Meine Wirecard-Gewinne - Thread!

Als die "chinesische Grippe" noch verdammt weit weg war und im Februar ein Allzeithoch das nächste jagte.

Es wird schon auf ein Ende des Desasters spekuliert, was nmM aber zu früh ist.

Halt das aktuell für eine haarige Bärenmarkt-Rally, die wahrscheinlich nochmal kippt...

Optionen

| Boardmail an "lehna" |

Wertpapier: Wirecard AG |

Aber vor Sommer wahrscheinlich nicht.

Denn sollte der Aktienmarkt nochmal abtauchen, werden sich auch Top Picks kaum entziehen können.

Das war jedenfalls bei Absaufszenarien der Vergangenheit fast immer so...

Optionen

| Boardmail an "lehna" |

Wertpapier: Wirecard AG |

Veröffentlichung KPMG in den nächsten Tagen - Kurs schnellt intraday stark nach oben (20-40%), wird aber im Tagesverlauf deutlich abverkauft am Ende bleiben noch ca 10% Kursgewinn stehen.

Das Testat bestätigt dass es keine nennenswerten Auffälligkeiten gibt/gab und WDI sauber ist.

Kurz darauf wird Wirecard mit den aktuellen Zahlen belegen dass das Wachstum weiterhin ungebremst ist.

Damit wird eine mehrmonatige Phase eingeleitet in der die Leerverkäufer sich langsam aber sicher zurückziehen runter bis auf eine LV-Quote von 2-5%.

In dieser mehrmonatigen Phase (vielleicht auch 1-2 Jahre) wird WDI langsam, aber kontinuierlich steigen. kleinere Rücksetzer wird es zwischenzeitlich natürlich immer mal wieder geben!

Ja, das ist meine persönlich Einschätzung, die ich allerdings darin bestärkt sehe dass es bei Wirecard in den letzten Jahren schon durchaus sehr ähnliche Ausgangspositionen gab.

sollte auch der Ölpreis so niedrig bleiben saufen Amis Frackings im dutzend ab.Auch nicht fördernd.:-)))

Aber poste das doch bitte in ein Topic zu Öl-Aktien oder in eines der zahlreichen anderen Aktien die davon sehr viel mehr betroffen sein werden als Wirecard oder noch besser in ein Topic in dem es um die allgemeine Weltwirtschaftssituation geht.

Hier im Speziellen zu Wirecard hat es kaum etwas verloren...

Vielleicht sind hier einfach mehrheitlich Investierte die an Ihr Investment glauben und für die es FAKTEn bedarf um vom Gegenteil überzeugt zu werden und da haben die Basher oder Auber auch die Pessimisten einfach nichts drauf, sorry!

ehrlich viel Glück mit euren Investitionen.:-)))

Wenn Du Deutsche Börse zu 50€ gekauft hast, dann muss das vor 2015 gewesen sein. Dann lag der Schlüssel zum Erfolg doch am ehesten im "buy and hold" :)

Was hat das aber in einem Wirecard-Forum verloren?

Merkwürdig dass gerade Du jetzt fragst ob wir uns in einer Bärenmarktrally befinden - denn vor ein paar Tagen warst Du Dir da angeblich noch absolut sicher und hast dies stolz hier verkündet...

Wenn Du überhaupt nichts zum Thread-Thema beizutragen hast, dann schreib doch einfach nichts!

Zeitpunkt: 20.04.20 11:03

Aktionen: Löschung des Beitrages, Nutzer-Sperre für 6 Stunden

Kommentar: Provokation

Ich hab die Tabelle doch nicht einmal erstellt, die ist für jeden frei zugänglich von finanzen.net..

Google doch einfach selbst mal: "dax year to date gewinner" (gleich der erste Treffer)

Du bist manchmal echt ganz schön schwer von Begriff...

