Der USA Bären-Thread

Seite 379 von 6257 Neuester Beitrag: 03.02.25 16:52 | ||||

| Eröffnet am: | 20.02.07 18:46 | von: Anti Lemmin. | Anzahl Beiträge: | 157.407 |

| Neuester Beitrag: | 03.02.25 16:52 | von: Katzenpirat | Leser gesamt: | 24.168.837 |

| Forum: | Börse | Leser heute: | 8.770 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 377 | 378 | | 380 | 381 | ... 6257 > | ||||

Die Lage ähnelt der eines Kleinaktionärs, der mit GPC 90 % Verluste eingefahren hat, Margin-Calls erhält und nun lieber seine Novartis-Aktien "mit kleinem Verlust" verkauft, statt beim wirklichen Schrott die Reißleine zu ziehen. Ganz Dumme kaufen dann noch mit dem Geld aus dem Novartisverkauf GPC-Aktien nach, weil die ja "das größte Erholungspotential haben".

Angehängte Grafik:

screen_00244.jpg (verkleinert auf 96%)

screen_00244.jpg (verkleinert auf 96%)

Cisco-Vorstandschef John Chambers sagte bei der Vorstellung der Quartalszahlen in der Nacht zu Donnerstag, es gebe "dramatische Rückgänge" bei den Aufträgen insbesondere von US-Finanzdienstleistern......Die Aussagen des Cisco-Chefs sind einer der bislang klarsten Belege dafür, dass die aktuelle Kreditkrise auch Teile der US-Wirtschaft belastet, die nicht in der Finanz- und Baubranche angesiedelt sind. Cisco gilt als Gradmesser für die Verfassung des gesamten Technologiesektors.

Topmanager aus klassischen Branchen äußern sich zunehmend skeptisch: "Unsere Kunden spüren ganz klar Gegenwind beim verfügbaren Einkommen", sagte am Donnerstag der Chef des US-Einzelhändlers JC Penney, Myron Ullman, bei der Vorlage seiner Quartalszahlen.

http://www.ftd.de/technik/it_telekommunikation/...dustrie/276864.html

Cisco-Vorstandschef John Chambers sagte bei der Vorstellung der Quartalszahlen in der Nacht zu Donnerstag, es gebe "dramatische Rückgänge" bei den Aufträgen insbesondere von US-Finanzdienstleistern......Die Aussagen des Cisco-Chefs sind einer der bislang klarsten Belege dafür, dass die aktuelle Kreditkrise auch Teile der US-Wirtschaft belastet, die nicht in der Finanz- und Baubranche angesiedelt sind. Cisco gilt als Gradmesser für die Verfassung des gesamten Technologiesektors.

Topmanager aus klassischen Branchen äußern sich zunehmend skeptisch: "Unsere Kunden spüren ganz klar Gegenwind beim verfügbaren Einkommen", sagte am Donnerstag der Chef des US-Einzelhändlers JC Penney, Myron Ullman, bei der Vorlage seiner Quartalszahlen.

http://www.ftd.de/technik/it_telekommunikation/...dustrie/276864.html

Fakt bleibt: Die USA können sich einen weiteren Dollarabsturz nicht leisten. Denn wenn Ausländer anfangen, ihr Kapital aus USA abzuziehen, weil sie weitere deutliche Dollarverluste befürchten, bricht die auf ständigen ZUSTROM ausländischen Kapitals angewiesene US-Wirtschaft völlig in sich zusammen. USA hängt am Tropf ausländischen Geldes wie ein Junkie an der Nadel. Die Rettung des Dollars vor dem Absturz ist daher für Bernanke und Co. zurzeit die Prämisse Nr. 1. Die EZB wird gegen ein Erstarken des Dollars auch nichts einzuwänden haben.

Einfacher ausgedrückt: Was nützt es den USA, wenn die Banken und Broker alle überleben, ihnen dafür aber das ausländische Spielgeld ausgeht?

:o))

ich habe fast die Befuerchtung, wenn er wieder so einen Schreianfall bekommt, wie damals auf CNBC wird Bernanke auch wieder entsprechend handeln.

