Trina Solar - Die strahlende Perle

Optionen

| Boardmail an "cango2011" |

Wertpapier: Trina Solar |

Optionen

| Boardmail an "-Sille-" |

Wertpapier: Trina Solar |

Optionen

| Boardmail an "-Sille-" |

Wertpapier: Trina Solar |

Optionen

| Boardmail an "-Sille-" |

Wertpapier: Trina Solar |

dann kann es ja heute an die 13 Euro gehen. Baut die Welt zu mit Trina Solar!!!!!!!!!!!!!!!!!!

Dann kann ich ja noch von einem genussvollem Ruhestand träumen!!!!!

Optionen

| Boardmail an "goldfinger45" |

Wertpapier: Trina Solar |

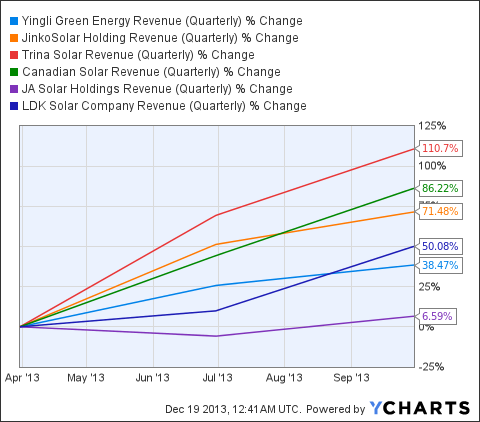

http://seekingalpha.com/article/...51-chinese-solar-manufacturer-pick

und daraus ein interessanter Chart

....Let's look at just the last one year:s.chart unten

it looks like 2011 and 2012 were really bad years for all the solar manufacturers and 2013 looks like the year where, maybe, things are turning around.

The Numbers

§Market Cap Debt Debt/Equity

Yingli $812M $2.5B 5.4

Jinko $789M $875M 2.9

Trina $985M $1.1B 1.3

Canadian $1.47B $992M 2.5

JA $369M $613M 0.87

interessant,dass Trina wohl am geringsten verschuldet ist

Angehängte Grafik:

last_year.png

last_year.png

http://seekingalpha.com/article/...l_macro_view_edi_pic_0_0&ifp=0

http://www.aastocks.com/EN/IPO/IPOCalendar.aspx

http://www.bloomberg.com/news/2014-01-08/...f-government-support.html

What Trina Solar is doing right

1) Top global solar panel supplier - Trina Solar is one of the biggest suppliers of solar panels in the world, having ~8-9% global market share in 2013 with shipments of ~2.6 GW for the whole year. The company had lost some market share in 2012, as it missed shipment forecasts due to a global glut in solar panel supply. The company has made a roaring come back in the last couple of quarters, with shipments for 2013 being just ~20% short than that of the No.1 solar panel supplier.

For the fourth quarter of 2013, we expect our shipments to be between 660 megawatt to 690 megawatts and overall gross margin to be in the middle teens in the percentage terms. We also revised our guidance for total PV module and system deliveries upwards to between 2.58 gigawatts and 2.62 gigawatts for the full year of 2013.

Source - Trina Solar Q3 Conference Call

2) Entry into Solar Development - Trina Solar is following its successful compatriot Canadian Solar (CSIQ) into the solar plant development business. The company plans to develop 100-200 MW of solar plants per quarter. The gross margins for solar plants these days are typically higher than that from the sale of solar modules. Canadian Solar, SunPower and First Solar (FSLR) have managed to generate higher margins through their solar system installation and development business. TSL recently signed a deal to develop 1000 MW with a local Chinese government.

3) Well Capitalized - Trina Solar has always managed its capital conservatively, being prudent in its capacity expansion. The company has got a total debt of $1.1 billion with net cash of $550 million. TSL has got one of the lowest debt to equity ratios in the solar industry.

4) Strong Chinese government support - Trina Solar is one of the largest solar companies in China and has got strong government backing. The Chinese government is being very selective in supporting renewable energy companies and is removing capital support for the smaller companies with uncompetitive factories. Suntech (STP) has already been referred to the bankruptcy court. Trina Solar will benefit from this cull, removing a lot of capacity from the solar panel market which were selling below cost.

5) Margin improvement - Trina Solar's margins have improved quite substantially in the last couple of quarters. Trina Solar reported a gross margin of 15.2% in the last quarter and also a small net profit. The gross margin of 15% is one of the highest amongst solar panel makers. Both the shipments and margins have been improving for TSL. The company has also reduced its processing costs for solar modules to ~40/c watt, making it one of the most competitive in the industry.

