Weltweit grösster Windkraftanlagenhersteller

13:10 22.02.12

Der dänische Windturbinen-Hersteller Vestas A/S (Vestas Aktie) hat einen Auftrag zur Lieferung von Windturbinen mit einer Gesamtkapazität von 150 MW in die USA erhalten. Auf Wunsch des Kunden sollen Name sowie Details zu dem Auftrag zunächst nicht genannt werden. Sicher ist, dass Vestas neben der Lieferung auch einen über fünf Jahre laufenden Service- und Wartungsvertrag unterzeichnet hat. Die Lieferung soll in der zweiten Jahreshälfte 2012 erfolgen.

© 2012 facunda green AG - greenfinancials.de

Hast du eine Quelle hierfür?

Optionen

| Boardmail an "silverfish" |

Wertpapier: Vestas Wind Systems AS |

Mit jedem neuen, fetten Auftrag werden wir Rückenwind bekommen und stetig steigen!

Nur darum bin ich hier investiert!

Good luck!

Unternehmen Event Datum Ergebnis§

Vestas Wind Systems A/S Jahresabschluss 08.02.12

Vestas Wind Systems A/S Hauptversammlung 29.03.12

Vestas Wind Systems A/S Quartalszahlen 02.05.12

Der Grund ist, dass das amerikanische Modell der Förderung erneuerbarer Energien (PTC) zum 31.12.2012 ausläuft. Deshalb versuchen alle, die ein Windprojekt in Planung haben dieses noch irgendwie 2012 fertig zu stellen, um von der Förderung zu profitieren. Durch diese Vorzieheffekte rechnet Vestas damit, dass in den USA dieses Jahr ~65% mehr Anlagen errichtet werden als 2011.*

Und eine (im Vergleich zu einem "normalen" Jahr) um 65% höhere Nachfrage sollte es Vestas ermöglichen deutlich höhere Preise durchzusetzen.

*Quelle: S.36 - www.vestas.com/Admin/Public/...presentations/2011/2011_AR_PRES_UK.pdf

Hier die Pressemeldung:

23 February 2012

•Main 2011 consolidated figures:

+10% in sales, to 3,033 million euro

+11% in EBITDA, to 364 million euro

+10% in EBIT, to 131 million euro

+2% in net income, to 51 million euro

229 million euro in capital expenditure (wind turbines)

NFD of 710 million euro (2 times EBITDA)

•Strengthened global presence: 92% of sales (2,802 MW) came from outside Spain: sales increased 2.6-fold in India (accounting for 19% of the total) and 3.8-fold in Latin America+Southern Cone (15%). Europe (Spain excluded) accounted for 20%, China for 23% and the US for 14%.

•Wind Turbines: MW sold +16.5%, and MW delivered grow 15% to 3,092 MW. The EBIT margin is 4%, in line with guidance

•O&M services: 16,300 MW under maintenance (including the 2,700 MW added in 2011), which provided recurring revenues of 250 million euro

•Development and sale of wind farms, a key area: progress in value creation plan, with 417 MW in sales agreements and 26 million euro in EBIT

•Progress along the three vectors: reduced the CoE by 10-15% in 2011 and rolled out new products and services; growth: +16.5% MW sold in 23 countries for 46 customers, plus entry into new markets; and efficiency: adjusted production capacity and optimised construction and logistics costs

•The pipeline amounts to 1,600 MW, for delivery in 2012 and 2013, +13% year-on-year

•In 2012, Gamesa will give priority to sound finances and profitability over sales volume and will bring forward its net free cash flow break-even target by one year. 2012 Guidance: Wind turbine sales, 2,800-3,200 MW; Wind Turbine EBIT margin: 2-4%; NFD/EBITDA ratio of <2.5

Gamesa fulfilled 2011 guidance in terms of volume, profitability and financial soundness. It also maintained profitable growth, supported by its globalisation strategy (which enables it to leverage growth in emerging markets and diversify market risks) and a rigorous efficiency programme, which led to double-digit growth in its key operating figures. The company also maintained margins despite the complex macroeconomic and industry situation as well as fierce competition.