Aber im Ernst, bei der Fed werden zur Zeit sicherlich allerlei Varianten durchgespielt; gluecklicherweise laesst man die Hazardeure aber erst mal richtig bluten (nicht so wie die BoE, die erst gross das Maul aufreisst und dann NR mit 2-stelligen Mrd-Spritzen ausloest). Aber allzu lange wird Bernanke nicht warten, meiner Meinung nach wird auch er keine der grossen amerikanischen Banken bankrott gehen lassen; und da alle Banken momentan mehr oder weniger in der Klemme sitzen, bleibt nur die Fed als Wight Night (oder die Chinesen oder Russen oder Saudis).

Optionen

| Boardmail an "obgicou" |

Wertpapier: S&P 500 |

Jeder vernünftig denkende Mensch weiß, dass eine Korrektur der Exzesse bitter nötig ist. Mit Zinssenkungen würde der Proess nur aufgeschoben - mit dem Risiko des Dollarabsturzes und der Abwendung ausländischer Gläubiger vom US-Kapitalmarkt.

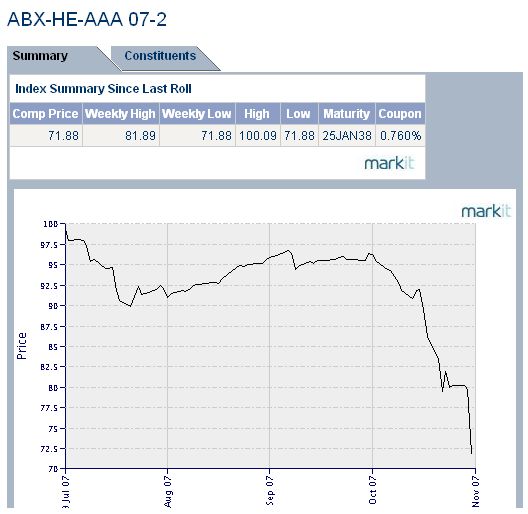

Man muss dabei bedenken, dass der Aktienmarkt nur einen Bruchteil des Kapitals gebunden hat wie der Bond-Markt. Dort ist schätzungsweise fünfmal so viel Geld investiert wie im Aktienmarkt. Auch US-Staatsanleihen zählen zu diesem Bond-Markt. Im Gegensatz zu AAA-Schrott aus dem ABX-Index stehen die ebenfalls mit AAA gerateten US-Staatsanleihen noch bei nahezu 100 %, dort gibt es kaum Risikoabschläge.

Eine Dollarabwertung würde die Scheichs und Asiaten, die ihr Geld in US-Staatsanleihen anlegen, daher viel härter treffen als eine stärkerer Aktienmarkt-Rückgang. Denn den abstürzenden Dollar bekämen Bondanleger hautnah zu spüren (bei Umrechnung des Kurses in ihre Heimatwährung), während ein Aktienmarktabsturz den Bond-Markt (und den Dollar) sogar kräftigt.

Wenn die Wahl besteht, den Dollar oder den Aktienmarkt abschmieren zu lassen, besteht für die Fed und die USA keine echte Wahl. Der Dollar ist das Schmiermittel, das den "Betrieb" dort am laufen hält. Bleiben die Petro- und Asiatendollars aus (negative TIC-Zahlen), kann sich Amerika die Kugel geben.

Wer die Bernanke-Rede (Auszüge in meinem Posting oben) liest, hört die Nachtigall auch in diese Richtung trappsen. Offenbar hat die Fed mit einem derartig starken Euro und so starkem Öl nach den letzten Zinssenkungen nicht gerechnet...

Angehängte Grafik:

screen_00247.jpg (verkleinert auf 64%)

screen_00247.jpg (verkleinert auf 64%)

Angehängte Grafik:

screen_00249.jpg (verkleinert auf 68%)

screen_00249.jpg (verkleinert auf 68%)

Japans Wirtschaft droht schwerer Rückschlag

von Martin Kölling (Tokio) und Ulrike Heike Müller (Berlin)

Japans Wirtschaft stehen trübe Zeiten bevor. Schwächere Daten der Industrie sowie eine hausgemachte Baukrise drohen nach Aussage von Volkswirten den Aufschwung abzuwürgen.

Zudem steigen die Risiken, dass die Finanzkrise und die schwächelnde US-Wirtschaft das Wachstum bremsen. Die Wahrscheinlichkeit einer Rezession sei innerhalb eines Monats um fünf Prozentpunkte auf rund 40 Prozent geklettert, sagte Tetsufumi Yamakawa, Japan-Chefvolkswirt bei Goldman Sachs.

