Uran Forum

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

A stealth #uranium bull market is underway. After a decade of low prices, the uranium spot price has surged 80% over the past 10 months to over $100 per pound. However, mining equities have yet to reflect this new reality, presenting a window for investors to profit enormously from the coming supply squeeze.

1. Nuclear Reactor Construction Booming

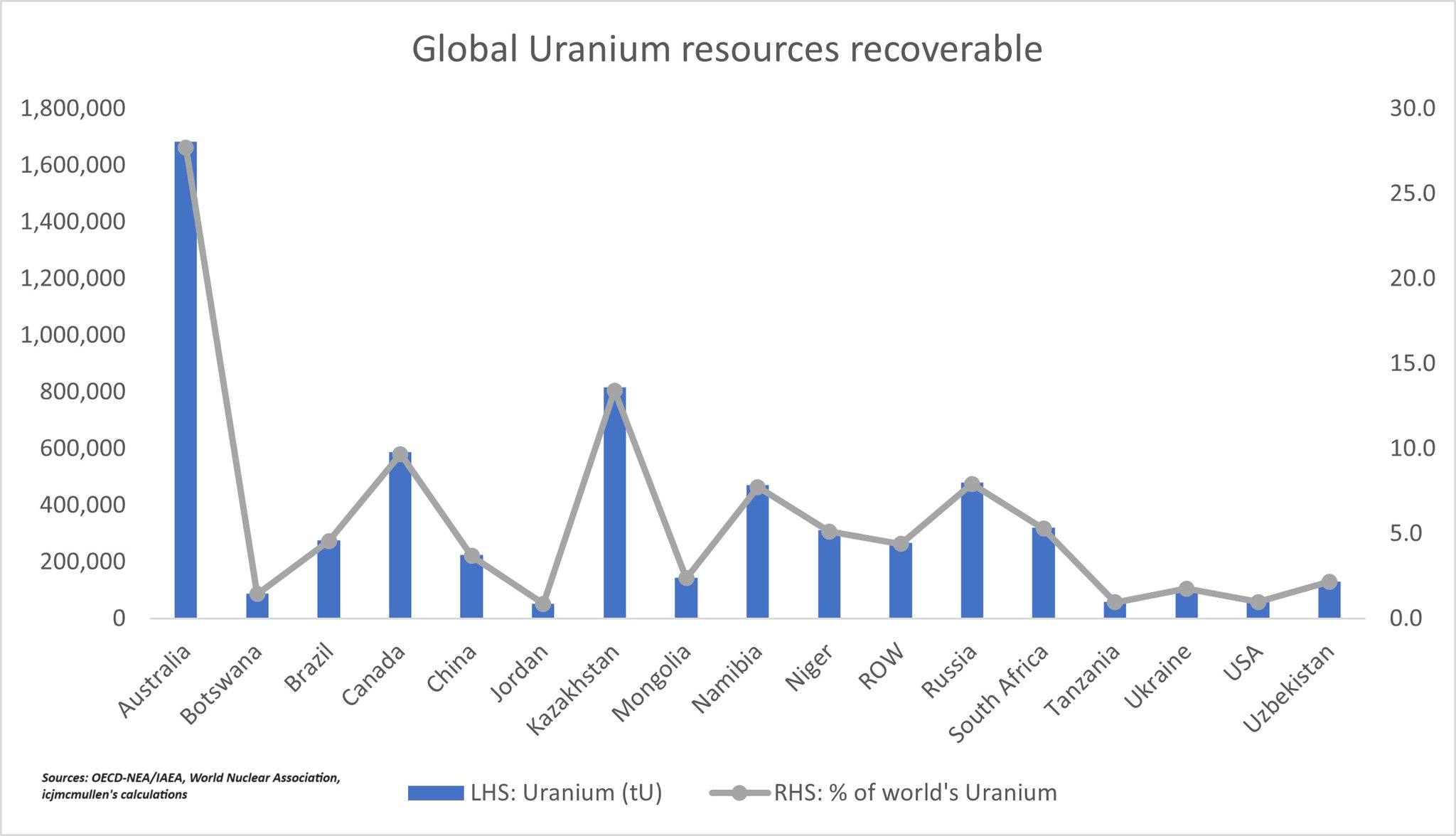

Over +50 new reactors are under construction globally, concentrated in China and Asia. These will require a major uranium supply to fuel decades of electricity generation. China & US must lock-up contracts now to secure future needs as demand swamps stagnant mine output.

