Thompson Creek Metals (Blue Pearl Mng)

Seite 166 von 883 Neuester Beitrag: 24.04.21 22:58 | ||||

| Eröffnet am: | 18.01.07 07:23 | von: CaptainSparr. | Anzahl Beiträge: | 23.072 |

| Neuester Beitrag: | 24.04.21 22:58 | von: Lenaldbqa | Leser gesamt: | 2.687.826 |

| Forum: | Hot-Stocks | Leser heute: | 1.270 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 164 | 165 | | 167 | 168 | ... 883 > | ||||

an tagen wo blue 70-80 cent gestiegen ist sind wir schier ausgeflippt. die waren aber öfter zusehen als solche tage wie heute. (zumindest in den letzten 2 wochen)

ist zwar alles andere als schön heute der chart, aber solche konsolidierungen müssen auch sein und sind auch gut für den kurs. blöder spruch stimmt aber immer wieder.

nagut heute geht es nach guten news eben etwas abwärts. aber erst als die tel.-conf. vorbei war ging es extrem runter. haben eben alle dieses bonbon erwartet nur kam es leider nicht.

ok machen wir eben die nächste konso durch. ich bleibe jedenfalls bis zum 13.-14. mai mindestens investiert.

DER kleine Absacker is' doch Killefix!!

Wir können cool bleiben bis 7 Eu.

Dann is' der kurzfristige Aufwärtstrend immer noch intakt! hehe *Kopfeinzieh*

MfG, Strato

Angehängte Grafik:

BPM_7.png (verkleinert auf 93%)

BPM_7.png (verkleinert auf 93%)

Moly Mines - 10,19%

New Cantech - 5%

Roca Mines unverändert, aber da wurden auch nur wahnwitzige 800 stück in ffm gehandelt.

--------------------------------------------------

Dhanoa Mines (gold) - 10,53%

Bravo Ventures - 2,86%

Sabina - 2,60%

--------------------------------------------------

Forsys - 7,51%

also ihr seht es geht wieder einmal überall runter. ist nicht auf blue allein zu beziehen.

unseren Vampir: ..... viiiieeeeeel helles Licht.

Das hilft garantiert!

MfG, Strato

Angehängte Grafik:

vampir-sarg[1].jpg

![vampir-sarg[1].jpg](https://a.onvista.de/forum/attachment.m?aid=90091)

vampir-sarg[1].jpg

gruss rs1

Angehängte Grafik:

Blaue_Berge.jpg (verkleinert auf 63%)

Blaue_Berge.jpg (verkleinert auf 63%)

bis morgen allerseits

und schlaft schön.

Angehängte Grafik:

gute_nacht.gif

gute_nacht.gif

Blue Pearl to adopt name of U.S. unit, list on NYSE

Canadian Press

TORONTO — The world\'s biggest publicly traded molybdenum producer, Toronto-based Blue Pearl Mining Ltd., is seeking to raise its corporate profile in the land of stars and stripes.

Blue Pearl executives told analysts in a conference call Tuesday the company expects to adopt the name of the major U.S. company it bought last fall, Thompson Creek Metals Co., and will apply for a listing on the New York Stock Exchange later this year.

“That requires additional preparatory work on our part, so it\'s not going to happen immediately, but we see that happening at some point in 2007,” CEO Kevin Loughrey said.

Blue Pearl acquired the Thompson Creek mine in Idaho last October. The mine is expected to have a life of 10 more years.

Related to this article

Latest Comments

Start a conversation on this story

The name change is subject to shareholder approval at the company\'s annual meeting May 10.

“Blue Pearl has been a very successful name for this company obviously and it has prospered under that name,” Mr. Loughrey said.

“However, in terms of all of our customers and most of our employees, the communities in which we operate and the molybdenum industry generally — and the customers who buy from our customers — the name Thompson Creek is the name that\'s associated with our products, and we believe it\'s going to be in the best interest of the company and the shareholders, going forward.”

Wayne Cheveldayoff, Blue Pearl\'s director of investor relations, said the U.S. stock exchange listing application and the name change aren\'t closely linked. The U.S. stock listing, he said, is to “appeal to a broader range of investors in the U.S.”

Mr. Loughrey said the company expects global demand for the base metal, which is used to harden steel, to remain strong as demand continues to grow at a rate of four per cent per year. The company is competing for market share with China, which is also a significant molybdenum producer.

“We think the outlook for the molybdenum business generally, and for Blue Pearl specifically, looks good into the future,” Mr. Loughrey said, noting prices have improved in the last few weeks.