Die Eintrübung dürfte es der Notenbank erschweren, ihre Zinspolitik zu normalisieren. Um die Deflation zu bekämpfen, hatte sie den Leitzins jahrelang nahe null gehalten. Derzeit liegt er bei 0,5 Prozent.

Viele Ökonomen senkten ihre Vorhersagen bereits zum zweiten Mal in nur vier Wochen. "Die Revision unserer Prognose vor einem Monat für das Haushaltsjahr 2007 von 2,5 auf 1,9 Prozent reicht nicht, eine weitere Senkung auf 1,2 Prozent ist notwendig", sagte Richard Jerram, Volkswirt von Macquarie Japan. Hiromichi Shirakawa von Credit Suisse senkte die Prognose um 0,4 Prozentpunkte auf 1,3 Prozent. Das Haushaltsjahr endet am 31. März.

Erst am Donnerstag hatten neue Daten die Konjunktursorgen verstärkt. Die Auftragseingänge im Maschinenbau brachen im September um 7,6 Prozent zum Vormonat ein. Dabei sind die schwankenden Aufträge vom Schiffbau und der Energieversorger nicht berücksichtigt. Bereits im August lag das Minus bei 7,7 Prozent. "Die Aufträge werden wohl auch im vierten Quartal zurückgehen, da die erwartete Abkühlung der US-Wirtschaft die japanischen Autobauer und den Technologiesektor treffen wird", sagte Caroline Newhouse-Cohen von BNP Paribas.

Schwerer wiegt der Rückgang des Frühindikators für die künftige Wirtschaftsentwicklung. Er fiel im September das erste Mal seit zehn Jahren auf null Punkte. Damit lag er weit unter der Wachstumsschwelle von 50 Punkten. Der Sammelindex fasst zwölf verschiedene Indikatoren von Lagerbeständen bis zum Konsumentenvertrauen zusammen.

Die Wirtschaft belastet zudem der Absturz der Bauindustrie. Die Regierung hatte nach einem Skandal um gefälschte Gutachten zur Erdbebensicherheit von Neubauten die Genehmigungsverfahren deutlich verschärft. Daraufhin brach die Bauwirtschaft im dritten Quartal um 37 Prozent zum Vorjahr ein, so stark wie seit Beginn der Baustatistik im Jahr 1964 nicht.

Zwar macht der Hausbau nur 3,4 Prozent des Bruttoinlandsprodukts aus. Aber zusammen mit dem erwarteten Umsatzrückgang der Elektronikkonzerne, die weniger Fernseher und Haushaltsgeräte verkaufen, werde die Krise tiefer, sagte Takehiro Sato von Morgan Stanley: "Der Hausbauschock wird die kurzfristigen Wachstumsaussichten deutlich trüben."

Baukrise kommt sehr ungelegen

Dabei kommt die Baukrise denkbar ungelegen, denn auch andere Indikatoren weisen schon länger nach unten. So ist die Erholung des privaten Verbrauchs durch die Eintrübung des Konsumentenvertrauens gefährdet. Obwohl Volkswirte den Arbeitsmarkt weiter als robust bezeichnen, könnte die psychologische Wirkung negativer Schlagzeilen den Konsum bremsen. Denn die Japaner finanzieren ihren Konsum nach einer Analyse der Credit Suisse vor allem aus Ersparnissen. Nach ihrer Beobachtung haben die Haushalte ihre Rücklagen inzwischen erheblich aufgebraucht. Die Volkswirte senkten daher ihre Prognose für den Konsum im vierten Quartal.

Zudem droht Japans wichtigste Wachstumsstütze, der Export, wegen der Hypothekenkrise in den USA Schwung zu verlieren. Bisher konnte sich das Land noch recht gut vor Turbulenzen schützen. Eine größere Nachfrage aus Asien und Europa federte schwächere Exporte in die USA ab. Die Abhängigkeit vom US-Markt hat dadurch in den vergangenen Jahren abgenommen.