In 2011, Gamesa obtained consolidated revenues of 3,033 million euro (+10%), driven by the recovery in manufacturing. EBIT amounted to 131 million euro (+10%) and net profit was 51 million euro (+2%).

The wind turbine division increased sales (in MWe) by 16.5% to 2,802 MW, almost all (92%) of which are outside Spain, as the company furthers its internationalisation strategy.

The recovery in wind turbine manufacturing activity and the focus on controlling costs provided the wind turbine division with an EBIT margin of 4% (in line with 2011 guidance: 4%-5%). Intense activity in the wind farm development and sales division and the development of farms for delivery in 2011 and early 2012 provided the division with EBIT of 26 million euro (17 million euro in 4Q 2011 alone, up three-fold to 4T2010).

Entry into new wind power markets (e.g. Brazil and India) with a growing contribution to group sales, supply chain localisation, and the recovery in wind farm development in the US raised the division's working capital/sales ratio to 24%, slightly higher than 2011 guidance.

During the year, Gamesa continued to invest (229 million euro) in international expansion (India and Brazil), in launching and manufacturing new products (G9X-2.0 MW and G10X-4.5 MW) and in R&D for new platforms (onshore and offshore). As a result, consolidated net financial debt (NFD) was 710 million euro (2 times EBITDA), in line with annual guidance.

In 2011, Gamesa made progress along the three main vectors of its Business Plan 2011-2013: reducing the cost of energy (CoE) by 10%-15% in 2011 (depending on platform and region) and launching new products and services; growth: MW sold increased by 16.5%, in 23 countries and to 46 customers, plus entry into new markets and growth in MW under maintenance and in wind farm sales; and efficiency, by adjusting production capacity to demand, localising the supply chain in India and Brazil, and optimising construction and logistics costs.

92% of revenues come from outside Spain: consolidation in 5 regions and new markets

In 2011, Gamesa sold 2,802 MW (+16.5%) and strengthened the globalisation process, with the result that the bulk (around 92%) of sales came from outside Spain. The company also registered record high wind turbine deliveries: 3,092 MW (+15%).

Gamesa diversified its revenues in 5 geographic areas: revenues increased 2.6-fold in India (accounting for 19% of the total) and 3.8-fold in Latin America+Southern Cone (Honduras, Mexico and Brazil; 15% of the total). Europe (Spain excluded) accounts for 20% of the total, with Eastern Europe (Poland and Romania, in particular) representing 14%. China accounts for 23% and the US for 14%. Spain's share was less than 8% for the second consecutive year.

While strengthening sales in regions with considerable wind potential, the company also entered new markets, registering its first sales in New Zealand, Algeria and Azerbaijan.

Along with its strategy of geographic diversification, Gamesa expanded its range of products (G9X-2.0 MW and G10X-4.5 MW) and will continue to do introduce turbines with larger rotors for all types of wind.

In 2011, the company received 356 MW of orders for the G97-2.0 MW Class III, in Europe, the US, China and India, accounting for 5% of the MW sold in the year. It also signed a framework agreement for 1,300 MW in India with G97-2.0 MW turbine, as part of the 2,000 MW agreement signed with Caparo (currently Mytrah) for 2012-2016.

16,300 MW under maintenance provides recurring revenues of 250 million euro

The operation and maintenance (O&M) services area is key for Gamesa's profitable growth, contributing to recurring revenues, improving margins and generating cash flow.

After expanding its portfolio by 2,700 MW during the year, Gamesa has 16,300 MW under O&M, which provides recurring revenues of 250 million euro.

Gamesa entered the large component repair and overhaul business in 2011 and extended its range of services for third-party fleets.

