der Euro/Dollar Long Thread

Seite 47 von 173 Neuester Beitrag: 25.04.21 10:13 | ||||

| Eröffnet am: | 15.05.04 15:07 | von: börsenfüxlein | Anzahl Beiträge: | 5.304 |

| Neuester Beitrag: | 25.04.21 10:13 | von: Mariejpgpa | Leser gesamt: | 272.698 |

| Forum: | Börse | Leser heute: | 15 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 44 | 45 | 46 | | 48 | 49 | 50 | ... 173 > | ||||

Was bitte schön sollte das bringen?

In dem Artikel geht man davon aus das die entsprechenden Verantwortlichen hier Vermögen bis dahin in Sachwerte angelegt haben und sie eine Abwertung des Geldes nicht so stark bzw. überhaupt nicht treffen würde.

Fakt ist aber das auch Sachwerte an die Währung gekoppelt sind.

Was nützen mir die Sachwerte(Imobilien, Rohstoffe usw.) wenn niemand mehr das Geld hat sie zu bezahlen?

Aus der Geschichte sollten wir gelernt haben das Weltwirtschaftskrisen und zu starke Inflation nur zu einem führen:

Krieg!!!!!

Und dann sind Sachwerte auch nutzlos.

ciao

aber ich habs ja auch schon oben angedeutet; solche Artikel haben natürlich einen wahren Kern in sich und sind ganz nett zu lesen...aber einen wahren Crash wird es bei den wichtigen Indizes und Währungen, meiner Meinung nach, niemals geben; weil einfach zu viel auf dem Spiel steht...

wenn man bedenkt, dass die Amis künftig zB. ihr Pensionssystem noch mehr über den Aktienmarkt finanzieren wollen, dann kann man sich ausmalen, dass der S&P500 (Dow) durch irgendwelche "Kontrollmechanismen" (wie das genau funktioniert hab ich nach über 10 Jahren Börse noch nicht herausgefunden...) immer vor dem Absturz bewahrt werden...künftig wohl noch mehr als in der Vergangenheit.

das gleiche gilt wohl auch für Euro/$ und Yen (künftig auch Yuan)...

kurz gesagt: die richtig schweren Jungs (inklusive Politik; diverse Finanzgruppierungen) , die sich ja gegenseitig die Bälle zuspielen und zig Milliarden an der Börse verdienen, werden ALLES nötig unternehmen um dieses System weiter aufrecht zu erhalten...

ob das ganze nun "fair" ist oder noch etwas mit "volkswirtschaftlichen Prinzipien" zu tun hat ist ne andre Frage

füxleinsmeinung;

Aber eins ist auch gewiss, wenn ein kleiner Teil der Weltbevölkerung immer reicher wird, während die anderen immer ärmer(relativ gesehen) werden führt das zu Missgunst und Neid.

Also so wie es in dem Artikel von Corypheana steht, wäre die Schere dann so groß das sich diese Emutionen irgentwie entladen müssen.

Wie das dann genau aussieht, weiss ich auch nicht.

ciao

Stephen Roach (Tokyo)

In all my years in this business, never before have I seen a central bank attempt to spin the debate as America’s Federal Reserve has over the past six or seven years. From the New Paradigm mantra of the late 1990s to today’s new theories of the current-account adjustment, the US central bank has led the charge in attempting to rewrite conventional macroeconomics and in making an effort to convince market participants of the wisdom of its revisionist theories. The problem is that this recasting of macro is very self-serving. It is a concentrated effort on the part of the Fed to exonerate itself from the Original Sin of failing to address asset bubbles. The result is an ever-deepening moral hazard dilemma that poses grave threats to financial markets.

