Der USA Bären-Thread

Seite 439 von 6257 Neuester Beitrag: 06.07.25 13:32 | ||||

| Eröffnet am: | 20.02.07 18:45 | von: Anti Lemmin. | Anzahl Beiträge: | 157.419 |

| Neuester Beitrag: | 06.07.25 13:32 | von: Frieda Friedl. | Leser gesamt: | 25.577.297 |

| Forum: | Börse | Leser heute: | 630 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 437 | 438 | | 440 | 441 | ... 6257 > | ||||

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

Freddie Mac hat heute nachbörslich erklärt, dass die Dividende (zuvor 7,7 % beim aktuellen Kurs) halbiert wird.

The $7 Billion Solution?

By Steven Smith

Senior Columnist

11/27/2007 11:06 AM EST

Shares of Citigroup (C) have slipped into the red and are trading back below the $30 level. Investors apparently used the early bump in price as a chance to unload shares.

Even though the Option Alert Model portfolio is long the Financial SPDR Select (XLF), of which Citi at 6% is the heaviest weighted component, I can't say I blame those who bailed out. In the big picture, $7 billion is not really a huge investment for a company that has some $2.5 trillion in assets, is still probably less than a third of the amount of mortgage related losses the it will ultimate take [Smith übersieht offenbar, was ich oben zur Tier-1 capital und leverage geschrieben hab] and most important, does next to nothing to address the long-term structural and managerial problems facing the company. Still, maybe this at least quiets the concerns about a cut in the dividend and helps put some sort of floor under the shares at the $28 level.

Option activity is heavily tilted to the put side, with some 180,000 puts trading to just 55,000 calls thus far. Most of the volume is focused in the January $25, $27.50 and $30 strikes, which have combined to trade more than 90,000 contracts, matching the current open interest of the three strikes.

By Gary Douglas Smith

Street.com

...Last night, Citigroup (C) announced that it had sold as much as a 4.9% stake in itself to the Abu Dhabi government for $7.5 billion. This could provide a much-needed confidence boost to the stock and the heavily shorted financial sector.

The NYSE reported last Wednesday that total short interest on the exchange rose another 3.8% over the first two weeks of the month, to 12.38 billion shares. Moreover, short interest on the Amex, where many ETFs trade, jumped 11.9%. Short interest in the Financial Select Sector SPDR (XLF) rose by 18,739,906 shares, to 116,045,478 shares. It is still the second most heavily shorted security on the exchange and the most heavily shorted sector ETF.

I expect stocks to finish the day modestly higher on strength in the financial sector and short-covering. I am positioned 75% net long heading into the day.

Stöffen: klar, careful. Es wäre ein großer Fehler, diesen Trade, falls er gegen einen läuft, durch Nichthandeln in ein "Investment" umzuwandeln. Hab auch keine große Posi.

Egal, wir werden sehen was kommt. Auf jeden Fall ist Long kein "Hochverrat", als Bär mit Familie kann man schließlich nicht nur von Erdnüssen (Peanuts) leben.

Wie gesagt, etwas weniger Emotion bitte.

Im XLF sind auch die Versicherer mit drin, nicht nur die Banken. Ob das wirklich ein Plus ist, muss sich allerdings noch rausstellen (Swiss Re lässt grüßen...).

Im Eingangsposting steht nur, "dass man mit einem Rückgang rechnen muss", nicht wie man damit sein Geld zu verdienen hat. ;-)

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

;o)

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

Auch mein Trade beruht auf der Annahme einer Bearmarket-Rally und hat nichts mit langfristig bullish zu tun. Mit der Absicherung hast du natürlich recht, nur muss man ab und zu was wagen um was zu verdienen. In die eine oder andere Richtung. Wichtig ist, eine Rally in der jetztigen Situation nicht auszureizen, denn sie wird nicht lange laufen.

Gute Nacht, für heute reichts mir.

Bis dahin ……

Euer Stöffen

Wenn's so ist, gut, long is on.