The services area plays a key role in growth, and new O&M programmes and services contribute decisively towards CoE optimisation. Gamesa's new programme, GPA, aims to achieve 99% availability of its fleet and reduce farms' operating costs by up to 10%. It has also launched a project to extend the useful life of the G4X fleet to ensure up to 30 years of operation.

Development and sale of wind farms, a key area: sales agreements for 417 MW and EBIT of 26 million euro

In 2011, Gamesa continued to focus on monetising wind farm development and sales, clinching sales agreements totalling 417 MW with some of the world's leading utilities and the delivery of 177 MW in Spain, Germany, France, Greece and the US. Moreover, the company has 734 MW in the final phases of construction and commissioning.

The wind farm development and sale division obtained EBIT of 26 million euro in 2011 (17 million euro in 4Q 2011), compared with 0 million in 2010, in line with annual guidance.

Wind farms is a vital division for Gamesa, as it provides the company with competitive advantages and complements its wind turbine manufacturing activity: at 31 December 2011, the company had a wind farm pipeline of 23,891 MW worldwide.

2012: focus on profitability and sound finances

In 2012, Gamesa will give priority to financial soundness and profitability over sales volume, and will bring forward its net free cash flow break-even target by one year.

At December 2011, Gamesa had 1,600 MW in orders for delivery in 2012 and 2013, up 13% year-on-year.

Despite this positive performance, Gamesa reduced its 2012 target sales volume range to 2,800-3,200 MW due to short-term market circumstances: regulatory uncertainty in the US, delays in connecting to the grid and financing restrictions in China, and greater demand volatility in India due to regulatory changes.

However, the company believes that the growing competitiveness of wind energy, together with governments' commitments to combating climate change, will lay the foundation for sustained sector growth in the medium and long term: in fact, independent sources predict double-digit growth (10-20%) in new facilities between 2011 and 2015.

The 2012 EBIT margin guidance for the wind turbine division is 2-4%, which takes into consideration the impact of the global launch of the new platforms (G9X-2.0 MW) and the lower margins expected in some emerging markets, which are partially offset by cost and product mix optimisation.

Gamesa expects capex of 275 million euro in 2012, which is going to be a peak year for investment under the Business Plan 2011-2013. It also expects NFD to reach <2.5 times EBITDA.

Measures in 2012 to continue reducing the CoE, expanding, and improving efficiency

In 2012, Gamesa will continue to advance along the three vectors of its Business Plan 2011-2013-all of which are critical for strengthening its leading position in the sector worldwide:

Optimisation of the CoE, focusing on improving turbine availability and reliability, with special efforts in 2012 to reduce the cost of materials. It will also develop two new wind turbines (G97-2.0 MW Class II and G114-2.0 MW) and will continue to improve the availability of its fleet;

Growth, by intensifying sales efforts among utilities in central and northern Europe and in markets in Southeast Asia, Australasia, South Africa and the Middle East. To do so, the company will leverage its presence in China, India and North Africa. The services area will step up sales efforts outside Spain for its new value-added and large component repair and overhaul services. The wind farm development and sale division will continue to monetise its pipeline, focusing especially on the US;

Efficiency is particularly important in the current market context, which requires adjusting capacity to demand. Having practically completed capacity reduction in Spain in 2011, the company will focus on consolidation and adaptation of that capacity to new products. In Brazil and India, it will complete supply chain localisation for the new G9X-2.0 MW platform.

It will also create a centralised logistics department to standardise procedures and improve logistics services contracts to cut costs. Gamesa will continue to advance in reducing construction times and optimising the use of storage yards. It will also roll out new procurement tools to simplify and accelerate supplier certification and lead times-maintaining strict quality criteria-and reduce supply costs.

Optionen

| Boardmail an "butzerle" |

Wertpapier: Vestas Wind Systems AS |

Das könnte ein Indizi dafür sein, dass kleinere Windanlagenhersteller besser auf Marktveränderungen eingehen können. Vestas ist zu groß und schwerfällig!

