Der USA Bären-Thread

Seite 363 von 6257 Neuester Beitrag: 06.07.25 13:32 | ||||

| Eröffnet am: | 20.02.07 18:46 | von: Anti Lemmin. | Anzahl Beiträge: | 157.419 |

| Neuester Beitrag: | 06.07.25 13:32 | von: Frieda Friedl. | Leser gesamt: | 25.580.954 |

| Forum: | Börse | Leser heute: | 4.287 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 361 | 362 | | 364 | 365 | ... 6257 > | ||||

Freitag, 2. November 2007

Verkauf von Krisenanleihen

Merrill hübscht Bücher

Die US-Investmentbank Merrill Lynch will einem Zeitungsbericht zufolge weitere teure Risiken im Anleihegeschäft vorerst aus ihren Büchern bekommen. Das "Wall Street Journal" meldete am Freitag in seiner Onlinausgabe, das Institut verkaufe derzeit in größerem Stil mit Hypotheken besicherte Wertpapiere an Hedgefonds.

Die Fonds hätten erst nach Ablauf eines Jahres das Recht, die Schuldverschreibungen zu einem garantierten Mindestpreis wieder an Merrill zu veräußern. Dadurch könne die Bank drohende Abschreibungen auf die Papiere, die wegen der Krise massiv an Wert verloren haben und für die sich derzeit keine Käufer finden lassen, mindestens um rund zwölf Monate aufschieben. Das Blatt berief sich dabei auf mit der Angelegenheit vertraute Kreise. Die Bank war zunächst nicht für eine Stellungnahme zu erreichen.

Merrill ist im abgelaufenen Quartal in den Strudel der Marktturbulenzen geraten und schrieb erstmals seit sechs Jahren rote Zahlen. Hauptgrund waren milliardenschwere Abschreibungen vor allem auf Wertpapiere, die mit US-Hypotheken für Kunden mit schlechter Bonität abgesichert sind. Der Markt für diese Baufinanzierungen ist komplett zusammengebrochen.

Dem "Wall Street Journal" zufolge ist Merrill mittlerweile auch ins Visier der Börsenaufsicht SEC geraten. Sie prüfe, wie die Bank die Papiere bewertet und das Engagement offengelegt habe. Auch die Geschäfte mit den Hedgefonds dürften demnach von der SEC angeschaut werden.

__________________________________________________

auf unserem Planeten gibt es nur Propheten

- wow die Zahlen sind ja besser als erwartet--also Eur verkaufen!!!

- 5min später...grummel....ist doch sowieso alles gelogen...schnell wieder die $chen verkaufen und gleich noch ein paar zusätzliche Euro horten---somit Allzeithoch für Euro.

Peter Schiff: „To arrive at this rate, the government had to assume that inflation during the quarter ran at an annualized rate of 0.8%. That is the lowest rate of inflation used to calculate U.S. GDP since the Eisenhower administration. With oil priced at almost $100 per barrel, gold futures trading over $800 per ounce, the dollar hitting record lows, and the Fed printing money like it is going out of style, the government has the nerve to claim that current inflation is the lowest it has been in half a century. Unbelievable!“

http://www.321gold.com/editorials/schiff/schiff110107.html

b)Zu den Arbeitsmarktzahlen gibt es kritische Anmerkungen von George Ure

Now, just how much of it was created by the CES Birth-Death Model, which statistically supposes jobs created? Try 103,000 for October. A true skeptic would say 166 thousand new jobs, backing out 103 thousand CES Birth/Death Model estimated, leaves a real gain of 63-thousand, but any port in a storm, right? And the 'engineers flipping burgers' report, Table A-12, category U-6 stayed steady at 8.4%. Predictably.