2. Chronic Underinvestment in New Mines

The 2011 Fukushima tsunami scared uranium explorers and developers. New mine investment dried up with low prices. But with reactors being built, sub $30 prices were unsustainable. Margins are improving to incentivize production, but few advanced projects exist to fill widening shortfalls as secondary supplies decline.

3. Inventory Stockpiles Shrinking

Utilities and speculators have consumed inventories, leaving thin buffers. Uncovered demand now pressures primary production. Further inventory liquidation exacerbates volatility.

4. Supply Shock Catalysts Mount

Mines face depletion while legacy long-term deals from the bull market end. Top global producer Kazatomprom’s output cuts remove 25 million lb through 2024. More losses loom with contract expiries. Supply shocks type stories.

5. Equities Severely Undervalued

Miners must rally huge just to restore historical fair-value ratios relative to rising uranium prices locked-in by utilities. Juniors possess the greatest leverage from exploration discoveries as sentiment shifts. Deep value persists after early 2023 gains.

Uranium equities look ready to rip given demand increasing against unreliable capacity. Nuclear power is essential for global emissions reductions. Investors have an extraordinary opportunity to buy into this narrative before market comprehension. The supply/demand trajectory suggests at least a doubling from current spot levels exceeding 2007’s prior peak. Stocks should offer multiples of that move. Consider having uranium equities in your investment portfolio.

https://x.com/CruxInvestor/status/1754943445540479066?s=20

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

img_0940.png (verkleinert auf 70%)

img_0940.png (verkleinert auf 70%)

https://www.youtube.com/watch?v=Mb9KS76PhIM

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

bildschirmfoto_2024-02-07_um_13.jpg (verkleinert auf 18%)

bildschirmfoto_2024-02-07_um_13.jpg (verkleinert auf 18%)

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

gft6usxxkaacktg.png (verkleinert auf 32%)

gft6usxxkaacktg.png (verkleinert auf 32%)

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

bildschirmfoto_2024-02-07_um_13.jpg (verkleinert auf 16%)

bildschirmfoto_2024-02-07_um_13.jpg (verkleinert auf 16%)

