Das Bärengebrüll wird schon wieder lauter,

Seite 55 von 1170 Neuester Beitrag: 25.04.21 13:17 | ||||

| Eröffnet am: | 20.08.07 21:30 | von: aktienspezial. | Anzahl Beiträge: | 30.241 |

| Neuester Beitrag: | 25.04.21 13:17 | von: Andreaugqqa | Leser gesamt: | 2.492.630 |

| Forum: | Börse | Leser heute: | 2.208 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 52 | 53 | 54 | | 56 | 57 | 58 | ... 1170 > | ||||

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

Optionen

| Boardmail an "lackilu" |

Wertpapier: DAX |

gestern zu schwach heute zu stark

nochmal frage : warum handelst du dax und nicht nur dow, weil es dort mehr scheine gibt, weil der dax als deutscher naheliegernder ist ???

also mir reicht dow / nasdaq, wozu eigenltich dax etc ???

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

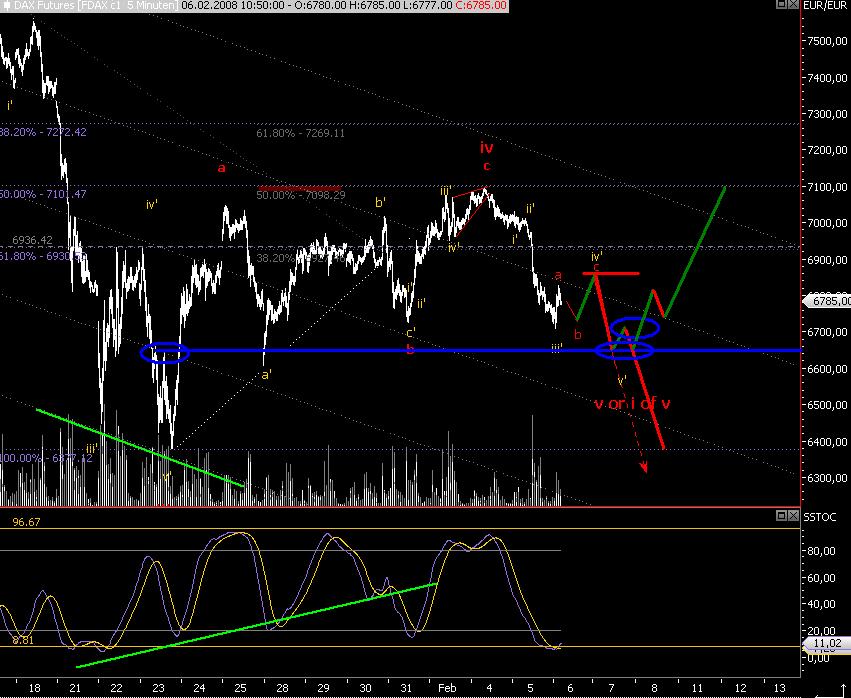

Angehängte Grafik:

2008-02-06_230831.png (verkleinert auf 76%)

2008-02-06_230831.png (verkleinert auf 76%)

7. Februar 2008 - Geldpolitische Beschlüsse

Auf der heutigen Sitzung beschloss der EZB-Rat, den Mindestbietungssatz für die Hauptrefinanzierungsgeschäfte sowie die Zinssätze für die Spitzenrefinanzierungsfazilität und die Einlagefazilität unverändert bei 4,00 %, 5,00 % bzw. 3,00 % zu belassen.

Der Präsident der EZB wird die Überlegungen, die diesen Beschlüssen zugrunde liegen, heute um 14.30 Uhr (MEZ) auf einer Pressekonferenz erläutern.

Europäische Zentralbank

Direktion Kommunikation

Abteilung Presse und Information

Kaiserstraße 29, D-60311 Frankfurt am Main

Tel.: +49 69 1344 7455, Fax: +49 69 1344 7404

Internet: http://www.ecb.europa.eu

Nachdruck nur mit Quellenangabe gestattet.

Ich persönlich glaube nicht daran (deckt sich mit der Aussage der FED gestern, ggf. von weiteren Senkungen abzusehen im Hinblick auf die Infla - Tendenzen)

Optionen

| Boardmail an "Trüffelschwein07" |

Wertpapier: DAX |

M.E. taugen die Chartbilder immer noch--entweder durch die 6700 und (hoffentlich ) den 6650 er Bereich. Dann gehts wohl down bis 6400-; oder wir drehen bei 6700/6650 bei, dann sollte man wohl Longinger bevorzugen. So verstehe ich AS.

Ciao B.L.

Gratulation, Godmode !

Optionen

| Boardmail an "Trüffelschwein07" |

Wertpapier: DAX |

Optionen

| Boardmail an "Trüffelschwein07" |

Wertpapier: DAX |

Jean-Claude Trichet, President of the ECB,

Lucas Papademos, Vice President of the ECB

Frankfurt am Main, 7 February 2008

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. Let me report on the outcome of our meeting, which was also attended by Commissioner Almunia.

