against all odds

Seite 27 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 342.567 |

| Forum: | Börse | Leser heute: | 52 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 24 | 25 | 26 | | 28 | 29 | 30 | ... 117 > | ||||

http://www.amosweb.com/cgi-bin/...d&c=dsp&k=paradox+of+thrift

Optionen

'Eigenverantwortung der Mitgliedsstaaten heißt Eigenverantwortung ihrer Bürger. Dass diese die Krisenlasten im Wesentlichen schultern und dabei auch schmerzhafte Reformen anpacken müssen, ist unvermeidlich. Aber die Grenze dieser Eigenverantwortung ist dort erreicht, wo elementare Lebenschancen bedroht sind. Wenn in Griechenland oder Spanien eine ganze Generation ihrer Möglichkeiten beraubt wird, ein produktives Leben zu führen, dann ist das nicht nur ein griechisches oder spanisches Problem, sondern eines, das alle Unionsbürger betrifft.

Die Währungsunion wird ohne kontrollierte Transferelemente nicht dauerhaft stabil sein können. Eine Situation, in der ein Euro-Land in einen akuten Zahlungsnotstand gerät und gezwungen wird, seiner Bevölkerung drakonische Sparmaßnahmen zuzumuten, muss die absolute Ausnahme bleiben. Damit es möglichst gar nicht erst so weit kommt, benötigen wir zwischen den Euro-Ländern einen Versicherungsmechanismus, der die Konsequenzen eines dramatischen Konjunktureinbruchs für die Bevölkerung abfedert....'

'...Im Übrigen wären Länder wie Deutschland in der aktuellen Niedrigzinsphase gut beraten, verstärkt in die eigene Infrastruktur zu investieren und damit zusätzliche Nachfrage in der gesamten Euro-Zone zu schaffen...'

Optionen

Optionen

Angehängte Grafik:

gd_2013-2_staatsfinanzen.gif (verkleinert auf 59%)

gd_2013-2_staatsfinanzen.gif (verkleinert auf 59%)

Optionen

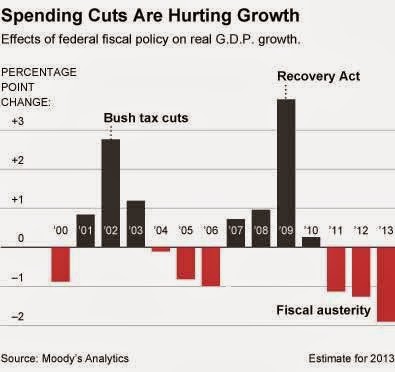

Angehängte Grafik:

us_spending_cuts__graph_steven_rattner__in_n....jpg

us_spending_cuts__graph_steven_rattner__in_n....jpg

Optionen

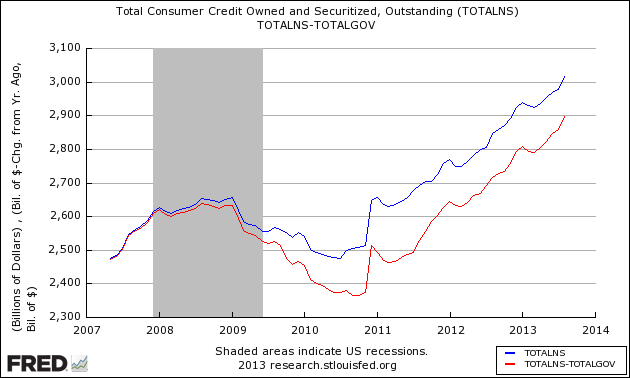

Angehängte Grafik:

fredgraph_consumer.png (verkleinert auf 80%)

fredgraph_consumer.png (verkleinert auf 80%)

Optionen

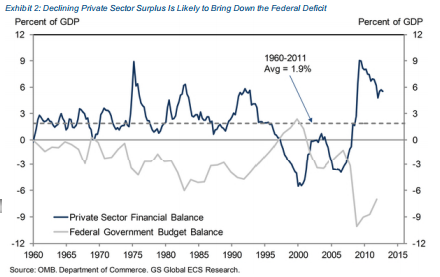

Angehängte Grafik:

gs1.png

gs1.png

Richard Koo erklärt warum

'Once every several decades, the private sector loses its mind in a bubble, leverages itself up to the hilt, and is forced into debt minimization in order to remove its debt overhang following the crash. When the private sector as a whole is deleveraging, even at record low interest rates, monetary policy is largely ineffective while fiscal policy becomes absolutely essential in keeping both the economy and money supply from shrinking. The superior effectiveness of monetary policy during private sector profit maximization and of fiscal policy during private sector debt minimization indicates that the latter was the long-overlooked ‘other half’ of macroeconomics.'