And while the government is telling us on the one hand how good things are, I can help but notice that Chrysler is slicing one job in three, with another 12,000 about to get axed. I'm not expecting this to show up as a noticeable blip on the Mass Layoffs report, though. Statistical series which have been historically noisy have all quieted down. All coincidental, I'm sure.

http://urbansurvival.com/week.htm

__________________________________________________

auf unserem Planeten gibt es nur Propheten

wenn wissen willst warum - siehe mein öl peak thread

Optionen

| Boardmail an "biomuell" |

Wertpapier: S&P 500 |

Begründung:

Wie ich letzten Freitag vor meinem Urlaub schrieb war es wichtig die Reaktion des Marktes auf die Zinssenkung zu beobachten (-25 bp waren ja klar). Die Reaktion war klar negativ zu deuten: Kurze - bedeutungslose - Schwankungen nach der Senkung am Mittwoch, dann herber Abverkauf am Donnerstag. Und eben KEINE Rally über Tage wie nach den letzten Senkungen.

Über Gründe kann man spekulieren. Ich vermute mal, dass die Aussicht, die vorerst letzte Zinssenkung gesehen zu haben und das im Zusammenhang mit einem nachlassenden Wachstum sowie steigener Inflation, zu Gewinnmitnahmen führte. Und mit denen beginnt nun mal jede Baisse. Charttechnisch wird das erhoffte Dreifachtag a la Herbst 2000 immer wahrscheinlicher.

Der heutige Tag verlief bislang für die Bullen enttäuschend, es blieb nämlich der immer nach Kursstürzen übliche Dip-Buy aus. Insofern ist das noch interessanter für mich als die Kursbewegung gestern.

Fazit: Vorerst klar short. Sollte der Tag heute an Wall Street grün werden, aber wieder raus.

P.S. Ja, ich habe mich erholt ;-)

Der Dollar wird künstlich nach unten gedrückt. Warum?

Das Haushaltsdefizit wird durch die Entwertung des Dollars unterm Strich immer kleiner. Im Gegenzug werden die Vermögenswerte wie z.B. Dollar und Gold immer mehr Wert.

Wenn ich das mal buchhalterisch sehe....

Vermögensgegenstände nehmen zu

Verbindlichkeiten nehmen ab

Eigenkapital steigt!

Ja, jetzt kommt dann "Halt mal, die Verbindlichkeiten in Dollar bleiben doch gleich!

§

Dann rechnet das bitte mal in Euro und nicht in Dollar. Die Amis treiben da ein ganz lustiges Spiel und verarschen den Rest der Welt.

Ich möchte nur mal anmerken das das Bruttoinlandsprodukt pro Kopf bei denen höher liegt als bei uns in Europa.

Warum das ganze?

Ganz einfach. Die USA lassen sich von den Schlitzaugen nicht den Rang als Weltwirtschaft ablaufen. Die treiben dieses Spiel künstlich weiter bis bei den Chinesen die Rezession einsetzt, um dann ihren Boom zu vollziehen. Goldreserven abstossen, Haushaltsdefizit auf einen Schlag ausgleichen, Dollar explodieren lassen. Ade Europa, Ade China

Meinte natürlich Ölreserven und Gold

die Aktienkurse von Merryl Lync und Citigroup nähren dass diese Spekulationen einen handfesten hintergrund haben könnten.

crashen die US Banken crashen auch die US Börsen und der USD - Öl würde eher fallen (und das sage ich als "ÖL PEAKIST" - weil dann die erwartung an eine US Rezession die erwartung eines deutlichen Nachgebens der NAchfrage nach Öl zu erwarten wäre.

Gold würde in den "Himmel schiessen" (auch der unaufhörlich steigende Goldpreis deutet auf etwas kommendes bei den Banken hin... - oder doch nur getrieben vom Inflationsdruck und schwachen USD??)

mhhh ?

Optionen

| Boardmail an "biomuell" |

Wertpapier: S&P 500 |

$2 Million Per Household Means Doom For Dollar

by Daniel Amerman

Overview

What is the total cost of all United States retirement promises and expectations, and what are the implications for the dollar? In this article we are going find a startling answer to that question - approximately $2 million per able to pay household. To get there will involve taking five steps:

1) Start with the well-publicized figure of $500,000 per household for the present value of government retirement promises;

2) Subtract out the below poverty line households

3) Subtract out the past retirement age households

4) Add in the cost of cashing out pensions, IRAs and Keoghs

5) Convert from current dollars to total dollars

When we add those simple steps together, we will find that our answer is an impossible sum - if the dollar in the future is worth anything close to a dollar today. Far too many symbols have been promised relative to the actual resources that will available - meaning doom for the dollar. We will close by discussing how through understanding this issue - we can find the means to turn it from major societal problem into potentially lucrative individual opportunities for building wealth on a long-term and tax-advantaged basis.

