Der USA Bären-Thread

Seite 351 von 6257 Neuester Beitrag: 06.07.25 13:32 | ||||

| Eröffnet am: | 20.02.07 18:46 | von: Anti Lemmin. | Anzahl Beiträge: | 157.419 |

| Neuester Beitrag: | 06.07.25 13:32 | von: Frieda Friedl. | Leser gesamt: | 25.593.202 |

| Forum: | Börse | Leser heute: | 2.374 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 349 | 350 | | 352 | 353 | ... 6257 > | ||||

Well, excuse me. The sky has fallen. The median price of US houses has crashed from a peak of $262,600 in March to $211,700 in September. This is an 18pc drop nationwide.

Yes, the year-on-year slide is still just 4.2pc, but that will soon change as the base effect catches up.

Merrill Lynch has just confessed to a $7.9bn write down on CDO subprime debt and assorted follies, nearly double what it suggested three weeks ago.

This is what happens when a bank values its CDO debt at “mark-to-market” rather than “mark-to-myth”, as some of Merrill’s rivals are still trying to do.

Merrill’s Q3 loss of $3.5bn has cut the group’s equity capital by a fifth. This has consequences. The bank’s lending multiples will have to shrink.

In Britain, we have had the first bank run since the City of Glasgow Bank collapsed in 1878. The Fed has cut the interest rates a half point and vastly increased the pool of eligible collateral for Discount operations. The European Central Bank has injected over €400bn of liquidity in the biggest intervention since the euro was created.

Japan is in recession. Housing starts fell 23.4pc in July and 43.4pc in August.

The US dollar has fallen below parity with the Canadian Loonie for the first time since 1976, and to all-time lows on the global dollar index.

All it will take now for a full-fledged rout is a move by the Saudi and Gulf states to break their dollar pegs, which they may have to do to prevent imported US inflation causing havoc; or for the Asian banks stop buying US Treasuries – as Vietnam, Singapore, Korea, and Taiwan, have gingerly begun to do.

And for good measure, the Bank of England has just warned in its Financial Stability Report that lenders are still in serious trouble, that there is a risk of commercial property crash, and that equities are “particularly vulnerable” to a downturn. It is said there may well be a repeat of the summer crisis, “potentially on an even larger scale.”

What more do you want?

It is true that stock markets have once again decoupled from the realities of the debt markets. But they did this in the early summer, when the Bear Stearns debacle was already well under way. They caught up famously in August.

Nobody I talk to in the City credit trenches believes for one moment that the crunch is safely over. Indeed, they think that we are edging back to extreme stress levels, and the longer it goes on, the worse the damage.

Yes, Blue Chip companies can borrow money, but most of them don’t need to do so because they have bloated cash reserves.

Once you go down the chain, the picture changes fast. The iTraxx Crossover index measuring spreads on mid to low-grade corporate debt has jumped 100 basis points or so in the last week to around 360. It costs companies 1.8pc more to borrow than it did in the halcyon days of the credit bubble in February, if they can borrow at all.

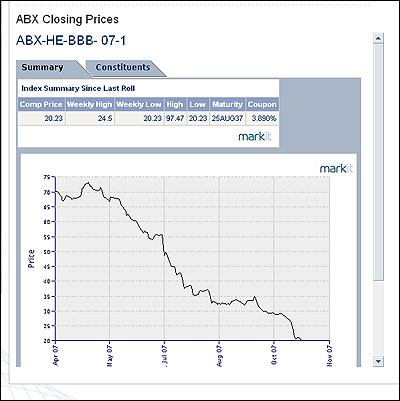

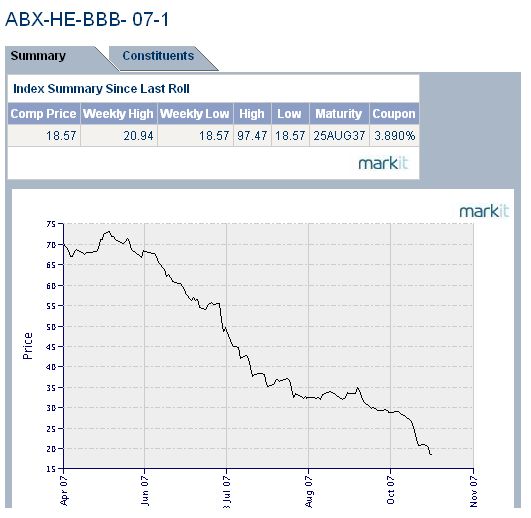

The ABX indexes measuring subprime debt – those infamous CDO packages of mortgages sliced and diced, and sold to German pension funds and Japanese insurers with a lot of lipstick -- are still falling to record lows. As Goldman Sachs strategist Peter Berezin put it: “It’s the summer that won’t end,”

“We continue to learn that it pays to respect the sell-offs in ABX and housing-related credit. This has elements of the February and August sell-offs, where credit markets signalled problems,” he said.

