forsys neue Kursrakete ?

Seite 52 von 562 Neuester Beitrag: 25.04.21 01:15 | ||||

| Eröffnet am: | 26.03.06 12:18 | von: Cincinnati | Anzahl Beiträge: | 15.039 |

| Neuester Beitrag: | 25.04.21 01:15 | von: Katharinazbo. | Leser gesamt: | 2.406.662 |

| Forum: | Hot-Stocks | Leser heute: | 567 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 49 | 50 | 51 | | 53 | 54 | 55 | ... 562 > | ||||

Optionen

| Boardmail an "oligator" |

Wertpapier: Forsys Metals Corp |

Denke der Entscheidende Außlößer war dieser Satz hier:

We expect to have a resource update completed within the next 30 days or so

February 9, 2007

Forsys Metals Corp

featuring President Wayne Isaacs

highlights from audio appear below

Questions:

1. Wayne, can you give us a brief overview of your company’s Valencia uranium deposit in Namibia and some of the background behind the previous exploration?

Valencia is our flagship resource property in Namibia, the historic resource drilling was performed by Goldfields in the late 70s and into the 80s. That amounted to about 23,000 meters or so of drilling. The majority of the core samples were available to us and we were able to use this material as a basis of our 43-101 report. That report yielded inferred resource of approximately 21.6 million pounds of uranium.

2. For the past year Forsys Metals has quietly been working under the radar screen, and only recently has your company’s shares dramatically jumped. Does this have something to do with Paladin opening their nearby uranium mine?

3.Your company has developed strong relationships within the government of Namibia. Can you tell us how this has benefited and is benefiting Forsys Metals, and how this will benefit Forsys Metals in the future?

Text zur Anzeige gekürzt. Gesamtes Posting anzeigen...

4. When we began covering Forsys Metals, your company was following on the coattails of Paladin Resources, which has become a major success story in the uranium sector. Now there are more than 20 companies exploring for uranium in Namibia. What advantage does Forsys Metals have over others, such as UraMin?

Paladin’s success has definitely helped shine a spotlight on Namibia and by extension placed a spotlight on Forsys and the Valencia project as the next uranium success story. Please keep in mind that we’re in very close proximity to two producing uranium mines, that being Paladin and the Rossing mine which has further fast tracked our ability to bring Valencia possibly to being the third production uranium mine in Namibia.

5. The prefeasibility study for the Valencia project is nearly wrapped up. Results should be out shortly. Your CEO is now in Africa. What can we expect about Forsys Metals moving this project into production?

We expect to have a resource update completed within the next 30 days or so. We also expect to commence our bankable feasibility within that time frame. On the heels of that there are five more uranium exploration projects expected to be generated out of our relationship with AnCash Investments. We’ve also recently announced the spin out of our non-uranium assets. So you can see we’re moving toward becoming a pure uranium company, to where we’re very excited about the future, we’re looking forward to making that production decision and moving ahead.

6. Who will be opening the next uranium mine in Namibia – Forsys or UraMin?

I guess I’m a little bit biased, but I believe that we’re closer to opening up the next uranium mine in Namibia. We’ve advanced our project, in my opinion, further at this stage than UraMin has.

7. Who is likely to have more production by the end of the decade – Forsys or UraMin?

That is unclear right now. We have other exploration targets that we’re looking into. We have the newly discovered Joly zone which we haven’t drilled yet. UraMin hasn’t come out with a resource definition at this particular point in time, so we’re not entirely certain. But again, being on the bias side, I’m rooting for Forsys.