weiter: http://www.safehaven.com/article-8738.htm

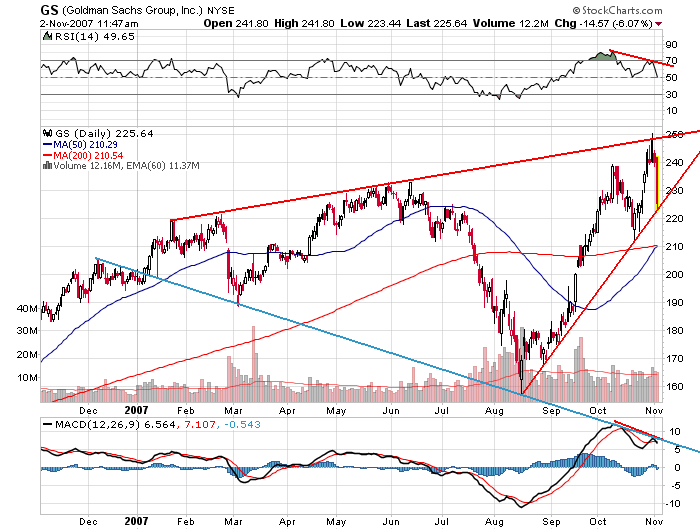

DAX hält ja Deine 7830 standhaft - wahscheinlich neiden die Traderfuzzis Dir Deinen erholsamen Urlaub.

Angehängte Grafik:

gs12m.png (verkleinert auf 72%)

gs12m.png (verkleinert auf 72%)

Eine solche Korrektur ist bisher, also in den letzten 3 Jahren, immer mehr oder weniger glimpflich abgelaufen. Meist war es so, dass nach einer relativ kurzen Schwächephase (- 20 %) die Käufer recht schnell wieder eingetstiegen sind ("Kaufgelegenheit"). Richtige Abstürze an einem Tag gab es auch kaum, vermutlich auch, weil die Institutionellen die Kurs-Abstürze mit eigenen Käufen gebremst haben. An einem richtigen Crash hat ja keiner ein Interesse, zu allerletzt die Institutionellen.

Was aber, wenn es in den nächsten Wochen zu einem Crash kommt, und den Institutionellen das Kapital fehlt, um die Kurse zu stützen. Eine Citibank, eine JP Morgan oder eine BOA, die finanziell in die Bredouille gekommen sind, werden zur Zeit kaum das nötige Kleingeld aufbringen können, um bei einem Crash zu intervenieren. Das gilt sicher auch für die anderen Banken, die im Zuge der Hypothekenkrise Federn gelassen haben.

These:

Die Märkte schwanken. Und wenn was passiert, ist keiner da, der schützend seine Hände "darunter" halten kann.

Wie seht ihr das?

Optionen

| Boardmail an "Ischariot MD" |

Wertpapier: S&P 500 |

und nochwas - wir haben es nicht nur mit einem zeitlich beschränkten Angebot-Nachfrage problem von Öl zu tun.

Das Angebot ist nicht mehr nennenswert zu erhöhen. Ölpreis wird daher mittelfristig erst dann fallen - wenn die Wirtschaften in die Rezession schlittern - dann fällt die Nachfrage.

dann erholen sich die wirtschaften wieder - aber der Ölpreis wird sich dann auch wieder schnell erholen und neue hochs bilden.......

dass werden die zyklen in den nächsten 10 - 15 Jahren sein

Optionen

| Boardmail an "biomuell" |

Wertpapier: S&P 500 |

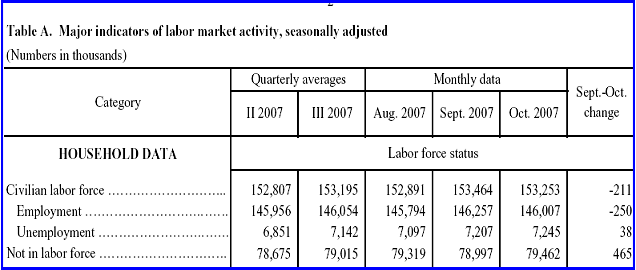

Quelle: http://globaleconomicanalysis.blogspot.com/ (Mike Shedlock/Mish)

