Ariad Pharma on the Top

Seite 323 von 373 Neuester Beitrag: 26.09.16 18:45 | ||||

| Eröffnet am: | 17.01.14 10:56 | von: Masterbroker. | Anzahl Beiträge: | 10.311 |

| Neuester Beitrag: | 26.09.16 18:45 | von: Masterbroker. | Leser gesamt: | 1.446.570 |

| Forum: | Börse | Leser heute: | 156 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 321 | 322 | | 324 | 325 | ... 373 > | ||||

Optionen

| Boardmail an "usambara" |

Wertpapier: ARIAD Pharmaceuticals, |

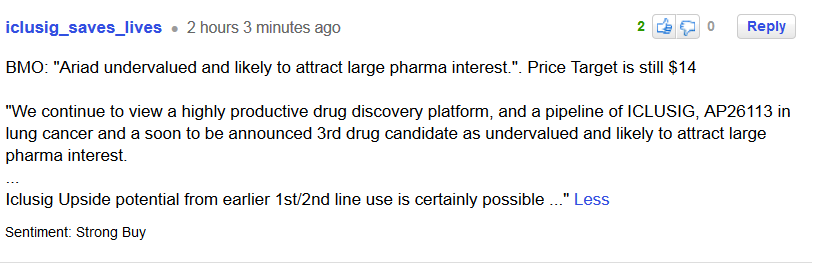

Angehängte Grafik:

bmo.png (verkleinert auf 61%)

bmo.png (verkleinert auf 61%)

Optionen

| Boardmail an "MasterbrokerUSA" |

Wertpapier: ARIAD Pharmaceuticals, |

RB: Sure. Ariad Pharmaceuticals Inc. (ARIA:NASDAQ) is a turnaround story as well. Last year the company ran into a significant snag. Ariad had the distinct pleasure of not only successfully getting Iclusig (ponatinib) approved in mid-December 2012, a full three months ahead of its Prescription Drug User Fee Act (PDUFA) date, but it also achieved regulatory approval both in the U.S. and in Europe for the drug. Iclusig was approved for third-line use in chronic myelogenous leukemia (CML). Ariad was running a head-to-head Phase 3 study against Gleevec (imatinib) in an effort to move its product toward front-line use in CML, but due to an increasing side-effect profile, including serious arterial thrombotic events and cardiovascular toxicities, the FDA suspended the marketing of ponatinib in the U.S. That led to a significant decrease in shareholder value for the company.

Subsequently, the company worked with the FDA and was able to revise its label to a more restrictive patient population, getting the drug back on the market. Most investors look at the more restricted label and think a company with a market valuation of more than $1B and a restricted label is more than fairly valued. Given the lower peak revenue potential in the $100–150 million range ($100–150M), investors perceive Ariad as an overvalued stock trading at 10 times its peak revenue potential for Iclusig. But, in our opinion, this is where the opportunity lies.

What we believe investors are missing is that Ariad has an extremely active drug with ponatinib. We know that off-label sales are occurring in the second-line CML market right now, and as more physicians get comfortable with the side-effect profile, we believe the significant activity seen with ponatinib will help increase market share in other indications—even within CML. We believe Ariad is going to grow market share beyond the third-line and fourth-line CML market. In addition, the drug is being evaluated in several other solid tumor indications.

Ariad also has a pipeline of products, including a new anaplastic lymphoma kinase (ALK) inhibitor called AP26113, which reported outstanding data in advanced malignancies at ASCO. When you think ALK inhibitors, you probably think of the two major ones, Xalkori (crizotinib; Pfizer) or Novartis' Zykadia (ceritinib). A slew of other ALK inhibitors are in development, but AP26113 seems to have generated some differentiated data, which was presented at ASCO. The data differentiates AP26113 not just in its activity, which we believe is slightly better than Novartis' Zykadia, but we also believe the side effect profile is better. Ariad's pipeline sets the company up as one of the more interesting acquisition targets in the biotechnology space.

TLSR: Ren, although Gleevec is going to lose its patent protection/exclusivity soon in the U.S., it has been the standard of care in CML for a good while. Did you hear data at ASCO indicating Iclusig could be more efficacious in CML than Gleevec?

RB: We did, actually. Ariad presented data from its Phase 3 EPIC trial, where it was evaluating ponatinib head-to-head against Gleevec. Ariad's drug showed a significantly better response rate versus Gleevec. But what Gleevec has, besides being efficacious, is a very good side-effect profile.

The question is, in the face of Gleevec going generic and having a better side-effect profile, will anyone move ponatinib to the front-line setting. That's a tough hurdle to cross, and we are not factoring that into our models at all. The EPIC trial was halted due to the marketing halt of Iclusig in CML last October. If Ariad wants to go for front-line status, it would have to run a head-to-head Phase 3 trial all over again. The data show that ponatinib is much more active than Gleevec, but it's also more toxic. Patients responding to Gleevec will continue on Gleevec. Those who don't respond have a good shot at getting exposed to ponatinib in the second-line setting, where we already see ponatinib prescriptions. A second-line label in CML would represent a triumph for Iclusig.

Optionen

| Boardmail an "dr.soldberg" |

Wertpapier: ARIAD Pharmaceuticals, |

Gut das ich mich mal diesmal durchgerungen habe und Ariad ende letzter Woche "oben" verkauft habe..

Dow könnte ja bald wieder drehen (bzw ist gerade schon dabei?) und Ariad ein wenig mit hoch ziehen..

Einen Wiedereinstieg sehe ich ich bei etwa $5,5x, was meint ihr =) ?

Optionen

| Boardmail an "weiar" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "dr.soldberg" |

Wertpapier: ARIAD Pharmaceuticals, |

...und will ja den tollen Anstieg nicht verpassen =)

Gehe mal davon aus das es nicht mehr allzu viel fallen sollte.

Optionen

| Boardmail an "weiar" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "weiar" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "MasterbrokerUSA" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "MasterbrokerUSA" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Limmin" |

Wertpapier: ARIAD Pharmaceuticals, |

http://investor.ariad.com/...Details&c=118422&eventID=5163922

Optionen

| Boardmail an "Limmin" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "AktienBaby" |

Wertpapier: ARIAD Pharmaceuticals, |

Bin gespannt wie viele bei 6.00$ / 6.01$ hinterherschmeißen...

Optionen

| Boardmail an "Lobster2014" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "MasterbrokerUSA" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Lobster2014" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "MasterbrokerUSA" |

Wertpapier: ARIAD Pharmaceuticals, |