Optionen

| Boardmail an "oligator" |

Wertpapier: Forsys Metals Corp |

Optionen

| Boardmail an "oligator" |

Wertpapier: Forsys Metals Corp |

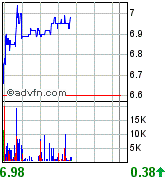

Angehängte Grafik:

unbenannt.bmp

unbenannt.bmp

Optionen

| Boardmail an "oligator" |

Wertpapier: Forsys Metals Corp |

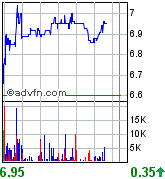

Angehängte Grafik:

unbenannt.bmp

unbenannt.bmp

Optionen

| Boardmail an "oligator" |

Wertpapier: Forsys Metals Corp |

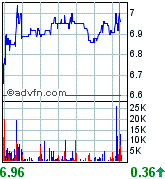

Angehängte Grafik:

unbenannt.bmp

unbenannt.bmp

Weitere Übersicht über den Zeitplan/wichtige Daten bei Forsys:

I have tried to summarize some FSY key numbers/facts below.

If...

...FSY management follow their plan

...U308 spot continues to climb

...succesful spin out of non uranium assets is accomplished

=> This equals great potential IMHO

+21 M lbs U3O8 inferred at 0,20kg/t

Q1-07 43-101 resource update...

Q1-07 commence of bankable feasibility study

Q3-08 mine construction begins...

Q3-09 start of production @ 2.5 M pounds/yr

$120 M investment for the mine

$25/lb production cost (high(!) estimate)

47 M shares outstanding

61 M shares fully diluted (=C$25M cash)

10 M shares @ $4,75 recent financing...

=> 71 M shares fully diluted (debt finance)

=> $1,65/share cashflow 2009 ($72 U3O8)

Optionen

| Boardmail an "oligator" |

Wertpapier: Forsys Metals Corp |

die rally ist im vollem gange...

Die Geduld bei dieser Aktie wird sich Auszahlen, ich bleibe auch weiterhin bei dem Spruch wer hier verkauft hat nicht verstanden was hier entsteht ;-)

Und solche Korrekturen bis zu (Minus 15% / 20%) sind bei Rohstoffaktien nichts ungewöhnliches...

Optionen

| Boardmail an "oligator" |

Wertpapier: Forsys Metals Corp |

A six-week long stalemate on the spot price of uranium has finally broken, with the price of the metal ticking up $3 to $75 per pound, according to Ux Consulting. Uranium investors have been holding their collective breath, waiting to see if uranium’s recent plateau was a peak. The answer seems to be, “not yet.” Indeed, my target for the metal is $100 per pound by the end of this year.

It could be a bumpy ride, though. I’ll tell you about forces that should drive uranium higher, as well as a few that could drive it lower in the short term.

An M&A frenzy in the uranium mining industry

Two weeks ago, I attended the 2007 Vancouver Resource Investment Conference. The size of the conference blew my mind! There were way more exhibitors than last year, and the hall was jampacked with investors looking for Canada’s natural resource bargains.

They were finding them, too - in gold, silver, lead, zinc, nickel, diamonds and many other things. And my favorite metal, uranium, is so hot that the exhibitors set up a special “Uranium Alley” so investors could find these companies more easily.

As I talked to miners at the conference, a couple of things became clear:

Staff is at a premium. Rockhounds love what they do, but even they can’t do it forever. And when the price of uranium cratered in the 1980s, staffs were decimated. About 20,000 engineers and geologists worked in the uranium sector in American companies during the last uranium boom. That number is about 400 now, too many of whom are close to retirement age. So if you can find a company with a fairly “deep bench” of uranium mining experts on its payroll, those guys are worth their weight in gold.

One solution to the staffing shortage: mergers. If two companies each with three expert rockhounds merge, that company now has six experienced prospectors to work on the best of its projects.

Speaking of projects…

Patchwork quilt of claims lays groundwork for merger mania. Look at a map of any uranium-prospective territory and you’ll see a patchwork quilt of claims. Heck, I could practically see some deals coming to mind across the exhibitor booths, as CEOs of various companies finally got a chance to get together.

I imagine the conversations started something like this: “Hey, you have two working projects in the Athabasca Basin, and I’ve only got one claim there and no time to work it. Meanwhile, you’ve got a stray property near my project in Wyoming. Let’s make a deal!”