Despite the positive forecasts, the company is facing a challenge in the development of its Davidson project, near the northern Interior town of Smithers, B.C.

A feasibility study is expected to be completed in the second quarter, and while Mr. Loughrey expressed optimism that the mine will receive environmental approval, a local investor said the “left-wing council” in the area opposes the project.

“I\'m not sure I hold your optimism for how easy your permitting process is going to be,” the investor told Mr. Loughrey. “Some of us who do hold stock up here, who aren\'t anti-mining, that\'s the feeling we\'re getting about this project, that it\'s not going to be as smooth as you seem to say.”

Mr. Loughrey said the company is confident it can work out the issues being raised by the community.

“We\'ll listen to the community and, obviously, do what we can to allay any concerns they have,” Mr. Loughrey said.

The company is planning to construct a new bypass road in response to some resident who opposed the location of the road that had been planned initially, Mr. Loughrey said.

Meanwhile, Mr. Loughrey said a major re-evaluation of the company\'s resources and reserves is underway, using higher molybdenum prices in calculations, to reflect the current market.

Blue Pearl reported Monday $150.8-million (U.S.) in revenue during the last 67 days of 2006, compared with zero in 2005.

The net loss for the year was $20.6-million or 36 cents per diluted share, including a loss of $12.4-million or 14 cents per share in the fourth quarter, when all the revenues were generated.

A year earlier, when Blue Pearl was still in development and prior to the Thompson Creek Metals acquisition, the 2005 loss was $4.1-million or 13 cents per share, including $2.5-million or 6 cents per share in the fourth quarter of 2005.

Production costs from the Thompson Creek and Endako mines averaged $6.28 a pound, while selling prices averaged $25.74 per pound.

Blue Pearl expects to produce 21 million pounds of molybdenum in 2007 and 27 million pounds the year after from its existing Thompson Creek and Endako mines.

Blue Pearl shares were down 48 cents (Canadian), or 4 per cent, to $11.58 in trading Tuesday on the Toronto Stock Exchange.

....und guts Nächtle!

So, sorry, dat mußte raus. Jetzt geht es mir wieder besser. ;-) Wenn unsre Perle heute nicht steigt, dann halt morgen. ;-)

Euch einen schönen Abend, ich guck heute mal nicht mehr nach dem Kurs

LG, Harley

Optionen

| Boardmail an "Harleyman500" |

Wertpapier: Thompson Creek Metals |

nein....unsere perle macht halt nie das was man denkt ;-)

hab den artikel im stockhaouse gefunden.....falls heute noch wer lust auf BPM hat ;-)

und ich mag es nicht wenn ich recht habe....aber ohne bonbon von ian war das schon fast klar :-/

na gut....mache jetzt auch erstmal aus....aber net für lange....gn8@all ;-)

ähm pichon....kannst mir nun mein nachtzeug bringen.....so als wenn es aus blauen perlen bestünde *gg*

mfg

me

Blue Pearl Chairman Foresees Molybdenum Supply Challenges

Posted on Mar 27th, 2007 with stocks: BLEFF.PK

James Finch submits: There is a polite arrogance to the new king of primary molybdenum producers that comes with being the big kid on the block. That’s how the executive chairman referred to Blue Pearl Mining (BLEFF.PK) during our hour-long telephone interview discussing his company’s developments, the future of the molybdenum market and new companies hoping to imitate his success.

Ian McDonald may very well be entitled to his opinions. After all, Blue Pearl could produce the same number of molybdenum poundage in 2007 as Cameco (CCJ) would produce of uranium. (And unencumbered by those pesky legacy contracts or remediation efforts at Cigar Lake.) Blue Pearl is now the largest publicly traded primary molybdenum producer. The company plans to mine about one-fifth of the world’ primary moly in 2007, about five percent of the world’s total mined molybdenum. His company will also roast about 12 percent of the world’s molybdenum. Not bad for a company which was a penny stock some seven months ago.

Blue Pearl has become the darling of Bay Street since the company announced its audacious US$575 million acquisition of privately owned Thompson Creek Metals Company. Having closed the transaction in late October, Blue Pearl now owns two operating molybdenum mines and concentrators and a metallurgical (roaster) facility in Pennsylvania. In mid June, the company’s shares traded for less than C$1.80; yesterday the stock closed at C$12.06. Since late August, shares in Blue Pearl have climbed relentlessly, with only brief pauses of consolidation.

