Range Res. ist Produzent und keiner hats gemerkt

Seite 18 von 21 Neuester Beitrag: 25.04.21 00:49 | ||||

| Eröffnet am: | 08.06.10 12:44 | von: Mikrokosmos | Anzahl Beiträge: | 517 |

| Neuester Beitrag: | 25.04.21 00:49 | von: Melaniewrey. | Leser gesamt: | 104.362 |

| Forum: | Hot-Stocks | Leser heute: | 16 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 15 | 16 | 17 | | 19 | 20 | 21 > | ||||

IF YOU WANT A MULTIBAGGER, BUY THIS NOW!

No smoke and mirrors from me today.

No riddles.

If you don't understand what is going on, then you need your bloody head read.

This is the real deal people.

This stock could easily be twice the current SP in a few days.

Before you knock me..........hold off and wait and see what can happen, when everything is primed like it is right now.

JR By magicman3

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

http://petrofed.winwinhosting.net/upload/30May-01June11/1.pdf

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

Trinidad wird noch richtig Geld bringen, Georgien wird in der zweiten Jahreshälfte interessant.

Bei Kolumbien wird der ein oder andere mit neuen Zahlen konfrontiert werden...

Puntland...tick-tack....

Optionen

| Boardmail an "Mikrokosmos" |

Wertpapier: Range Resources Ltd. |

Range will ja jetzt auch onshore gehen, haben wir eigentlich die dazu gehörige Ausrüstung, oder müssen wir die erst kaufen, oder werden damit andere, die wir ja bezahlen müssen, beauftragt?

Ich frage nur, weil das ja Geld kostet, das wiederum ja irgentwo her kommen muss! und wenn wir schon bei so einem kleinen Geschäft wie PL 150Mio neue Aktien auf den Markt schmeißen müssen, wie soll denn erst das onshore Projekt von statten gehn! Wer soll die mächtige Ölplattform dahin bekommen, oder sind da welche, die man uns bereit stellt! Bin da nicht so ganz auf dem Laufenden, kann mich da mal einer aufklären? Ich sehe ja die Plattform in der Nordsee, die da ein Problem hat und alle Leute schon evakuiert sind...

Wenn das ein Flop werden sollte, ist Range dann Pleite?

Würden die enormen Kosten Range vielleicht in die Pleite drücken?

Sone Platform, was kostet die? 1 bis 2 Milliarden, oder 500Mio? Die Manschaft und die Schleppkosten, was ist damit?

Ich glaube fast, das Range sich damit übernommen hat....nur so ein Gedanke

Die Kosten liegen mE bei ca 100Mio $ für eine Bohrung - das aber nur abgeleitet von den Preisen der derzeit um die Falklands bohrend LeivErik (die Plattform zum bohren wird nur gemietet)

pleite werden wir daran also wohl nicht gehen... IMHO

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

See what you all think of this!

"good sunny and happy days from Africa

My dear Freind after weeks of speculation of the testing of the first and second zones I can confirm that testing has been conducted. Not that I need to say thanks to a nice mistake courtesy of the last ops RNS....

Still no news as to the data from these tests but rumor round the big M is its very likely to have exceeded the first one by quite a mile stone.

Multiple pay zones are now been discussed from various sources and one can only conclude the following

* they have oil not only from the first section but now of a deeper section

* they have already conducted tests to this point and are waiting for final govermet aproval

* 400mob recoverable is very likely to be the minimum case

*4 billion is likely to be the current guidance for the feild itself with upside to the deeper zones

As always hope you are well and you havnt lost too much weight

Your dear Freind

U"

By BULLBOY2010

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

Aus dem iii - DYOR!

15:01 29/03/2012 Puntland Q & A Big Gib to PL

Right before the dogs say its fake I don't really care this is being shared because its information I wanted not what I wanted you all to have so your lucky I'm sharing my questions let alone answers.

Enjoy!!!

My questions to Peter Landau!!!