I am not a believer in conspiracy theories. But the Fed’s behavior since the late 1990s is starting to change my mind. It all began with Alan Greenspan’s worries over “irrational exuberance” on December 5, 1996, when a surging Dow Jones Industrial Average closed at 6437. The subsequent Fed tightening in March 1997 was aimed not only at the asset bubble itself, but at the impacts such excessive appreciation in equity markets were having on the real economy -- consumers and businesses alike. It was a classic example of the Fed playing the role of the tough guy -- the central bank that, to paraphrase the words of former Chairman William McChesney Martin, “takes away the punchbowl just when the party is getting good.” Unfortunately, the tough guys weren’t so tough after all. Predictably, there was a huge outcry on Capitol Hill as the Fed took aim on the US stock market. But rather than stay the course as an independent central bank should, the Fed ran for cover in the face of political criticism. Not only were its initial bubble-containment efforts put aside, but Alan Greenspan went on to champion the notion of a sea-change in the macro climate -- a once-in-a-century productivity miracle that would justify the stock market’s exuberance as rational. That was the Original Sin that has since been compounded in the years that have followed.

Out of that pivotal moment in the late 1990s, a New Economy actually did come into being. But it was not the new economy of ever-accelerating productivity growth that infatuated the New Paradigm Crowd and legions of equity-market speculators. Instead, it was the Asset Economy that enabled consumers and businesses to draw on the pixie dust of a new source of purchasing power -- asset appreciation -- as a means to augment what has since turned into a stunning shortfall of organic domestic income generation.

Unfortunately, the asset-based spending model has given rise to many of the distortions and imbalances evident in the US today. That’s especially true of low saving rates, the housing bubble, high debt loads, and a runaway current account deficit. When the equity bubble burst, asset-dependent American consumers barely skipped a beat. Courtesy of an extraordinary shift to monetary accommodation, the pendulum of asset depreciation quickly swung into property markets; US house-price inflation has since surged to a 25-year high. To the extent that equity extraction from ever-rising property appreciation was viewed as a substitute for organic sources of labor income generation, hard-pressed consumers went deeply into debt to monetize the windfall. As a result, household sector indebtedness surged to nearly 90% of US GDP -- an all-time record and up over 20 percentage points from levels in the mid-1990s when the Asset Economy was born. Secure in the asset-driven spending posture that resulted, consumers saw no need to save the old-fashioned way out of earned labor income. That’s why the personal saving rate has collapsed and currently stands near zero. Asset-based consumption is also at the core of America’s current-account problem. In an income-based accounting framework, the “missing saving” has to come from somewhere. In this case, that “somewhere” is the foreign saver -- giving rise to the current-account and trade deficits required to attract the foreign capital. As a result, the US current-account gap probably exceeded 6.5% of GDP in the first quarter of 2005 -- easily another record and well in excess of the 4% deficit prevailing in the mid-1990s.

This whole story, in my view, remains balanced on the head of a pin of absurdly low real interest rates. And the Fed has certainly been pivotal in nurturing this low-interest-rate regime. In an extraordinary display of policy accommodation, the real federal funds rate is only now moving above the zero threshold after having spent three years in negative territory. Of course, a central bank has little choice to do otherwise if it has made a conscious decision to underwrite the Asset Economy. After all, it takes low interest rates to provide valuation support to most financial assets -- initially stocks, then bonds, and now property. Furthermore, it takes low rates to make refi debt -- and the equity extraction it sponsors -- look attractive from a carrying cost perspective. Low rates also discourage income-based saving by underscoring the paltry returns available to savers in traditional asset classes. A migration to riskier assets -- such as property and “spread” products (i.e., high-yield and emerging market debt) -- is encouraged as a result. And low real rates make it easier to finance an ever-widening current-account deficit -- especially if the incremental flows come from foreign central banks, where there is reason to tolerate subpar returns in exchange for currency competitiveness. In short, without low real interest rates, the Asset Economy -- and all of its inherent imbalances and excesses -- is nothing.

The Fed is not only hard at work in the engine room in keeping the magic alive with a super-accommodative monetary policy but is has also become the intellectual architect of the New Macro. Time and again, since Alan Greenspan rolled out his New Paradigm theory in the late 1990s, senior Federal Reserve policy makers have taken the lead role as proselytizers of a new macro spin that condones the saving, debt, property bubble, and current-account excesses of the Asset Economy. The examples are far too numerous to mention, but consider the following highlights:

* Chairman Greenspan has made light of traditional measures of household indebtedness -- even going so far as to urge consumers to move from fixed to floating rate obligations (see his February 23, 2004, speech, Understanding Household Debt Obligations. Note: All references are to speeches available on the Fed’s website at www.federalreserve.gov).