These two factors should pump up M&A activity in an industry that is already riding a growing flow of investor cash. I even got the feeling at the conference that if I changed my name to Sean Uranium Inc., suddenly I’d find myself raising a ton of cash pretty quickly.

Well, that’s half in jest. But I’m dead serious about the forces driving uranium, though - forces that are approaching critical mass…

Why the second wave of the uranium bull market is about to begin

I call uranium the “white-hot metal,” and not only because it glows in the dark. During the course of 2006, the uranium spot market price continually climbed by 99%, from $36.25 to $72 per pound of U3O8. At $75 per pound, the price is now more than 10 times its record low of $7 per pound that it hit in 2000.

The first big move in uranium is over - the next one is about to begin. And if uranium prices DOUBLE from here - which I think could easily happen -- some of these small-cap wonders I’m looking at could go to the moon.

I believe we’re poised to enter the “Second Wave” of uranium’s big bull market…probably the biggest bull market the world has ever seen.

Despite the big bull rally in uranium over the past couple years, on a historical basis, it’s still dirt-cheap! Uranium hasn’t come anywhere near its old peak in inflation-adjusted terms. In 1978, uranium topped out at $43.40 per pound - but adjusted for inflation, that’s around $145 per pound in today’s dollars. It’s now trading at $75 per pound. That means uranium could nearly DOUBLE and still not surpass its old inflation-adjusted highs.

That’s why I think we’re looking at $100 uranium by the end of this year - a 39% move from recent levels. Pretty sweet - and even then, uranium will still have plenty of room to run! How high? Let me show you…

Forces that will drive uranium price to $100 a pound - and beyond

Force #1: The Supply/Demand Gap

Consider these facts...

1. About 16% of the world\'s electricity came from 440 nuclear reactors last year, according to the World Nuclear Association. Currently, there are 28 reactors under construction around the world and another 62 being planned:

- Japan intends to add 11 by 2010

- China hopes to add as many as 30 by 2020. More on China in just a bit…

- India wants to build up to 20 more

- Russia’s energy goals call for at least 42 new nuclear reactors...perhaps as many as 58!

2. An additional 100 plants will be built in the next 10 years, with 40 of them in Asia.

3. Bottom line: By 2050, scientists estimate the world will need about 900 more nuclear power plants to keep up with growing energy requirements.

As a result, the undeniable reality is that demand for uranium is outstripping supply. In 2005...

• Supply from mines was 102.5 million pounds

• Demand was 171 million pounds

• The gap was 68.5 million pounds.

Totals for 2006 aren’t in yet, but demand probably topped 180 million pounds. And as new nuclear power plants come online, that demand will grow. A typical 1-gigawatt nuclear reactor requires around 200 metric tonnes of natural uranium per year. During startup, a new nuclear plant can use TRIPLE its normal requirements.

The fact is production from world uranium mines now supplies only 62% of the requirements of power utilities. The rest is made up from rapidly dwindling stockpiles, mainly old Russian nuclear warheads that are converted to material for power plants. That agreement expires in 2013, and won’t likely be renewed, since the Russians have a very ambitious nuclear program of their own.

Moreover, here in the U.S., utility consumption of uranium outpaces U.S. uranium production by more than 20-to-1.

Force #2: Crisis at Cigar Lake

Uranium prices were already climbing steadily when the nuclear power industry was rocked in October by disastrous news out of Cameco’s Cigar Lake Mine.

Cameco planned to bring Cigar Lake online in 2008, with 7 million pounds of uranium in the first year and full-scale production of 18 million pounds annually thereafter. Keep in mind, 18 million pounds is more than a tenth of last year\'s total global demand of 171 million pounds. That’s like the global oil market losing Saudi Arabia’s production!

In 2008, uranium demand was already expected to exceed supply by 25 million pounds. With Cigar Lake seriously delayed, that gap will be 32 million pounds. Put another way - the shortfall in uranium is going to soar by 30% just in 2008.