As your probably aware there are lots of rumours going around at present some believable and some totally crazy. The shorters have moved in and the discussion boards are going crazy.

Can we expect an update before the end of Q1 regarding casing set upto 2700m?

Can we expect electric wireline log results over the depths of 1600m - 2700m anytime soon before drilling down to TD?

I have been trying to find out how much a barrel of oil is worth to each of the 3 companies upon any sale once a discovery has been made.

What sort of price can we expect to see per barrel of oil sold if indeed we do make a discovery? I have my own figures but can't find anything official. My guess is around $5 per barrel on sale????

Does the government have a slice of the sale of each barrel sold if any sale is agreed?

If so what percentage are they looking at taking from any sale?

Apparently HORN have said all the rumours are BS which yes I agree and we should only go by RNS which I agree. They also state they intend to sell once discoveries have been made.

Do HRN, RRL and RMP have potential buyers waiting to snap any discoveries up?

Do you have a set price per barrel of oil already agreed with these waiting predators?

His brief but to me very valuable reply!!!

Fair few questions there - I'd say update tue / wed next week - for casing and running logs - in ground value of recoverable oil would be between 3 and 7 bucks (pure guestimate) - govt get royalties and profit share from physical oil sold (not selling the project) - certainly some companies coming out of the wood work over the last few weeks and will always entertain any ballpark offers.

Cheers p By Big Gib loves alot of black

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

--------------------------------------------------

18:30 09/04/2012 Colombia

Colombia

From the RNS dated 20th March 2012

http://www.iii.co.uk/investment/...n:RRL.L&display=news&it=le

"The Company is also pleased to announce that it is has secured a 65% farm-in

opportunity (350m of 3D seismic and 2 new wells) on two highly prospective

licenses in the on shore Putamayo basin in Southern Columbia."

http://www.geomarkresearch.com/res/...rica/Colombia%20Oil%20Study.pdf

Looking at page 4 of this report it tells you a little about the location of Putamayo basin. This statement stood out to me.

"The Putumayo Basin, which lies in southern Colombia between the Eastern Cordillera

of the Andes and the Guyana-Brazilian Shield (Figure 1), is considered to be the

northern extension of the Oriente Basin of Ecuador."

So if we look to the Oriente Basin of Ecuador ....

http://sp.lyellcollection.org/content/50/1/89.abstract

Please be aware that this article is very old but shows the potential at the time.

"The Oriente Basin of Ecuador is one of the most productive of the South American Sub-Andean Basins. Cumulative production of oil to the end of 1986 was over one billion barrels, and current production stands at approximately 300 000 barrels per day. At least 20 oil fields have been discovered to date ..."

http://pubs.usgs.gov/dds/DDS-63/DDS-63.pdf

This is from 2001 but one of the paragraphs on page 2 gives you an idea.

"This is one of the major geologic provinces for which undiscovered oil and gas resources were assessed for the World Energy Assessment Project of the U.S. Geological Survey"

Below is a company that have just been awarded a licence for exploration in 2012. They are in a 50% JV with VETRA Exploration and Production Colombia S.A..

http://www.ccenergialtd.com/operations/...basin/putumayo-8-block.html

What hasn't been mentioned in our RNS of 20th March was who has the other 35%.

I have a feeling that Colombia will be BIG ... Very Big. By Shumna1

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

--------------------------------------------------

19:12 09/04/2012 Trinidad

From 12th September 2011 RNS

http://www.iii.co.uk/investment/detail/...ticle&articleid=8352610

Range is pleased to announce that the first well drilled by one of its subsidiaries, Trincan Oil Limited, in the Company's initial 21 well program in the Morne Diablo Block, onshore Trinidad, has been successfully completed with a down hole pump and pump jack having been installed with the well producing high quality 36 degree gravity oil at initial water-free test rates of approx 20 bopd. Higher rates will depend on final pump selection and depletion by offset well bores.

