Facebook der Anfang vom Ende der Tulpen-Hausse?

Ich bin gespannt....dieser Markt ist halt weit mehr umkämpft, als manche denken. Außer FB kauft noch paar Messenger auf :D

Optionen

| Boardmail an "Buchloe" |

Wertpapier: Meta Platforms Inc |

So, whatsapp?

Optionen

| Boardmail an "Fred vom Jupiter" |

Wertpapier: Meta Platforms Inc |

User-Zahl werden auch die Whatsapp-Alternativen für Google, FB, etc. wieder interessant...

FB kann nur noch an sich selbst scheitern. Nicht mehr an den Marktbegleitern und Schwankungen der User-Zahlen, Genauso wenig wie andere Riesen z.B. Amazon, Google, Apple, etc., die nicht mehr aufzuhalten sind.

Optionen

| Boardmail an "georch" |

Wertpapier: Meta Platforms Inc |

:-)

Optionen

| Boardmail an "georch" |

Wertpapier: Meta Platforms Inc |

Optionen

| Boardmail an "Fred vom Jupiter" |

Wertpapier: Meta Platforms Inc |

Optionen

| Boardmail an "georch" |

Wertpapier: Meta Platforms Inc |

@Jupiter

Microsoft, the world’s largest software maker, paid $8.5 billion to buy Skype in 2011 to add the most popular Web-calling service, targeted at consumers. Skype had about $800 million in sales when Microsoft acquired the company.

Microsoft Corp.’s Skype unit, which includes Lync software for corporate instant messaging and Internet calling, is approaching $2 billion in annual sales.

http://www.bloomberg.com/news/2013-02-19/microsoft-s-skype-unit-approaching-2-billion-in-annual-revenue.html

Wen Windows weiter abgrasst und sich auf Augenhöhe im Smartphone etabliert.....und skype integriert wird....

http://www.pocket-lint.com/news/126828-windows-phone-continues-to-claw-smartphone-market-share-as-apple-loses-ground

Facebook the next Netscape or the next Google?

So Skype is now the Robin Hood of voice traffic, taking from rich telcos and giving to... itself. And its customers. Fair enough. That's the free market.

Still, I wonder if Microsoft benefits much from owning a big stake in a depreciating asset (voice), one that brings with it a host of data privacy issues. Again, video may well prove to be the winning bet, with instant video communications popping up around Word documents and PowerPoint files.

But come on: do you really want that?

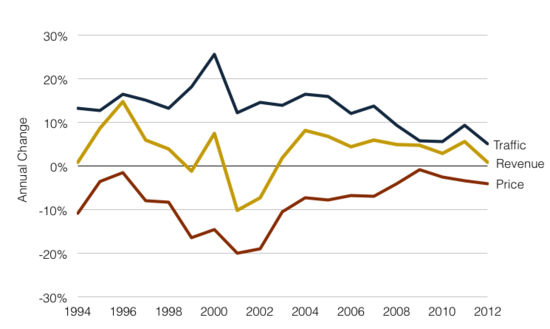

http://readwrite.com/2013/03/08/...now-commands-1-3-of-a-dying-market

http://www.telegeography.com/page_attachments/...xecutive_summary.pdf

https://www.dri.co.jp/auto/report/telegeo/images/price-vs-volumes.png

{kind=link}

WeChat hat eine Kooporation mit Lionel Messi.

Ich würde gerne wissen wie viel Geld die dafür ausgeben haben müssen.

FB bekommt bald den Papst als "Werbeträger", weil er bald ein eigenes FB-Profil erhalten wird und dafür muß FB sicher nichts bezahlen :)

Sie sind schon und werden heute noch sehr steigen. Auf ca. 60-65€. Aktuell schon 2,3€ im Aufwind heute, nach 15:30Uhr gehts ab nach Süden. Gruß

Ps.: Hatte recht mit meinem Wechsel zu YY!

Co issues upside guidance for Q1, sees Q1 revs of RMB 625-635 mln vs. RMB 540.00 mln Capital IQ Consensus Estimate.

"In the fourth quarter, not only we were able to exceed our expectations on both the top and bottom line growth, but we also further increased our profitability with non-GAAP net margin expanding to 35.4% from 22.0% a year ago. These results were driven by the greater operating leverage of our platform, which has increasingly been able to attract and engage massive audiences in a cost-effective manner through viral online marketing as well as self-promotions by performers and channel owners within our platform. We believe that YY has significant potential to become an even more powerful, pervasive and profitable platform through the ongoing diversification and expansion of our entertainment and education services."

Es is nicht zu spät einzusteigen, da komm noch viel mehr.

Ich bin bei 61,8€ rausgegangn, leider zu früh!

Ich denke jetzt kommen Gewinnmitnahmen und ich warte auf Einstieskurse.

Schaut mal im Forum bei YY, da steht viel wissenswertes über die Aktie.

FB is auch super, aber YY ist besser u. steigt schneller.

Gruß

diesmal möchte ich auch dabei sein (langfristig)

Habe Faktor 3 gekauft.

by VW StaffMarch 10, 2014, 1:30 pm

TwitterFacebookLinkedInGoogle+Email

UBS Global Research analysts Eric J. Sheridan, Vishal J. Patel and Timothy E. Chiodo rate Facebook Inc (NASDAQ:FB) as a Buy as they run the company through a series of Q1 checks.