Noch hält Notenbankchef Toshihiko Fukui unbeeindruckt von den jüngsten Entwicklungen an seiner Zinserhöhungsrhetorik fest. Am Dienstag entscheidet die Bank of Japan (BoJ) erneut über das Niveau der Leitzinsen. Er wisse zwar, dass die Gefahren für Japans Wirtschaft steigen, sagte Fukui. "Aber wir müssen den Risiken einer anhaltend lockeren Geldpolitik mehr Aufmerksamkeit schenken." Die Wirtschaft sei noch immer dynamisch und könne Schwankungen auf den Märkten bewältigen. Experten rechnen allerdings damit, dass die BoJ erst im nächsten Jahr die Zinsen anheben wird, wenn das Wachstum tatsächlich wieder anziehen so.... (gekürzt).

Kass: This Bear Sees a Year-End Rally

By Doug Kass

Street.com Contributor

11/8/2007 8:56 AM EST

...

This is a tough call for me to make because I believe the world's economy and capital markets face significant challenges. But, increasingly, many of those concerns have been recognized, and some of my shorts have reached my targeted price objectives. [Schon merkwürdig, da Kass seit SP-500 = 1350 short ist, wie kann da bei 1480 "das Ziel erreicht" sein? - A.L.] That said, in a roller coaster market that has no memory from day to day, successfully gaming 5% moves (or so) becomes a necessary ingredient to creating alpha (excess returns). This will be particularly true in the generally low-return setting for equities that I envision over the next year or two.

In summary, the ingredients for a market rally are now falling into place. Whether it occurs today, tomorrow or in the next few weeks, I think it is coming, albeit at far lower levels than Barton Biggs had predicted recently on CNBC's "Fast Money."

I would note that while the anticipated recovery in share prices (amidst this week's gloomy headlines) could be far more brisk than the growing ursine crowd expects, the economy and financial system face broad challenges that will likely limit the rally in scope and duration. A relatively choppy and uncertain picture should unfold after the anticipated year-end rally.

A short-term rally could now occur for some of the following reasons.

Economic: Even the most optimistic bulls now acknowledge the likelihood of a consumer-led slowdown and the likelihood that housing will not recover for several more years, two themes I have emphasized over the last year. It will now come as no surprise to most, and it might be partially discounted.

Subprime Storm: The credit event, until recently (like housing's depression), has been ignored by the steadfastly bullish crowd. No more. Media coverage and investors' preoccupation of this issue is now elevated.

I am looking for a sign of relief on the part of investors after Goldman Sachs (GS), Merrill Lynch (MER) and Morgan Stanley (MS) have quantified their fourth-quarter credit writedowns and their exposure. Frankly, the exposure levels are less than I anticipated.

In the badly beaten down financials -- where I see the reverse of momentum compared to anointed ones Apple (AAPL), Research In Motion (RIMM), Google (GOOG), Baidu (BIDU), etc. -- some have actually done a relatively reasonable job in managing and taking down that exposure, though few have been unscathed.

Importantly, the Administration finally appears to get the severity of the subprime crisis, and the odds of an organized (and sensible) government response (in the form of a fiscal Marshall Plan to save homeowners) will be roundly appreciated by the markets.

Sentiment: I judge sentiment more on what I see hedge funds doing (admittedly a thin-reed indicator), through my personal contacts, rather than sentiment polls of writers or individual investors. And over the last week, there is little question in my mind that shorting/hedging is dramatically on the rise. Some of those shorts are being executed in stocks/sectors that have experienced dramatic near-term drops, potentially setting the stage for a violent rally from oversold levels.

Stated simply, there appears to be too much piling on based on obviously disappointing headlines (that many of us anticipated).

My experience, however, has been that when the headlines are this bad, and with sentiment from my cabal at nearly the polar opposite than when stocks hit their highs two months ago, the market typically has done a pretty good job of discounting. (Supportive of my anecdotal observations on rising skepticism is the latest ISI Hedge Fund Survey, which indicates hedge fund long exposure is now at the lowest level since 2004.)

Takeover Activity: While private-equity firms have been quiescent (for obvious reasons), I expect to see a flurry of opportunistic corporate takeovers (perhaps even some high profile ones!) aimed at attempting to take advantage of the recent market drubbing.

Year-End Seasonality: The latter part of the year is usually seasonally strong. According to Stock Traders Almanac, since 1950, the DJIA and S&P 500 have averaged a 1.7% gain. The Dow has been up in 40 years and down in only 16 years while the S&P has risen in 42 years and dropped in only 14 years. The gain in the Nasdaq and Russell 2000 are even better, averaging 2.0% increases since 1971 and 2.6% gains since 1979. These are historically powerful seasonal tailwinds that might even be exaggerated in 2007 as hedge funds, thirsty for performance, go all in.