Sure, Cigar Lake will be brought into production eventually. But meanwhile, demand keeps building up. Uranium consumers around the world can see this squeeze coming, so the race is on. That explains why spot uranium prices basically doubled in the course of a year, and the stocks of near-term uranium producers vaulted higher.

Cigar Lake could be a force driving uranium prices this year both UP and down. I’ll tell you more about that in just a bit.

Force #3: China, the Uranium-Devouring Monster

China deserves mention as a force all its own. How hungry is China for uranium? The Chinese are hot-footing it through the Australian outback with bags of cash, investing in the best small companies sitting on large quantities of uranium. And no wonder! China plans to import 2,500 metric tonnes of Australian uranium per year by 2020, as it builds 24-30 new atomic power plants.

The really bullish news is that China’s total expected annual uranium demand is three times as much - 7,500 metric tonnes. And it will use every pound of it, as China plans to construct two new 1,000-megawatt nuclear reactors every year, including two coming online this year.

Force #4: Global Warming Trumps Everything

Fact: The 11 hottest global temperature years (since records began in 1861) have been since 1990.

The ice caps are melting at an alarming pace. And whether it’s hurricanes in the Atlantic or typhoons in the Pacific, storms are whipping up with an intense fury. Unless your name is “ExxonMobil,” there is very little argument about why this is happening. A normal global warming cycle is being worsened by man-made pollution - greenhouse gasses that trap heat.

And though people rant and rave about gas-sucking SUVs, the biggest source of greenhouse gasses (apart from methane-farting cows and other livestock) is coal-fired power plants. People point to the fact that China is building a new coal-fired plant every week and shake their heads. Well, here in the U.S., we have about 150 new coal plants planned or already being built. Many of these are using “old-coal” technology for cost savings.

It’s almost as if China and the U.S. are engaged in some kind of suicide pact. And I doubt it’s going to have a happy Hollywood ending. There is hope, though. Awareness of the crisis of global warming is becoming so acute that major corporations are joining forces with environmental groups in an unprecedented alliance to push for quicker action on global warming.

The alliance of greens and Corporate America is called the U.S. Climate Action Partnership, and we’re talking some really BIG names here: Alcoa, BP America, DuPont, General Electric, FP&L Group, and more. One of the solutions to global warming is nuclear power.

Here’s why: An operating nuclear power plant produces zero greenhouse gases. Compare that with your average coal plant, which can spew 3.7 million tons of carbon dioxide (a greenhouse gas) into the air every year, along with hundreds of tons of heavy metal-laden ash.

I expect public awareness on this issue to grow over the next few years and the public to start demanding utilities make the switch. This boosts nuclear power in two ways - increasing demand for uranium at power plants and lifting bans and overregulation on mining.

Force #5: Peak Oil and Peak Natural Gas

In 2006, global oil demand grew 0.9%, thanks to steady growth in China and the Middle East. The world used 84.5 million barrels of oil per day last year, according to the International Energy Agency. That’s nearly 31 billion barrels, and the most oil used in a year...EVER. What’s more, world demand is forecast to rise 1.6% this year to 85.77 million barrels a day.

Worldwide oil and gas reserves are becoming depleted at an ever increasing rate, with many analysts convinced that we are fast approaching Peak Oil and Peak Natural Gas.

In fact, the former Soviet Republic Belarus, which was hardest hit by the Chernobyl nuclear accident, is pulling out all the stops to accelerate its nuclear energy program. Reason: President Alexander Lukashenko is desperate for an alternative to Russian natural gas that is fast rising in price.

If Belarus is embracing nukes, I believe even the most die-hard holdouts won’t be far behind.

Force #6: Nuclear power looks cheaper all the time.

Standard & Poor’s recently published a study showing that the next wave of nuclear power plants should be able to produce electricity at $55 per megawatt hour, versus the average rate of $50 per megawatt hour at a coal plant.