PLEASE NOTE THE FIGURE OF ONLY 20 BOPD

From 10th October 2011 RNS

http://www.iii.co.uk/investment/detail/...ticle&articleid=8380782

"Rig 8 is the third and last drilling rig to be introduced into the 2011 drilling program. The Company will introduce other drilling and completion rigs into the fleet to accelerate drilling and production increases early 2012."

This from TT's Ministry of Energy and Energy Affairs

http://www.energy.gov.tt/content/...dated_Bulletins_February_2012.pdf

Look on the 6th page down. PTRIN (FO) is us.

The Jan figure is 964 BOPD and in Feb that went to 999 BOPD. These are retrospective figures so we should be expecting a higher figure for March.

I would be very interested to know the following:

How many of these shallow wells have been drilled so far?

How many rigs are now in operation?

We are hoping for 1400 - 1800 BOPD so we are getting there (Obviously we are way behind PL's end of 2011 comments).

Does anyone think we will finish drilling all 21 wells before start drilling a Herrera?

Regards

S By Shumna1

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

http://www.asx.net.au/asxpdf/20120412/pdf/425kmkjwtcykgw.pdf

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

Range Resources Limited ("Range" or "the Company") is pleased to announce its

initial 21 well program continues to make significant progress with three of

the Company rigs now fully operational. The QUN 119 / QUN 120 and QUN 122 wells

have all been successfully drilled and logged and are in the process of being

brought into production. QUN 121 now has a drilled surface hole and cemented

surface casing.

The QUN 119 well was successfully completed, targeting the Lower Forest

formation. Following the successful completion, the well achieved initial

production rates of 130 bopd with production now stabilised to circa 100 bopd

under natural pressure.

The QUN 120 well was drilled to target depth (TD) of approximately 2,475 ft

targeting the Lower Forest and Upper Cruse formations. The well is scheduled

for testing in several zones with indications of 39 feet of oil pay in the

Upper Cruse formation and 47 feet of additional pay in the Lower Forest

formation. The well is targeting 120 bopd from the several zones encountered.

The QUN 121 well has cemented surface casing and will be drilled with Rig 5

(the Company's third rig into operation) to a TD of approximately 950 ft

targeting the Lower Forest formation in the coming days.

The QUN 122 well was drilled to a TD of approximately 950 ft intersecting the

Lower Forest formation. Well logs have indicated approximately 90 ft of

resistive oil sands. Production testing is currently being performed with the

well showing initial production rates of up to approximately 50 bopd under

natural pressure.

Rig 2 has moved from the QUN 120 well to the QUN 124 location and is preparing

to commence drilling shortly. Rig 1 has moved to a new location, QUN 123. Both

the QUN 123 and 124 wells will be targeting the Lower Forest sands with a TD of

approximately 950 ft and 1,300 ft respectively.

The above activity should see the operations move over 1,000 bopd in the coming

weeks.

Key Developments Moving Forward

The Company's fourth rig (#8) is set to join operations during the month

(April) and will be targeting the Middle to Lower Cruse sands to a depth of

circa 6,500ft which have the potential to produce in the range of 150-300 bopd.

Rig 8 is also capable of drilling the deep Herrera formation targets.

The remaining two medium depth rigs are scheduled to be operational by mid

year. This will see the Company utilising all of its 6 rigs in the coming

months. Of note, a further 30 personnel have recently been hired as the Company

continues to accelerate its development program.

The Company's developmental drilling program on the Morne Diablo license will

continue to look to extend the existing trends that have been confirmed by the

current drilling program. Rig's 1, 2 and 5 will drill 10-12 Lower Forest wells

in response to the excellent flow rates being achieved from that section.

Completion of each individual well is anticipated to be between 2-3 weeks with

a target initial production rate from each of circa 50-100 bopd.

3D Seismic Reprocessing

Work is nearing completion on the Company's extensive reprocessing of its 3D

seismic database in Trinidad. State-of-the-art reprocessing by Houston-based

seismic experts Geotrace will improve Range's ability to identify and image

deeper drilling targets across its Morne Diablo and South Quarry acreage,

including the prolific Herrera Formation.