Angehängte Grafik:

jobs-household-2007-11-02.png (verkleinert auf 80%)

jobs-household-2007-11-02.png (verkleinert auf 80%)

Level 3 storm about to hit Wall Street

By Martin Hutchinson

There's a mystery on Wall Street. Merrill Lynch wrote off $8.4 billion in its subprime mortgage business, a figure revised up from $4.9 billion, yet Goldman Sachs reported an excellent quarter and didn't feel the need for any write-offs. The real secret of the difference is likely to be in the details of their accounting, and in particular in the murky world, shortly to be revealed, of their "Level 3" asset portfolios.

Both Merrill and Goldman have Harvard chairmen - Merrill's Stan O'Neal from Harvard Business School and Goldman's Lloyd Blankfein from Harvard College and Harvard Law School. Thus it's pretty unlikely their approaches to business are significantly different - or is a Harvard MBA really worth minus $8.4 billion compared with a law degree? (The special case of George W Bush may be disregarded in answering that question.)

We may be about to find out. From November 15, we will have a new tool for figuring out how much toxic waste is in investment banks' balance sheets. The new US accounting rule SFAS157 requires banks to divide their tradable assets into three "levels" according to how easy it is to get a market price for them. Level 1 assets have quoted prices in active markets. At the other extreme Level 3 assets have only unobservable inputs to measure value and are thus valued by reference to the banks' own models.

Goldman Sachs has disclosed its Level 3 assets, two quarters before it would be compelled to do so in the period ending February 29, 2008. Their total was $72 billion, which at first sight looks reasonable because it is only 8% of total assets. However the problem becomes more serious when you realize that $72 billion is twice Goldman's capital of $36 billion. In an extreme situation therefore, Goldman's entire existence rests on the value of its Level 3 assets.

The same presumably applies to other major investment banks - since they employ traders and risk managers with similar educations, operating in a similar culture, they probably have Level 3 assets of around twice capital. Citigroup, J P Morgan Chase and Bank of America may have less since their culture is different; before 1999 those institutions were pure commercial banks and a substantial part of their business still lies in retail commercial banking, an area in which the investment banks are not represented and Level 3 assets are scarce.

There has been no rush to disclose Level 3 assets in advance of the first quarter in which it becomes compulsory, probably that ending in February or March 2008. Figures that have been disclosed show Lehman with $22 billion in Level 3 assets, 100% of capital, Bear Stearns with $20 billion, 155% of capital, and J P Morgan Chase with about $60 billion, 50% of capital. However those figures are almost certainly low; the border between Level 2 and Level 3 is a fuzzy one and it is unquestionably in the interest of banks to classify as many of their assets as possible as Level 2, where analysts won't worry about them, rather than Level 3, where analyst concern is likely.

The reason analysts should worry is that not only are Level 3 assets subject to eccentric valuation by the institution holding them, but the ability to write up their value in good times and get paid bonuses based on their capital uplift brings a temptation that few on Wall Street appear capable of resisting. Both Goldman Sachs and Merrill Lynch are reported to have made profits of more than $1 billion on their holdings of Level 3 assets in the first half of 2007, for example, profits on which bonuses will no doubt be paid at the end of their fiscal years. Given that we have had five good years on Wall Street, years in which nobody has known the amount of Level 3 assets on banks' balance sheets, and no significant media waves have been made questioning their valuation methodologies, it would not be surprising if many banks' Level 3 assets had become seriously overstated, even without any downturn having occurred.

When Nomura Securities sold its mortgage portfolio and exited the US mortgage business in this quarter, it took a write-off of 28% of the portfolio's value, slightly above the 27% of the portfolio that was represented by subprime mortgage assets. Were Goldman Sachs's Level 3 assets similarly value-impaired, it would result in a $20 billion write-off, more than half Goldman's capital, leaving the bank severely damaged albeit probably still in existence.

