Der USA Bären-Thread

Seite 352 von 6257 Neuester Beitrag: 06.07.25 13:32 | ||||

| Eröffnet am: | 20.02.07 18:45 | von: Anti Lemmin. | Anzahl Beiträge: | 157.419 |

| Neuester Beitrag: | 06.07.25 13:32 | von: Frieda Friedl. | Leser gesamt: | 25.571.115 |

| Forum: | Börse | Leser heute: | 2.806 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 350 | 351 | | 353 | 354 | ... 6257 > | ||||

http://www.investorsinsight.com/otb_va_print.aspx?EditionID=604

Unheimlich

So ganz allmählich müsste jedem Beobachter der Finanz- und insbesondere der Aktienmärkte mulmig werden. Zuletzt mehren sich die Anzeichen für einen deutlichen Abschwung der Welt- und insbesondere der amerikanischen Konjunktur, die Ölpreise steigen auf neue Rekorde, die Unternehmen melden schlechte Quartalszahlen, die Kreditkrise schwelt weiter, der amerikanische Verbraucher scheint aus seinem Konsumrausch aufzuwachen, der Dollar bekommt einen Schwächeanfall nach dem anderen.

Aber trotz aller schlechten Nachrichten - die Aktienkurse halten sich in der Nähe ihrer Hochs auf.

Bullische Akteure erklären das damit, dass die schlechten Nachrichten regelmäßig "eingepreist" würden. Und wenn dies geschehen sei, könnten die Kurse wieder/weiter steigen. Diesem Argument kann man ja in früheren Phasen einer Hausse durchaus etwas abgewinnen. Aber auch noch nach über vier Jahren im Aufwärtstrend und fortschreitenden Zeichen für (mindestens) einen zyklischen Abschwung?

Das erinnert an einen Schwimmer, dem man ständig mehr Gewichte anhängt. Wenn er dann wieder auftaucht, freut man sich über dessen Robustheit und macht weiter. Irgendwann taucht er dann eben nicht mehr auf. So ähnlich ist die Situation im Aktiengeschäft: Die Risikofreude sieht sich mit jeder verdauten schlechten Nachricht bestätigt. Die Gier reißt alle mit. Bis zu viel zusammen kommt und die Gier in Angst umschlägt.

In den vergangenen Tagen sprach viel für ("Werbe"-)Aktivitäten großer Akteure. Bis 20:00 unserer Zeit ließ man die Aktienindices fallen, danach erholten sie sich deutlich. Dow und S&P 500 wurden an die EMA50 "hingedengelt", die von institutionellen Investoren viel beachtet wird. Die Umsätze waren dabei deutlich überdurchschnittlich. Jeweils zeitgleich erholten sich auch die "Liquiditätsindikatoren": Die Rendite der T-Bills stieg, die Wechselkurse von Euro und Dollar jeweils gegen Yen legten zu.

Die Akteure sind in Anbetracht der am Mittwoch stattfindenden Zinssitzung der Fed hin- und hergerissen zwischen deutlich steigenden Inflationsaussichten auf der einen und weiteren Zinsschnitten der Fed auf der anderen Seite. Inflation ist gut für Schuldner - und davon gibt es genug. Eine weitere deutliche Zinssenkung schürt die Hoffnung auf einen abgefederten zyklischen Abschwung und weitere günstige Verschuldung. Die steigenden Inflationsaussichten aber dämpfen die Hoffnung auf schnelle, weitere Zinsabschläge.

Nicht ganz ins bullische Bild passen da die Renditen von Staatsanleihen, die zuletzt deutlich gestiegen sind - und das, obwohl z.B. Bundesbankpräsident Weber kürzlich vor einer Beschleunigung der Inflation gewarnt hat. Die Papiere profitieren angesichts der weiter schwelenden Kreditkrise und konjunkturellen Belastungsfaktoren vom Wechsel aus riskanteren Anlagen in Staatsanleihen. Zudem rechnet kaum jemand für die nahe Zukunft mit Zinssteigerungen.

Es ist wahr - wird z.B. der S&P 500-Index um die Inflationserwartungen bereinigt, die sich aus der Entwicklung von Goldpreis und Zinsen ergeben, so liegt dieser "reale" Wert aktuell so hoch wie im Juni 2005 und deutlich unter den Spitzenwerten vom November 2001 und Juli 2003. Selbst der so bereinigte Ölpreis liegt noch unter dem Hoch aus August 2005. Und genau der Blick durch die Inflationsbrille dürfte die bullische Attitüde gegenwärtig noch stützen - inflationsbereinigt notieren die Kurse nicht im Extrembereich. Fragt sich nur, was geschieht, wenn selbst die "realen" Kurse zu hoch liegen im Vergleich zu dem Niveau, das angesichts der fundamentalen Perspektiven "fair" wäre.

Zu dieser Frage hat sich kürzlich der Perma-Bär Stephen Roach von Morgan Stanley wieder mit einem lesenswerten Beitrag zu Wort gemeldet (Link im Diskussionsforum der Web-Seite der TimePattern).