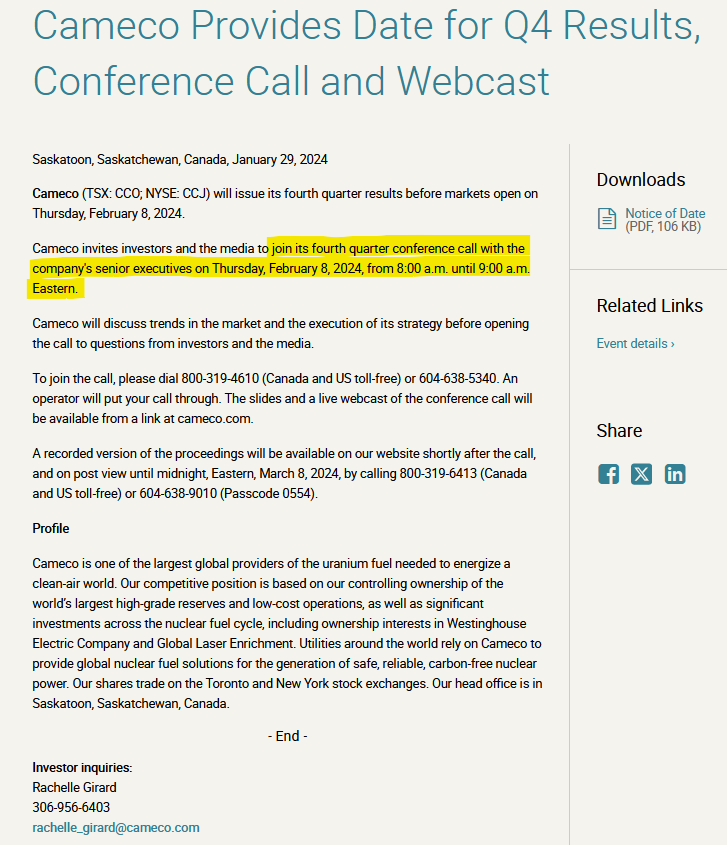

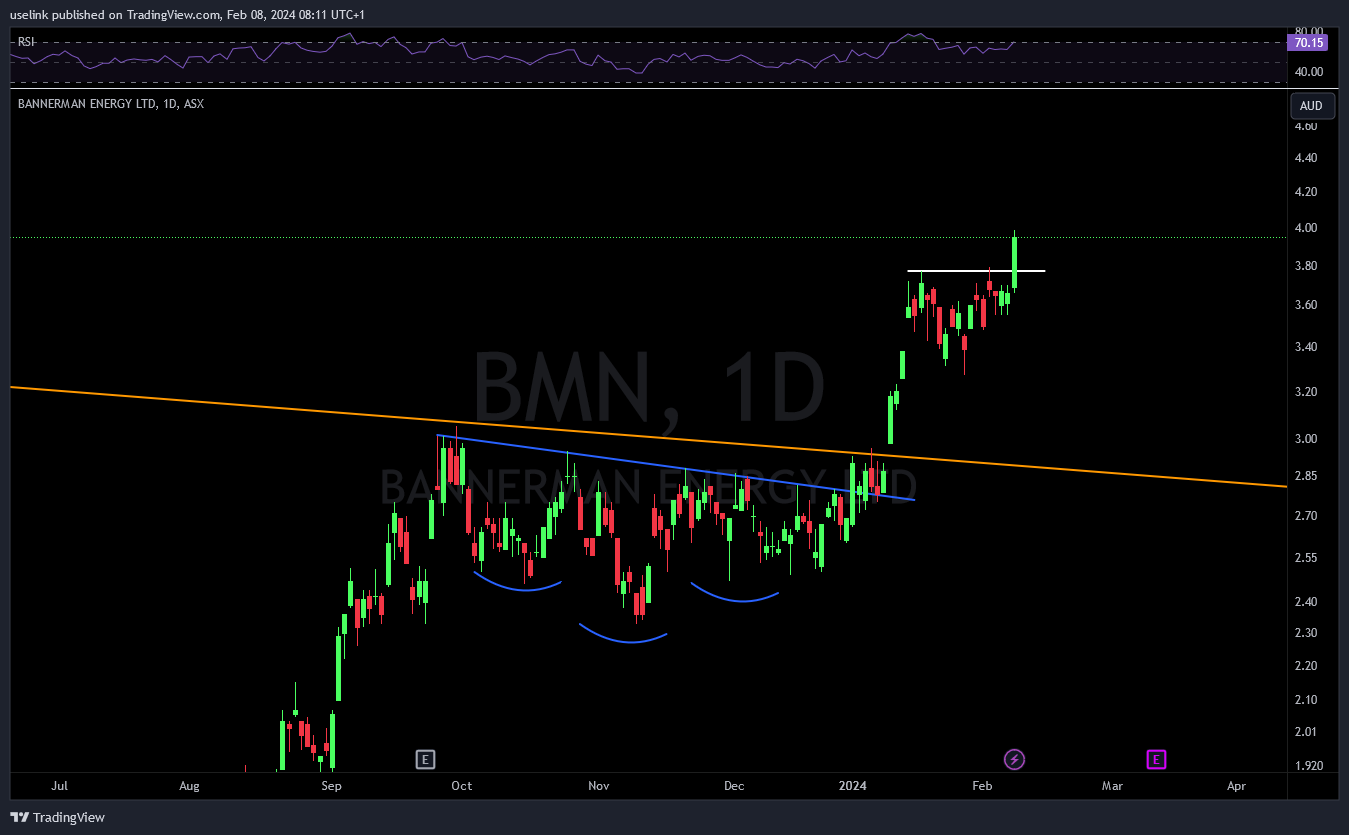

Wann geht denn Bannerman in Produktion?

Beste Grüße

Falls Cameco Produktionsengpässe verkündet wird es bei den Minen scheppern. Jute Nacht

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

img_0946.jpeg (verkleinert auf 24%)

img_0946.jpeg (verkleinert auf 24%)

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

img_0947.png (verkleinert auf 37%)

img_0947.png (verkleinert auf 37%)

https://laramide.com

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

bildschirmfoto_2024-02-08_um_10.jpg (verkleinert auf 16%)

bildschirmfoto_2024-02-08_um_10.jpg (verkleinert auf 16%)

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

bildschirmfoto_2024-02-08_um_11.png (verkleinert auf 82%)

bildschirmfoto_2024-02-08_um_11.png (verkleinert auf 82%)