PS: Inzwischen hat Deine deutsche Börse Fresenius auf Platz 2 abgelöst! :)

By

April 16, 2020, 7:00 AM EDT

Worried about Covid-19, shoppers use phones to buy, get food

Keypads on credit-card readers are also a red flag in pandemic

A worker disinfects a Verifone contactless electronic payment terminal in Moscow.

Photographer: Andrey Rudakov/Bloomberg

Sign up here for our daily coronavirus newsletter on what you need to know, and subscribe to our Covid-19 podcast for the latest news and analysis.

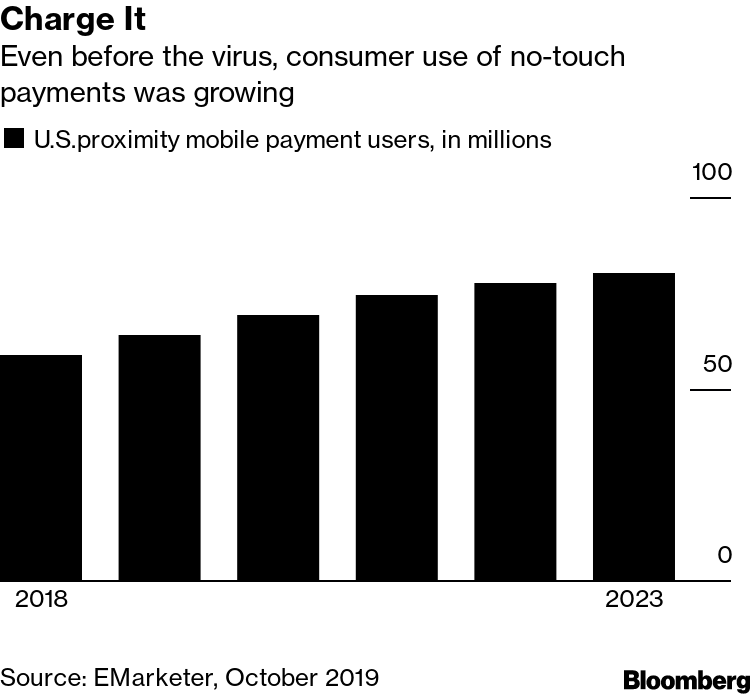

As more people worry about catching coronavirus from touching cash and credit-card terminals, a onetime niche technology is roaring into the mainstream.

Use of contactless mobile payments -- services that once struggled to catch on in the U.S. -- is surging as people come to see their phones as the safer way to pay. They’re also using mobile apps tied to payments, such as Amazon Prime Now, to place delivery or pickup orders for groceries. The Treasury Department may even let people who don’t have bank accounts receive their coronavirus relief checks via mobile-payment services like Venmo.

“We shouldn’t be touching anything,” said Richard Crone, chief executive officer of mobile-payment research firm Crone Consulting LLC. He expects contactless payments to grab an additional 10% to 20% of transactions at stores and ATMs as the result of the pandemic. Person-to-person services like PayPal, Venmo and Zelle should benefit as well, Crone said.

It’s easy to see why. Even with retail stores cleaning more often than ever -- if they’re open at all -- handling cash or touching payment keypads stands out as a major risk. With contactless pay, you link a bank account or credit card to your phone and then tap the device on a contactless reader or hover over it to trigger payment.

Already, 27% of U.S. small businesses have seen an increase in customers using services like Apple Pay, according to a survey of 361 companies released in April by the Strawhecker Group and the Electronic Transactions Association. Publix Super Markets Inc. sped up its transition to contactless terminals because of Covid-19, according to the company. Starting in early April, consumers at all Publix stores have been able to use services like Apple Pay and Google Pay to check out.

“I know a lot of merchants are putting signage up at the point of sale, ‘Please use contactless,’” said Linda Kirkpatrick, a Mastercard executive who works with banks and credit unions.

Burger King released a commercial in March to encourage customers to use an order-ahead app to pay at drive-thrus.