Q1 checks reflect continuing pricing strength

Our Q1 advertiser channel checks suggest that the pricing strength exhibited in Q4 (+92% YoY price-per-ad) has carried over into early 2014 and is likely sustainable for longer than our prior estimates had assumed. In particular, we note the improved quality of advertisers & increased frequency of higher CPM formats (mobile app ads in particular) within the existing ad load. We also point to an Ogilvy study highlighting declines in organic page reach (from ~12% in Oct to ~6% in Feb), which we believe is acting as an impetus for greater ad spend as brand advertisers seek to maintain their audience – outsized ROIs on FB are more than sufficient to justify this greater spend.

Recent advertising deals show traction with brands

Facebook Inc (NASDAQ:FB) is gaining increased traction with brands, who view the platform as a means to buy audience/reach (based on our conversations). In particular, we highlight the global partnership announced by Mondelez International – the agreement covers 52 countries & includes a joint commitment to innovation, opportunities to opt into Facebook’s beta-testing programs, access to research and capability building through immersion days in priority markets. Separately, AdAge reports that Omnicom has signed a $100mm deal to roll out paid advertising on Instagram on behalf of its brand clients. That said, we believe our estimates are achievable without a meaningful contribution from Instagram or auto-play video ads.

Increased operating estimates partially offset by dilution

Our new FY14 ests are revs $11.9b (from $11.1b); Adj. EBITDA $7.4b (from $6.8b), Adj. EPS $1.25 (from $1.27). Our new FY15 ests are now revs $16.0b (from $14.0b); Adj. EBITDA $10.2b (from $8.6b), Adj. EPS $1.80 (from $1.67).

Facebook’s valuation

Our $90 price target (prior: $72) for Facebook Inc (NASDAQ:FB) is based on our weighted avg. framework (EV/Sales, EV/EBITDA, EV/FCF) based on our ’13-’15 ests. Our ests do not reflect revenue & EBITDA from WhatsApp (as the deal has not closed) but account for the expected share count dilution – an approach we consider conservative.

Beispiele, langfristig:

Google von 100 auf 1200 rauf

Yahoo von 1 auf 40

MS von 0.17 auf 37

was macht es da aus, wenn du die ersten 100% verpasst hast ?

Einer auf Yahoo hat geschrieben: Mitte Jahr 90, Ende Jahr 120 Endziel 500 :-)

Who knows ????

FB Citigroup upgrades to $85 target. Should be a nice day today.

Last updated: March 10, 2014 8:54 pm

Facebook gains on analyst optimism

By Eric Platt in New York

©Alamy

Facebook climbed on Monday as analysts at UBS raised their price target on the world’s largest social networking site to $90, the highest so far from an investment bank.

UBS’s optimism comes from signs, the analysts say, that Facebook has the muscle to increase its advertising rates, including a recent deal signed with advertising agency Omnicom worth as much as $100m.

“Our first-quarter advertiser channel checks suggest that the pricing strength exhibited in Q4, up 92 per cent year on year, price per ad, has carried over into early 2014 and is likely sustainable for longer than our prior estimates had assumed,” UBS analyst Eric Sheridan said.

Shares in Facebook, which tumbled in the months after its botched IPO in May 2012, have surged 30 per cent this year and Wall Street has warmed to the company. Today, more than eight in 10 analysts rate Facebook with a buy rating, compared with roughly half one year ago.

The company now generates most of its advertising revenue from ads on mobile phones. Rivals such as Yahoo’s Tumblr have adopted its format of showing ads in user news feeds.

Mr Sheridan said shares could go as high as $112 in the next year on “faster than expected advertiser acceptance” of new commercial formats, including video and Instagram-centred ads.

“In particular, we note the improved quality of advertisers and increased frequency of higher CPM formats – mobile app ads in particular – within the existing ad load,” he said.

Facebook shares rose 3.2 per cent by the close to $72.03, a fresh record high

==================================================

Wo soll FB denn Deiner Meinung nach hin und wie hoch müssen dafür Buchwert und Gewinn dann sein? Microsoft als mittlerweile "ausgewachsenes" Unternehmen hat ein KGV von 15 oder so, also ganz normal halt. FB hat jetzt >50. Also muss FB jetzt schon ordentlich wachsen um dann als ausgewachsenes Unternehmen ok bewertet zu sein, wenn der Kurs noch weiter steigt nur nochmehr.

Also, mach was du magst, ich wollte nur darauf aufmerksam machen, dass du hier einer eher naiven, "kleinanlegertypischen" Denke auf den Leim gehst.

Weiter oben hab ich's ja geschrieben, Einsatz der Portokasse, voraussichtlich sehr langfristig.

Werde mir erlauben, positive Meldungen weiterhin zu posten.

Rein Virtuelle Werte !

In 2013 hatten sie einen Jahresumsatz von 7,9 Milliarden USD

Nehmen wir mal an, Sie erreichen 2014 einen Umsatz von 10 Milliarden USD

Dann wäre eine Börsen-Bewertung von 40 Milliarden USD wohl mehr als ausreichend.

Aktuell ist FB ca. 175 Milliarden USD wert.

Zwischen 15-20 USD wäre die Aktie absolut korrekt bewertet.

Alles was darüber hinaus geht, ist heisse Luft.

Optionen

| Boardmail an "Pendulum" |

Wertpapier: Meta Platforms Inc |