The Company believes that improved imaging of its 3D dataset will help define

existing targets (with volumetrics) and lead to additional prospects. This in

turn should result in lower dry hole costs and continued growth in reserves and

production, respectively. Once data reprocessing is completed, the Company's

technical team will begin by confirming its existing portfolio of deeper

drilling targets (expected in May / June) with the first deep Herrera well

scheduled for Q3.

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

Ich frage mich nur, wie kann ein Executive Director so viel Zeit finden hunderte von Emails woechentlich zu beantworten.

Das kann doch gar nicht sein, dass der neben seiner richtigen Arbeit soviel Zeit hat...

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

Angehängte Grafik:

unbenannt.png (verkleinert auf 62%)

unbenannt.png (verkleinert auf 62%)

Societe Generale Starts Stock Coverage on Range Resources (RRC)

Posted by Patrick Bannon on Apr 24th, 2012 // Read 0 Times // No Comment

Range Resources logoEquities researchers at Societe Generale began coverage on shares of Range Resources (NYSE: RRC) in a report issued on Monday. The firm set a “buy” rating on the stock.

Shares of Range Resources traded up 0.40% during mid-day trading on Monday, hitting $58.30. Range Resources has a 52 week low of $50.55 and a 52 week high of $77.24. The company has a market cap of $9.202 billion and a P/E ratio of 162.66.

RRC has been the subject of a number of other recent research reports. Analysts at Macquarie upgraded shares of Range Resources from a “neutral” rating to an “outperform” rating in a research note to investors on Friday, April 13rd. Separately, analysts at Zacks upgraded shares of Range Resources from an “underperform” rating to a “neutral” rating in a research note to investors on Tuesday, March 6th. They now have a $67.00 price target on the stock. Finally, analysts at Stephens upgraded shares of Range Resources from an “equal weight” rating to an “overweight” rating in a research note to investors on Monday, March 5th.

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |

Angehängte Grafik:

iii_mail_pl_10052012.png (verkleinert auf 52%)

iii_mail_pl_10052012.png (verkleinert auf 52%)

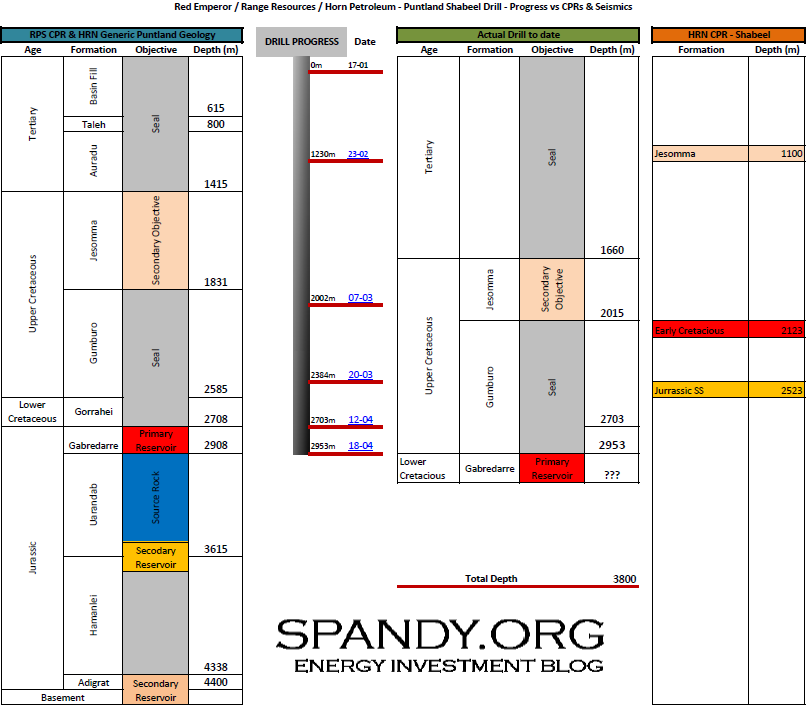

Range Resources Limited ("*Range*" or "*the Company*") is pleased to

announce that the

Shabeel-1 well currently being drilled in Puntland by the Joint Venture

partner and

operator, Horn Petroleum Corp. (TSXV: HRN) is drilling ahead at a

current depth of

3,425m (as at 13 May 2012).