http://www.elgaronline.com/view/journals/ejeep/...FE3x4K&result=1

Optionen

Optionen

Angehängte Grafik:

consumer_sentiment.gif

consumer_sentiment.gif

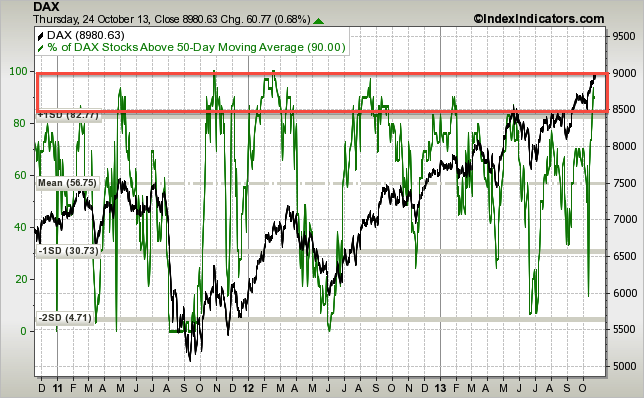

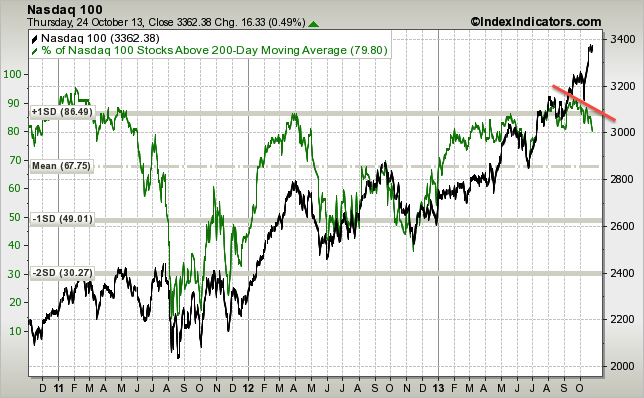

Eine große Korrektur darf man allerdings nicht erwarten, da sich bisher kein starker bärischer Trigger offenbart hat.

Angehängte Grafik:

dax-vs-dax-stocks-above-50d-sma-params-3y-x-....png (verkleinert auf 79%)

dax-vs-dax-stocks-above-50d-sma-params-3y-x-....png (verkleinert auf 79%)

Angehängte Grafik:

nasdaq100-vs-nasdaq100-stocks-above-200d-....png (verkleinert auf 79%)

nasdaq100-vs-nasdaq100-stocks-above-200d-....png (verkleinert auf 79%)

Angehängte Grafik:

sp600-vs-sp600-stocks-above-200d-sma-params-....png (verkleinert auf 79%)

sp600-vs-sp600-stocks-above-200d-sma-params-....png (verkleinert auf 79%)