From a par of 100, these indexes have fallen to (depending on the vintage):

AAA grade: 90

AA: 64

A 33

BBB 21

This means that the toxic BBB tier has lost almost four fifths of its value. Even the AA has lost a third.

Now, remember that the total stock of subprime and Alt-A (close kin) debt issued from early 2005 to early 2007 amounts to $2 trillion. Ben Bernanke’s estimate that losses would be $100bn looks wildly optimistic.

Not to labour the point, but three-month Euribor rates are still at 62 basis points over the ECB’s 4pc rate. This amounts to a de facto half point rise since the crunch for all those in the euro-zone with floating mortgage rates – 98pc of the total in Spain, the biggest property bubble of them all.

Asset-backed security (ABS) issuance peaked at €78bn in March, fell to €52bn in July, €9.8bn in August, €5.6bn in September, and €2.5bn in October. It has died. Banks no longer dare to hawk the stuff of fear of a humiliating rebuff.

As for asset-backed commercial paper in the US, it has contracted every week since August as the lenders refuse to roll over short-term loans. Roughly 25pc of the market has been closed down, cutting off almost $300bn of funding for SIVs.

These SIVs (structured investment vehicles) are `conduits’ – in City argot – that allow banks to juice profits by speculating off books on high-risk debt. They borrow short (three to six months) to invest long (five years of so), making money on the interest arbitrage. Until the game blows up, of course.

Some $370bn still needs to be rolled over, and there lies the rub. The strong suspicion is that Hank Paulson’s $75bn SIV rescue for the big four US banks is intended to cover up the problem by feeding out losses slowly, rather than allowing firesales to cause a cascade.

As the Bank of England warned, the Super-Siv should not be used to prop up fictitious valuations.

“It stinks, as does the Treasury’s sponsorship of the scheme. It seems designed to prevent price discovery.”” says Bernard Connolly, global strategist for Banque AIG.

Connolly says it resembles the slippery practices at the start of the Bear Stearns debacle, when creditors quickly abandoned attempts to force CDO sales by the Bear Stearns hedge funds as soon as they realized that prices were collapsing – exposing the awful truth that hundreds of billions were falsely valued on books.

Nauseating though Paulson’s MLEV -- `Master Liquidity Enhancement Conduit’ – may be, it probably has to be done.

Connolly says the Fed-led pack of central banks have made such a mess of capitalism by blowing credit bubbles (with low rates in the late 1990s and 2003-2006) that they now have no alternative other than to relaunch the “Ponzi Scheme”, or risk depression.

This will have political consequences, of course. “The looming threat on the horizon, or just over it, is that the socialization of risk will be accompanied, in many countries, by the socialization of wealth,” he said.

Indeed. The investors now baying for bail-outs had better be careful what they wish for. Democracy will have its way of making them pay. One recalls the 98pc tax rate on dividends in Britain in the late 1970s. Haircut now, or haircut later.

In any case, the Paulson Super-Siv has failed to calm the horses. “This rescue has back-fired. The central banks don’t want anything to do with it. There is a fear that the big four US banks are trying to hide their debts,” said Hans Redeker, currency chief at BNP Paribas.

The DOW is down 500 points or so since peaking in early October, and it looks wobbly.

Even so, equities have not begun to reflect the reality that the 2006-2007 credit bubble has popped and cannot be easily reflated at a time of stubborn, lingering inflation. Spare me the mantra that the “fundamentals” are sound. Credit is the ultimate fundamental.

Woe betide Wall Street if the Fed fails to slash rates dramatically over the Winter, starting on October 31.

Woe betide the dollar if it does.http://blogs.telegraph.co.uk/business/...chard/oct07/skyhasfallen.htm

Angehängte Grafik:

abx.jpg

abx.jpg

igendein tropfen sprengt das fass und wahrscheinlich eine nichtigkeit, denn wenn ich allein die heutigen negativen nachrichten mit den kursen vergleiche ?????

es gibt nur eine aktie wo das negative richtig eingeschlagen hat und die ist aus der Solarbranche

__________________________________________________

auf unserem Planeten gibt es nur Propheten

Experten der Researchabteilung des US-Bankenhauses heute ihre Bewertung für den US-Finanzsektor von „market weight“ auf „underweight“ gesenkt. Es werde im Finanzsektor im Zuge der Kreditkrise weiteren Abschreibungsbedarf geben,

und die Finanztitel im DOW ????

