Jinkosolar - hat die niemand auf dem Radar?

http://blogs.barrons.com/emergingmarketsdaily/...half-says-jp-morgan/

JinkoSolar-Aktie: Größter Profiteur des nächsten Solar-Booms - Kaufen mit Ziel USD 45,60

06.01.14 20:16 aktiencheck.de

Shanghai (www.aktiencheck.de) - Aktienanalyst Joseph Fong von Jefferies hat die Aktien des chinesischen Solarmodul-Herstellers JinkoSolar Holdings Co., Ltd. (ISIN: US47759T1007, WKN: A0Q87R, Ticker-Symbol: ZJS1) in einer aktuellen Aktienanalyse zum Kauf empfohlen.

JinkoSolar sei einer der ersten Solarmodul-Hersteller, die den Weg zurück in die Profitabilität geschafft hätten. JinkoSolar habe den Turnaround im zweien Quartal geschafft. Dies sei vor allem der Tatsache zu verdanken, dass JinkoSolar der Produzent mit den niedrigsten Kosten sei, so Aktienanalyst Joseph Fong von Jefferies in seiner aktuellen Aktienanalyse.

JinkoSolar werde daher zu den großen Profiteuren des nächsten Solar-Booms gehören. JinkoSolar sei auf gutem Wege die SunEdison von China zu werden. Der Solarmodulhersteller wolle bis zum Ende des Jahres 2014 Solarparks im Gesamtvolumen von 500 MW planen, entwickeln und selbst betreiben.

Aktienanalyst Joseph Fong veranschlagt das Kursziel für die JinkoSolar-Aktie auf USD 45,60. "Buy" lautet das Rating des Analysten von Jefferies in seiner ersten JinkoSolar-Aktienanalyse.

Warte wieder den Pre Market ab,ob es sich lohnt weiter mit zu fiebern,oder erstmal Kasse machen.

Eigentlich spricht nichts gegen weiter steigende Kurse.Wenn auch nicht mehr im zweistelligen Bereich.

Weiterhin viel Spass mit JKS.

das finde ich ganz ok. ähnlich wie chris sehe ich das als zeichen, dass wir im trend sind. regelhaftigkeit beruhigt mich. :)

der ungeheuerliche newslfow tut sein übrigens. ich sehe noch keinen grund für gewinnmitnahmen. noch. aber die luft ist schon sehr dünn. der newswflow könnte abreissen. und eine konsolidieren wird eh kommen.

hat schon jemand ein datum für die q4-zahlen?

http://seekingalpha.com/article/...51-chinese-solar-manufacturer-pick

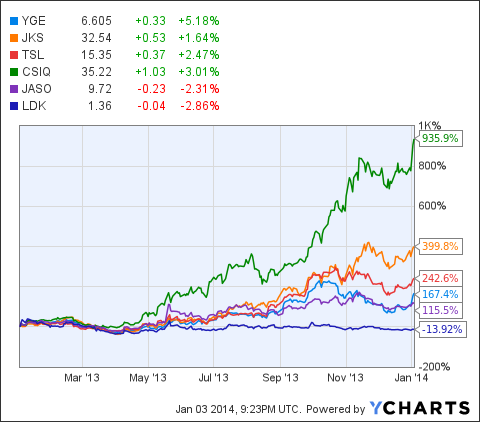

...... What I hope to do is find which of these is the most likely to survive and be successful. Let's look at just the last one year:

http://static.cdn-seekingalpha.com/uploads/2014/1/...85ace3ac974b.png

{kind=link}

Here Trina Solar (TSL), Canadian Solar, Jinko Solar (JKS), LDK Solar (LDK) and Yingli Green Energy (YGE), all stand above JA Solar (JASO).

Earnings

None of these companies are reliably profitable as there is and has been for a while, a glut of solar panel supply. ......it looks like 2011 and 2012 were really bad years for all the solar manufacturers and 2013 looks like the year where, maybe, things are turning around.

The Numbers

§Market Cap Debt Debt/Equity

Yingli $812M $2.5B 5.4

Jinko $789M $875M 2.9

Trina $985M $1.1B 1.3

Canadian $1.47B $992M 2.5

JA $369M $613M 0.87

LDK $265M $2.9B

interessant auch die Performance im letzten Jahr s.chart unten

Considering the economics, the future of solar power is bright and considering that the Chinese government is supporting all these solar companies, it is likely that most of them are here to stay.

Picking The Ones To Buy

If I were to pick favorites amongst the Chinese Solar Manufacturers, I would pick these:

Canadian Solar - Growing fast, less volatile earnings. I would be wary that the stock has had a great year already though and trades at the highest P/S amongst the companies. If buying, I would wait for dips.

Trina - Growing fast, less volatile earnings. Needs to catch up in panel efficiency but offers a better, lower degradation (only 0.5%/year) linear warranty. Stock has appreciated a lot but not as much as Canadian Solar or Jinko. Trades at a lower P/S than Canadian Solar and Jinko Solar and can potentially catch up.

Angehängte Grafik:

performance_solar.png

performance_solar.png

J.P. Morgan believes the solar industry’s fundamentals are sound, at least in the first half this year. Here are analysts Paul Coster, Mark Strouse, and Paul J Chung:

2014 should be a good year for the solar industry owing to strong demand for PV solar capacity in China and Japan, capacity constraints across tier 1 module manufacturers, stabilizing polysilicon and module prices, and improving business models. We expect 2014 to start out strong, with PV suppliers’ gross margins trending into the 15-20% range, EBIT margins ticking up into single digits, and improving balance sheet health.

However, the risk is on the second half, when new capacity or new technology, attracted to improving business conditions, could enter the market:

Risks escalate in 2H14 when new capacity could enter the market, Japanese deployments peak, and potentially disruptive next-gen technology arrives.......

J.P. Morgan has a Buy rating on First Solar and SolarCity. It does not cover the individual Chinese solar companies yet.

http://blogs.barrons.com/emergingmarketsdaily/...-morgan/?mod=BOLBlog

Jinko geht seinen Weg, und wo welche Gewinne mitnehmen freuen sich andere billiger reinzukommen.

Es bleibt bei Jinko nur eins, und das Wort heißt SPANNEND !

Optionen

| Boardmail an "Obelisk" |

Wertpapier: Jinkosolar Holdings Com |

Ist aber egal, ich Verkauf hier erst eine kleine Posi wenn die 50 $ erreicht sind !

Ob es wohl klappt?

Optionen

| Boardmail an "Eskimoo" |

Wertpapier: Jinkosolar Holdings Com |

Skorp

Optionen

| Boardmail an "Skorp" |

Wertpapier: Jinkosolar Holdings Com |

Also ich denke auch, dass es erstmal eine Korrektur gibt, dabei sehe ich zwei Gaps.

Das erste Gap ist ist vom 3.1.2014 zum 6.1.2014 und das zweite Gap ist vom 26.12.2013 zum 27.12.2013.

Das erste Gap liegt bei 32,5$ und das zweite Gap bei 28,25$, was auch relativ eng am GD20 und GD50 liegt.

Ich denke, dass erste Gap sollte problemlos geschlossen werden. Das zweite Gap sollte bei einer mittelfristigen Korrektur das Ziel sein.

Angehängte Grafik:

chart_08012014-1406.png (verkleinert auf 43%)

chart_08012014-1406.png (verkleinert auf 43%)

Das ist wohl der Herdentrieb,bei den Zockern.

Bin auch etwas nervös und bedaure,nicht wie andere schon gestern,Kasse gemacht zu haben.

Werde noch etwas warten,aber dann reagieren....