Suzlon

mfg

Kalle

Optionen

| Boardmail an "kalleari" |

Wertpapier: Suzlon Energy GDR |

Optionen

| Boardmail an "kalleari" |

Wertpapier: Suzlon Energy GDR |

MUMBAI: Shares of Suzlon EnergyBSE 9.85 % have rallied 20 per cent in the last two sessions after the company reported decline in net loss in fourth quarter results.

Investors also lapped up the stock after the management reiterated its plan to raise Rs 1000 crore through sale of non-core assets.

http://economictimes.indiatimes.com/...-1209,cn-suzlon-energy-ltd.cms

.....there are some signs of easing, the market is hoping for a turnround.

The first such sign was when after several quarters the company reported a consolidated earnings before interest, taxes, depreciation, and amortisation (Ebitda) of Rs 328 crore in March quarter on a 54 per cent year-on-year growth in revenues at Rs 6,581 crore. But this isn't enough. The sales turnover only covers the business expenses, as the earnings before interest and tax (Ebit of Rs 116 crore) was not enough to pay interest costs of Rs 578 crore in the quarter. But because of higher sales, the intensity of losses is dropping. In March quarter, Suzlon made a net loss of Rs 603 crore compared to Rs 1,913 crore a year ago and Rs 1,075 crore in the December quarter.

The good news is the company has an order book of Rs 45,600 crore (5,300 Mw of equipment), 2.2 times its FY14 sales and is deliverable by FY15. Also, earlier, the biggest challenge to grow sales and acquire orders was lack of sufficient working capital. This is easing, with the money coming from bankers and asset monetisation. The company raised Rs 700 crore from asset sale and is aiming Rs 1,000 crore in FY15 on this account. These will support growth and reduce debt and interest cost.

The company is sitting on a net debt of Rs 12,700 crore and has interest cost of Rs 2,000 crore annually. To cover the interest cost, assuming the Ebitda margin at five per cent, it needs sales turnover of Rs 55,000 crore. So, improvement in sales and margins is vital. At the run rate, it is possible to achieve annual sales of Rs 26-27,000 crore.

But, more important, it will have to shore up operating profit margins. If it is able to achieve an Ebitda margin of 10 per cent, the sales turnover required for servicing the interest cost would not be more than Rs 28,000 crore. There is scope for margins to improve because some of the operational fixed cost will not move as much as the increase in sales. Also, the focus on high-margin orders and execution of low-margin orders in the past could add to margins.

To sum up, though operational and financial restructuring is paying dividends, a lot is yet to be achieved in sales growth, margins and debt reduction. The company is looking to refinance its high cost debt with the low cost forex loans. Also, monetisation of assets, with plans to list its European subsidiary Senvion (earlier REpower), could help cut debt and interest cost, crucial for generating positive return on equity.

http://smartinvestor.business-standard.com/market/...htm#.U49XXiiuOuo

Optionen

| Boardmail an "kalleari" |

Wertpapier: Suzlon Energy GDR |

Optionen

| Boardmail an "kalleari" |

Wertpapier: Suzlon Energy GDR |

The order for 100.8 MW wind farms has been awarded by ReNew Wind Power.

"The project is scheduled for execution at the Bhesada wind site, Dist Jaisalmer, Rajasthan," Suzlon said in a statement today.

....It is a repeat order placed by ReNew Wind Power. Sources said the order is worth around Rs 750 crore. Besides supplying 48 units of S97-120 m wind turbine generators, Suzlon Group would also oversee operations, maintenance and service of the wind site over the contracted period, the statement said.

Read more at:

http://economictimes.indiatimes.com/articleshow/...utm_campaign=cppst

Optionen

| Boardmail an "kalleari" |

Wertpapier: Suzlon Energy GDR |

Versorgung

Nordex

Herkunft Deutschland

Website www.nordex.de

Indizes/Listen

CDAX, HDAX, Prime All Share, TecDAX, mehr »

Aktienanzahl 80,9 Mio. (Stand: 02.01.14)

Marktkap. 1,35 Mrd. €

Suzlon

Website www.suzlon.com

GDR Basiswert INE040H01021

Verhältnis 1:4 (GDR : Basiswert)

Aktienanzahl 2.417 Mio. (Stand: 05.03.14)