We were fortunate to have included Blue Pearl in our seminal molybdenum article about the metal’s relationship with the energy bull market, this past July, at a time when few had heard of the company.

On Monday, the company announced encouraging cash flow from the recently acquired Thompson Creek operations. In the 67 days following this acquisition, Blue Pearl generated revenues of $150.8 million, about $2.25 million per day. Annualized, this could reach more than $800 million in 2007 if the price molybdenum remains firm and production continues according to plan.

Production costs for output from the company’s Thompson Creek and Endako molybdenum mines averaged $6.28/pound. The company sold this production at an average price of $25.74/pound. By 2008, the company hopes to mine 27 million pounds from these mines. The firm moly price helped Blue Pearl discharge the Second Lien Credit Facility of $64.3 million in mid March. According to Monday’s news release, the company cash balance stands at approximately $135 million.

The company expects its bank debt to fall to $320 million after paying its first quarterly installment in 2007 of $18.75 million. Blue Pearl incurred $401.9 million in long-term debt as part of its acquisition of Thompson Creek Metals. At its current production pace, the quarterly bank payments amount to a little more than one week’s production.

What’s on Ian McDonald’s Mind?

Historically, according to Western Troy’s Rex Loesby, annual molybdenum demand has grown about four percent since the 1950s. This fits well with McDonald’s forecast of 700 million pounds by 2020. “That’s what will need to be the supply,” he told us.

And where will this come from? “That, of course, is the big question,” McDonald said. “There’s a dearth of new projects in the pipeline.” And he reminded us that China has started to consume more of their own molybdenum production.

As with uranium and other metals, China is a wild card for molybdenum supply. In any moly discussion, China remains a primary concern for miners. “China was producing, 13 to 14 years ago, about 110 million pounds and exporting 100 million into a 230-million pound market,” McDonald pointed out. "Last year, in a 400-million pound market, China produced about 80 million pounds, net exporting about 30 million, so they are keeping more. The story is they use more of their own."

He is quick to point out that global moly demand was up six percent in 2006, but China’s demand increased some 20 percent.

“I’m not going to sugar coat it,” McDonald points out. “If they wanted to make it look bad, they would. If they start dumping on the market, everybody’s trashed.” But he doesn’t believe this is a likely scenario. There are only 39 big mines in the world, producing molybdenum, he told us. “But in China, there are over 500 small mom-and-pop operations. China is desirous of having some world-class companies, and they’ve shut down some of the smaller operations because they don’t use their power efficiently. If you have a big mining company, they are going to have a long-term view and maximize the country’s resources.”

From where supply comes from is second to the increasing demand McDonald sees ahead. “There are a growing number of applications for molybdenum.” He pointed out that cars consume molybdenum. “There’s about 0.9 pound or so in about a dozen different places in the automobile, and with 55 million cars in the world, that’s about 50 million pounds.” This is probably the third largest application of moly.

“High-end molybdenum stainless steel applications consume the biggest amount,” McDonald said. “Any steel that’s used in the ocean or near the ocean has got molybdenum in it.”

He pointed out that Blue Pearl leaves about 10 percent of the company’s molybdenum production in the sulphide form for the high-end lubrication market – the oil companies.

“Most of it is made into tech oxide, MO3, and about 25 percent would be ferromolybdenum,” he said. “We just sold some (ferromoly) in Europe for $34/pound.”

His company was chosen to help produce advice on the newly launched Sprott Molybdenum Participation Fund. We asked about his involvement. “We get a small fee for storing molybdenum if they choose to buy,” he told us. It would be stored at Blue Pearl’s metallurgical facility in Pennsylvania. “We would also sell them some,” he added. His company would not be counseling the fund in which companies to take investment stakes. “It would pose a conflict of interest and we would have to recuse ourselves,” he said.

Sees New Supply on the Horizon Lacking

“There’s a tremendous barrier to entry for a new primary molybdenum mine to come onstream with no forward market,” McDonald observed. “Because without a forward sale, financing requirements for the capital to build one of these new mined could be very, very challenging.”

He believes one of the other big molybdenum mines will get financed, but he cautioned, “I think that once one does, it doesn’t mean they are all going to.” He explained his own personal experience: "When we raised the US$575 million last year to buy Thompson Creek, this was a company making close to US$400 million a year after tax, and we had some heavy lifting to do. It was difficult. It would be difficult for another junior."

One place where he sees imminent molybdenum supply is from Blue Pearl’s Davidson deposit, not far from the company’s Endako mine and milling facility.