Unter der Überschrift "A Subprime Outlook for the Global Economy" sieht er das exzessive Wachstum des US-Konsums zu Ende gehen. Das US-BIP ist aktuell zu 72 Prozent vom privaten Verbrauch bestimmt, nach durchschnittlich 67 Prozent in den letzten 25 Jahren des vergangenen Jahrhunderts. Einkommens- und Vermögenseffekte gerieten jetzt unter Druck und würden den schuldenlastigen Verbraucher empfindlich treffen.

Mit der kommenden Konsolidierung des amerikanischen Konsums steigen zwar die Chancen für eine partielle Ausbalancierung der globalen Ungleichgewichte. Dies aber müsse nach Roach einhergehen mit einer Ausweitung des Konsums in den Ländern mit deutlich positiver Sparquote. Je weniger dies geschieht, je mehr muss der US-Verbraucher die Lasten des Anpassungsprozessen tragen. Dies würde wiederum einen bedeutenden negativen Einfluss auf das globale Wachstum haben und ein hohes und steigendes Rezessions-Risiko beinhalten.

Roach wäre nicht überrascht, wenn die Wachstumsraten der Weltwirtschaft nach Jahren um die 5 Prozent irgendwann in 2008 auf 3,5 bis 4 Prozent fiele. Das wäre für sich zwar kein Desaster, bliebe doch der nach-1970-Trend bei 3,7 Prozent immer noch intakt. Andersherum gerechnet würde das aber eine Reduktion der Wachstumsrate um 25 Prozent bedeuten. Und dies könnte dem Optimismus hinsichtlich der Entwicklung der Unternehmensgewinne einen empfindlichen Schlag versetzen, und damit auch den Aktienkursen. Positiv wäre, dass eine solche Entwicklung die Inflation dämpft und Staatsanleihen zu einem Comeback verhilft.

Aber, so schreibt Roach, die mittelfristige Prognose für die Weltwirtschaft steht nicht nur im Zeichen eines normalen zyklischen Abschwungs. Nein, Amerikas Finanzmarkt-bezogenes Wachstum kommt jetzt auf den Prüfstand. Und damit wiederum werden Kollateral-Schäden anderswo in einer USA-zentrierten Weltwirtschaft wahrscheinlich. Ein neuer, von den großen Wirtschafts-Nationen gemeinsam getragener Ansatz sei erforderlich - "before it's too late".

Halten Sie eine solche konzertierte Aktion für wahrscheinlich?

Klaus Singer

Marktstatus, Markttrends und Prognosen unter Timepatternanalysis

Leichtfertige Kommentare wie diese, die jetzt wieder die Runde machen und implizieren sollen, dass die Kreditabschreibungen von rund 8 Mrd. $ bei Merrill trotz aller Kreditmarktwirren vor allem ein unternehmensspezifisches Problem seien, kann man bald nicht mehr hören. Ebenso wie das Mantra, die Banken hätten ihre Risiken inzwischen besser diversifiziert - und ohnehin einen Großteil davon an Dritte abgegeben.

Auch wenn das für einzelne Banken der Fall sein mag: Im Großen und Ganzen kann die Sache nicht aufgehen. In der Euro-Zone ist die Passivseite des Bankensystems - wo beispielsweise Kundeneinlagen verbucht werden - über die vergangenen zehn Jahre um die sagenhafte Summe von 11.600 Mrd. Euro gestiegen, während das nominale annualisierte BIP um 2900 Mrd. Euro zugelegt hat.

Dummerweise muss die Aktivseite einer Bilanz aber immer gleich der Passivseite sein. Mit anderen Worten und einfach ausgedrückt: Um die Kundeneinlagen verzinsen zu können, müssen die Banken auch Kredite vergeben, aus denen sie ihrerseits Zinseinnahmen erlösen. Natürlich haben sie einen Teil der Kredite verpackt und verkauft. Nur haben die Banken die hochglanzverpackten Problemfälle auf der anderen Seite auch gekauft - oder Finanzinvestoren mit Darlehen versorgt, damit diese das tun können. Wenn die Kreditausfälle zunehmen, wie es nun der Fall ist, werden die Banken also ihr Fett wegkriegen, ob direkt oder indirekt. Selbst den auf Provisionen und Handelsgewinnen beruhenden Brokern ist wenig geholfen, wenn die Märkte in einer Kreditkrise austrocknen.

Verkannte Signale

Dass die US-Broker ebenso wie der gesamte US-Finanzsektor nach der Zinssenkung der Fed nicht recht auf die Beine gekommen sind, während der Gesamtmarkt die alten Spitzenstände übertroffen hat, ist derweil schon für sich genommen ein Unheil verkündendes Zeichen. Denn lässt die Unruhe im Finanzsektor nicht befürchten, dass die Finanzierung des defizitären US-Verbrauchers stockt? Dazu würde passen, dass außer den Finanzwerten, die heuer um rund zwölf Prozent gefallen sind, nur ein anderer ökonomischer Sektor im Minus ist: der konjunkturabhängige Konsum, der um sechs Prozent gesunken ist. Geht man etwas tiefer in die einzelnen Unterbranchen, fallen der Rückgang der Regionalbanken und Warenhäuser um 22 Prozent, das Minus der Bausparkassen um 30 Prozent sowie der Einbruch der Hausbaufirmen um 55 Prozent besonders ins Auge. Alles Branchen, die mittel- oder unmittelbar mit dem Ausgabengebaren der Verbraucher in Verbindung stehen. Auch die relative Schwäche des hoch zyklischen Transportsektors gibt zu denken.