__________________________________________________

auf unserem Planeten gibt es nur Propheten

Haussen sterben nie wie hier angenommen im Jammer sondern im Glückstaumel und hohem KGV.

Erreicht der Dax hier seinen langfristigen Durchschnitt bei 15,5 steht er über 9000.

Ein Schmankerl für Bullen bleibt, dass in Endphasen eines Börsenbooms die Bewertungen explodiern, das seh ich, von Einzelfällen abgesehn, nirgends...

Optionen

| Boardmail an "lehna" |

Wertpapier: S&P 500 |

Offenbar scheint die Fed und Bernanke für die Marktteilnehmer ja auch mittlerweile so eine Art Vollkasko-Versicherung gegen Crashs zu sein.

Na ja, auf die Höhe der Versicherungsprämie darf man gespannt sein, nichts ist umsonst ;-)

b) Außerdem entscheiden an den Märkten die Großanleger und nicht irgendwelche glückstaumeligen Kleinanleger. Und die entscheidenden Player, das sind halt mittlerweile Pensionsfonds, Versicherungen, Hedge-Fonds, die asiatischen Zentralbanken, Petrodollar- Anleger und Beteiligungsunternehmen. Wenn man sich überlegt, dass allein die People"s Bank of China und die Bank of Japan über 2.000 Milliarden Dollar verwalten, wird sehr schnell klar, woher der Wind an den Aktienmärkten weht, auch in Deutschland.

http://www.ariva.de/...schild_Theorie_t283343?pnr=3680315#jump3680315

Ich bin nur der Überzeugung, dass wir keine RALLY mehr sehen werden.

Die Cleveren werden bei Erreichen der bisherigen Highs immer wieder genug sellen.

Die haben ja schon die Hose voll wegen ihren dicken Dingern, die sie seit der Kreditkriese mit in ihren Büchern rumschleppen.

Wer jedoch der Meinung ist, dass die kritischen Hinweise auf die Risiken nützlich sind, der mag hier weiterlesen.

The Spreading Contagion

The credit crisis is continuing to spread while the housing situation looks more and more like a bottomless pit. At the same time evidence keeps accumulating that shows the malaise spreading to the rest of the economy.

This week Merrill Lynch wrote off $8.2 billion in assets and the word on the Street is that there is more to come. Just a few weeks ago Merrill estimated the write-down at $5 billion. The firm says that the new number is not the result of any newly-found bad assets, but a judgment call on what discount to take from the original valuations. The huge disparity therefore either indicates the wide degree of latitude various financial institutions have in determining the amount of write-downs to take or, on the other hand, indicates a deterioration of perceived value over the last few weeks. Either way, it makes us wonder how many more write-downs are in store for companies that have already taken one write-down and how many other institutions have yet to take their first one.

At the same time it is still unclear whether the Treasury-sponsored SIV rescue plan will do any good and whether it will it even be implemented. On the surface it looks like a temporary holding action aimed at keeping the assets off the books and preventing a showing of their real values. Already a number of prominent voices such as Buffet and Greenspan have expressed their doubts. Since the plan was announced it has become even more apparent that the SIVs are a global problem. Tango Finance, one of the world’s largest SUVs, is selling assets. The firm had assets of $14 billion in July. Chyne Finance with assets of $6.6 billion said it may have trouble paying its debts. Rhinebridge ($2.2 billion), run by IKB Deutsche, may also not be able to pay all of its debts.

Meanwhile the continually worsening housing situation threatens to bring about even more credit problems and a hard landing for the economy. September existing home sales were down 8% for the month and 19% year-to-year with inventories soaring to a 10.5 months supply. Unlike new homes, you can’t alleviate the supply situation by halting new building—these houses are already here. With mortgage quality continuing to deteriorate and foreclosures likely to rise, a significant increase of additional houses on the market is virtually a sure thing. New home sales were up 4.8% in September, but only with the help of a sharp downward revision of August sales. Furthermore, according to NAHB chief economist David Seiders the report indicating a 38% increase in sales in the West was highly questionable. The new housing sales numbers also do not include cancellations, which ranged from 27% to 68% among seven leading home builders.