“We will have the feasibility out in the second quarter – I say second quarter, but I hope it’s very soon,” McDonald told us. “It will become the highest-grade molybdenum mine in the world.”

He said his company was lucky to have gotten it three years ago. “It had been ready for production and there was a lot of development done on it.” So, the company decided to move to the final feasibility study instead of bothering with a scoping study or pre-feasibility. He said the Davidson project would be in full production in 2009.

What about mine development? “There’s already 2.5 kilometers of underground workings there and terrific ground conditions,” he said. “We opened that up a couple of years ago, after no one had been underground in 25 years. All of the scaling for the entire 2.5 kilometers fit in a five-gallon paint bucket.” McDonald told us Blue Pearl plans to just mine the deposit and little else, “We will not even crush it, just a rock breaker, and just haul it right down to Endako.”

But Blue Pearl may take in a partner on Davidson – the Japanese trading company, Sojitz. “They own 25 percent of Endako, and they want to buy 25 percent of Davidson,” McDonald said. "It would make sense, if they own the same percentage of both. There wouldn’t be any recovery issues, or combining of ore and al that. We would have the same labor force.” He did caution the deal was not done yet. “We’ll look to possibly do a transaction with them."

Another project where McDonald hopes will provide additional molybdenum supply comes with the possible expansion of Endako into a ‘super pit.’ The company plans to have the scoping study done later this year, possibly by June. "I feel pretty good about that, it’s pretty realistic,” he told us. “We have a massive resource there, and it would be a pretty big job. But, it could take the wind out of some of these other juniors."

We discussed his vision of expanding the mill to 50,000 tons per day. “It’s probably 32,000 tons per day now,” he pointed out. The first step involves redoing the reserves and resource calculations at Thompson Creek and Endako using a $10/pound moly price. The previous pricing was “way too conservative,” according to McDonald. We suspect the higher resource figure would open the door to raising the likely $250 million to upgrade the facility to the higher tonnage operation. And his mind is already moving in that direction.

“Let’s say we had a study done within the next year,” he explained. “It would take to 2008 or 2009 to build it. Unfortunately, because the mine has been operating for forty-two years, we would have to move the existing mill.” The mill would have to be moved because there is ore beneath the present mill site. “It won’t happen overnight,” he warned.

And what about those other junior molybdenum companies?

"We aren’t going to grow our company by buying all these other moly deposits,” he responded. “Then, we have to go and raise $700 million, worry about marketing another 20 million pounds a year, and betting the company on it. Personally, and our board agrees, we’d rather buy something that’s either in production, and pay a little more for it, or take something at a feasibility stage, like copper/moly. We have a pretty good balance sheet, or we will have by the end of this year. Then maybe we could buy some moly production."

What are his plans as 2007 rolls on?

“We qualify for the New York Stock Exchange,” McDonald confided. “We’ve talked to them. I think we will get the ball rolling this spring, and we could look for an early fall consummation. We are going to come to the U.S., we qualify and they seem pretty keen on having us.”

Just to make sure we got his story right, McDonald added:

We’re not going to sit on our laurels. We have a lot of growth ahead of us, bringing on Davidson, expanding the reserves of both mines and doing a scoping study for expanding Endako. Our main job is to get the debt paid down and increase the reserves. That’s quite a bit. It’s all within our backyard and with our own expertise. Anything we do outside of that – we will do other things, I think, but they are things that are going to be for sure.

Disclosure: Author has no position in the above-mentioned securities

§

NewsBlast Sign-Up

StockHouse NewsBlast: Receive company sponsored news and information via email.

§

Optionen

| Boardmail an "GeldundCo" |

Wertpapier: Thompson Creek Metals |

Optionen

| Boardmail an "GeldundCo" |

Wertpapier: Thompson Creek Metals |

guts nächtle an alle....

Zwei Machbarkeitsstudien in 2007: Blue Pearl Mining goes Wall Street

Neuer Name trotz Erfolgsstory: Blue Pearl Mining wird Thompson Creek MetalsNeuer Name trotz Erfolgsstory: Blue Pearl Mining wird Thompson Creek Metals