Die Sorglosigkeit der Anleger in den anderen Sektoren (insgesamt ist der S&P 500 mit fünf Prozent im Plus) ist da geradezu verblüffend. Konsum und Wohnungsbau machen drei Viertel des US-BIP aus. Die US-Firmeninvestitionen, deren Einbruch von 12,6 auf 9,8 Prozent des BIP zwischen 2000 und 2003 die ganze Welt in Aufruhr versetzt hat, standen im zweiten Quartal 2007 für 10,7 Prozent. Kurzum: Die Gewinnschätzungen für die kommenden Quartale sind nicht mal die Kalkulationstabellen wert, in denen sie errechnet wurden.

http://www.ftd.de/boersen_maerkte/analysten/...erleugnung/269938.html

…..With that in mind, Curve Watcher's Anonymous is noting a striking similarity between recent yield curve action and that in 2001. Let's take a look.

$TYX is the yield on the 30 year long bond.

$TNX is the yield on the 10 year treasury note.

$TYX is the yield on the 5 year treasury note.

$IRX is the discount on the 3 month treasury bill.

Take a good look at the above chart. Haven't we seen this series of plays before?

There's only three small problems. The last time the Fed embarked on a slash and burn campaign lowering interest rates, the U.S. dollar index was sitting near 120, gold was near $300, and oil was near $20. Now the dollar index is under 80, gold is over $700, and oil is over $80.

The second problem is the Fed created a housing bubble (and lots of jobs) the last time they tried slashing interest rates. Who needs a house now that does not already have one (or two or three)? Should the Fed dramatically lower rates again, where are the jobs going to come from?

The third problem is that drug-induced highs need stronger and stronger doses to maintain the same high. There is not much room below interest rates of 1 to even think about a higher high.

The Irony of Bernanke's Predicament

High energy prices and falling home prices are two things of concern to consumers. The irony of the situation is that the only way oil prices are likely to sink is if the U.S. heads into a recession and/or the dollar strengthens considerably.

Bernanke is acting to prevent said recession by cutting rates. Good luck with home heating season coming up. If Bernanke does not cut rates, it will hasten the recession. A recession is badly needed, I might add, but Bernanke does not see it that way.

In addition the U.S. Dollar is likely to rally if the Fed pauses because rate cuts are priced in. Given that the dollar and the stock market have been inversely correlated for quite some time, if Bernanke acts to shore up the dollar by failing to cut rates, the stock market is likely to take a big hit.

I call this situation Economic Zugzwang. There are no winning moves.

http://www.minyanville.com/articles/index/a/14629

Angehängte Grafik:

yield_curveplaybook_10-07.gif (verkleinert auf 62%)

yield_curveplaybook_10-07.gif (verkleinert auf 62%)

Oder wollte der Autor Umschreibungen wie "forced step" nicht benutzen, weil "Zugzwang" in angelsächsischen Ohren martialischer klingt? ;-)

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

"In last week's letter I talked about the $80 billion Super SIV fund that is being created by Citigroup, Bank of American and JP Morgan Chase. A lot of commentators have been writing about what a bad idea it is, and a few have taken me to task. They think it is a bad idea to rescue bad investments. They want the market to clean out the bad stuff so we can start functioning again.

And I agree, but that is not what the fund is going to do, as I understand it. The Super SIV fund is simply offering to buy only the good assets in failed SIVs. In essence, they (and the US Treasury) are worried that there will be a rush to the exits from failing SIVs (mostly in Europe) that will result in a panic forcing down the prices of good assets far below where they should be. That could seriously affect the capital structure of US banks and create a severe credit crunch. This fund simply sets a floor for the price of good assets at $.94 cents in cash and a 4% note.

They are not going to take the subprime junk. That is going to have to be written off by whoever owns it. This does not seem like a bail-out to me, but self-interested parties in a free market whose interest is in avoiding a panic and also will allow a mark to market price for assets. I think it makes sense.

If I am wrong and any of the toxic subprime assets show up in the Super SIV, then I would agree that it is a very bad idea indeed. Anyone who wants to read my entire take on the SIV problems and missed it last week can go to http://www.2000wave.com/article.asp?id=mwo101907."

Strike on Iran Would Roil Oil Markets, Experts Say

Price Hits Record Close; U.S. Tightens Sanctions

"If war breaks out, anticipate that all hell will break loose in the oil markets," said Robin West, chairman of PFC Energy, a District oil consulting firm.

http://www.washingtonpost.com/wp-dyn/content/.../AR2007102502840.html

Halloween bei Merrill

Preisfrage: Wie verliert man 3,4 Milliarden Dollar in drei Wochen? Antwort: Man durchforstet die Bilanzen der Wall Street nach Subprime-Leichen. Wer den Schaden hat, braucht für den Spott nicht zu sorgen. In Ihrem Fall, Mr. O’Neal, ist beides verdient.

http://www.handelsblatt.com/News/Boerse/...halloween-bei-merrill.html

Anleger flüchten aus dem US-Dollar

Die zunehmenden Spekulationen über weitere Zinssenkungen der US-Notenbank haben den Dollar unter Druck gesetzt. Die US-Währung wertete auf breiter Front ab. "Die Anleger sind aus dem US-Dollar geflüchtet und in hochverzinsliche Währungen gegangen", sagte Carsten Fritsch, Devisenanalyst der Commerzbank…..