Political: Surprisingly, the Republicans are beginning to catch up to the Democrats in the 2008 Presidential polls. This could be an underappreciated and constructive (at least for stocks) factor. As reported by RealClearPolitics, Rudy Giuliani (the likely Republican candidate) is actually now ahead in two of the 11 national head-to-head polls; in the others, Hillary Clinton is holding on to a diminishing lead.

This is shocking to me, quite frankly, as I anticipated another Democratic tsunami. A further shrinkage in the Democratic lead will be viewed as a positive, as the trend toward trade protectionism and higher corporate and individual taxes may be less clear than I previously thought.

In conclusion, I stressed flexibility this week, and my intention is to practice what I preach and to avoid the dogma that some too often attribute to my market views. Nevertheless, I should emphasize that I am hardly a long-term bull. That couldn't be further from my view.

"Importantly, the Administration finally appears to get the severity of the subprime crisis, and the odds of an organized (and sensible) government response (in the form of a fiscal Marshall Plan to save homeowners) will be roundly appreciated by the markets.">/I> [aus # 6463]

... dann wird es bei den runtergeprügelten Financials in der Tat einen Mega-Shortsqueeze geben, der für eine Jahresend-Rallye gut sein könnte. Dadurch ändert sich freilich an den Kreditproblemen nichts, so dass langfristig kaum mehr als Aufschub erreicht werden kann.

Einzige Frage, die ich mir stelle: vorher ein deflationärer Schock (sieht so aus!) oder eher ein geordnter "salamicrash"........?

Optionen

| Boardmail an "biomuell" |

Wertpapier: S&P 500 |

Angehängte Grafik:

zb1007.jpg (verkleinert auf 86%)

zb1007.jpg (verkleinert auf 86%)

Leichen im Hypothekenkeller

Weitere Abschreibungen

Die Abschreibungen auf besicherte Schuldverschreibungen (CDO) dürften im Zuge der US-Hypothekenkrise nach Einschätzung von Analysten der Citigroup auf ungefähr 64 Milliarden Dollar steigen. "Von den vielen Leichen im Keller der Hypothekenkrise sind die Abschreibungen auf die CDOs wahrscheinlich die schrecklichsten", hieß es in der Mitteilung der Analysten unter Führung von Matt King mit Datum 6. November. Zwar seien die Verluste hoch, sie seien jedoch nicht so unkontrollierbar, wie spekuliert werde.

Allein im dritten Quartal schrieben die drei größten US-Banken zusammen ungefähr 25 Milliarden Dollar ab. Merrill Lynch vermeldete deswegen einen Verlust von 2,3 Milliarden Dollar im Quartal. Die fraglichen Schuldverschreibungen sind häufig mit zweitklassigen Hypothekenkrediten hinterlegt, die von den Schuldnern angesichts zuletzt gestiegener Zinsen und fallender Häuserpreise zunehmend nicht mehr bedient werden können.

Negatives von Mizuho

Das japanische Aktienhandelshaus Mizuho Securities steht einem Zeitungsbericht zufolge möglicherweise wegen der US-Hypothekenkrise vor einer Abschreibung von bis zu 100 Milliarden Yen (gut 600 Millionen Euro). Dies könnte die geplante Fusion mit Shinko Securities um mehrere Monate verzögern, berichtete die Zeitung "Nikkei" am Freitag. Die Muttergesellschaft Mizuho Financial wies den Bericht zurück. Er basiere auf Spekulationen, hieß es.

Die Fusion von Mizuho und Shinko zum drittgrößten Unternehmen der Branche in Japan steht im Januar an; sie könnte dem Bericht nach auf Juni oder später verschoben werden. Bisher sei dazu jedoch keine Entscheidung gefallen, teilten beide Fusionspartner mit.

__________________________________________________

auf unserem Planeten gibt es nur Propheten

Optionen

| Boardmail an "biomuell" |

Wertpapier: S&P 500 |

#9464 ist nicht unrealistisch ("Marshall-Hypotheken-Plan") und der "Aufschub" könnte dann mindestens ein Jahr sein.