Gestern hat Blue Pearl Mining den Finanzbericht des vergangenen Jahres veröffentlicht und einen Cash-Flow von rund 75 Millionen US-Dollar vermeldet, der innerhalb von wenigen Wochen erwirtschaftet wurde. Ein Beweis dafür, dass das Unternehmen produziert und bereits Geld verdient. Die heutige Analystenkonferenz brachte weitere Neuigkeiten zu Tage. Die Veröffentlichung der Machbarkeitsstudie für das Davidson-Projekt wurde auf das zweite Quartal dieses Jahres terminiert und es wurde angekündigt, dass man auch für die Endaco-Liegenschaft eine Machbarkeitsstudie in Planung hat. Diese soll noch in diesem Jahr begonnen werden. Neben Updates zu den Liegenschaften gab Blue Pearl Mining bekannt, dass man den Namen des Unternehmens in Thompson Creek Metals ändern wird. Das Management ließ verlauten, dass dieser Name bei Kunden geläufiger sei und insbesondere in den USA besser aufgenommen werden würde. Während der Hauptversammlung sind die Aktionäre gefragt, dem Antrag zur Namensänderung zuzustimmen.

Die Vereinigten Staaten sind auch in anderer Hinsicht das erklärte Ziel von Blue Pearl Mining: Noch im Jahr 2007 möchte man auch an der New York Stock Exchange (NYSE) gelistet sein. Blue Pearl hat seine Aktionäre hinreichend informiert. Vor allem die geplanten Machbarkeitsstudien und das Listing an der NYSE können positiv gewertet werden. Wenn der Kurs seit der gestrigen Meldung auch ein wenig stagniert, so sollten Aktionäre doch zuversichtlich sein. Als einziger börsennotierter Molydän-Produzent kann Blue Pearl schon heute von den hohen Preisen für Molybdän profitieren. Die Ankündigung, auch weiterhin regelmäßig Kredite tilgen zu können, bestätigt dies zusätzlich.

Quelle: aktienblog

-einbruch beim US Verbrauchervertrauen (gesamtmarkt down)

-ein paar "sells on good news"

-ein paar stop loss ausgelöst

-zwar super zahlen, aber quasi schon mehr oder weniger zu erwarten

-dann kein richtiges extra Bonbon

So, und wenn ich das mal zusammen nehme, muss ich sagen, unser Perlchen war richtig stark heute, zumal die letzten wochen ja ordentlich Kurssteigerung gebracht haben.

und wenn ich dann noch zurückschaue auf meine gut einjährige "Mitgliedschaft" bei Blue, dann kann ich nich anders, dann muss ich machen einen

Optionen

| Boardmail an "NewBarbossa" |

Wertpapier: Thompson Creek Metals |

Angehängte Grafik:

Luftsprung.jpg

Luftsprung.jpg

Optionen

| Boardmail an "NewBarbossa" |

Wertpapier: Thompson Creek Metals |

Angehängte Grafik:

bp.gif

bp.gif

Optionen

| Boardmail an "NewBarbossa" |

Wertpapier: Thompson Creek Metals |

Angehängte Grafik:

Licht_aus.jpg

Licht_aus.jpg

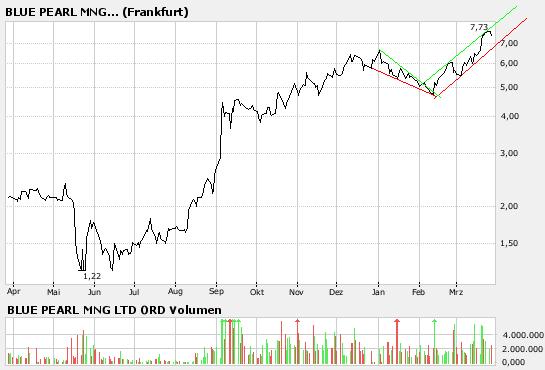

Ich wünsche uns allen einen schönen grünen und natürlich auch sonnigen Börsentag!

Und nun zu Chartex:

Wie kommt der ausgewiesene Verlust zustande?

Auf den ersten Blick hätte Blue Pearl in den letzten 67 Tagen des Jahres 2006 (seit der Thompson-Creek-Übernahme) einen Gewinn ausweisen müssen, da pro Kalendertag nach Steuern 1 Mio US-$ Gewinn erzielt wird (Quelle: Aussage von McDonald bei der Präsentation am 21.11.2006 (Tondokument, abzuhören über www.bluepearl.com)), auch wenn man verschiedene Zusatzkosten und Einmaleffekte (Gewährung von Optionen an 110 Mitarbeiter) in Zusammenhang mit der Übernahme in Betracht zieht.

Tatsächlich jedoch wurden rund 20 Mio US-$ Verlust ausgewiesen (Quelle: Audited Annual Financial Statements vom 26.3.2007 bei www.sedar.com).