…..Zur Aufwertung vieler Hochzinswährungen gegenüber dem US-Dollar tragen nach Meinung von Hans Redeker, Devisenanalyst von BNP Paribas, auch die privaten US-Haushalte bei, die massiv Kapital im Ausland, vor allem in Schwellenländern anlegen. "Solange die Aktienmärkte dort gut laufen, wird dieser Trend anhalten. Sobald die Aktienmärkte nach unten gehen, könnte der US-Dollar aber vorübergehend wieder aufwerten", sagte er.

Dann würden US-Anleger ihre ausländischen Vermögenswerte verkaufen und das Kapital in die USA zurückfließen lassen. Dazu könne es kommen, wenn die Angst vor einer US-Rezession die Finanzmärkte stärker erfasse, so Redeker. So eine rezessionsbedingte Dollar-Aufwertung wäre Marktteilnehmern zufolge nur von kurzer Dauer. Insgesamt rechnen Anleger weiter mit einem schwachen Dollar….

Bank of England wird unruhig

Das beunruhigt zunehmend die Bank of England (BoE). Sie warnte in ihrem Finanzstabilitätsbericht für eine Notenbank ungewöhnlich deutlich vor einem "steilen Abfall" des US-Dollar, sollten die Vermögenspreise in den USA wegen der dortigen Konjunkturschwäche weiter fallen oder sich die jüngste Stimmung gegen US-Staatspapiere als dauerhaft erweisen. So ein Dollar-Verfall könne ein potenzieller weiterer "Schock" für das weltweite Finanzsystem sein. Die BoE bemerkte kritisch an, dass es trotz der jüngsten Schwäche des Dollar kaum Zeichen gebe, dass sich das US-Leistungsbilanzdefizit nachhaltig verbessert habe. "Es gibt das Risiko, dass der US-Dollar weiter fallen muss, um die US-Außenposition zu stabilisieren", so die BoE…..

http://www.ftd.de/boersen_maerkte/geldanlage/...%20Dollar/270502.html

Folker Hellmeyer - Datenpotpourri für den USD wenig bekömmlich - Gold en vogue!

Mithin haben die drei größten Währungen unseres Finanzsystems latente und nachhaltige Defizite. Unter diesen genannten Aspekten ist es nur verständlich, dass Gold als Alternative ohne demographische Belastungen, ohne strukturellen Defizite, ohne Bilanzskandale, ohne politische Lüge und ohne Arbeitslosigkeit eine Renaissance als nachhaltiges Investment erlebt. Dabei steht weniger der spekulative Aspekt im Vordergrund, als vielmehr der Aspekt der Werthaltigkeit.

http://www.goldseiten.de/content/marktberichte/...te.php?storyid=5653

Inflationsangst dämpft Konsumklima

26.10.2007

Ergebnisse der GfK-Konsumklimastudie für Oktober 2007

Der starke Euro und zunehmend kritische Stimmen hinsichtlich der weiteren konjunkturellen Entwicklung verpassen der Konjunkturerwartung in Deutschland einen Dämpfer.

http://www.innovations-report.de/html/berichte/.../bericht-93674.html

Home builders: Worst is yet to come

Economists offer dour outlook for housing prices and construction, citing continuing credit crisis - weakness is likely to persist into 2009.

http://money.cnn.com/2007/10/24/news/economy/...ostversion=2007102414

Doug Kass: They're Still Not Getting It on Housing

I have mentioned in the past that a 20% drop in home prices, as currently predicted in the Case Shiller Futures Index by 2011, means that about $4 trillion of consumer wealth will be wiped out. Another $500 billion to $1 trillion of losses looks to be taken by the financial institutions and hedge funds from the collateralized debt obligation mess.

That's close to the amount lost after the tech bubble -- and very large in the context of a $13 trillion U.S economy (the number Larry used last night). Moreover, the financial industry's reluctance to provide credit to homeowners provides another important economic headwind.

The housing problem ring-fenced? Not likely.

http://www.thestreet.com/pf/newsanalysis/newsonthego/10386473.html

Paul Krugman - A (Subprime) Catastrophe Foretold

Yet such loans were primarily offered to those least able to evaluate them. "Why are the most risky loan products sold to the least sophisticated borrowers?" Mr. Gramlich asked. "The question answers itself - the least sophisticated borrowers are probably duped into taking these products." And "the predictable result was carnage."

http://www.spiegel.de/international/0,1518,513748,00.html

When Crumbling Credit Meets Deadly Leverage

The credit cycle has clearly turned. Financial institutions, such as banks, have only begun to add to the massive loan loss reserves they’ll need to shelter from the storm of at least $2 trillion of consumer, commercial real estate, corporate, and single family mortgage loans, that could easily roll over into default. And that’s not all.

http://www.prudentbear.com/..._content&view=article&id=4808&Itemid=57

IT SURE HAS BEEN DIFFERENT - SO FAR!

