term value creation. We think that ultimately investors will look through the noise to see the value.

Alex Pitti: You cut metallurgical coal production by 1.5 million tons per year in Queensland, Australia. How do you see the Australia market supply/demand situation playing out for met coal?

Vic Svec: We've recently seen signs of the stabilization in the spot metallurgical coal price which is probably the largest indicator of supply/demand balance. We do think that supply continues to come off in the seaborne met markets. We think Australia remains the go to source for metallurgical coal in the world. We're pleased to have a significant presence there. A very large asset base. We also are not going to push tons onto a market that isn't rewarding producers for doing so these days. And to the extent that we can maintain or reduce our cost structure while preserving our volumes for a better market time. That's our focus.

Alex Pitti: It seems that the major problem form Australia is just the currency hedging.

Vic Svec: Well that's right. What you've seen from Peabody is a set of metrics which suggests that over the next less than 2 years we have $685 million in improvement potential on annual cash outlays between our hedging on currency and fuel and also some of our fixed charges which fall away over the next few years.

Alex Pitti: There's been a few reasons for the decline in your stock and the challenging environment. Cheaper coal prices are being caused by tougher emission standards and slowing demand from China. So how are these effecting coal prices?

Vic Svic: Well I think that the decline in coal prices have caused a cyclical decline in earnings as well. We think that changes over time. We think that Peabody is taking the type of actions we need to have an organization that is competitive in all market conditions. I continue to buy Peabody stock. I know management has been buying Peabody stock as well so. We are believers in the long term. We're believers in the commodity and we're certainly believers in BTU.

Alex Pitti: How are the cheap natural gas prices causing competitive challenges for coal? So you're seeing a moderate increase in the price of natural gas over the long-term?

Vic Svec: We do see some modest increases in natural gas prices. We don't think that current levels are sustainable. You'll find ways to reinvigorate demand gas in the U.S. particularly to allow inexpensive natural gas to be exported either through pipeline or LNG to places that will pay more for it. So you will have some equilibration in the price and the product. There's a significant amount of natural gas that is produced associated with oil and that is likely to continue to come down given the oil price decline as well.

Alex Pitti: Thank you so much.

Vic Svec: Very good. I appreciate the time.

http://seekingalpha.com/article/...ng-vic-svec-of-peabody-to-find-out

Peabody Energy puts exploration assets on the block

US coal giant Peabody is selling most of its Queensland coal exploration portfolio, in what could be the first step in executing a wider exit of its Australian portfolio.

Peabody's market capitalisation has collapsed 70 per cent his year to hover at around $US685 million ($890 million) – which, notably, is less than Whitehaven's at $1.45 billion.

Street Talk understands Peabody is handling the sale of its exploration permits and will be hoping that miners, including neighbouring players in Queensland, see in it "synergies", or a cost-effective way to access low cost resources, if future market conditions are right.

It could also be a way to ease in and start testing broader appetite for Peabody's operating assets. Some industry players have suggested Peabody has designs on an exit from Australia.

Peabody's shares have retreated to $US2.45 – a far cry from the lofty heights of the coal boom in mid-2011, when its shares peaked at almost $US73. The US giant's Australian mines are lower-cost than its American operations but it is getting squeezed on the quality of its coal down under, much of which is PCI.

But the question of course, is – who would be interested in buying some or all of the Peabody mines portfolio?

The local coal market is awash with assets for sale, many of them decent, but very few sellers are distressed and deals have failed to materialise despite an extended price malaise that shows little sign of improving.

Last month, Peabody said it would shed up to 210 jobs and cut production at its North Goonyella coal mine, in north Queensland, as depressed prices for both thermal and metallurgical coal continued to deteriorate.

Glencore's mothballed United Collieries mine and Peabody's Wambo mine share a "stratified" lease, so the two miners have agreed to combine the operations (and share costs) in 2017 – provided market conditions are right.

Peabody last year also abandoned the $80 million sale of its Wilkie Creek thermal coal mine in Queensland to fallen coal baron Nathan Tinkler, when he failed to come up with the required funding.

http://www.afr.com/street-talk/...assets-on-the-block-20150618-ghqt4w

California measure to ban Peabody, Arch from investment funds advances

A bill that would require state pension funds in California to divest their investments in companies that generate at least half their revenue from coal mining has advanced in the state.

The measure, which passed an Assembly committee by a 5-1 vote on Wednesday, would require pension funds Calpers and CalSTRS to sell their investments in mining companies, Reuters reports. Calpers' coal mining investments are valued at $100 million to $200 million and include investments in both Peabody Energy and Arch Coal.

Peabody's shares fell 24 cents to close at $2.48 Wednesday, down 8.8 percent. Arch Coal fell 5 cents, or 11.1 percent, to close at 39 cents.

The bill now goes to the California Assembly Appropriations committee.

Peabody spokesman Vic Svec told Reuters that the bill was "wholly symbolic and political."

http://www.bizjournals.com/stlouis/morning_call/...ody-arch-from.html

Moody's downgrades Peabody in light of ongoing decline in met coal

OHANNESBURG (miningweekly.com) – Moody's on Friday reported that it had downgraded the ratings of NYSE-listed coal company Peabody Energy Corporation, reflecting the ratings agency’s expectation of continued deterioration in the company's credit metrics, owing to the ongoing decline in the seaborne metallurgical (met) coal markets. “The negative outlook reflects our expectation that met coal markets will remain weak over the next 18 months, while the company's Debt/ earnings before interest, taxes, depreciation and amortisation (Ebitda), as adjusted, will approach 9x in 2015,” stated Moody’s, pointing out that a ratings upgrade was unlikely. However, this would be considered if Debt/Ebitda were to approach 6x, with roughly neutral free cash flows.

Moody’s did anticipate some recovery in 2016, but still expected the leverage to remain elevated at around 7x. Alternatively, a further downgrade would be considered if liquidity deteriorated, free cash flows were persistently negative and/or Debt/Ebitda exceeded 8x on a sustained basis. Moody’s downgraded the St Louis, Missouri-headquartered company’s corporate family rating (CFR) to B3 from B2, which continued to reflect pressures on Peabody’s US thermal coal business from increased regulatory pressure and low natural gas prices.

Hier geht es weiter:

http://www.miningweekly.com/article/...decline-in-met-coal-2015-06-26