* Fed governors have also borrowed a page from the Roaring 1990s in denying the possibility of a housing bubble (see Chairman Greenspan’s October 19, 2004, speech, The Mortgage Market and Consumer Debt, and Governor Kohn’s April 1, 2004, speech, Monetary Policy and Imbalances).

* More recently, an army of senior Fed officials -- namely, Chairman Greenspan, Vice Chairman Ferguson, and Governors Bernanke and Kohn -- have unleashed a veritable broadside against the time-honored notion of the current-account adjustment (see their various 2005 speeches, especially Governor Kohn’s April 22 speech, Imbalances and the US Economy, Vice Chairman Ferguson’s April 20 speech, U.S. Current Account Deficit: Causes and Consequences, and Chairman Greenspan’s February 4 speech, Current Account).

* Governor Bernanke has also led the charge in coming up with a new theory of national saving -- that the United States is actually doing the world a favor by absorbing a so-called glut of global saving (see his April 14, 2005, speech, The Global Saving Glut and the U.S. Current Account Deficit); Vice Chairman Ferguson has been on a similar wavelength in dismissing concerns over subpar personal saving (see his October 6, 2004, speech, Questions and Reflections on the Personal Saving Rate).

Is this is an appropriate role for a central bank? In my view, absolutely not. The problem with an activist central bank is that decision makers in the real economy -- consumers and businesspeople alike -- mistake the Fed’s point of view for strategic advice. And so do financial market participants. After hearing the Fed pound the table, consumers feel left out if they don’t spend their housing equity. Business managers felt equally deprived in the late 1990s if their companies didn’t achieve the dotcom-type valuations in the stock market that Chairman Greenspan insisted in the late 1990s and even early 2000 were well grounded in a once-in-a-century productivity miracle. The resulting overhang of excess IT spending was a direct outgrowth of this perceived deprivation. Needless to say, when investors and financial speculators saw the equity train leave the station and the Fed condone the high growth of a productivity-led economy by leaving interest rates low, they saw no reason to believe that a bubble was about to burst. When consumers hear from a Fed chairman that it makes little sense to take on fixed rate debt, they rush to floating rate instruments; not by coincidence, the adjustable rate portion of newly originated mortgage debt shot up in the immediate aftermath of Chairman Greenspan’s comments on consumer indebtedness. And should asset-dependent, saving-short, overly indebted American consumers feel at risk if the Fed assures them that there is no housing bubble -- that the asset-based underpinnings of their decision making are well grounded? A record consumption share in the US economy -- 71% of GDP since 2002 versus a 67% norm over the 1975 to 2000 period -- speaks for itself.

The rhetorical flourishes of America’s central bankers have dug the US economy -- and by definition, a US-centric global economy -- into a deep hole. To this very day, the Fed has never confessed to the Original Sin of condoning the equity bubble. On the contrary, Greenspan & Company have been on the defensive ever since by dismissing the increasingly dangerous repercussions of the original post-bubble shakeout. Far from playing the role of the tough guy that is required of independent central bankers, the Fed has become an advocate of the easy money of a powerful liquidity cycle. One bubble has since begotten another -- from equities to bonds to fixed income spread products (i.e., emerging market and high-yield debt) to property. And financial markets have gone along for the ride -- not just in the US but also around the world as global investors and foreign central banks have rushed with reckless abandon to finance America’s record current-account deficit.

The day is close at hand when US monetary policy must get real. At a minimum, that will require a normalization of real interest rates. Given the excesses that now exist, it may even require a federal funds rate that needs to move into the restrictive zone -- possibly as high as 5.5%. Yes, this would cause an outcry -- perhaps similar to that which occurred in the spring of 1997 on the occasion of the Original Sin. But in the end, there may be no other choice. Fedspeak has taken us into the greatest moral hazard dilemma of all -- how to wean an asset-dependent system from unsustainably low real interest rates without bringing the entire House of Cards down. The longer the Fed waits, the more perilous the exit strategy.

füx

xpfuture

Angehängte Grafik:

EUR-USD_16.png (verkleinert auf 85%)

EUR-USD_16.png (verkleinert auf 85%)