In 2001, the Dow was then down over the next two weeks. But it rallied back in anticipation of a second rate cut late in January, about as has been happening over the last week. However, with the second rate cut the Dow began to decline, and was down 14.2% two months later (even though the Fed had cut rates two more times in the interim). The Nasdaq rallied for three weeks after the first rate cut, and then also began plunging with the second rate cut, and was down a big 37% two months later.

The jury is still out on how the market will react if the Fed cuts rates for the second time in this cycle, next Wednesday, as is widely expected. Faith in the power of the Fed riding to the rescue was sure not a good bet in the last cycle of a slowing economy.

But then, this time has been different so far.

http://www.decisionpoint.com/TAC/HARDING.html

Sondermüll mit neuer Verpackung

Laut einem Bloomberg Bericht, erwägt die Deutsche Bank, dem 80-Milliarden-Dollar Vehikel amerikanischer Banken beizutreten, um den commercial paper Markt neu zu beleben.

„Wir machen uns darüber Gedanken und sind in einem konstruktiven Dialog mit den amerikanischen Banken und den amerikanischen Behörden“, sagte Joe Ackermann in einem Interview in Frankfurt. „Jegliche Unterstützung für den Markt, besonders von privater Seite, ist wünschenswert, aber die Details sind noch zu wenig klar um eine definitive Entscheidung zu fällen.“

Citigroup, JPMorgan Chase und die Bank of America, die drei grössten U.S. Banken kamen am 15. Oktober überein, einen Fonds zu gründen, welcher Wertschriften von notleidenden strukturierten Investment Vehikeln, kurz SIV, aufkaufen soll. (Siehe auch Sondermüll mit neuer Verpackung) Quelle: Blog Zeitenwende

Fed likely to cut rates to 3.75 percent: PIMCO's Gross

NEW YORK (Reuters) - The Federal Reserve will cut interest rates again but probably not at the October policy-making meeting, said Bill Gross, manager of the world's biggest bond fund on Tuesday.

The Fed's target rate for federal funds is on a downward track because of slower economic growth, said Gross, the chief investment officer of Pacific Investment Management Co. or PIMCO, speaking on CNBC television.

"The Fed needs to cut interest rates probably as low as 3.75 (percent) before we are all done," he said.

http://www.reuters.com/article/ousiv/idUSN1644452520071016

Mixed Economic Picture Ahead of Fed Meeting

The Fed will meet on Tuesday and Wednesday and is expected to consider an additional cut to its benchmark interest rate. Investors betting on the Fed’s action appear certain that the governors will cut rates, but some analysts say underlying strength in the economy could dampen chances for a cut. The reports are the final flurry of economic data before the meeting.

http://www.nytimes.com/2007/10/26/business/...oref=slogin&oref=slogin

Asset-backed Securities (ABS) issuance increased to $9bn this week. Year-to-date total US ABS issuance of $496bn (tallied by JPMorgan) is running 32% behind comparable 2006. At $214bn, y-t-d Home Equity ABS sales are 54% off last year's pace. Year-to-date US CDO issuance of $272 billion is running 5% below 2006."

(Doug Noland, The Credit Bubble Bulletin, PrudentBear, 27.10.07)

Happige Zahlen!

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

Ich weiss, "die Lemminge werden eingelullt und die Profis verkaufen" euer Glaube an diese Experten ist hier total ausgeprägt, obwohl nur ganz selten einer seinen Index schlägt.

Und dass die Insider zuletzt stark eingestiegen sind, darauf geb ich gar nix, ist für mich als Bulle eher ein schlechtes Zeichen, diese Spezies sitzt zu nah dran und der Markt ist meist andrer Meinung...

Optionen

| Boardmail an "lehna" |

Wertpapier: S&P 500 |

scheint ja wieder auf 50bps naechste Woche rauszulaufen, soweit ich das nach 10min ueberfliegen der News letzter Woche einschaetzen kann.

Haltet die Ohren steif ;-)

Optionen

| Boardmail an "obgicou" |

Wertpapier: S&P 500 |

Über Details wollte Ackermann aber noch nicht reden. ......Neben der Deutschen Bank prüfen auch andere deutsche Großbanken eine Beteiligung an dem Krisenfonds in den USA. Bekannt ist derzeit, dass es bei der Dresdner Bank ähnliche Überlegungen gibt wie bei der Deutschen Bank. Der Präsident des Bundesverbands deutscher Banken (BdB) und Commerzbank-Chef, Klaus-Peter Müller, warnte zudem vor einer vorschnellen Verurteilung des geplanten Fonds. Bei der IWF-Tagung am vergangenen Wochenende sagte Müller, es wäre positiv, wenn der Superfonds durch Bereitstellung von Liquidität und mehr Preistransparenz dazu beitrage, den Markt wieder in Gang zu setzen.