Optionen

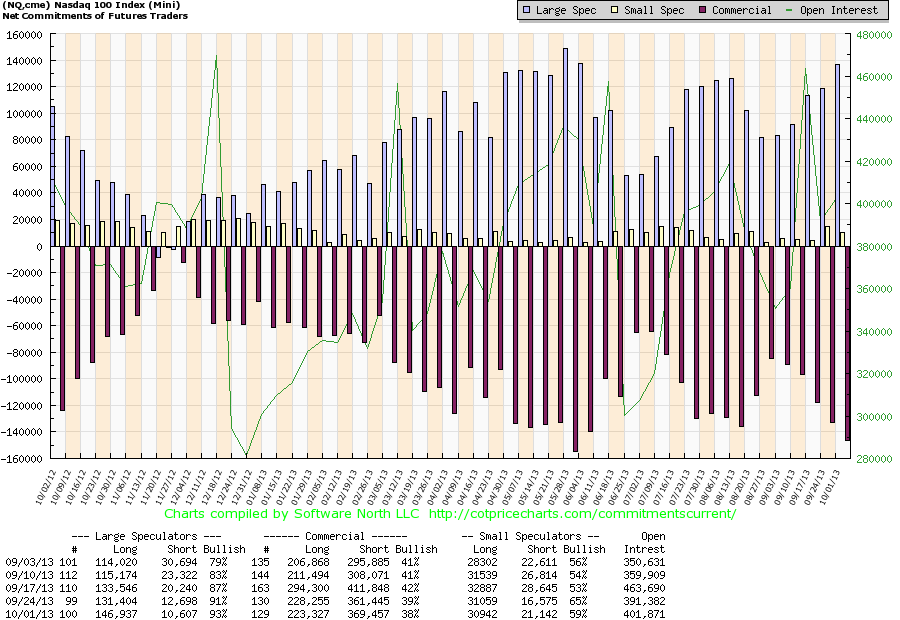

Angehängte Grafik:

nq.png (verkleinert auf 56%)

nq.png (verkleinert auf 56%)

Optionen

Angehängte Grafik:

obsgshort.gif (verkleinert auf 85%)

obsgshort.gif (verkleinert auf 85%)

Optionen

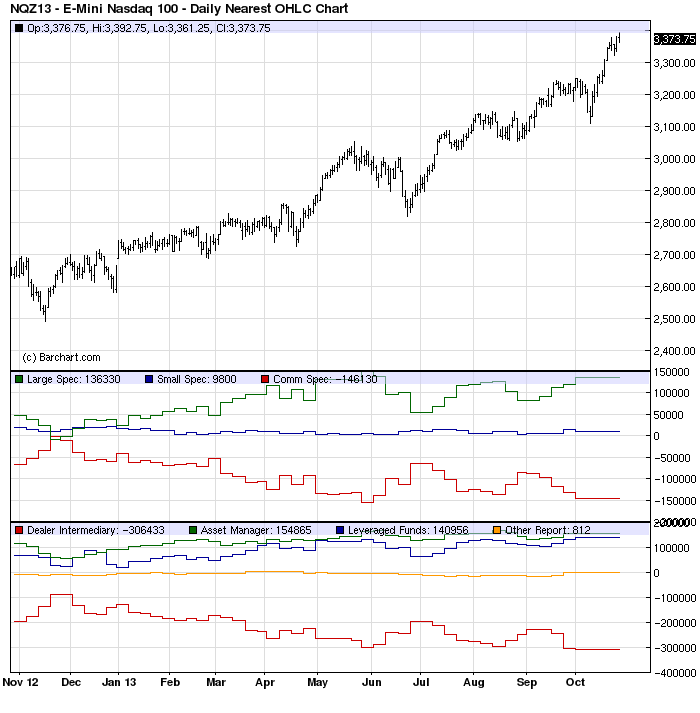

Hier mal die Akteure:

1. Commercials, consisting of Producer/Merchant/Processor/User and Swap Dealers (Red Line)

2. Large Speculators, consisting of Managed Money and Other Reportables (Green Line)

3. Small Speculators (Blue Line)

zu 1.

Producer/Merchant/Processor/User

A "producer/merchant/processor/user" is an entity that predominantly engages in the production, processing, packing or handling of a physical commodity and uses the futures markets to manage or hedge risks associated with those activities.

Swap Dealer

A "swap dealer" is an entity that deals primarily in swaps for a commodity and uses the futures markets to manage or hedge the risk associated with those swaps transactions. The swap dealer's counter parties may be speculative traders, like hedge funds, or traditional commercial clients that are managing risk arising from their dealings in the physical commodity.

zu 2.

Money Manager

A "money manager," for the purpose of this report, is a registered commodity trading advisor (CTA); a registered commodity pool operator (CPO); or an unregistered fund identified by CFTC. These traders are engaged in managing and conducting organized futures trading on behalf of clients.

weitere

Dealer/Intermediary - These participants are what are typically described as the "sell side" of the market. Though they may not predominately sell futures, they do design and sell various financial assets to clients. They tend to have matched books or offset their risk across markets and clients. Futures contracts are part of the pricing and balancing of risk associated with the products they sell and their activities. These include large banks (U.S. and non-U.S.) and dealers in securities, swaps and other derivatives.

The rest of the market comprises the "buy-side," which is divided into three separate categories:

Asset Manager/Institutional - These are institutional investors, including pension funds, endowments, insurance companies, mutual funds and those portfolio/investment managers whose clients are predominantly institutional.