A gross section of 150m of oil (possible net pay between 12-20m) has been

encountered

in the Cretaceous Sandstones (previously announced) whilst further oil

shows have been

encountered in the deeper sandstones which are currently being drilled.

A testing program including the zones discovered to date and any deeper

potential pay

zones encountered will be agreed with the Operator upon total depth being

reached.

Optionen

| Boardmail an "Mikrokosmos" |

Wertpapier: Range Resources Ltd. |

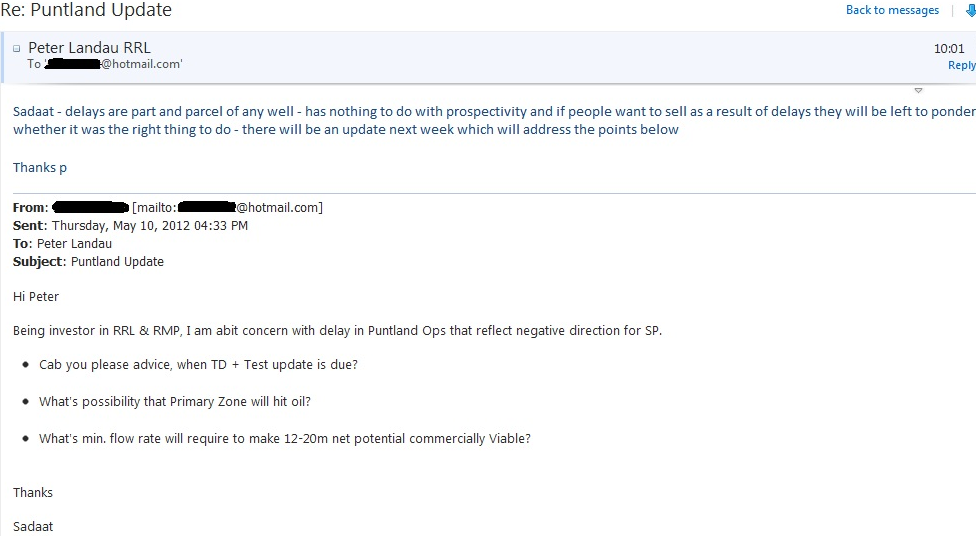

I hope this email finds you well. As previously agreed between ourselves, I have a few questions for you this week from a large number of fellow investors that we would appreciate you answering. I do understand that a few may be a tad pressing but after not contacting you last week with a set of questions to see if your answers to the questions from 2 weeks ago would come to fruition, our group feels that these questions do need answering in light of some of your answers not fitting in with the timescales that you provided.

We would appreciate if you could answer them with more certainty rather then "next week" answers that do not ever happen as stipulated. As you can imagine, PI's are becoming increasingly frustrated with this and feel like they are being walked up the garden path with all of these missed timelines. This is by no means a derogatory statement as we understand that there are outside factors that play a part in things but, surely you should have more of an idea of what is going on as these statements and answers you give that don't come to fruition is not giving your PI's any faith at the moment in the game plan of RRL.?

A lot of business that I conduct is in international trade and when drawing up a contract I use performance bonds to ensure that timescales are adhered to. I'm sure you already know how these work and if investors were to use these (as example) with RRL then you can imagine the cost to RRL in the way of penalties. I guess PI's take your words as their performance bond and the "payment penalty" is the sentiment of the PI's which is increasingly waning which in turn, is detrimental to the SP of RRL. We are just asking for clarity and for the "performance bond" to be exactly what it is meant to be used for.