In addition the evidence that the economy is softening outside the housing sector is quite clear. September chain store sales were down 1.5% and are down over 2% since late July. A number of leading retailers have reduced their expectations including Target, Talbots and Coach. UPS reduced their estimates on the expectation of slower retail sales, and they are in a position to know. September industrial production was up only 0.1% following a flat reading in August. Over the last four months payroll employment has increased by an average of 90,000 compared to 143,000 in the prior four months. In the last two weeks initial unemployment claims has jumped to near the top the range that has been in force since mid-2006. The semiconductor manufacturers’ book-to-bill ratio is at 81, a two-year low while September orders were down 10.6%. Caterpillar surprisingly lowered its forecast, blaming widespread economic weakness. The outlook for capital expenditures is also not encouraging. New orders for durable goods ex-defense and transportation is down 5% from a year earlier while the NABE survey of business confidence is falling sharply. In addition Ward’s is reporting a sharp decline in median and heavy-duty truck sales.

Those looking for strength from abroad may also be disappointed. The German government recently cut its 2008 economic forecast, blaming a strong Euro, high oil prices and credit market turmoil. The Eurozone PMI is down sharply. The housing boom in Europe has also been cooling off significantly. Japan’s economy continues to be sluggish. Together, the U.S., the EU and Japan account for about 70% of world GDP. The other 30% have relatively low domestic consumer spending as a percent of GDP, and are heavily dependent on exports to the other 70%. In our view the global economy is far from immune to a hard landing in the U.S.

The stock market, despite its recent gyrations, has remained at an elevated level based on the widespread belief in a soft landing, continued ease by the Fed and strong global growth. In our view that belief will become as discredited as the belief that the end of the dot-com boom and the housing boom would be contained, that derivative instruments eliminated risk and that subprime loans were safe. The current market discounts nothing ahead of time and does not connect the dots. Instead it reacts to the news each day almost as if the prior day did not exist. In our view the news on the economy will get worse and the market will then react strongly on the downside.

http://www.comstockfunds.com/index.cfm/act/...rID/1333/startrow/1.htm

Beide Punkte, obwohl ironisch gemeint, kann ich unterstreichen. Fakt ist, dass die internationalen Investoren (Scheichs, Fonds und Banken) voll mit Geld sind. Und bevor sie das ganze Geld in China etc. investieren, investieren sie lieber in USA oder Europa.

Interessant ist auch, dass es einen neuen Spielball gibt: Öl! Genau so wie die Aktienkurse, Metallpreise, Commodities etc. wird der Öl-Preis auf bisher nicht vorstellbare Höhen getrieben.

Henry Paulson presses for aid to sub-prime lenders

Suzy Jagger in New York

Henry Paulson, the US Treasury Secretary, is seeking to persuade the White House to offer financial compensation to American mortgage lenders that try to help troubled homeowners by renegotiating the terms of their loans.

The Times has learnt that Mr Paulson is lobbying President Bush to provide funds so that mortgage lenders can reduce the loss that they would incur from either reducing the rate of an adjustable home loan or extending the life of the mortgage to make it cheaper for the property owner.

It is understood that Mr Paulson’s proposals are meeting significant resistance within Washington, where it is perceived that such a move would be a bank bail-out scheme.

Washington is nervous about being seen to be preventing Wall Street companies from having to face the financial implications of their own lax lending practices and ill-judged investment decisions.

America is suffering its worst housing recession for 16 years. Mortgage arrears and foreclosures have soared as homeowners have struggled to keep up with their mortgage repayments.

A number of those homeowners — who typically have low incomes and poor credit histories — took out sub-prime mortgages that begin with a low introductory interest rate but which increase in their cost throughout the life of the loan.

Sub-prime borrowers bet that by the time the interest rate rises, the value of their home will have appreciated sufficiently to allow them to remortgage. Unfortunately, the housing slowdown has seen some states suffer house price falls of 40 per cent.

In the summer, President Bush sought to avert a deepening mortgage crisis and reduce the number of Americans who faced losing their homes. He urged mortgage lenders to contact borrowers and try to renegotiate the terms of their mortgages.

Earlier this week, Countrywide, America’s biggest mortgage lender, said it would begin contacting borrowers and modify $16 billion (£7.8 billion) worth of home loans whose interest rate will reset by the end of 2008.

David Sambol, Countrywide president and chief operating officer, said: “We are determined to assist borrowers who have the willingness and wherewithal to remain in their homes but need a little help to do it.”

It is expected that other mortgage lenders will follow suit, even though the cost of negotiating the terms of sub-prime mortgages will eat into their profits.

It is understood that Mr Paulson wants to offer the lenders compensation to offset these losses.