Leveraged Funds - These are typically hedge funds and various types of money managers, including registered commodity trading advisors (CTAs); registered commodity pool operators (CPOs) or unregistered funds identified by CFTC.3 The strategies may involve taking outright positions or arbitrage within and across markets. The traders may be engaged in managing and conducting proprietary futures trading and trading on behalf of speculative clients.

Other Reportables - Reportable traders that are not placed into one of the first three categories are placed into the "other reportables" category. The traders in this category mostly are using markets to hedge business risk, whether that risk is related to foreign exchange, equities or interest rates. This category includes corporate treasuries, central banks, smaller banks, mortgage originators, credit unions and any other reportable traders not assigned to the other three categories.

Optionen

Angehängte Grafik:

cot_nasdac.png (verkleinert auf 72%)

cot_nasdac.png (verkleinert auf 72%)

The Commodity Futures Trading Commission (CFTC) releases a new report every Friday at 3:30 Eastern Time, and the report reflects the commitments of traders on the prior Tuesday.

The Weekly COT Report

The weekly report details trader positions in most of the futures contract markets in the United States. Data for the report is required by the CFTC from traders in markets that have 20 or more traders holding positions large enough to meet the reporting level established by the CFTC for each of those markets.1 These data are gathered from schedules electronically submitted each week to the CFTC by market participants listing their position in any market for which they meet the reporting criteria.

The report provides a breakdown of aggregate positions held by three different types of traders: “commercial traders,” “non-commercial traders” and “nonreportable.” “Commercial traders” are sometimes called “hedgers”, “non-commercial traders” are sometimes known as “large speculators,” and the “nonreportable” group is sometimes called “small speculators.”

As one would expect, the largest positions are held by commercial traders that actually provide a commodity or instrument to the market or have bought a contract to take delivery of it. Thus, as a general rule, more than half the open interest in most of these markets is held by commercial traders. There is also participation in these markets by speculators that are not able to deliver on the contract or that have no need for the underlying commodity or instrument. They are buying or selling only to speculate that they will exit their position at a profit, and plan to close their “seller” or “buyer” position before the contract becomes due. In most of these markets the majority of the open interest in these "speculator" positions are held by traders whose positions are large enough to meet reporting requirements.

The remainder of holders of contracts in these futures markets, other than "commercial" and "large speculator" traders, are referred to by the CFTC as “nonreportable.” This is because they don’t meet the position size that requires reporting to the CFTC. (Thus they are “small speculators.”) The “nonreportable” open interest in a futures market is determined by subtracting the open interest of the “commercial traders” plus “non-commercial traders” from the total open interest in that market. As a rule, the aggregate of all traders’ positions reported to the CFTC represents 70 to 90 percent of the total open interest in any given market.2

Since 1995 the Commitments of Traders report includes holdings of options as well as futures contracts.

Purposes and Uses

Many speculative traders use the Commitments of Traders report to help them decide whether or not to take a long or short position. One theory is that "small speculators" are generally wrong and that the best position is contrary to the net nonreportable position. Another theory is that commercial traders understand their market the best and taking their position has a better chance of profit (which is pretty much the same thing as the "small speculators" being wrong).

(wiki)

Optionen

The percentage GDP gap is the actual GDP minus the potential GDP divided by the potential GDP.

.

Optionen

Angehängte Grafik:

output_gap_(g10)__estimates__imf__graph_mo....jpg

output_gap_(g10)__estimates__imf__graph_mo....jpg

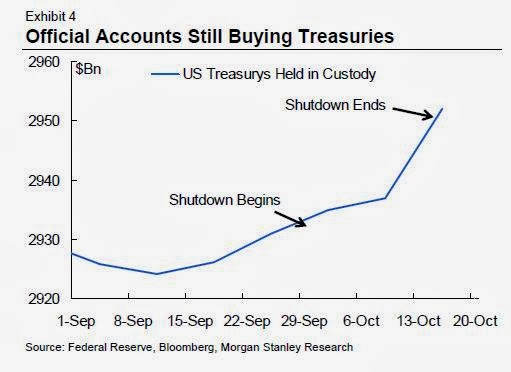

Auch während des Shutown war as Ausland Nettokäufer:

Optionen

Angehängte Grafik:

official_accounts_still_buying_ust__graph_morg....jpg (verkleinert auf 99%)

official_accounts_still_buying_ust__graph_morg....jpg (verkleinert auf 99%)