On the basis of our regular economic and monetary analyses, we decided at today’s meeting to leave the key ECB interest rates unchanged. This decision reflects our assessment that risks to price stability over the medium term are on the upside, in a context of very vigorous money and credit growth. The current short-term upward pressure on inflation must not spill over to the medium term. The firm anchoring of inflation expectations over the medium and long term is of the highest priority to the Governing Council, reflecting its mandate. Against this background, the Governing Council remains committed to preventing second-round effects and the materialisation of upside risks to price stability over the medium term. As the reappraisal of risk in financial markets continues, there remains unusually high uncertainty about its overall impact on the real economy. While the economic fundamentals of the euro area are sound, incoming data have confirmed that the risks surrounding the outlook for economic activity lie on the downside. We will continue to monitor very closely all developments over the coming weeks.

Allow me to explain our assessment in greater detail, starting with the economic analysis.

The latest information on economic activity around the turn of the year points to a more moderate pace of growth in the euro area than the quarter-on-quarter rate of 0.8% observed in the third quarter of 2007. This assessment is in line with indicators for business and consumer confidence which, while having declined over the past few months, overall remain consistent with ongoing growth.

Looking ahead, while the slowdown in the economies of some of the euro area’s major trading partners is likely to have an impact on euro area real GDP growth in 2008, both domestic and foreign demand are expected to support ongoing growth. This assessment is broadly in line with available forecasts from private and public-sector sources. The fundamentals of the euro area economy remain sound. The euro area economy does not have major imbalances . Profitability has been sustained and unemployment rates have fallen to levels not seen for 25 years. As a result of the improved economic conditions and wage moderation, the number of people employed and labour force participation have increased significantly. Consumption growth should therefore continue to contribute to economic expansion, in line with real disposable income, and investment growth should provide ongoing support.

That said, uncertainty about the prospects for economic growth is unusually high and the risks surrounding the outlook for economic activity have been confirmed to lie on the downside. Risks relate mainly to a potentially broader than currently expected impact of financial market developments on financing conditions and economic sentiment, with negative effects on world and euro area growth. Further downside risks stem from the scope for additional oil and other commodity price rises, concerns about protectionist pressures and the possibility of disorderly developments due to global imbalances.

With regard to price developments, according to Eurostat’s flash estimate the annual HICP inflation rate was 3.2% in January 2008, compared with 3.1% in December 2007. This confirms the continued strong upward pressure on inflation in the short term, stemming mainly from strong increases in commodity prices, in particular oil and food prices, in recent months.

Looking ahead, the annual HICP inflation rate will most likely remain significantly above 2% in the coming months and moderate only gradually in the further course of 2008. This confirms our expectation of a protracted period of temporarily high rates of inflation. Moreover, it is important to stress that the moderation in the rate of inflation which is embedded in the December 2007 Eurosystem staff macroeconomic projections is based on the assumption that the recent rises in commodity prices will be partly reversed, in line with futures prices. More fundamentally, the projections assume that recent oil and food price dynamics and their impact on HICP inflation do not have broadly-based second-round effects on wage and price-setting behaviour.

Risks to this medium-term outlook for price developments are confirmed to lie on the upside. These risks include the possibility that stronger than currently expected wage growth may emerge, taking into account high capacity utilisation and tight labour market conditions. Furthermore, the pricing power of firms, notably in market segments with low competition, could be stronger than expected. At this juncture, it is therefore imperative that all parties concerned meet their responsibilities and that second-round effects on wage and price-setting stemming from current inflation rates be avoided. In the view of the Governing Council, this is of key importance in order to preserve price stability in the medium run and thereby the purchasing power of all euro area citizens. The Governing Council is monitoring wage negotiations in the euro area with particular attention. Indexation of nominal wages to the consumer price index should be avoided. Finally, further rises in oil and agricultural prices, continuing the strong upward trend observed in recent months, as well as increases in administered prices and indirect taxes beyond those foreseen thus far pose upside risks to the inflation outlook.

The monetary analysis confirms the prevailing upside risks to price stability at medium to longer-term horizons. Annual M3 growth, although declining somewhat in December, remained very vigorous at 11.5%, whereas M1 growth continues to moderate, reflecting the dampening impact of higher interest rates. Broad money dynamics in recent quarters are likely to have been influenced by a number of temporary factors, notably the flattening of the yield curve, which may have supported some substitution into monetary assets. Overall, taking these special factors into account, a broad-based assessment of the latest data confirms that the underlying rate of monetary expansion remains strong.

This conclusion is supported by the sustained expansion of loans to the domestic private sector, which grew at an annual rate of 11.1% in December. Although the growth of household borrowing has moderated further over the past few quarters, reflecting the impact of higher key ECB interest rates since December 2005 and cooling housing markets in several parts of the euro area, the growth of loans to non-financial corporations has remained very robust. Bank borrowing by euro area non-financial corporations was 14.4% higher at the end of December 2007 than a year earlier.

For the time being, there is little evidence that the financial market turbulence since early August 2007 has strongly influenced the dynamics of broad money and credit aggregates. In particular, according to the available data, increased financial market volatility has not led to substantial portfolio shifts into monetary assets, as was the case between 2001 and 2003. Notwithstanding the tightening of credit standards reported in the bank lending survey for the euro area, continued strong loan growth suggests that the supply of bank credit in the euro area has not been significantly impaired by the financial turmoil thus far. Further data and analysis will be required in order to obtain a more complete picture of the impact of the financial market developments on banks’ balance sheets, financing conditions and money and credit growth.