http://www.n-tv.de/871575.html

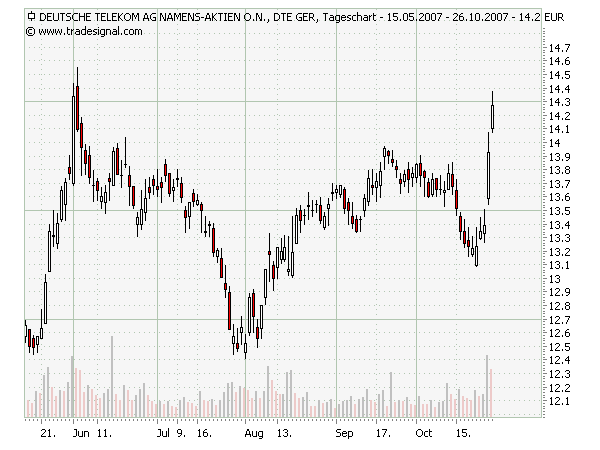

Angehängte Grafik:

dte6m.png (verkleinert auf 85%)

dte6m.png (verkleinert auf 85%)

This Time, Housing Is Taking Department Stores Down With It

By FLOYD NORRIS and MICHAEL BARBARO / New York Times

When home builders' stocks plunged in 2006, Wall Street was confident that the problems would not spill over into the larger economy. Exhibit A? Department store stocks rose steadily despite the housing woes.

Not this time around.

Housing stocks have fallen again — and this time the department store stocks have marched down with them.

Since April, when investors voiced optimism that the housing slide had been contained, shares of the country's biggest department store chains have fallen by about 30 percent.

With the sagging prices, investors have rendered a harsh judgment on the coming holiday shopping season, predicting that consumers will severely cut back on spending.

The gloom since April 20 has been spread evenly across the big chains: shares of J. C. Penney are down 33 percent, Macy's by 27 percent, Kohl's by 28 percent and Sears by 28 percent.

Robert J. Barbera, the chief economist of the Investment Technology Group, said, “The conventional wisdom of a year ago was that we would have a soft landing in housing.” But today, he said, “the stock market message is a hard landing for housing, with clear damage to consumer discretionary spending.”

In interviews, retail executives conceded that the slumping housing market was taking its toll. “We are in the window-covering business, and you don't cover windows in houses you don't build,” said Myron E. Ullman III, the chief executive of J. C. Penney.

But some executives remain at least a little upbeat, complaining that investors are lumping the department stores together.

“I believe in the fourth quarter people will continue to buy,” said Terry J. Lundgren, the chief executive of Macy's. Analysts, he said, “are speculating that the consumer is going to withdraw and not spend at the same levels as she has in the past several seasons.”

And over at Saks, the view is that the housing and credit crisis is somebody else's problem. “The underlying strength in the luxury market is there,” said Stephen I. Sadove, the chief executive. “That consumer is driven more by confidence in the stock market than in the housing market.”

Investors also appear less certain that Saks will suffer. Its shares are off just 7 percent since April 20.

Still, the stocks of other higher-priced department store chains, which have been largely immune to housing market troubles over the last several years, have plunged this year. Nordstrom is down almost a third.

Economic slowdowns traditionally hurt stores catering to a less affluent customer base, like Wal-Mart and Target. But in a reversal, those discount chains have not done as poorly as department stores.

“The problems have crept up the consumer food chain,” said Bill Dreher, an analyst at Deutsche Bank Securities.

Behind the falling stock prices are slipping sales at stores.

After a strong performance early this year, sales at department stores open at least a year have fallen three of the last six months, according to Deutsche Bank.

The stores have blamed a variety of factors, like an unseasonably warm August and September, which hurt back-to-school clothing sales, and poor sales of household goods, tied to the slowing housing market.

Sales at Macy's and J. C. Penney have fallen five of the last six months. Kohl's sales have fallen four of the last six.

Not everyone is blaming economics and weather. Mr. Lundgren has pointed to a big marketing campaign last fall to introduce Macy's in cities like Chicago and Boston, which made for tough sales comparisons this year.

The accompanying charts show that in 2006, when housing troubles first became apparent, shares in home builders plunged but department store shares held their value. The charts show the 26-week change in prices of the Standard & Poor's 500 home-building index and of the S. &P. 500 department store index.

In 2006, when the home building stocks plunged, the rest of the market, including department stores, kept on rising, and the home builders themselves recovered in late 2006.

But this year, with the credit crisis taking hold over the summer, housing stocks have fallen again, and so have department store stocks.

The overall stock market has held up fairly well. The S. &P. 500 hit a record high earlier this month and has since lost only a small part of its value. That performance, however, may reflect better on the health of American companies than on the American economy. A rising share of profits is coming from foreign operations, while domestic earnings are weak for many companies.

Those who think Americans are likely to reduce their spending point to two related factors. First, in recent years the amount of home equity loans rose by as much as $180 billion a year, with much of the money going to consumption. New loans of that variety are much harder to get now that banks have tightened credit standards and home values are falling in many areas.

Second, the wealth effect of seeing that a house had risen in value helped to encourage spending, even if the money did not come directly from a mortgage loan. Now there may be a reverse effect, as worries about home values lead to a reluctance to spend.