Mein Problem mit Long derzeit ist aber, daß keiner weiß, wann der nächste Hammer kommt, der mich prompt auf dem falschen Fuß erwischt. Deshalb bin ich derzeit, wenn überhaupt mal long, maximal gestreßt und nach spätestens 6 Stunden entnervt wieder draußen, und das lohnt dann den Streß nicht.

Barclays und Citi heute mit positiver Überraschung, und was ist mit etrade, den monolines, und den maximal EK- und Einlagendefizienten GB-Spezis aus der Ecke um Northern Rock, und den ganzen Beteuerungen der ZBs gerade in den letzten Tagen, notfalls auch weiterhin Liquidität bereitstellen zu wollen? Noch genug Tretminen am Wegesrand, oder?

Hierzu eine kurze Anmerkung zu den Sentiment-Indikatoren: der Mechanismus, daß man long gehen kann, wenn die breite Berichterstattung am negativsten ist, hat häufig gut funktioniert (Titelblatt-Indikator, Kanonendonner, u.v.m.). Es ist aber auch die Situation vorstellbar, daß erst das smart money alert ist, dann die breite Masse die Krise verzögert verinnerlicht, und hey, alle haben recht, die Kacke ist wirklich am dampfen, und die breite Erkenntnis derselben bedeutet keineswegs den Wendepunkt der Krise, sondern deren Fortsetzung. Solange das noch im Raum steht, ist antizyklisches Trading wirklich riskant, auch mit SL.

Ich bleibe also lieber short, mal mehr, mal weniger, aber nicht wirklich long ...

Good n8, Isc.

Optionen

| Boardmail an "Ischariot MD" |

Wertpapier: S&P 500 |

Optionen

| Boardmail an "Ischariot MD" |

Wertpapier: S&P 500 |

Die Gefahren sind hier ja Allen (inszwischen sogar Lehna!) hinlänglich bekannt ;-))

(Es war noch nie wirklich leicht, an der Börse Geld zu verdienen.)

Angehängte Grafik:

big.gif (verkleinert auf 88%)

big.gif (verkleinert auf 88%)

Wenn Metro jetzt tendenziell bullisch ist (da selber long) und Malko tendenziell skeptisch (da in sicheren Staatsanleihen), ist das für beide Seiten verständlich. Jeder versucht halt, das eigene Engagement zu rechtfertigen - vor sich selbst wie hier im Thread. Solange das nicht in zwanghafte Beschwörungen oder Verschwörungstheorien ausartet, ist das auch in Ordnung so. Schwieriger wird es, wenn eine Fraktion versucht, die andere zu belehren. Unerträglich wird es, wenn der Streit in Beleidigungen mündet.

Ariva - das Spiegelbild der deutschen Anleger-Seele ;-))

Whitney's Halloween report downgraded the stock to market underperform, the equivalent of a "sell." But that was just the beginning. She predicted that Citi would be forced to cut its dividend and shed valuable assets to boost its ratio of tangible capital to assets, which had fallen to 2.8%, just over half the level of its peers.

Whitney began work on the report in early October, after Citi reported a dramatic decline in earnings and took a third-quarter writedown of $6.5 billion. She issued the report to coincide with the Fed's Oct. 31 meeting, which warned of slowing economic growth. That was bad news for banks, which already have reported huge writedowns related to subprime mortgages.

Whitney reasoned that given the current economy, the bank didn't have the means to boost its capital ratios through organic growth. She argued that cutting the dividend or selling assets was the only quick way to raise cash. She predicts that "in six to 18 months, Citi will look nothing like it does now. Citi's position is precarious, and I don't use that word lightly," she says. "It has real capital issues." Citi is likely to report an additional $8 billion to $11 billion in writedowns for the fourth quarter.