To sum up, a cross-check of the outcome of the economic analysis with that of the monetary analysis confirms the assessment that there are upside risks to price stability over the medium term, in a context of very vigorous money and credit growth and sound economic fundamentals in the euro area. The impact of the ongoing reappraisal of risk in financial markets on the real economy is still surrounded by unusually high uncertainty. Incoming data have confirmed that the risks surrounding the outlook for economic activity lie on the downside. Accordingly, we will monitor very closely all developments. The Governing Council remains committed to preventing second-round effects and the materialisation of upside risks to price stability over the medium term. It is paramount that medium and long-term inflation expectations remain firmly anchored in line with price stability. Reflecting its mandate, such anchoring is of the highest priority to the Governing Council.

With respect to fiscal policies, a discretionary fiscal loosening in EU countries should be avoided. There is ample evidence that activist fiscal policies were not effective in stabilising European economies but rather led to sustained increases in the ratios of government expenditure and debt to GDP. Allowing the free operation of automatic stabilisers in countries with strong fiscal positions and safeguarding the long-term sustainability of public finances are the best contributions that fiscal policy can make to macroeconomic stability. Countries with fiscal imbalances are urged to make further progress with consolidation, in line with the requirements of the Stability and Growth Pact. There is a clear risk that some countries will fail to comply with the provisions of the preventive arm of the Pact, thereby undermining its credibility.

Structural reforms help economies to adjust to adverse shocks, foster productivity growth and increase employment and competition, thereby also helping to reduce inflationary pressures. In particular, enhancing competition in the services sectors and network industries, as well as applying adequate measures in the EU agricultural market, would be conducive to price stability in the euro area.

We are now at your disposal for questions.

European Central Bank

Directorate Communications

Press and Information Division

Kaiserstrasse 29, D-60311 Frankfurt am Main

Tel.: +49 69 1344 7455, Fax: +49 69 1344 7404

Internet: http://www.ecb.europa.eu

Optionen

| Boardmail an "Trüffelschwein07" |

Wertpapier: DAX |

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

Optionen

| Boardmail an "lackilu" |

Wertpapier: DAX |

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

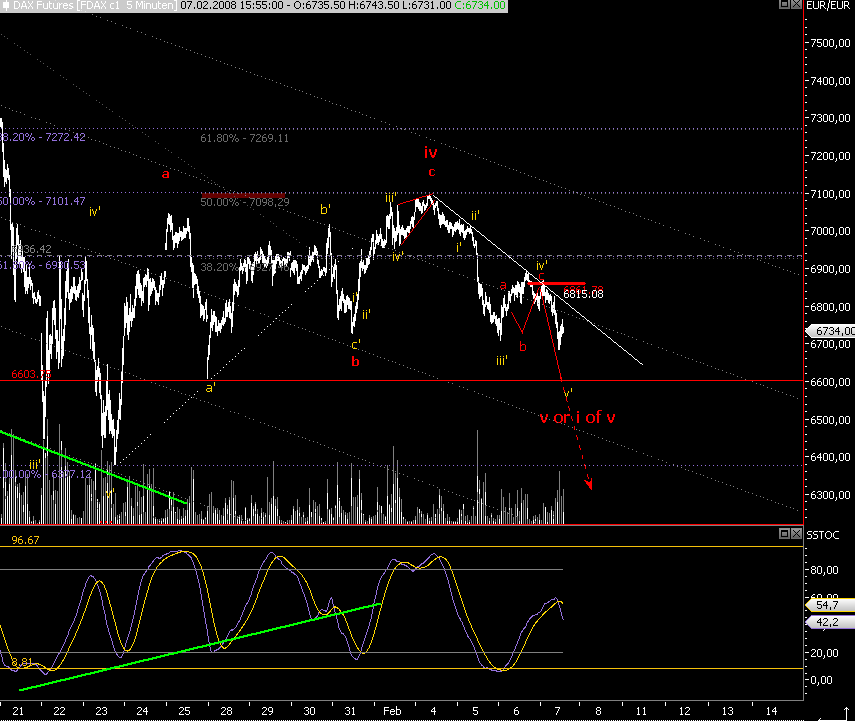

Angehängte Grafik:

2008-02-07_154831.png (verkleinert auf 63%)

2008-02-07_154831.png (verkleinert auf 63%)

Angehängte Grafik:

geklaut_as.jpg (verkleinert auf 59%)

geklaut_as.jpg (verkleinert auf 59%)

schauen wir mal.. dank dir erstmal.. wäre nett, wenn du mich auf dem laufenden halten könntest...

Gruss

M.

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

Optionen

| Boardmail an "aktienspezialist" |

Wertpapier: DAX |

Angehängte Grafik:

2008-02-07_160813.png (verkleinert auf 59%)

2008-02-07_160813.png (verkleinert auf 59%)