Anyway, hopefully you can help us with these questions;

1) "No raising at these levels... said back in Summer 2011 when SP was above 15p" - Since then we have raised at at 11p and 12.5p?

Yep - said in summer - world changes , life changes , circumstances change - everything is done because we believe we have a footprint to get range to $1bn minimum on existing cap structure with little exploration success required - when we look at these things we say 5% dilution can return 3-5x minimum in value over and above the dilution - problem is with your time frames and current share performance you can basically say im full of shit and did it solely to screw shareholders over - so when aoc raised a bucket load of money ay 90c for a massive dilution they clearly got it wrong - everything revolves around a big value based event - we have at least 3 available in texas (sale), trin and Colombia - didn’t even mention puntland because we took the view that we needed to protect shareholders if puntland didn’t happen (it has and that is now number 4) - based on your performance bond theory you would have sacked aoc for their 3 year delay in drilling a well and we would all be no where

"Colombia will only happen when SP is higher." - Colombia was raised at 11p?

12.5p and see above re rationale - do you walk away from something that can provide exponential returns on the basis that puntland and georgia are guaranteed successes - called business judgement and more than happy for people to say ive got no idea - would actually prefer that as opposed to time lines and performance bonds - puntland has worked to date, so has texas and Trinidad, jury out on georgia and Colombia just starting - whats not working is the share price and happy to cop that but based on your caustic comments range is a basket case - we are fully funded and can now implement what we need to do to fix the share price - combination of buy back, consolidation, spin out of assets (maybe puntland on shore / offshore solely) into separate aim listed vehicle with free stock distribution to existing range holders - the fact is we recognise the issue and know what we need to do to fix it - wont happen overnight and investors can either chose to be part of it or not - as I said last time (I think) - the time frames you base your expectations on are far different to mine

" Offshore Puntland is an RRL only play" - they now intend to offer RMP a substantial part of it?

Do we - where does it say that , what is the deal - get over yourself on this one - if on shore is a big winner rmp is best placed to offer over the top odds as a farm in partner on a long term play - there is no deal right now - called doing good business and accessing those who would be prepared to pay more to give range the best deal

"21 Wells in TT before end 2011" - less than a third of that transpired?

Yep - and each well has been a disaster - the on ground team underestimated the teething problems is ramping up activity - what a mess I mean most people would normally worry if the oil was there or not - show me where else in the world right now you can get a 1000 ft well to flow naturally at 130 bopd and have a well payback of 2 months - we have 50 of these wells planned and they form part of our p1 reserves - sorry if would prefer 21 wells on time with no oil and shit flow rates

"Socius Raising for Herrera fastrack" - now DELAYED until Q3/4 2012?

Yep - go and see baker Hughes and ask them about the quality of the seismic data shot in early 2000s when it was sent to texas for scrubbing and reinterpretation - outside our control - you say I make excuses - I say I rely on what im told at the time by the consultants (both internal and external) - drilling is q3 and 4 - volumetrics may / june

"Site prep for the spudding of second Georgian well has been hampered by weather", previous announcement erroneously by NOMAD mentions change in tack to CBM gas exploration. This was therefore the plan all along?

Seriously mate - you are welcome to go visit the site pics in georgia - be very clear - if GIG weren’t in we would be doing the second well (called running plan a and b), they are in , they are massive in gerogia and its makes perfect sense to go with them on the revised plan - again good business judgement for me , deliberate ploy to fuck over pi 's for you

When can your shareholders take what you say to be true? The evidence suggests your spoken and written word is not to be relied upon when making investment decisions.

Simple don’t - see my explanations above and if investors don’t feel comfortable don’t be there

2) Is it pure coincidence that the only time, without exception, RRL trades in volumes of over 50M for consecutive days making significant gains, there is a subsequent placing of discounted stock to House broker clients?