The report hit the stock market with the force of a freight train slamming into a brick wall. Citi shares fell 7% Nov. 1, as analysts at Morgan Stanley (MS) and Credit Suisse (CS) followed with their own downgrades. The broader market also dropped on the news, with the Standard & Poor's 500-stock index falling nearly 2.5%. Citi's board called an emergency meeting for the following weekend, and CEO Prince stepped down three days later, on Nov. 4. Citi's weak capital position makes it particularly vulnerable, according to Whitney. She says Citi has no choice but to boost its capital ratio through divestitures and a smaller dividend. "They don't have enough capital, pure and simple. They will have to address that, ASAP," Whitney said in a November interview (BusinessWeek.com, 11/1/07). She says Citi will have to sell higher-quality assets such as real estate and credit cards because no market for weaker assets currently exists. Those sales, she predicts, will depress earnings for years to come.

Citi declined to comment on Whitney's analysis. It maintains, however, that it can rebuild its capital ratio by the middle of 2008 without a dividend cut or massive asset sales. The company may be on the verge of a massive job cut, though. CNBC reported Nov. 26 that Citi could cut as many as 45,000 of its 327,000 jobs. Citi confirmed that it was looking at ways to become more efficient, but issued a statement saying any specific reported number was "not factual." ....It remains to be seen whether her predictions about Citi's dividend and capital structure will be vindicated. But so far, in the words of one senior investment banker, "the market is betting on her being right."das war am 26.11.2007

ADIA is investing up to $7.5 billion equity units, which will be mandatorily convertible into common stock between Mar. 15, 2010 and Sept. 15, 2012. ADIA could thus gain as much as 4.9% of Citi, surpassing the 3.6% stake held by Saudi Prince Al Waleed bin Talal, currently Citi's largest shareholder.

The new money will help bolster Citi, whose balance sheet was becoming overstretched thanks to a deteriorating business environment and subprime-related writedowns. But just the fact that the bank needed to go to the Gulf with its hand out should be worrying to investors. The capital injection "shores up [Citi's] capital base and reduces investment risk," according to a market note by Morgan Stanley analyst Betsy Graseck. However she notes that the terms of the investment "leave the door open for more incremental hybrid issuance, suggesting that Citi considers this possibility high enough to include in its negotiations with ADIA. More hybrid capital is more earnings dilution." http://www.businessweek.com/

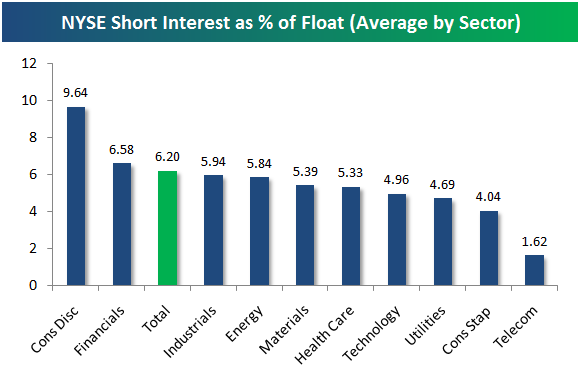

Based on the most recent NYSE short interest data released mid-month, NYSE listed Consumer Discretionary stocks have the highest average short interest as a % of equity float. Financials rank second at 6.58%, while Telecom, Consumer Staples and Utilities have the lowest short interest as a % of float. Look for high short interest sectors to do well on market rallies and poorly on market declines. Click here to view a list of sector ETFs among others.

November 26, 2007 at 02:17 PM in Market Analysis | Permalink | Comments (0) | T

Optionen

| Boardmail an "Platschquatsch" |

Wertpapier: S&P 500 |

Angehängte Grafik:

nyseshortinterest.png (verkleinert auf 87%)

nyseshortinterest.png (verkleinert auf 87%)