Chris Whalen, of Institutional Risk Analytics, said: “Paulson can’t go there. Paulson wouldn’t just be trying to help the banks, he would be trying to help the dealers, Wall Street as a whole. Ultimately, it’s the investors who take the hit.”

Mr Whalen added: “It is wrong for the Government to try to mandate loan modification. It sounds brutal, but a lot of these families should not have got mortgages in the first place. They couldn’t afford them. Modifying the loan in a number of cases won’t work. Historically, 30 to 40 per cent of borrowers whose loans are modified default again.”

The US Treasury and Countrywide failed to return calls yesterday

http://business.timesonline.co.uk/tol/business/.../article2741522.ece

ich zu 70 prozent in gold und goldminen investiert bin.

das geht schön nach oben und wird den indizes die lange nase zeigen.

echtes geld gegen spielgeld eben!

und nur das echte ist mir gut genug, auch wenn die indizes nochmal richtig auftrumpfen sollten, bevor sie verglühen. in der asche wird das gold immer noch als gold zu finden sein.

diesistkeineaufforderungzuirgendetwas

Optionen

| Boardmail an "louisaner" |

Wertpapier: S&P 500 |

Wer das gleiche mit dem Hebel 5 gemacht hat, ist de facto pleite. Konkret: Wer im Januar 100 Dollar hatte und auf Kredit für 500 Dollar BBB-Shit kaufte, hat jetzt einen Depotwert von Null.

Horrend, dass z. B. die drei faulen Bear-Stears-Hedgefunds Hebel von 20 hatten. (dshalb mussten sie auch als Erste dran glauben). Die IKB hat aber vermutlich ähnlich hohe Hebel. Richtig lustig wird es, wenn Banken wie die IKB nun beginnen, ihre Subprime-Assets tatsächlich zu Marktbedingungen zu verkaufen. Noch ist nämlich der ganze Mist im Depot, lediglich durch Bürgschaften anderer gesichert...

Der Super-Rettungs-"Bail-out-everbody"-100-Milliarden-Fond von Paulson kann daher als der letzte Versuch betrachtet werden, den sinkenden Housing-Tanker noch einmal mit Geld zu floaten.

Herr, erlöse mich von meinen Schulden,

ob prime oder subprime,

Dein Wille geschehe,

im Himmel wie in der Chart-Hölle.

Angehängte Grafik:

screen_00230.jpg (verkleinert auf 96%)

screen_00230.jpg (verkleinert auf 96%)

Optionen

| Boardmail an "Börsenfan" |

Wertpapier: S&P 500 |

http://www.ariva.de/Der_Doomsday_Baeren_Thread_t245194

Da es eine Teillöschung des Eingangspostings gab, haben wir hier weitergemacht - und dabei auch klargestellt, dass es nun vorwiegend um Probleme in USA gehen soll (siehe Eingangsposting dieses Threads). Sie sind inzwischen weitgehend eingetreten. Fehlt nur noch, dass die US-Indizes fallen. Aber was nicht ist, kann ja noch werden ;-))

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

Aber, wie Charttechniker ja nicht müde werden zu belehren: Der Markt hat immer Recht - auch wenn es zur Abwechselung mal nach unten geht ;-))

Danke an relaxed, der diesen Artikel als Link gepostet hat. Da er wichtig ist, poste ich ihn hier noch mal komplett:

Valuing mortgage bonds: Don't ask, don't tell

Hedge fund guru David Einhorn says a lot of people are afraid to offload their mortgage-backed investments for fear of discovering what they're really worth. Fortune's Carol Loomis reports.

FORTUNE Magazine

By Carol J. Loomis, Fortune senior editor at large

October 23 2007: 3:41 PM EDT

(Fortune) -- Ever hear of a 20/90 bond? According to David Einhorn, head of hedge fund Greenlight Capital, that's a security for which would-be buyers are bidding 20 (that is, $200) and would-be sellers are offering 90 ($900).

Einhorn is talking tongue-in-cheek, of course, but in today's credit markets, he's on the rim of reality. Rafts of investors who own mortgage-backed securities aren't willing to put them up for sale, for fear of finding out what prices truly are.

"So the fear," says Einhorn, "is that the new prices are actually disclosed." He calls that the "don't ask, don't tell" method of security valuation.

Einhorn, 38, spelled out his criticisms at a speech sponsored last week by Columbia Business School's Heilbrun Center for Graham and Dodd Investing. His 11-year-old fund, Greenlight, manages $5 billion in assets and has had average annual percentage gains that he says are in "the mid-20s."

