Der USA Bären-Thread

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

5:58 China central bank to raise reserve requirement ratio 50bp

Hidden U.S. subprime losses may mirror Japan bank crisis

NEW YORK (Reuters) - Investors and banks holding on to U.S. subprime mortgage bonds in hopes of a recovery in value may make losses worse, mirroring the Japanese banking crisis in the 1990s, according to authors of a new report.

The Japanese banking crisis, triggered in the early 1990s by a slumping property market and brokerage collapses, led to a decade-long credit crunch. The government subsequently had to step in to stabilize the banking system by injecting public money into top banks.

"The Japanese experience of holding large losses as opposed to taking a hit and moving on was a direct cause of the Japanese malaise," said Josh Rosner, co-author of the report and a managing director at Graham Fisher, an investment research firm in New York.

The new report, "Financial Services Exposures to Subprime," said "there are many institutions with significant levels of embedded losses that have not yet been recognized as a result of questionable valuations."

Today, only a few banks and brokerages have recognized losses on U.S. subprime mortgage bets, as the housing market has weakened. Bear Stearns Cos (BSC.N: Quote, Profile, Research) has publicly recorded losses from its hedge fund bets on subprime mortgage bonds held in collaterized debt obligations. Outside the U.S., four hedge funds, two in Britain and two in Australia, have said they suffered losses.

More investors are hiding losses that may only get worse, the report said. Growing concern about the deteriorating U.S. housing market may hurt corporate buyouts, debt financing and stock markets. The Standard & Poor's 500 Index lost $300 billion in value this week on concern about credit markets.

Today's investors and financial institutions are now "playing a dangerous game," Rosner said on Friday. "The losses will almost certainly be larger than they are today."

As more rating downgrades come, values will continue to fall and margin calls will increase, the report said.

Standard & Poor's cut ratings on $6.4 billion in debt this month and Moody's Investors Service slashed $5.2 billion worth. S&P on Thursday cut various residential mortgage-backed securities to junk, including one class of bonds whose ratings were out of synch by 12 levels.

S&P lowered its grade from "AA," S&P's third best rating, to "B," or five levels into junk status.

Bear Stearns also on Thursday seized control of most assets in a troubled hedge fund, after declines in the value of riskier, subprime home loans caused the fund's value to plummet to almost nothing.

Bear Stearns said it "assumed possession of the assets" securing a $1.3 billion credit facility provided to its High-Grade Structured Credit Strategies Fund after the fund was unable to meet a margin call.

Joseph Mason, co-author of the report, said the drying up of capital for investors and banks that rely on that financing to fund leveraged buyouts may begin to weigh on growth.

"I'm not saying it will cause a recession, but we could have a low economic growth environment," Mason said.

Rosner and Mason also compared the current subprime crisis to the U.S. savings and loans crisis in the 1980s, when waves of S&L failures led to a federal bailout.

In the Japanese case, the bursting of the asset bubble in the real estate and stock markets led to a deteriorating economy. Japanese banks were saddled with massive non-performing loans, raising concerns about a systemic meltdown.

http://www.reuters.com/article/businessNews/...420070727?feedType=RSS

Zwischen 1990, als die Bankenkrise in Japan (# 3283) begann, und 2003 ist der Nikkei von knapp 40.000 auf 8.000 Punkte gefallen.

Überträgt man das auf den DAX, so würde der in 13 Jahren - also im Jahr 2020 - unter 2000 Punkten stehen.

Der DOW würde bis dahin von 14.000 auf 2.800 abschmieren.

Klar gibt es große Unterschiede zwischen Japan, Deutschland in USA. Der Nikkei-Chart zeigt dennoch sehr eindringlich, wie sehr man mit "Buy-and-Hold" (also ohne aktives Risikomanagement) auf die Nase fallen kann. Selbst mit 13 Jahren Geduld beim Warten (Kostolany meinte ja, Schlaftabletten für 10 Jahre würden reichen...) haben Anleger in Japan ihr Geld gefünftelt - was inflationsbereinigt (in Euro) einer Zehntelung gleichkommt, d.h. 90 % realer Kaufkraftverlust des eingesetzten Kapitals.

Angehängte Grafik:

nikkei_a3176.gif (verkleinert auf 88%)

nikkei_a3176.gif (verkleinert auf 88%)

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

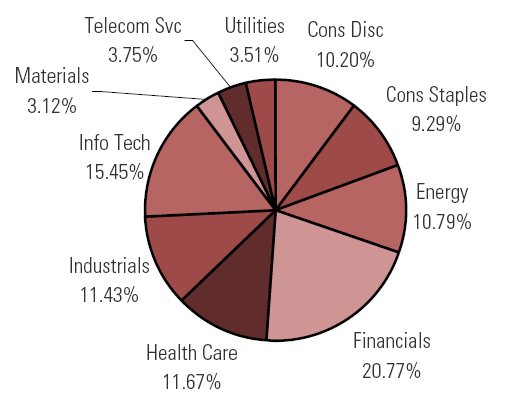

Ein weiterer Blick auf die Gewichtung der Financials im S&P lässt da nichts Gutes erahnen.