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

Meredith Whitney, the CIBC World Markets' analyst whose comments last week on Citigroup's balance sheet sparked a $369bn (£177bn) fall in world markets, has led calls for a carve-up. She said: "That's really the only thing they can do. They don't have the capital to manage it as an ongoing entity."

Those views echoed similar calls from Credit Suisse analysts Susan Roth Katzke and Ross Seiden who said a pick-up in Citigroup's share price would only come through a "break-up into several separate, more manageable or saleable businesses". They later suggested Citigroup's interim management should search for "new CEOs atop several more manageable entities".Citigroup chairman Robert Rubin and interim chief executive Sir Win Bischoff have so far resisted break-up calls.

On taking charge of the bank, which has a market value of more than $170bn, Sir Win said: "I see my role to hand over a vibrant firm which has learnt from its mistakes and is ready once again to take advantage of its considerable assets and heritage. I believe in the strategy."

Analysts predict a long queue of potential buyers interested in taking control of Smith Barney, Citigroup's brokerage unit.

Robert Ellis, an analyst with Celent, a Boston-based research and consulting firm, said: "Potential buyers include some of the largest eurozone banks who would be getting a significant discount with the current dollar-euro exchange rate. Other parties that might be interested include HSBC, plus some of the larger UK and Canadian banks that would like a greater share of the US wealth management business."

Mr Ellis said brokerages typically sell for about twice annual revenues which would give it a value above $20bn, according to this year's figures. "The valuations of the big brokerages peak in line with the equity markets and you tend to get seven-year cycles. Either Citigroup gets on with this or they could be waiting for a long time."

Another analyst said JP Morgan would likely be in the running for the brokerage as well as Citigroup's international banking network. "JP Morgan would have zero interest in the investment bank and regulatory problems with some of the US retail operations, but the brokerage would definitely interest them."

The analyst said Morgan Stanley would be interested in the US retail bank, while Wachovia could consider a bid for the investment banking operations.

http://www.telegraph.co.uk/money/main.jhtml?xml=/...ILC-mostviewedbox

Take a glance at these two dollar charts.The Greenback has slumped to 91 cents against the Canadian Loonie, the lowest since Canada’s currency was floated in 1950.

It has fallen for three years against the Brazilian real, the Mexican peso, the Russian ruble, et al – the first time it has ever lost ground in this fashion against a mix of emerging market currencies. And, of course, the euro has risen 70pc in six years to $1.47.

http://blogs.telegraph.co.uk/business/...tchard/nov07/witchesbrew.htm

Why is the dollar crumbling? Is it just because the Federal Reserve has begun to cut interest rates, while other central banks are still tightening?

Or have we reached the moment when the United States is downgraded as an economic, political, and military power by the rest of the world - permanently - reflecting its new status as a super-debtor with $3 trillion in external liabilities?

What we know is that Asian and Mid-East central banks are cutting their holdings of US Treasuries at a brisk clip. Qatar has cut the dollar share of its $50bn sovereign wealth fund from 98pc to 40pc.The effect was disguised as long as the credit bubble continued to lure huge sums of foreign “hot money” into America’s $2.2 trillion commercial paper market. But this market is half-frozen. Loans have contracted by $300bn in twelve weeks. The risk this winter is that a hot money exodus will follow the glacial exodus of Chinese, Japanese, Taiwanese, Korean, Saudi, Emirati, and Norwegian cold money – if it has not begun already.

Nor is that the only risk. Stephen Jen, chief currency strategist at Morgan Stanley, says we may face a full-fledged crisis in short order if hedge funds armed with leverage come off the sidelines and begin to pummel the dollar as well.And then there is the yen “carry trade”, that $1,200bn flow of Japanese money (often borrowed at near-zero rates in Tokyo) that has juiced global asset markets through the boom.

"The most dangerous threat is that the yen will snap back and destroy the carry trade," he said. This is exactly what happened in 1998, setting off a chain of falling dominoes.

While we are talking about Morgan Stanley, let me quote the latest thoughts of their credit strategist Gregory Peters – which were e-mailed to me today:

“Systemic risk is very high. I am as negative as I have been in years, given the deep structural issues plaguing the credit markets – which will in turn hurt the US consumer and the US economy. The Federal Reserve cutting rates does little to solve these deep structural issues......As for the inflation part of our witches' brew, a note today from Capital Economics warned that headline CPI inflation in the US is likely to reach 4.5pc in November, and could reach 5pc by the end of the year – largely due to the effects of oil doubling this year.