If consumers do cut back, it stands to reason that department stores like Macy's and Nordstrom may lose market share to lower-priced merchants. That could explain the smaller declines in shares of those chains.

www.nytimes.com/2007/10/27/business/27charts.html

Angehängte Grafik:

fivethingsripple.png

fivethingsripple.png

Many states seen facing water shortages

By BRIAN SKOLOFF, Associated Press Writer

Fri Oct 26, 9:24 PM ET

An epic drought in Georgia threatens the water supply for millions. Florida doesn't have nearly enough water for its expected population boom. The Great Lakes are shrinking. Upstate New York's reservoirs have dropped to record lows. And in the West, the Sierra Nevada snowpack is melting faster each year. Across America, the picture is critically clear — the nation's freshwater supplies can no longer quench its thirst.

The government projects that at least 36 states will face water shortages within five years because of a combination of rising temperatures, drought, population growth, urban sprawl, waste and excess.

"Is it a crisis? If we don't do some decent water planning, it could be," said Jack Hoffbuhr, executive director of the Denver-based American Water Works Association.

Water managers will need to take bold steps to keep taps flowing, including conservation, recycling, desalination and stricter controls on development.

"We've hit a remarkable moment," said Barry Nelson, a senior policy analyst with the Natural Resources Defense Council. "The last century was the century of water engineering. The next century is going to have to be the century of water efficiency."

The price tag for ensuring a reliable water supply could be staggering. Experts estimate that just upgrading pipes to handle new supplies could cost the nation $300 billion over 30 years.

"Unfortunately, there's just not going to be any more cheap water," said Randy Brown, Pompano Beach's utilities director.

It's not just America's problem — it's global.

Australia is in the midst of a 30-year dry spell, and population growth in urban centers of sub-Saharan Africa is straining resources. Asia has 60 percent of the world's population, but only about 30 percent of its freshwater.

The Intergovernmental Panel on Climate Change, a United Nations network of scientists, said this year that by 2050 up to 2 billion people worldwide could be facing major water shortages.

The U.S. used more than 148 trillion gallons of water in 2000, the latest figures available from the U.S. Geological Survey. That includes residential, commercial, agriculture, manufacturing and every other use — almost 500,000 gallons per person.

Coastal states like Florida and California face a water crisis not only from increased demand, but also from rising temperatures that are causing glaciers to melt and sea levels to rise. Higher temperatures mean more water lost to evaporation. And rising seas could push saltwater into underground sources of freshwater.

Florida represents perhaps the nation's greatest water irony. A hundred years ago, the state's biggest problem was it had too much water. But decades of dikes, dams and water diversions have turned swamps into cities.

Little land is left to store water during wet seasons, and so much of the landscape has been paved over that water can no longer penetrate the ground in some places to recharge aquifers. As a result, the state is forced to flush millions of gallons of excess into the ocean to prevent flooding.

Also, the state dumps hundreds of billions of gallons a year of treated wastewater into the Atlantic through pipes — water that could otherwise be used for irrigation.

Florida's environmental chief, Michael Sole, is seeking legislative action to get municipalities to reuse the wastewater.

"As these communities grow, instead of developing new water with new treatment systems, why not better manage the commodity they already have and produce an environmental benefit at the same time?" Sole said.

Florida leads the nation in water reuse by reclaiming some 240 billion gallons annually, but it is not nearly enough, Sole said.

Floridians use about 2.4 trillion gallons of water a year. The state projects that by 2025, the population will have increased 34 percent from about 18 million to more than 24 million people, pushing annual demand for water to nearly 3.3 trillion gallons.

More than half of the state's expected population boom is projected in a three-county area that includes Miami, Fort Lauderdale and Palm Beach, where water use is already about 1.5 trillion gallons a year.

"We just passed a crossroads. The chief water sources are basically gone," said John Mulliken, director of water supply for the South Florida Water Management District. "We really are at a critical moment in Florida history."

In addition to recycling and conservation, technology holds promise.

There are more than 1,000 desalination plants in the U.S., many in the Sunbelt, where baby boomers are retiring at a dizzying rate.

The Tampa Bay Seawater Desalination Plant is producing about 25 million gallons a day of fresh drinking water, about 10 percent of that area's demand. The $158 million facility is North America's largest plant of its kind. Miami-Dade County is working with the city of Hialeah to build a reverse osmosis plant to remove salt from water in deep brackish wells. Smaller such plants are in operation across the state.

Californians use nearly 23 trillion gallons of water a year, much of it coming from Sierra Nevada snowmelt. But climate change is producing less snowpack and causing it to melt prematurely, jeopardizing future supplies.

Experts also say the Colorado River, which provides freshwater to seven Western states, will probably provide less water in coming years as global warming shrinks its flow.

California, like many other states, is pushing conservation as the cheapest alternative, looking to increase its supply of treated wastewater for irrigation and studying desalination, which the state hopes could eventually provide 20 percent of its freshwater.