Yeah. Let me repeat because where we $0.45 for process cost is not correct in given number. So when we our process cost we only calculate and for our in-house production cost and the conversion cost which that's we typically do the vertically integrated from ingots, wafer and cell module and that area will be approximately under $0.40 already.

But I'm saying that with cost of sold per watt basis is $0.54 and we have approximately about $0.10 in poly, so we have some outsourcing couple of cents more. So that's you add up that's a $0.54.

So going forward, I think that we do have a room to reduce our cost of non-poly and poly but poly is kind of a stabilize. Non Poly we do have a room to continually improve our efficiency and both in the efficiency and sale at module level but also in productivity and given that excellency of operation in our product line.

6) Strong industry demand in 2014 - Most analysts and research houses expect that solar demand will range in between 40-50 GW in 2014, which will be a big increase from the ~35 GW demand expected in 2013. This will imply that solar panel prices will remain flat at worst and might increase substantially at best. Both the scenarios should allow TSL to keep its margins intact.

Trina Solar Risks

a) Chinese and Japanese Growth slows down - China will account for almost 25-30% of the global demand in 2014, as the Chinese government accelerates the pace of solar development with a target of 35 GW by 2015. Japan is also set to become the second biggest demand driver due to a very favorable feed in tariff policy. Any policy reversals in these two countries can result in panel prices going down due to overcapacity.

b) Upstream Price Increases - The increase in solar panel prices has not resulted in a concurrent increase in upstream solar material prices. The prices of solar wafers and polysilicon have remained subdued for most of 2013. However, as the demand increases I expect the upstream material prices will start to rise again, which could lead to margin compression for the solar panel producers.

c) More US duties on Chinese solar imports - Troubled German solar panel company Solarworld, is petitioning the US government to impose more stringent duties on imports of solar products from China. USA and China are already at loggerheads, with the US government imposing duties on Chinese made solar products last year. China has imposed tit for tat duties on the US made polysilicon, leading to job losses amongst polysilicon companies such as REC and Hemlock. USA accounted for roughly ~12% of the global demand.

Stock Performance

Trina Solar has shown a strong performance in the last one year, as the solar industry fundamentals have improved. The company's stock has surged by almost 200% in the last one year, though it remains below that of leading performers such as SolarCity, SunPower and JinkoSolar.

The company's valuation multiple at 0.7x remains well below that of SunPower (P/S ratio of 1.7x) and SolarCity (26.7x) and has room to expand, as the company continues to execute well during the current year. The company's stock is trading at ~$15, which is far below its all time peak price.

Summary

Trina Solar was one of the best run solar companies during the last solar boom phase, regularly beating expectations on both the top line and bottom line. The company lost market share during 2012, but came back strongly in 2013. Solar demand is increasing in almost all parts of the world, as solar electricity prices become more and more competitive with the fossil fuel generated electricity. Trina Solar will also benefit from its entry into the solar development market, as China looks to develop ~10 GW of solar power each year. I would look to buy Trina Solar on dips due to the company's cheap valuation, strong industry demand and improving execution.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

http://m.seekingalpha.com/article/1934221

Optionen

| Boardmail an "-Sille-" |

Wertpapier: Trina Solar |

http://seekingalpha.com/article/...e-chinese-solar-boom?source=nasdaq

Optionen

| Boardmail an "goldfinger45" |

Wertpapier: Trina Solar |

Jinko+Yingli ist mir bekannt....

Optionen

| Boardmail an "Benz 2" |

Wertpapier: Trina Solar |

Optionen

| Boardmail an "-Sille-" |

Wertpapier: Trina Solar |

Optionen

| Boardmail an "-Sille-" |

Wertpapier: Trina Solar |

Solar shares outperformed in 2013 largely due to short covering and day traders, says Deutsche. But as global demand diversifies and new business models arise, the broker expects this year’s outperformance to be driven by long-only investors.

Solar stocks have historically traded at a big discount to the market due to concerns about low entry barriers, low margin manufacturing businesses and high reliance on government subsidies. We believe evidence of more sustainable, diverse demand drivers along with emergence of new business models with high entry barriers could result in increased investor participation and valuation multiple expansion.

Shah also raised his global demand estimates:

We are raising our 2014 and 2015 demand expectations to ~46GW and ~56GW respectively. We believe upside demand surprises from the US, Japanese and Chinese markets could continue in 2014. We expect streamlined incentive programs in China, additional subsidy cut signals in end 2014, and decreasing financing constraints to act as catalysts for upside.