The price of everything, in flux

Einhorn is labeled a value investor, though he's also known as a short seller. In fact, he implicitly suggested in his speech that one of his current short positions is Moody's, the securities-rating agency. Moody's and Standard & Poor's, the ratings arm of McGraw-Hill (Charts, Fortune 500), have recently been accused of contributing to the credit crisis by putting high-grade ratings on fixed-income securities that didn't deserve them.

At the heart of today's crisis, Einhorn said, is that lenders have lent too much money without demanding sufficient compensation. The problem, he said, goes far beyond that ballyhooed villain, subprime: "There has been a colossal undercharging for credit across the board." The sins, he said, extend to prime mortgage loans, commercial real estate, and corporate lending.

"The only difference between these areas and subprime residential is that we haven't seen the losses yet," says Einhorn. That makes him marvel at "how fast the world is trying to go back to business as usual."

Ich möchte mal an dieser Stelle mal ausdrücklich Roland Leuschel zitieren der da meint:

Wenn jemand den Mut hat, angesichts all dieser Tatsachen sein Vermögen in eigene Hände zu nehmen und zu verwalten, dann sollte er alte, erprobte Grundsätze nicht vergessen. Einer dieser Grundsätze stammt von den Rothschilds: Verkaufe, wenn die Violinen in den Strassen spielen und kaufe, wenn die Kanonen auf den Schlachtfeldern donnern. Ein Crash an der Aktienbörse kommt immer unverhofft. :-(( Wenn also im Moment die Aktienkurse weltweit auf dem Höhepunkt sind, und es keinen Crashpropheten mehr gibt, dann sollte der Anleger nachdenklich werden... und entsprechend handeln.

Wer im Januar 100 Dollar hatte und auf Kredit für 500 Dollar BBB-Shit kaufte, hat jetzt einen Depotwert von Null.

Nö, der hat jetzt 300$ Schulden, denn die 500$ Kredit haben sich ja nicht gefünftelt;o)

Merrill Lynch schloss das dritte Quartal 2007 mit einem Verlust von 2,2 Mrd. USD ab. Grund für diesen ersten Verlust seit sechs Jahren waren Wertberichtigungen auf Schuldverschreibungen – überwiegend auf Basis verbriefter US-Hypotheken – in Höhe von 7,9 Mrd. USD.

Merrill Lynch gehört zu den größten US-Investmentbanken. Daher war das Haus auch traditionell stark bei aktivabasierten Wertpapieren (ABS-Emissionen) engagiert und hielt als Marktführer bei forderungsgedeckten Emissionen – so genannten CDOs (Collateralised Debt Obligations) – ein umfangreiches Portfolio dieser Papiere. Zur Strukturierung von CDOs hatte Merrill Hypotheken ausgereicht bzw. Hypothekenforderungen angekauft und diese Forderungen verbrieft. Zur Platzierung bei Anlegern wurden die CDOs in Tranchen unterschiedlicher Bonität aufgeteilt – die Tranchen mit den schwächsten Ratings waren mit hohen Kupons ausgestattet, während die qualitativ hochwertigsten AAA-Tranchen deutlich niedriger verzinst wurden.

Dieser Strukturierungsprozess war einer der Gründe dafür, dass Merrill permanent umfangreiche Eigenbestände dieser Papiere hielt – nach Eintritt der Subprime-Krise war ein erheblicher Teil dieser Bestände unverkäuflich, und waren zudem noch zu pari oder knapp darunter bewertet. Natürlich war Merrill Lynch nicht der einzige Marktteilnehmer, der sich diesem Problem ausgesetzt sah – aber einer der größten.

Zwischenzeitlich hat Merrill Lynch sein CDO-Engagement von 32 Mrd. USD im Juni auf aktuell 15 Mrd. USD reduziert. Teilweise wurde dies durch massive Abschreibungen im Gesamtvolumen von 7,9 Mrd. USD erreicht, mit denen die Bewertung der Bestände auf 60-70 % korrigiert wurde. Diese aus gegenwärtiger Sicht konservative Bewertung eröffnet Potenzial für die Realisierung von Gewinnen bei einer eventuellen Veräußerung von Beständen.

Sollte sich die Subprime-Krise weiter verschärfen, könnte sich jedoch selbst die vorgenommene Wertberichtigung als unzureichend erweisen. Eine exakte Prognose ist kaum möglich: Sofern sich die Lage im Subprime-Markt nicht weiter erheblich verschärft, ist die Wertberichtigung als Einmaleffekt zu sehen, den Merrill durchaus verkraften kann. Hiermit sollten auch die absehbaren Risiken abgedeckt und ein systematisches Risiko für den Finanzsektor abgewendet sein – diese Einschätzung wird auch vom Aktienmarkt geteilt.