Defenders of Goldman Sachs and the rest of Wall Street will insist that less than 27% of their Level 3 assets are represented by subprime mortgages yet that is hardly the point. Subprime mortgages, estimated to cause losses of $400-500 billion to the market as a whole, though only a fraction of that to Wall Street, have been only the first of the Level 3 asset disasters to surface. There is huge potential for further losses among assets whose value has never been solidly based. These would include the following:

Mortgages other than subprime mortgages. With the decline in house prices accelerating, the assumptions on which even prime mortgages were made are being exposed as fallacious. As house prices decline, debt to equity ratios increase, and for mortgages with an original loan-to-value ratio of 90% or more, quickly pass the 100% at which a mortgage becomes uncovered. If the value of conventional mortgages decline many securities related to them, currently classed as Level 1 or 2 assets, will become un-marketable and descend into Level 3.

Securitized credit card obligations. $915 billion of credit card debt is currently outstanding, the majority of it securitized, and its default rate is likely to soar as the full effects of the home mortgage market's crack-up spread to the credit card area. The risks in Level 3 portfolios derived from this asset class arise particularly in the areas of complex derivatives and manufactured assets based on credit card debt pools.

Leveraged buyout bridge loans. After a hiccup in August, the market in these has reopened recently, although around $250 billion of them still remains on banks' balance sheets. The value of a leveraged buyout bridge loan that has failed to find a pier to support the other end of the bridge is very dubious indeed, even though these loans are being carried in the books at or close to par. As the value of underlying assets declines and the cash flow fails to match debt payments, the deterioration in credit quality of these loans will accelerate.

Asset backed commercial paper. The amount of asset backed commercial paper outstanding has dropped from $1.2 trillion to $900 billion in the last three months. This financing structure was always unsound; it was basically a means of removing the assets backing the commercial paper from bank balance sheets, and always faced the problem of a severe mismatch between asset and liability duration. The $100 billion vehicle intended to rescue this market has found a mixed reception to say the least. It is likely that as credit conditions deteriorate, the assets underlying ABCP vehicles will increasingly find themselves on bank balance sheets, where they will prove to be almost completely unmarketable.

Complex derivatives contracts. Even simple interest rate swaps and currency swaps caused large losses in the last significant credit tightening in 1994, although most of those losses were suffered by Wall Street's customers rather than Wall Street itself. The more complex transactions that have been devised during the last 12 giddy years are much more likely to prove impossible either to sell or to hedge. Goldman Sachs reported that in the third quarter of 2007 its profits on derivatives used for hedging more or less matched its losses on subprime mortgages. It is likely in reality that the bulk of those profits were incurred through model-based write-ups of value on contracts that were within the Level 3 category - after all, Goldman's Level 3 assets increased by a third during the quarter. It's not much good shorting to match a long position you don't like if your hedging shorts prove to be impossible to close out.

Credit Default Swaps, the global outstanding value of which in June 2007 was $2.4 trillion, according to the Bank for International Settlements. These are a relatively new instrument, the efficacy of which has not been tested in a downturn. It appears likely that the value in banks' books of their Level 3 credit derivatives contracts bears no relation whatever to reality. As discussed above, the incentives have been all in favor of inflating it.

The capital underlying Wall Street, at the top, is not all that large - a matter of a few hundred billion. Given the piling of risk upon risk that has been engaged in over the last few years, and the size of the losses in the mortgage market alone that seem probable - my own estimate last spring of $980 billion looks increasingly likely to be somewhat below the final figure - it appears almost inevitable that in a bear market in which liquidity dries up and investors become skeptical, Wall Street's capital will be wiped out. Only the commercial banks like Wachovia and Bank of America whose investment banking ambitions have been largely thwarted and whose portfolios of Level 3 rubbish are correspondingly lower, are less likely to disappear.

Given the size of the overall figures involved and the excessive earnings that Wall Street's participants have enjoyed over the last decade, a taxpayer-funded bailout of Wall Street's titans would seem politically impossible, however loud the lobbyists scream for it.

In the long run, that is probably a blessing for the US and world economies.

Immerhin soll der Angestellte die Bombe einfach in seinem Truck in das Werk gebracht haben.

Was die Börse angeht da gebe ich dir recht. Im Normalfall reagiert die Börse sofort auf solche Nachrichten, heute nicht.

Gruß

Permanent