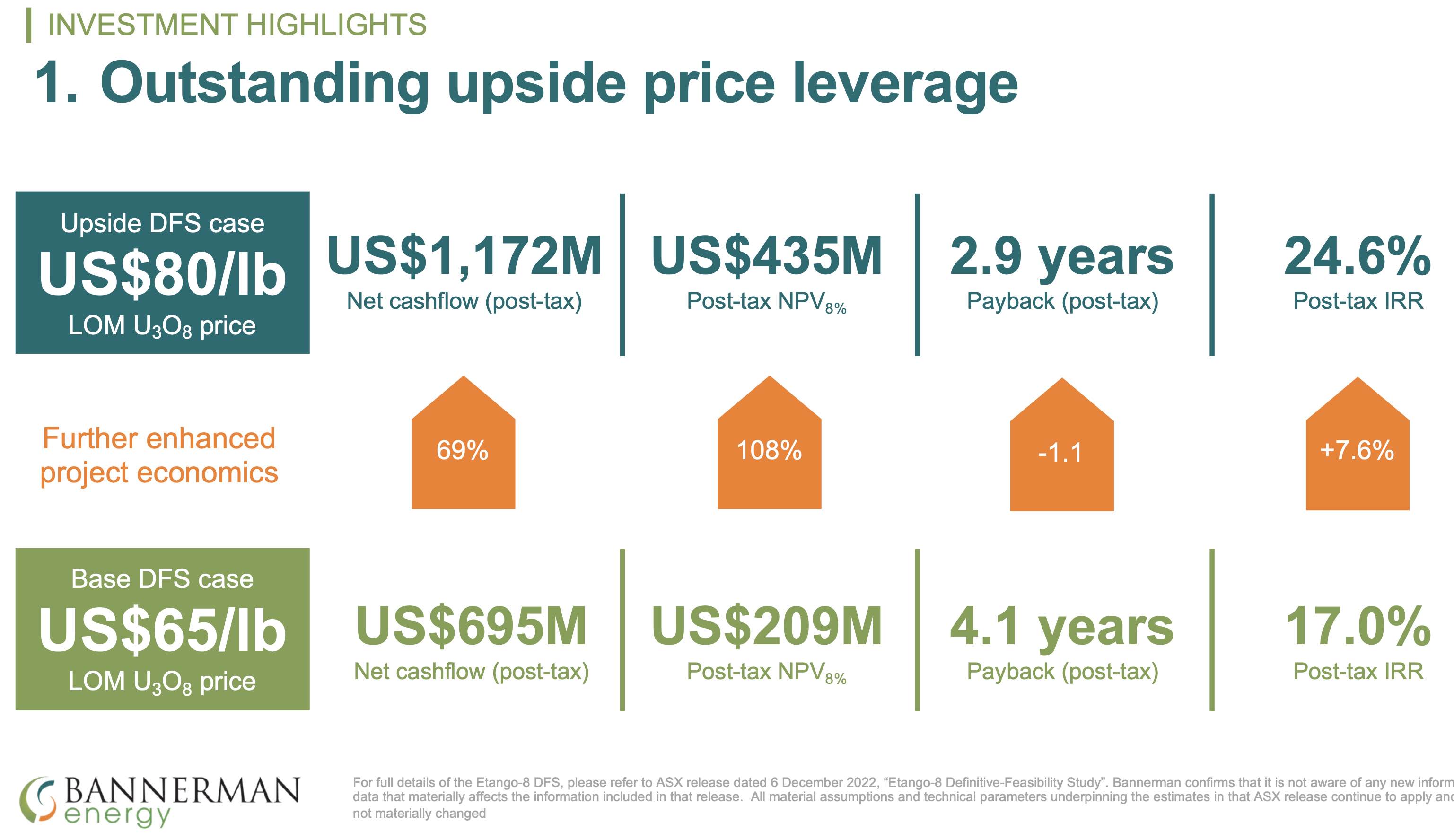

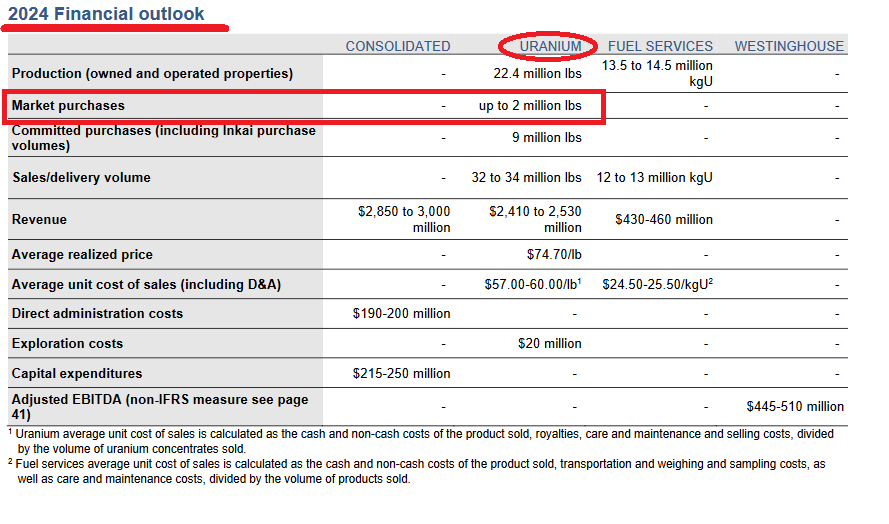

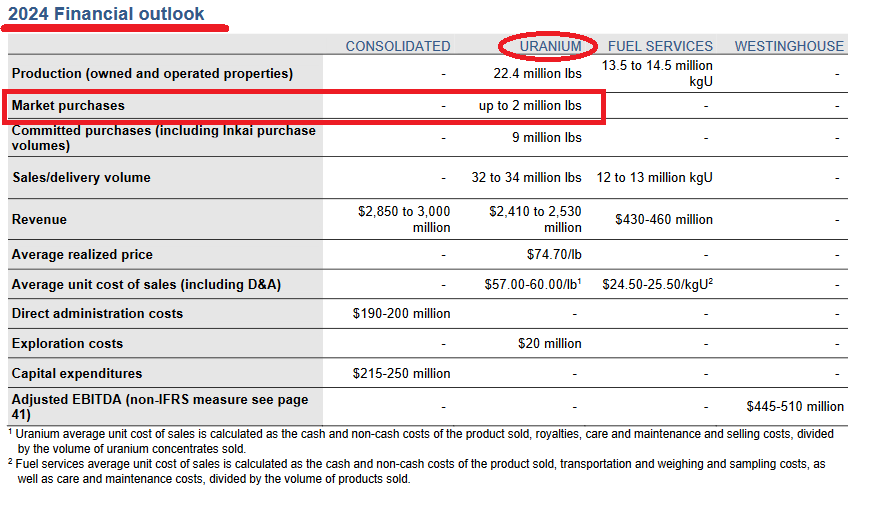

Positiv ist, dass sie ihr revidiertes Produktionsziel 2023 nochmals verfehlt haben.

Angehängte Grafik:

screenshot_2024-02-08_at_13-10-50_cco-....png (verkleinert auf 57%)

screenshot_2024-02-08_at_13-10-50_cco-....png (verkleinert auf 57%)

The September 2023 revision was already down 2.7 Mlbs (100% basis) for Cigar Lake and McArthur River/Key Lake production.

I have tried to convert everything on 100% basis:

Initial 2023 production target: 33 Mlbs (18 + 15)

September revision: 30,3 Mlbs (16,3 +14)

Actual 2023: 28.4 Mlbs (15 + 13,4)

Assuming 54.4 % ownership Cigar Lake and 70% ownership McArthur River

I do not see a miss of the September revision being priced in by the market in av very high degree.

20 minutes left until the presentation...

https://x.com/gjermundgroven/status/...6&t=luJBTDwxNH0u_oaa7JzNtA

Präsentation kommt noch gleich!

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

https://twitter.com/casperj33081634/status/1755576462999011692

Investing.com

Veröffentlicht am 08.02.2024 12:45

Investing.com - Cameco (NYSE: CCJ) hat im vierten Quartal ein EPS von 0,21$ gemeldet, 0,03 $ mehr als die Analystenschätzung von 0,18$.

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Kazatomprom GDR |

Angehängte Grafik:

img_0955.png (verkleinert auf 57%)

img_0955.png (verkleinert auf 57%)

Danke die vorab.

1 Nutzer wurde vom Verfasser von der Diskussion ausgeschlossen: silverfreaky