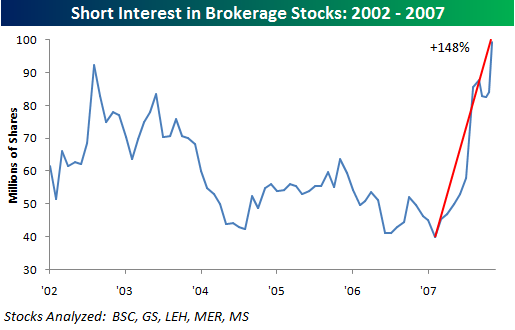

As of the most recent mid-month NYSE data, short interest in the brokerage group has shown a 148% increase since its lows in February. At current levels, combined short interest in Bear Stearns (BSC), Goldman Sachs (GS), Lehman (LEH), Merrill Lynch (MER), and Morgan Stanley (MS) is currently at its highest levels in over five years.

November 26, 2007 at 09:59 AM in Market Analysis | Permalink | Comments (0) | T

Optionen

| Boardmail an "Platschquatsch" |

Wertpapier: S&P 500 |

Angehängte Grafik:

brokerage_group_short_interest.png (verkleinert auf 99%)

brokerage_group_short_interest.png (verkleinert auf 99%)

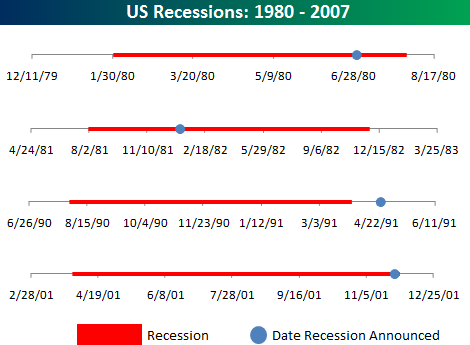

As debate over whether or not the US is on the verge of a recession, we would remind investors that waiting for the economists to tell us we are in one is probably not the best advice. The time-lines below highlight the four recessions in the US economy since 1980 (red line). In each chart we also show the date (blue dot) when the National Bureau of Economic Research (NBER) declared that the US economy was actually in a recession. While the NBER was pretty timely in its recognition of the recession that began in Summer 1981, they were late to the game in the remaining three. In fact, during the last two recessions, the NBER did not officially declare the start to a recession until the recession had already ended.

November 27, 2007 at 07:46 AM in Economy | Permalink

Optionen

| Boardmail an "Platschquatsch" |

Wertpapier: S&P 500 |

Angehängte Grafik:

recessions19802007.png

recessions19802007.png

,.... does 11 per cent represent a “slight premium” to a seven per cent yield on Citi stock? That’s actually a premium of 57 per cent. Even after the spurious tax argument, it is difficult to see how this funding can be costing much less than 9 per cent.

Oh dear. Oh dearie dearie me. Gentlemen, there was a clue in the first quote: ".... although a particular bond's structure could affect the interest rate paid". You bet it can. Let's take a look at the key features of the deal term sheet:

* Size: $7.5bn

* Type: Mandatory convertible (DECS is the Citi brand for these ubiquitous instruments, otherwise known as reverse convertibles)

* Payment rate: 11%, quarterly

* Term: Approx 4 years

* Settlement amount: (a) 235m Citi shares if stock below 31.83

(b) 201.39m shares if stock above 37.24

(c) straight line interpolation between these numbers.

The 235m shares @ 31.83 is, indeed, equivalent to a $7.5bn equity financing. But ADIA has effectively sold a call option as well. It doesn't participate (much) in the rise from the low strike to the high strike. Perhaps, just perhaps, the value of this call option is equal to the 4 year additional yield premium on the DECS.

Let's break down the deal into alternative components which have an identical cashflow profile (assuming pricing the day the deal was struck at 31.83):

* ADIA pays $7.5bn for 235m shares of Citi stock at 31.83, at, say, 7% yield

* ADIA sells 235m (ish) calls Citi stock strike 31.83 expiry 2010-11 (staged)

* ADIA receives 201m calls on Citi stock strike 37.24 expiry 2010-11 (staged)

* ADIA receives 4% pa dividend enhancement for 2.5-3.75 years (staged)

The dividend enhancement is probably worth 12% of the deal amount of $7.5bn. With sensible assumptions, the value of the call options sold back to Citi is around 8%, so the cost to Citi is around 4% or about 1.5% pa over the weighted average life of the deal. Put another way, Citi has raised tax deductible, upper tier capital funds for 4 years at a cost equivalent to another financing source of Libor+150. Smart business.