Das Rating von Fitch:

Die amerikanische Ratingagentur Fitch hat ihre Bewertung für die US-Investmentbank Merrill Lynch & Co. Inc. (ISIN US5901881087/ WKN 852935) und ihre Tochtergesellschaften abgesenkt....

Das Rating von Moodys:

Nach Fitch hat mit Moody’s Investors Service eine weitere Ratingagentur ihr Rating für die US-Investmentbank Merrill Lynch & Co. Inc. (ISIN US5901881087/ WKN 852935) gesenkt.

Wie die Tochtergesellschaft der Moody's Corp. (ISIN US6153691059/ WKN 915246) mitteilte, wird das Rating für langfristige Verbindlichkeiten von Aa3 auf A1 gesenkt. Als Grund für die Anhebung gab Moody’s die verbesserten Ergebnisse und Verschuldung an. Außerdem gab Moody’s einen negativen Ausblick.

Und die Reaktion:

Angehängte Grafik:

mer.jpg

mer.jpg

Noch Ende vergangener Woche hatte Thomson ein geringeres Minus von 0,1 Prozent prognostiziert, Anfang Oktober wurde sogar ein Plus von 3,6 Prozent erwartet. Selbst dieser Wert hätte eine starke Abschwächung bedeutet: Im zweiten Quartal hatten die Unternehmen des S&P 500 einen Gewinnzuwachs von 7,7 Prozent geschafft, im ersten Quartal waren es 7,9 Prozent. Davor hatte es eine lange Serie von 14 Quartalen mit jeweils zweistelligen Gewinnzuwächsen gegeben.

Kreditausfälle sorgen für Vertrauenskrise

Klares Schlusslicht der Quartalssaison ist der Finanzsektor, für den Thomson nun ein Gewinnminus von 16 Prozent erwartet. Ende vergangener Woche lag die Prognose noch bei minus 11 Prozent. In den Zahlen der Banken hat sich die Krise in den Hypotheken- und Kreditmärkten voll niedergeschlagen......

http://www.faz.net/s/...D386EDDC8F113B609E~ATpl~Ecommon~Scontent.html

Und auch schon eingepreist, sagen zumindest die einschlägigen Kommentatoren.

Gestern haben sich die US-Banktitel deutlich erholt, alles wird gut. ;-)

Ich weiß nicht, ob zur Zeit die Violinen spielen oder die Kanonen donnern. Ich sehe nur, dass es die momentane Strategie ist, Probleme nicht bewerten zu wollen, in der Hoffnung, dass sie nach Halloween mit der Zeit von selbst verschwinden. Vielleicht ist diese Strategie erfolgreich.

Doch sollten die Probleme realisiert werden, dann ist die Liquidität weg und es gibt nur noch eine Richtung.

Wenn ich Geld brauche, dann verkaufe ich - übrigens auch Gold, Energie und andere Rohstoffe. ;-)

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

Gold, often seen as a hedge against oil-led inflation and traditionally deemed a safe-haven asset, was gradually advancing towards the next big target of $800 an ounce while the dollar struggled to find a solid base.

A series of disappointing U.S. economic data has fuelled near-universal expectation that the U.S. Federal Reserve will cut interest rates by at least 25 basis points at its meeting next week -- a negative factor for the dollar and good for gold.

"The deteriorating economic picture is manifesting itself in a weaker dollar and that's helping gold. Oil is also looking strong. We are getting close enough to $800," said John Reade, head of metals strategy at UBS Investment Bank.

"The danger of a correction is still there but you are going to need a trigger for it," he said......http://www.reuters.com/article/marketsNews/...2641938820071026?rpc=44

"She basically said they can't exclude the possibility that growth in the Baltic's will go down to zero next year," said the analyst, "The market is starting to getting very worried about a melt down in the Baltic area next year, a real credit crunch with significant credit losses".