Marktkap. 987,4 Mio. €

Optionen

| Boardmail an "kalleari" |

Wertpapier: Suzlon Energy GDR |

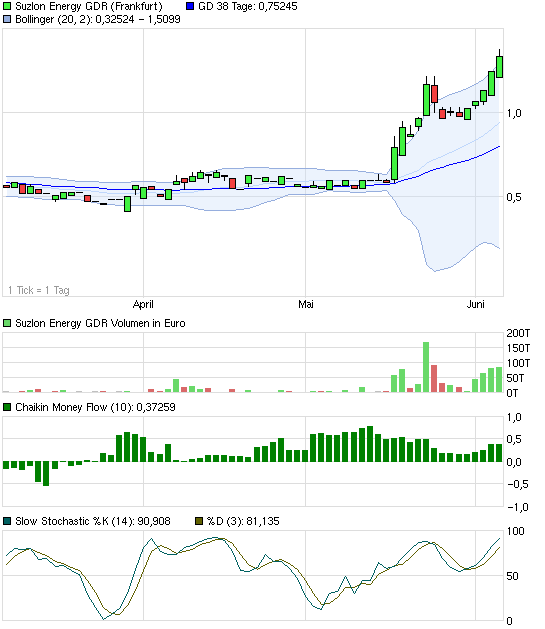

Angehängte Grafik:

suzlonenergygdr.png (verkleinert auf 93%)

suzlonenergygdr.png (verkleinert auf 93%)

Richten wir uns nach den Tagelinien und die zeigen einen beginnenden längerfristigen Aufwärtstrend.

Optionen

| Boardmail an "kalleari" |

Wertpapier: Suzlon Energy GDR |

die wollen senvion an der Börse gescheit verscherbeln und deshalb wird der Kurs hochgetrieben, koste es was es wolle, denn mit dem Verkauf ist dann herrlich viel mehr Geld zu machen.

Die Käuferherde beisst von selber den Köder und wenn mal nicht, dann kaufen die Banken nach, vermute ich.

Die PARTY geht noch bis zum Börsengang der senvion so weiter, hoffe ich....

Optionen

| Boardmail an "aktopus" |

Wertpapier: Suzlon Energy GDR |

Natürlich wollen sie mit Ex-RePower Geld verdienen und nicht nur das know-how ausschlachten. Da kann ich aber nichts Verwerfliches dran erkennen.

Hast Du noch im Kopf, was sie für RePower bezahlt haben? Wird schwer, das Ding mit Gewinn zu verkaufen.

Und wie Kalle schon sagte: Die MK ist ein schlechter Witz.

der ja nun deutlich unter den deutschen Kursen liegt

Suzlon Energy rose 4.92 per cent to Rs 29.85 after the company said it has been awarded a 100.8-MW order by ReNew Wind Power,schreibt indiatimes heute

0,369 Euro???

und in London gestern $1,80 das wären 1,322 Euro ,das sind wohl die neuen (4Stück)

http://www.londonstockexchange.com/exchange/...3USUSDIOBU&lang=en

Die Kapitalerhöhung war keinesfalls ein Witz ,sondern die Firma spart damit Geld ,weil die Zinsen auf indischen Krediten viel höher sind und sie hat erstmalig Eigenkapital

"The company is sitting on a net debt of Rs 12,700 crore and has interest cost of Rs 2,000 crore annually." Das ist wirklich sehr viel!

s.die schöne Analyse von http://smartinvestor.business-standard.com/market/...htm#.U5FXVyiuOup

In Indien will man anscheinend zu schnellen Anstieg verhindern !

Optionen

| Boardmail an "kalleari" |

Wertpapier: Suzlon Energy GDR |

CMP Rs61, Target Rs73, Upside 19.4%

WTG sales pick up, but continue to remain muted, 38% lower over the previous year as customers defer deliveries

Gross profit/MW improves to Rs24.6mn/MW during Q4 FY10 from Rs20.3mn/MW in Q3 FY10, expected to stabilize here

High depreciation and tax outgo coupled with lower other income translate into adjusted loss of Rs2bn

Order book and order inflow remain weak during the quarter, concerns on weak order book position continue

Reduce earnings to reflect weaker than expected FY11; but steep correction leaves room for upside despite cut in target price to Rs73/share, re-iterate BUY

sieht so aus ,dass es da eine Regel gibt

Optionen

| Boardmail an "kalleari" |

Wertpapier: Suzlon Energy GDR |