Pure coincidence but please stick with your conspiracy theories

3) Puntland Offshore - On the diagram provided with the Quarterly Report you show a series of seismic lines and a well - Gerard Main 1 - Can you share any information about the history of this well and what the seismic's are telling us?

We will put out a full power point preso on the offshore potential when we complete the PSA with the government - wont give a time frame because youll just hang for it and suggest I should be able to control the Puntland Government and Somali politics

4) We would also like to know why range have given an unsecured loan to another PL company, continental coal, of circa $2m whilst issuing shares in the same period diluting ranges share value even further?

Yep range was and is down to its last $2m - whats a better deal for range - money sitting in the bank at 3% or getting effective 15-25% return for short term financing - if you are suggesting in any way that range had to do a placement because we had lent money elsewhere you are wrong

5) The possible "re-entry well" in Colo, why was it closed in/abandoned in the first place please and how long do you estimate the seismics to take please?

Model was run at 15-17-20 usd per bl in the late 70's and logistics / security in the area back then weren’t great - 12 months for seismic and interpretation - re-entry time frame quicker but being finalised

6) This question relates to your compensation arrangements with OKAP Ventures. As you can see on page 60 of the annual report Range paid OKAP (of which You are a director) and another Landau related company $2M in 2011 for general corporate services. This is in addition to the $300,000 you were paid in salary (plus $300,000 in salary, $990,000 you were awarded in stock options and $1.4M to OKAP in 2010) by Range. It seems to us that your interests are not completely aligned with those of Range shareholders. We feel it would only be right of You to disclose how much compensation you are paid by OKAP and what the ownership structure of OKAP is given that you are the founder and managing director. We have questioned some industry experts about this arrangement and they have categorically stated that an opaque relationship like this would give them serious cause for concern when considering an investment in this company.

Good don’t invest - okap is not me alone - it’s the cfo and the 5 accounts managers that are needed to run the projects, the comp cec, the in house legal advisor, the fully serviced offices in perth and London, the pr and ir services, the travel management and the corporate / capital raising services - we do our own comparative analysis and we come in far cheaper than a lot of other companies with our size and operations - its ironic that some people are happy to pay double the number just to see the word consultants, cfo, merchant banks, 15 employees etc etc next to the line item as opposed to the one stop shop - we have a staff of over 20 that can provide the services better and cheaper because with 8 listed companies a lot of the fixed costs can be spread put amongst the group (range is the biggest yes) - many industry experts think the opposite about okap and our model

7) you stated that we would be hearing news on Texas, Georgia and Colombia last week along with Stockmailer being released, all we got was Georgia. What has happened to the details on Texas and Colombia and what has caused the further delay of the Stockmailer?

Texas and colom coming you can see the relevant extract from stockmailer and you are welcome to confirm anything with him given you think all we do is bullshit and screw pi's over

(4 may) Melissa - Hoping to get the Proofs back from Graphic people today - we will proof to get print ready. I will email you the proof as soon as I get them.

Thank you in advance for your time in reading this email and hopefully you can restore a little faith with your PI's with some answers that will actually happen when you stipulate they will.

Please don’t be shareholder if my number one objective and performance target is to meet time frames I provide as a best estimate at the time (what would you have done with aoc with their 3 year delay, dilution and intro of the Kenyan and Ethiopian assets) – our assets are great, fully funded, so much activity (clearly not on time) – fully aware of our faults and always open to constructive criticism and suggestions (especially on the share price) – unfortunately I don’t find your emails constructive in any way – they are aggressive and designed purely to suggest that it’s all a big con job – as I said will always respond because I actually know what we can and will achieve and cannot stand the fact that your approach to everything is half glass empty – the other irony is range (not aoc, horn and rmp) has done such a good job legitimising puntland, that as a value proposition which we sought to mitigate and insure against is currently flying (was that good or bad business judgement – don’t know but be very clear that whatever the share price our 20% interest is the same as rmp;s and horns (pro rata)

Optionen

| Boardmail an "MalkusTax" |

Wertpapier: Range Resources Ltd. |