51 Mio Gewinn und 3 Milliarden Umsatz ist doch Topp von Gamesa!

Werden also ggf. den einen oder anderen Auftrag, wenn nicht margenkräftig genug, sogar ablehnen

Optionen

| Boardmail an "butzerle" |

Wertpapier: Vestas Wind Systems AS |

Vestas hat hier meiner Meinung nach einiges verschlafen, ist aber vielleicht auch einfach nur zu groß um zu reagieren.

sieht man ja am PTC, wenn das nicht verlängert wird, dann muss Vestas über 1000 Mitarbeiter in den USA entlassen.

kann hier bitte mal einer den order eingang von vestas reinstellen , danke !

da hat doch vestas so einen tollen link , den meine ich

Optionen

| Boardmail an "DR.FAUST" |

Wertpapier: Vestas Wind Systems AS |

Angehängte Grafik:

chart_week_vestas.png (verkleinert auf 93%)

chart_week_vestas.png (verkleinert auf 93%)

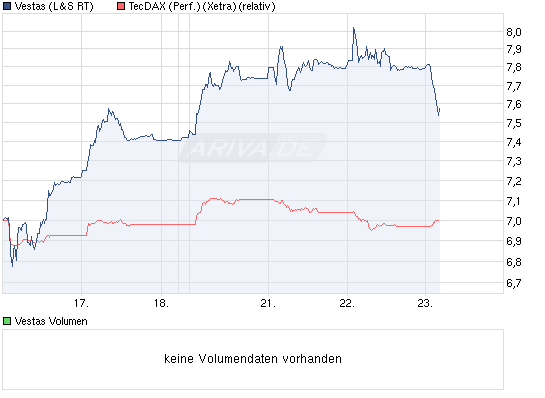

Also, Deine Korrelation in Ehren, aber schaue selbst, anderer Zeitraum und gegenteiliges Bild:

Optionen

| Boardmail an "DrShnuggle" |

Wertpapier: Vestas Wind Systems AS |

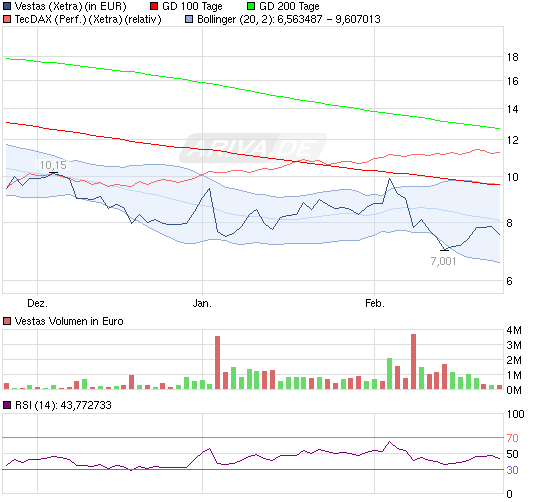

Angehängte Grafik:

120223_chart_quarter_vestas.png (verkleinert auf 93%)

120223_chart_quarter_vestas.png (verkleinert auf 93%)

Optionen

| Boardmail an "WitLeeu" |

Wertpapier: Vestas Wind Systems AS |

Angehängte Grafik:

vestas-chart.png (verkleinert auf 56%)

vestas-chart.png (verkleinert auf 56%)

Ich denke da hat ein Ami Gewinne aus seinen Shorts mitgenommen und das Handelsvolumen unterschätzt. Kurs kommt ja auch schon wieder deutlich zurück.

Oder kommt bald ein Schub für die gesamte Windbranche mit der Verlängerung des PTC?

Mindestens 30% Gewinn für alle Ü 10 Aussteiger!

Finger weg!

Der Chartverlauf verrät eigentlich schon alles, wie schlecht es derzeit bei Vestas läuft. Eine Bodenbildung bei der Aktie ist nicht erkennbar. Anleger meiden das Papier.

http://www.deraktionaer.de/aktien-deutschland/...d-aus---17781209.htm