Die Zahlen, welche wesentlich zu der Berechnung des Verlustes beigetragen haben, habe ich in meinem Posting von gestern Mittag bereits erwähnt. Rein rechnerisch war mir der Weg zu diesem Verlust durchaus klar. Ich hatte jedoch zunächst ein Verständnisproblem, warum diese Zahlen zu dem Verlust führen. Nach längerer Überlegung und Analyse der Berichte bin ich zu folgender Erklärung gekommen:

Bei der Übernahme von Thompson Creek wurden 7,8 Mio Pfund Molybdän als Lagerbestand übernommen und dafür ein Betrag von 98,5 Mio US-$ berechnet (Quelle: MD&A vom 26.3.2007 bei www.sedar.com). Der bei den Übernahmeverhandlungen vereinbarte "faire Preis" pro Pfund, der an den Alteigentümer bezahlt wurde, betrug damit etwa 12,62 US-$ und ist somit rund doppelt so hoch, als wenn Blue Pearl dieses Moly selbst produziert hätte.

Aus diesem übernommenen Lagerbestand wurden etwa 70% (rund 5,7 Mio Pfund) nach dem FIFO-Prinzip in 2006 verkauft. Der Lagerbestand wurde aus der laufenden Produktion ergänzt und dürfte sich insgesamt kaum verändert haben.

Aufgrund der Buchhaltungsbestimmungen (McDonald hat dies in der Telefonkonferenz gestern kurz angesprochen) wurde der diesen Verkäufen zuzurechnende Einkaufspreis von rund 69 Mio US-$ als Kosten angesetzt. Für die laufende Produktion des Molybäns, das als Ersatz der verkauften Ware eingelagert wurde, fielen Kosten in einer Höhe von etwa 24 Mio US-$ an (3,846 Mio Pfund x 6,28 US-$ Produktionskosten (Quelle: MD&A)).

Weiter Kosten in Höhe von 46 Mio US-$ sind wohl unter anderem für den Betrieb von Langeloth (Fremdröstung sowie Ankauf-Röstung-Verkauf von Moly unter eigenem Namen) anzusetzen (Other operating expenses 70 Mio US-$ (24+46=70) Quelle MD&A).

Halten wir fest: Es wurden die Ankaufkosten des Lagerbestandes als Kosten verbucht (in doppelter Höhe der eigenen Produktionskosten) und zusätzlich die Kosten der laufenden Produktion, zusammen also ganz grob 69 Mio US-$ mehr als dem normalen Geschäftsbetrieb entspricht. Hingegen konnte der durch den angekauften Lagerbestand erhöhte Wert an Molybdän in der Gewinn- und Verlustrechnung keine Berücksichtigung finden, da eine nicht verkaufte Ware natürlich keine Einnahmen in Cash bringt. Als weitere Verschärfung kommt hinzu, dass dieser Mehrfach-Kostenaufwand für die gleiche Ware nur mit den Einnahmen von etwas über 2 Monaten gegengerechnet werden konnte.

Wenn man diese buchhaltungstechnisch bedingte Verzerrung herausrechnet (also nach dem gesunden Menschenverstand geht), dann hätte sich ein Gewinn in Höhe von 69 Mio abzüglich 20 Mio, also rund 49 Mio US-Dollar ergeben.

Um Einwürfen die Spitze zu nehmen:

Mir ist bewusst, dass die buchaltungstechnisch korrekte Vorgehensweise die einzig mögliche ist. Zur Beurteilung des zukünftigen Gewinns (und damit des Kurses der Aktie) entsteht so jedoch ein verzerrtes Bild. Die Anleger sollten zumindest nachvollziehen könne, warum ein Unternehmen, das eigentlich riesige Gewinne erwirtschaftet, auf dem Papier plötzlich Verlust ausweist.

Ich bitte um Diskussion, falls jemand die Sache anders beurteilt.

Im 1. Quartal 2007 wird sich die Sache übrigens auch noch etwas auswirken. Es sind noch etwa 30 Mio US-$ aus dem Lagerankauf nicht verrechnet (da in 2006 noch nicht verkauft). Vermutlich wird dies jedoch dadurch über-kompensiert, dass der Lagerbestand in diesem Quartal verringert wurde (Quelle: Mail von Wayne Cheveldayoff an "therefore", gepostet hier im Thread am 11.3.2007) und damit zusätzliche Einnahmen von etwa 25-30 US-$ pro Pfund generiert wurden.

chartex

LG, Harley

Optionen

| Boardmail an "Harleyman500" |

Wertpapier: Thompson Creek Metals |