The futures markets seem to be disregarding this......The Fed is caught between the Scylla of screaming CPI inflation and the Charybdis of a housing crash. Call this stagflation, if you want.....Nor will there be much help from the rest of the world on the inflation front. The disinflation era of the 1990s is no longer on offer. The cost of Chinese manufacturing is shooting up.

Here is a sampling of global inflation rates.

Eurozone 2.6pc, (highest since the launch of the euro).

China 6.2pc

Russia 9pc

Vietnam 14pc

United Arab Emirates 9.3pc

Saudi Arabia 4.9pc

Latvia 13pc

Romania 6pc

Chile 6.5pc

Kazakhstan 8.6pc

Most of these levels are the highest in a decade, whether caused by commodity booms, dollar pegs or euro pegs, or a mix.

We are reaching the point when governments across the world will have to do something before inflation spirals out of control.

Angehängte Grafik:

_.jpg

_.jpg

Published: November 9 2007 02:12 | Last updated: November 9 2007 02:12

http://www.ft.com/cms/s/0/...dc-8591-0000779fd2ac.html?nclick_check=1

The funding problems hurting structured investment vehicles are so acute that most managers now do not expect the industry to survive the current crisis, according to Moody’s, the ratings agency.The inability of most vehicles to raise short-term debt since the summer is putting even the largest, oldest and most diversified of these vehicles under tremendous strain.It led Moody’s late on Wednesday to put the capital notes of a flood of SIVs on review for possible downgrade. These programmes are designed to profit from the difference between short-term borrowing rates and longer-term returns from structured product investments. The funding crisis meant there was a growing threat that even seemingly healthy vehicles would have to increasingly sell assets at a loss, the agency said.

.....

Moody’s on Wednesday also downgraded the capital note ratings on a number of weaker SIVs that had been on review, including those for two SIVs run by WestLB, the German bank, and one run by Ceres Capital, a specialist New York-based manager.

Capital notes are long-term junior securities issued by SIVs which pay the highest return but absorb the first losses. However, the decision by the agency to put on review the ratings of capital notes issued by some of the biggest bank-run SIVs is even more significant. These include three run by Citigroup, the largest player in the sector, two run by HSBC and one by MBIA, the US bond insurer.Also on review are notes from SIVs run by HSH Nordbank, Standard Chartered, Rabobank, SocGen, Bank of Montreal and Banque AIG.

.....

Moody’s said that most of the banks affected had sufficient breathing space to support their SIVs if necessary, although some would probably avoid doing so in order to preserve their capital bases. Citigroup’s own financial strength remains on review at Moody’s and the effect of the rating actions on its SIVs would have to be taken into consideration as part of that review.Citi itself, which is reeling from a jump in subprime related losses, has said it will not do anything that could lead to its SIVs being consolidated onto its balance sheet.

However, the problem that dogs the ratings agencies is that if they downgrade the monolines, this could spark a much wider chain reaction. For the business model of the monolines does not work unless they have a AAA rating (or equivalent.) Or as a non-executive director of one monoline says: “The credit rating agencies are like our regulators – they have the power of life and death over us.”

Moreover, a downgrade of the monolines would mean that all the bonds they have guaranteed would be downgraded too. And that does not just affect subprime securities, but swathes of the municipal bond market as well – which in turn could hurt mainstream US investors (such as pension funds), and borrowers (such as schools or hospitals).

This is the stuff of Washington nightmares. But the US Treasury cannot afford to be seen to be pleading with the rating agencies to go softly on these monolines right now. After all, in recent months these very same agencies have been roundly criticised for having been too lax – by American politicians, among others. Thus, in a sense, the agencies are now damned whatever they do: if they tip the muni market over the edge, they could become a political whipping boy; but if they fail to act, they will face more criticism for being too lax.

.....Is there any solution to this tangled mess? Fitch, for its part, is bravely trying to forge one: it indicated earlier this week that it will give the monolines a period of time in which they can raise fresh capital to avoid downgrades, if its review shows that they do not have enough capital to warrant a top-notch rating.But it remains unclear if this tactic will quell investor unease. .....

http://www.ft.com/cms/s/0/ffe67a8e-8e26-11dc-8591-0000779fd2ac.html