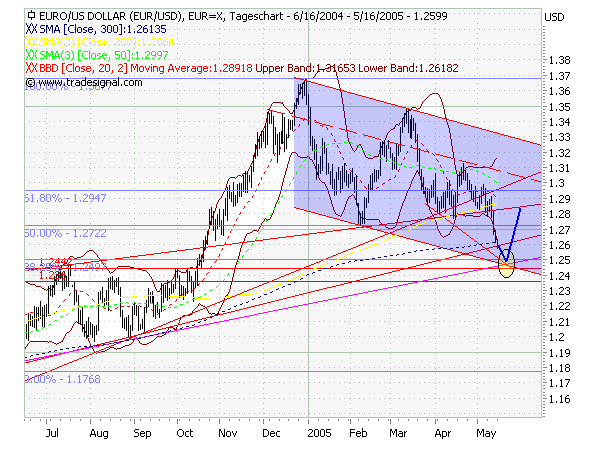

warum long-spekulieren, wenn der trend short ist?

Optionen

| Boardmail an "Parocorp" |

Wertpapier: PERUSAHAAN GAS N. RP 5 |

Optionen

| Boardmail an "Logos" |

Wertpapier: PERUSAHAAN GAS N. RP 5 |

Optionen

| Boardmail an "Parocorp" |

Wertpapier: PERUSAHAAN GAS N. RP 5 |

Optionen

| Boardmail an "Logos" |

Wertpapier: PERUSAHAAN GAS N. RP 5 |

Ich möchte ein Forex Konto eröffnen, und habe im Moment ein Demo Konto bei FXCM. Mit den Charts kann ich nichts anfangen. Geht bis März und dann der letzte Tag?!? (Das Chart Programm heißt Market Scope).

Kann jemand einen Broker empfehlen - mit vernünftigem Chart-Programm?

hobo

Optionen

| Boardmail an "Parocorp" |

Wertpapier: PERUSAHAAN GAS N. RP 5 |

Ich trade nicht jeden Anstieg bzw. Rückgang. Nur sehe ich die Chance bei 1,2470 Long zu geh´n als sehr sicher an um ein paar Euros zu verdienen. Wenn´s nicht so weit kommt macht´s auch nicht - ich hab Zeit um auf meine nächste Chance zu warten.

xpfuture

Optionen

| Boardmail an "Parocorp" |

Wertpapier: PERUSAHAAN GAS N. RP 5 |

Optionen

| Boardmail an "Parocorp" |

Wertpapier: PERUSAHAAN GAS N. RP 5 |

bin wieder wech, viel erfolg zusammen!

Optionen

| Boardmail an "Parocorp" |

Wertpapier: PERUSAHAAN GAS N. RP 5 |

aber ich denke mal du hast mich gemeint mit deinen Postings; ist ja auch ok und eigentlich sollte man ja auch nicht unbedingt so traden wie ich es gerade hier veranstalte;

aber maßgeblich für mich noch immer der $-Index wo noch immer keine Entscheidung gefallen ist + innere Trendlinie..Chart weiter oben (wird von nicht so vielen Beachtung geschenkt und das ist auch gut so; hat desweiteren schon einige Male gut gehalten in den letzten Tagen)

sollte ich mit Stop rausfallen waren es 2mal leicht Verluste und ich würde es (wenn wir in einem Rutsch weiter fallen) im Berich 1,25-1,2460 auch noch ein drittes Mal versuchen...nur dann mit einem höheren Hebel...

letztlich ist jeder selbst für seine Trades verantwortlich...und wer glaubt das short auf aktuellem Niveau die bessere Alternative ist solls eben damit versuchen...

aktueller Kurs 1,2620

mentales SL auf 1,2570 (neues Intrady-Tief) erhöht

gruss

füx

Vielleicht kannst du mir meíne Frage beantworten. (Welcher Forex Broker ist empfehlenswert?) Oder tradest du KO Zertis?

hobo

handle KO Zertis und bin zufrieden damit; Vor- u. Nachteile wurde hier im Thread schon mal diskutiert...

gruss

füx

aus dem kurzfristigen Downtrend ausgebrochen und mit kleinem Intradaydoppelboden...kleiner Anfang mal gemacht...

füx