SEB is heavily exposed to the three Baltic States of Estonia, Latvia and Lithuania where record growth, particularly since membership of the EU in 2004, has helped propel its income and profits. However fears of overheating economies, debt levels, and a looming property price correction have been troubling the market this year. The analyst said Falkengren's comments seem to confirm people's worst fears. "We had something similar in Sweden in the early 1990's and as I sit here now re-doing my figures for the Baltics I am now factoring in something similar to that in the Baltics going forward. It's as bad as that", said the analyst. The analyst said he is awaiting further comment for SEB on the Baltics at its analyst conference call this afternoon. http://www.sharewatch.com/story.php?storynumber=69431

http://au.biz.yahoo.com/071025/36/1ghdm.html

.....After the central banks stepped up to bail out the markets and the details of the super conduit fund have emerged, many financial instruments returned to their pre-credit crunch norms. Volatility in equities, debt and currencies dropped significantly while implied volatility in the carry trade has fallen back to levels comparable to the 2005/2006 lows. The benchmark stock indices have similarly settled from their extreme down days of August. And, as volatility has been ushered out, bullish sentiment quickly returned. The FTSE 100 and Nikkei have rebound from multi-month lows to climb back towards their cycle highs, while the Dow Jones Industrial Average has actually moved on to set a new record. The carry trade has received similar reprieve as EURJPY and the other yen crosses have recovered a majority of their lost ground.

Problems beneath the surface:

However, though investor sentiment seems to be on the rebound and many of the popular investments have returned in strength, many problems are still floating just below the surface and officials and traders are just now starting to appreciate their possible long term consequences of the fallout. One glaring sign that the credit crunch has merely gone into hibernation is the big hit to earnings the major US banks reported over the third quarter. Credit Suisse reported a $1.56 billion and $1.35 billion write off on subprime and leverage debt losses. UBS wrote a $3.42 billion hit from mortgage backed securities off its books. Perhaps the most shocking so far, Merrill Lynch announced a write down of $7.9 billion in losses from subprime loans and collateral debt obligations (CDOs). Even Goldman Sachs, the premier bank on Wall Street, who reportedly had a positive quarter, saw most of its profit in unrealized gains while ‘hard-to-value’ assets were pushed to the background. Despite the mark downs on the books, it is still not clear whether further losses will carry over to the fourth quarter. What’s more, the depressive impact on lending is already evident in other areas of the financial services group and even in other sectors.

Another problem that has received greater media attention recently is the existence of SIVs in money market funds. Typically considered one of the safest and most liquid areas for investment, a number of these funds have admitted to investing in the same ‘high-finance’ derivatives built on subprime loans that have cut into banks’ earnings. A report by The Wall Street Journal suggests a number of major money market mutual funds run by names like Credit Suisse Asset Management, Bank of America and Federated Investors were holding 10 to 20 percent of their total portfolios in SIV created debt. Should there be another sudden run for the doors in the credit market, even the most liquid assets may come under fire and a run on the money market finds could be the 21st century equivalent of a run on the banks.

Finally, taking the credit crisis full circle, the next global market shock may find its epicenter in the US housing market. After so many hedge funds and banks have reported crippling losses from subprime and other mortgage backed securities, there are still a substantial number of mortgages that may fall into default in the near future. This looming danger exists because many of the mortgages taken out during the boom years of US growth from 2002 to 2007 were adjustable rate mortgages (ARMs) that were initially set with a low ‘teaser’ rate and will later reset to an interest rate based on the prime rate at the time of adjustment. A record $50 billion worth of these loans are set to adjust in October alone and an estimated 2 million homeowners with ARMs are expected to be reset by the end of 2008. The latter statistic is particularly concerning considering 80 percent of those carrying ARMs deemed ‘current’ on their payments only make the minimum payments. The rate adjustment or perhaps a drop in income could easily push thousands more into default. As it stands, the Federal Housing Administration expected a quarter of the 2 million owners set for adjustment to be forced into foreclosure.

Taking all these potential problems into consideration, what is the presumed impact on the currency market? First of all, should any one of these looming threats trigger another flight from risk and threaten financial markets and growth, the Federal Open Market Committee would likely step in with additional, potentially large cuts to the Federal Funds rate. While the immediate impact of yet another wave of risk liquidation would actually be positive for the dollar as the carry trades unwind, the long term consequences are likely to be dire. With the greenback already pushing record lows on a trade-weighted basis, the currency could continue to ratchet new lows against its major counterparts as interest rate differentials compress further. A run on the dollar could easily lift EURUSD to 1.4500, GBPUSD to 2.1000, and carry USDJPY down to 110.00. The USDJPY pair, once the preeminent carry trade vehicle, is already showing signs that the dollar is loosing its clout. While the greenback still enjoys a considerable 4.25 percent yield advantage over the yen, the pair has gotten nowhere near its former swing high at 124.00 in the rebound from mid-August lows as traders worry about further US rate cuts. Taking a much longer-term outlook on a second round credit crunch, the US wouldn’t be the only economy to feel the impact. The waning demand from the US economy for goods from countries like Japan, China and UK, among others, would slow global growth and could ultimately mark a bottom for the greenback. In the meantime, however, the buck could be in for more pain.