Even the $55 figure may prove conservative, because the second wave of nuclear plants could benefit from standardization. All told, the cost of a megawatt hour could potentially drop to about $44!

That’s right: Nuclear power could end up being cheaper than coal, and without the tons of greenhouse gases and poisonous ashes that coal plants spew into the atmosphere.

Force #7: The Feeding Frenzy Could Get Even MORE Intense Next Year

Most uranium is sold under long-term contracts. But the utilities that contracted for uranium in the Future are finding they’re coming up short, and for good reason: When a nuclear reactor is first fired up, it can use TRIPLE its normal amount of uranium oxide.

While the price of uranium is rising, suppliers can still scrape together enough to meet demand. But come 2008, we may reach a tipping point. A lot of uranium users don’t seem to have enough contracts to cover their needs. And many of the contracts they do have are ending - which means suppliers can negotiate at MUCH higher prices.

So if you think uranium prices have been on a tear so far, just wait…2008 could be an even more intense feeding frenzy.

And when you come down to it, we should see prices move well in advance of that. That, in turn, should take the stocks of small, well-managed companies sitting on big resources and potentially send them ballistic!

Can Uranium Prices Come Down Temporarily? Heck, Yeah!

In fact, I’m hoping we get a pullback. That would be a golden buying opportunity.

Reasons for a short-term fall in the uranium price

1. Russian imports. Right now, Russia has two choices. It can sell uranium to the U.S. market through the United States Enrichment Corp. (USEC) or it can pay a 116% tariff. But Russian-owned Techsnabexport is working on a new civilian nuclear power deal between Russia and the U.S. You can bet that U.S. utilities, desperate for lower-cost uranium, are pushing hard for this deal, which could come as soon as the first quarter of 2007.

2. Cigar Lake update. Last week, Cameco announced it expects to seal off water flow to its Cigar Lake uranium mine by the second quarter. But it has delayed preliminary cost estimates and timelines, which were supposed to come out in February, until late March.

Does that sound to you like Cameco’s going to get that mine back online anytime soon? It sure doesn’t sound like it to me.

So Cameco is STILL having trouble stopping water from flooding the mine. One engineer I spoke to in Vancouver joked that so much water is pouring in, Cameco should stop trying to mine uranium at Cigar Lake and turn it into a hydroelectric project.

Nonetheless, it would be surprising if the March report isn’t upbeat.

Corporations have a way of putting even the worst news in the best light…and maybe Cameco will surprise everybody by reporting actual good news.

On the other hand, if Cameco pushes its timeline for Cigar Lake back by years, uranium could lift off the launch pad.

3. Overspeculation. I like speculation as much as the next guy, but according to a recent update from TradeTech’s Nuclear Market Review, “Speculators are holding about 24 million pounds of U3O8 equivalent.” That is about 22% of global uranium production in 2005.

So if Cameco announces good news on Cigar Lake, or if Russia’s Techsnabexport hammers out a trade deal, speculators could decide to sell, temporarily exaggerating any short-term decline. The Uranium Participation Corp. is holding a bunch of uranium with the intention of selling to utilities at a higher price at a later date. If prices start to go down, the fund could decide to start unloading.

SUMMARY: I expect a pullback in uranium prices this year, but it will be a short-term correction in a big bull market. What I recommend is you put HALF your money to work NOW, then put the rest to work if and when we get a sizeable pullback.

If uranium doesn’t pull back, at least you’re in the game. If uranium does pull back, you’ll average in for a better price.

http://www.moneyweek.com/file/25277/...ce-will-hit-100-this-year.html

Optionen

| Boardmail an "oligator" |

Wertpapier: Forsys Metals Corp |

unsere geduld hier zahlt sich immer mehr aus, auch nach mehreren hundert prozent gewinn gibt es nur einen weg!!!

wünsche eine schöne börsenwoche

Optionen

| Boardmail an "oligator" |

Wertpapier: Forsys Metals Corp |