Tight financing in the more commoditized upstream segment means supply will be limited, which is good for margins:

We expect global project finance focus to remain skewed towards downstream as opposed to upstream, which in our view could limit capacity expansion and drive some supply tightness. We expect some tightness in the poly and wafer segments and see prices rising by ~10-20% from current levels......More importantly, we also expect availability of working capital financing from Chinese banks to remain relatively challenging which in turn means supply tightness could persist through early/mid 2015 timeframe until new greenfield/brownfield projects come on line.

http://blogs.barrons.com/emergingmarketsdaily/...-year-says-deutsche/

Optionen

| Boardmail an "goldfinger45" |

Wertpapier: Trina Solar |

Optionen

| Boardmail an "Benz 2" |

Wertpapier: Trina Solar |

Optionen

| Boardmail an "-Sille-" |

Wertpapier: Trina Solar |

Optionen

| Boardmail an "-Sille-" |

Wertpapier: Trina Solar |

VG

Taktueriker

Trina Solar has again started performing quite well in the last couple of quarters. The company's processing costs make it competitive with the lowest cost players such as JinkoSolar (JKS) and Yingli Green Energy (YGE). Trina Solar has also got relatively low valuation multiple compared to the other US solar stocks such as SunPower (SPWR) and SolarCity (SCTY). Q3 shipments of 775 MW were almost 100 MW higher than guidance, making the company amongst the top 5 global panel suppliers. Trina has a low debt equity ratio plus it is strongly supported by the Chinese government. Given that the company has started to perform well and the industry backdrop remains very strong, I would advise investors to start buying the stocks on dips.

What Trina Solar is doing right

1) Top global solar panel supplier - Trina Solar is one of the biggest suppliers of solar panels in the world, having ~8-9% global market share in 2013 with shipments of ~2.6 GW for the whole year....

The company has made a roaring come back in the last couple of quarters, with shipments for 2013 being just ~20% short than that of the No.1 solar panel supplier.

For the fourth quarter of 2013, we expect our shipments to be between 660 megawatt to 690 megawatts and overall gross margin to be in the middle teens in the percentage terms. We also revised our guidance for total PV module and system deliveries upwards to between 2.58 gigawatts and 2.62 gigawatts for the full year of 2013.

Source - Trina Solar Q3 Conference Call

2) Entry into Solar Development The company plans to develop 100-200 MW of solar plants per quarter. The gross margins for solar plants these days are typically higher than that from the sale of solar modules. Canadian Solar, SunPower and First Solar (FSLR) have managed to generate higher margins through their solar system installation and development business. TSL recently signed a deal to develop 1000 MW with a local Chinese government.

3) Well Capitalized - Trina Solar has always managed its capital conservatively, being prudent in its capacity expansion. The company has got a total debt of $1.1 billion with net cash of $550 million. TSL has got one of the lowest debt to equity ratios in the solar industry.

4) Strong Chinese government support - Trina Solar is one of the largest solar companies in China and has got strong government backing.......

5) Margin improvement - Trina Solar's margins have improved quite substantially in the last couple of quarters. Trina Solar reported a gross margin of 15.2% in the last quarter and also a small net profit. The gross margin of 15% is one of the highest amongst solar panel makers. Both the shipments and margins have been improving for TSL. The company has also reduced its processing costs for solar modules to ~40/c watt, making it one of the most competitive in the industry.....

Trina Solar Risks

a) Chinese and Japanese Growth slows down -

b)..... as the demand increases I expect the upstream material prices will start to rise again, which could lead to margin compression for the solar panel producers.

c)Solarworld Prozess in USA könnte zu höheren Zöllen führen

Trina Solar has shown a strong performance in the last one year, as the solar industry fundamentals have improved. The company's stock has surged by almost 200% in the last one year, though it remains below that of leading performers such as SolarCity, SunPower and JinkoSolar.

The company's valuation multiple at 0.7x remains well below that of SunPower (P/S ratio of 1.7x) and SolarCity (26.7x) and has room to expand, as the company continues to execute well during the current year. The company's stock is trading at ~$15, which is far below its all time peak price.

http://seekingalpha.com/article/1934221-trina-solar-time-to-buy-again

Es gibt aber wohl keinen Grund für eine grundlegende Richtungsänderung!

Optionen

| Boardmail an "deutsche_bank24" |

Wertpapier: Trina Solar |

Optionen

| Boardmail an "-Sille-" |

Wertpapier: Trina Solar |