"The need to reduce water waste and inefficiency is greater now than ever before," said Benjamin Grumbles, assistant administrator for water at the Environmental Protection Agency. "Water efficiency is the wave of the future."

http://hosted.ap.org/dynamic/stories/V/...CTION=HOME&TEMPLATE=DEFAULT

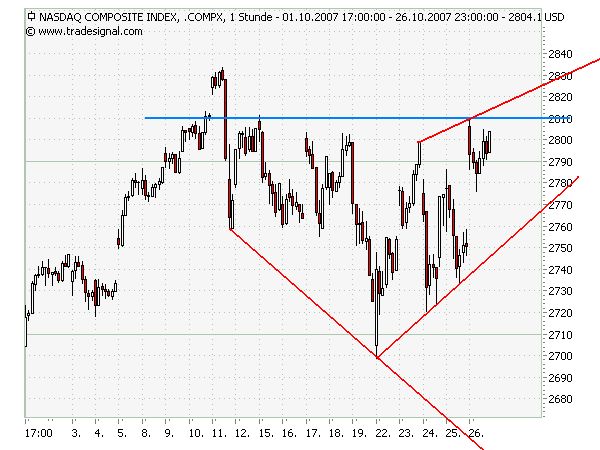

Nachfolgend ein paar Daten zum Nasdaq % of stocks above 200 dMA Index ($NAA200R):

Februar 2007: 60 % Juni: 55 %

Mitte August: 31 %

Anfang Oktober: 47,5 % (exakt im Schnittpunkt von wMA 100 durch wMA 200!) Vorwochenschluss: 41,5 %

aktueller Wochenschluss: 42,5 %

Dies deutet darauf hin, dass die aktuelle Nasdaq-Rallye auf sehr tönernen Füßen steht. Der breite Markt zieht kaum mit. Im Anhang der COMPX-Stundenchart, der hohe Volatilität erkennen lässt.

Angehängte Grafik:

compxhourly1m.png (verkleinert auf 85%)

compxhourly1m.png (verkleinert auf 85%)

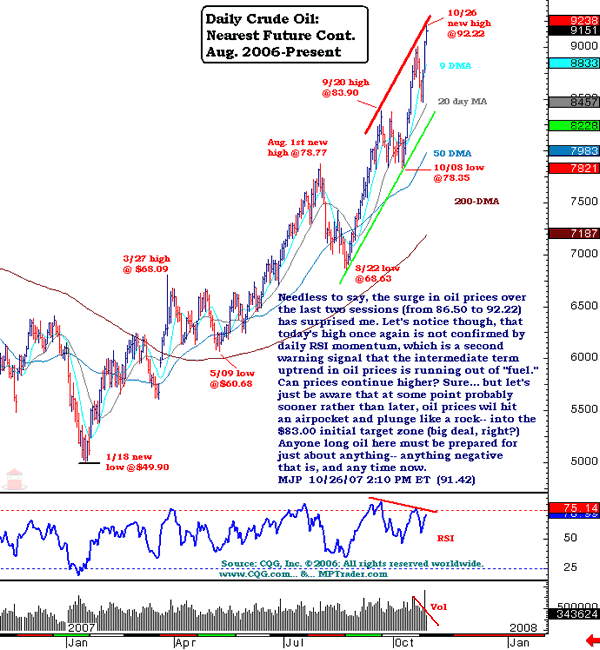

Angehängte Grafik:

wtic.png (verkleinert auf 85%)

wtic.png (verkleinert auf 85%)

Wenn ich darüber nachdenke, dass es wohl Alternativen zu Öl gibt, nicht jedoch zu Wasser, so frage ich mich, wieviel Wasser wohl in Summe der Ethanol-Boom benötigt. Denn dass z.B. die Mais- oder Getreide-Felder in den USA allein vom Regen bewässert werden, erscheint mir eher unwahrscheinlich, mal abgesehen von den übrigen benötigten Wasserressourcen im Produktionsprozess von Ethanol.

Addiere dazu Bevölkerungswachstum sprich auch mehr landwirtschaftlich genutzte Fläche für Nahrungsmittel, schlechte Infrastruktur im Bereich des Wassersektors, und und ….

…..In support of his forebodings, he cites the Nasdaq 100's spectacular performance so far this year -- last we checked, it had shot up a cool 25%, or some 448 points -- as a startling illustration of how a few exceptionally strong stocks can give the impression of a big bull move. Of that roughly 25%, or nearly 450 points, gained by the Nasdaq 100, a whopping 230 points, or over half the index's rise, has come from just three issues: Apple (135 points), Research In Motion (60 points) and Google (35 points)……

Gut aufgepasst, Gsamsa. Mir war das schon beim Schreiben aufgefallen, aber ich hatte keine Lust, das zu redigieren, weil meine Internetverbindung zeitweise wackelig ist (zurzeit in Urlaub und Net per WiFi).

Wo wir schon mal beim Erbsenzählen sind. Der Kredit bleibt in obiger Konstruktion konstant: Er beträgt immer 400 Dollar (es gab ja 100 Dollar Eigenkapital zum Kauf der 500). Variabel ist der Depot-Gesamtwert = Haben minus Soll. Als die Bonds noch bei 100 standen, lag der Gesamtwert bei 100 Dollar (500 Haben minus 400 Soll). Bereits bei 20 % Wertverlust der Bonds sinkt der Gesamtwert auf Null (400 Haben minus 400 Soll). Beim jetzigen Stand von 19 % der Nominale ergibt sich ein Gesamt-Depotwert von 500 x 0,19 = 95 minus 400 Schulden, also insgesamt -295.

"Erst wenn der letzte Baum gerodet, der letzte Fluß vergiftet, der letzte Fisch gefangen ist, werdet ihr feststellen, dass man Dollars nicht trinken kann."

[Indianerweisheit, Trinker-Variante]