A couple of weeks ago, retail giant Walmart Inc. tweaked its self-checkout system to go completely contactless when shoppers use Walmart Pay. Previously, you had to touch a “Pay now” button after scanning your groceries. Now, you can read a QR code with your phone to pay. Use of pickup and delivery at Walmart is growing as well.

“You are seeing customers start to use services they weren’t interested in before,” said Molly Blakeman, a Walmart spokeswoman.

Many sellers at farmers’ markets have stopping accepting cash, and are instead using apps like Venmo, which is owned by PayPal Holdings Inc. The app got it start as a way for friends to reimburse each other for dinner or for roommates to handle rent.

PayPal said it’s allowing people to receive their stimulus checks through its namesake service and testing it on Venmo.

At Zelle, a person-to-person payment app supported by Bank of America Corp., JPMorgan Chase & Co. and others, users have been sending money to loved ones for prescriptions and groceries, said Meghan Fintland, a spokeswoman. Some are buying items in bulk for the whole neighborhood, and then using Zelle to collect payments. Others are sending cash gifts to relatives for their birthdays.

“People don’t want to handle cash, especially at this time, so they are looking to mobile payments as the best alternatives,” Fintland said.

That said, the coronavirus shutdown has hurt some types of mobile payment services and forced others to adjust.

Toast Inc., which makes management systems for restaurants, laid off half its staff in April. Earlier this week, Grubhub Inc. pulled its 2020 guidance, largely because of the acute situation in New York, where many restaurants have closed. Companies that serve ride-sharing companies, like Stripe Inc. and Adyen NV, may also suffer as usage declines.

The industry’s established players are also facing new competition. In March, portable-reader heavyweight Square Inc. rolled out ways for its restaurant owners to offer pickup and delivery options.

“We’ve seen so many folks pivoting to online to keep their businesses going,” said Katie Dally, a Square spokeswoman. Independent booksellers and other businesses are offering pickup and delivery too, she said.

As more people embrace contactless technology and get used to paying that way, consumer behavior is going to change for good, experts say.

The rush delivery service at supermarket chain Safeway hit 670,000 weekly active U.S. mobile users the week of March 29, up from fewer than 50,000 in the week of March 1, according to the analytics platform App Annie. Amazon Prime Now’s Android and iPhone active user base grew 60%, according to App Annie.

“It’s behavior that’s going to stick after stay at home ends,” said Jordan McKee, an analyst at 451 Research. “There will be muscle memory about paying, and consumers will use it going around their daily life.”

https://www.kapitalmarktexperten.de/2020/04/...e-change=1587366798752

Steht der nächste markante Down-move bevor?

Optionen

| Boardmail an "Kornblume" |

Wertpapier: Wirecard AG |

chart_3years_wirecard.png (verkleinert auf 25%)

So hält sich Wirecard heute im schwachen Gesamtmarkt doch ziemlich gut!

Zeitpunkt: 22.04.20 10:23

Aktion: Löschung des Beitrages

Kommentar: Regelverstoß - Aussagen bitte belegen

Optionen

| Boardmail an "Kornblume" |

Wertpapier: Wirecard AG |

Zeitpunkt: 22.04.20 11:02

Aktion: Löschung des Beitrages

Kommentar: Regelverstoß - Bitte das Threadthema beachten

Brauchst nicht melden ist Tatsache ...

Quelle Wikipedia

Beruflicher Werdegang[Bearbeiten | Quelltext bearbeiten]

Braun startete seine Karriere als Consultant bei der Contrast Management Consulting GmbH und blieb bis November 1998 in dieser Position. Von 1998 bis 2001 arbeitete er für die KPMG Deutschland[3] in München.[4]

Zeitpunkt: 22.04.20 11:03

Aktion: Löschung des Beitrages

Kommentar: Regelverstoß - Bitte das Threadthema beachten

Optionen

| Boardmail an "Kornblume" |

Wertpapier: Wirecard AG |