Citigroup's advance helped stocks rebound from losses yesterday that brought the decline from October to 10 percent, the first so-called ``correction'' in four years.

American house prices have suffered their worst plunge for two decades as defaults on sub-prime mortgages shatter homebuyers' confidence and battered lenders withdraw cheap financing dealsAccording to the key Standard & Poor's housing index, third-quarter US prices were down 4.5% on 2006 and were 1.7% lower than the second quarter of this year - the sharpest drop in the study's 21-year history.

The figures, which were released on the same day as research revealing a collapse in consumer confidence, showed that a once patchy economic downturn has become a nationwide phenomenon. The investment bank Goldman Sachs today warned that the chances of a recession had risen to between 40% and 45%.

S&P found a drop in house prices in all 20 of the cities in its study between August and September with Miami, Detroit and San Diego leading the downward march.

David Blitzer, chairman of the index committee, described the outlook as "pretty much resoundingly negative".

"If you look at a chart of housing statistics and recessions, they coincide," he said. "Based on housing, the odds of a recession are over 50%."

Hundreds of thousands of Americans have found themselves unable to keep up repayments on controversial sub-prime mortgages sold at the peak of the housing boom. Many had two-year "teaser" repayment rates which are expiring just as the property decline bites.

The squeeze is increasingly damaging the mood on American high streets. The New York-based Conference Board's measure of consumer confidence fell to its lowest level this month since the aftermath of Hurricane Katrina in 2005. The board said its confidence scale has dropped from 95.2 to 87.3 since October.

Lynne Franco, director of the board's consumer research centre, said: "Consumers' apprehension about the short-term outlook is being fuelled by volatility in the financial markets, rising prices at the pump and the likelihood of larger home heating bills this winter."

In spite of the gloom, Wall Street enjoyed a bounce today sparked, in part, by the Abu Dhabi government's decision to pump $7.5bn (£3.62bn) into struggling Citigroup. By midday in New York, the Dow Jones Industrial Average was up 173 points to 12,917.

America's traditional manufacturing heartland is feeling the economic pinch particularly badly as it juggles home repossessions with a long-term decline in the automotive industry.

In the Ohio city of Cleveland this week, more than 6,000 people applied for 300 jobs at a new branch of the discount retailer Wal-Mart.

Amy Hanauer, director of Policy Matters Ohio, told Cleveland's Plain Dealer newspaper that the queue was "deeply troubling", adding: "That's Depression-era kind of imagery."

The mortgage-induced downturn could result in 524,000 fewer jobs being created next year and a loss of economic outlook of $166bn in 361 American cities according to the US Conference of Mayors, which is meeting in economically depressed Detroit this week.

It put the cost of the housing downturn at $10bn in New York, $8.3bn in Los Angeles and $4bn in both Dallas and Washington.

"The foreclosure crisis has the potential to break the back of our economy, as well as the backs of millions of American families, if we don't do something soon," said Douglas Palmer, the mayor of Trenton, New Jersey, who chaired the national gathering.

In a downward revision of its growth forecast, Goldman Sachs said it expected the Federal Reserve to cut interest rates to 3% over the next six to nine months, down from its previous estimate of 4%. It predicted that unemployment would rise from 4.7% to 5.5% by the end of next year.

Ken Goldstein, an economist at the Conference Board, said all eyes were on the employment market, which could be the next sector to suffer a knock-on impact from the downturn.

"If the labour market starts to weaken, as consumers now believe it might, then the post-holiday season is going to be really bleak," he said. "The worry here is not about the shoe that's already hit the floor - the worry is about the next shoe to hit the floor."