Angehängte Grafik:

sp500_zusammensetzung.png (verkleinert auf 99%)

sp500_zusammensetzung.png (verkleinert auf 99%)

Es gibt mMn zuviele Leute, die glauben, dass Aktien "langfristig immer steigen". Japan beweist das Gegenteil. 1990 stand der Nikkei bei 40.000, heute steht er - trotz Verdoppelung seit 2003 - bei 17.300. Nach 17 Jahren geduldigen Wartens ist noch immer mehr als die Hälfte der Kohle weg.

Und die Ursache war eine Bankenkrise - wie jetzt in USA. Ich will die Gefahren nicht künstlich aufblasen, aber es gibt in der Wirtschaftsgeschichte bislang keine Parallelen zur jetzigen US-Derivate-Blase, die mit einem "Underlying Value" von 150 Billionen Dollar bereits das 15-fache des jährlichen US-BIP erreicht hat. Und ein Großteil dieser Risiken liegt in Händen von Hedgefonds wie den beiden pleite gegangenen von Bear Stearns. Einen Härtetest bzw. Realitäts-Check dieses wackeligen Systems gab es bislang noch nicht - und ich bezweifle stark, dass er bestanden wird.

Stimmt schon, dass die Indizes in USA und Europa bei Weiten nicht so stark überbewertet sind wie der Nikkei im Jahr 1990. Aber dafür gibt es heute wegen der Derivate-Blase ein deutlich größeres Abwärtsrisiko als damals in Japan (mMn) - was in der Summe ebenfalls zu einer Fünftelung führen könnte (vermutlich aber viel schneller als beim Salami-Crash in Japan).

Die Gefahren der US-Kreditblase dringen erst jetzt langsam ins öffentliche Bewusstsein, nachdem immer klarer wird, dass sie globale Ausmaße hat: Betroffen sind australische Hedgefonds, die britische Bank HSBC, die holländische Bank ABN Amro, in Deutschland die IKB und viele anderen Banken, die sich die faulen Subprime-Eier ins Nest gelegt haben (ziemlich sicher auch die Deutsche Bank).

Diese Probleme gibt es in US alle nicht. Die Situation ist also überhaupt nicht vergleichbar, AL.

Contracts on 10 million euros ($13.8 million) of debt included in the iTraxx Crossover Series 7 Index of 50 European companies increased 60,000 euros to 504,000 euros at 11:45 a.m. in London, according to JPMorgan Chase & Co., the biggest one- day move. Credit-default swaps are used to speculate on the ability of companies to repay debt and an increase indicates worsening perceptions of credit quality.

http://www.bloomberg.com/apps/...20601087&sid=ahJLgbXdvXo4&refer=home

Optionen

| Boardmail an "obgicou" |

Wertpapier: S&P 500 |

Wir hatten vor 4 Jahren den DAX bei 2300. Der DAX ist ein Performance-Index und die 2300 wurden nur erreicht, weil die Versicherer bei Tiefstständen zwangsverkaufen mussten. Dies wird, solange die gleichen Entscheider da sind, nicht gleich wieder passieren. Solche wirtschaftlichen Fehler werden pro Generation meistens nur einmal gemacht. Ein neuer DAX-Tiefstand würde diesmal eher durch Mangel an billigem und keinem ausländischen Geld definiert werden.

Mir gibt primär der Einfluss des ausländischen Geldes auf den DAX zu denken. Deshalb denke ich auch, dass die Zahlen über den Investitionsgrad der hiesigen Institutionellen und Privatanleger nicht sehr relevant für den jetzigen DAX- Stand und die abgeleiteten kurzfrisigen Prognosen sind.

Das Ganze könnte sich noch verschärfen, wenn der US$ gegen den Euro wider Erwarten steigen sollte.

Für die US Indizes gelten natürlich etwas andere Argumente.

Optionen

| Boardmail an "relaxed" |

Wertpapier: S&P 500 |

Ich habe in den letzten Tagen nie den Mut gehabt zuzugreifen. Die Investitionsquoten in Aktien sind bei institutionellen Anlegern historisch gesehen nicht hoch, somit verbleibt noch genügend Spielraum für Nachkäufe in Schwächephasen.

Sehe ich dann allerdings den Spillover (wie auf die IKB) dann kann alles doch ganz schnell gehen.

Wie also geht es weiter?

Permanent

The tremors from the subprime debacle are vibrating throughout the interconnected web of modern global financial markets. Derivatives, corporate debt, loans and bank stocks are all getting trashed. Here are five reasons to expect the turmoil to worsen.

Don't Bet on Helicopter Ben . . .

A week ago, traders in the futures and options markets were pricing the chances of December interest-rate cuts from the U.S. Federal Reserve at about 21 percent. Prices now suggest a 47 percent chance that Fed Chairman Ben Bernanke will sanction lower borrowing costs to rescue the mortgage market, based on July 26 closing levels.

The rapid turnaround in interest-rate expectations shows the financial community is far from convinced that the wider economy is immune from the woes afflicting particular pockets of the bond and credit markets.

Is Helicopter Ben, as he was dubbed early in his monetary- policy career, really going to fly over the global financial markets and shower investors with dollar bills in the form of cheaper money? Even a hint that the Fed might be planning a rescue would be a signal that the outlook is bleaker than officials have admitted so far.

. . . Do Bet Against Moody's

Investors made more than 23 million bets against Moody's Corp.'s share price in the month to mid-July, according to Bloomberg data on the total amount of stock that was sold short and hasn't been repurchased yet. Those trades, known as short interest, have surged from 18 million in mid-June, and have almost quadrupled in the past four months.

Moody's shares have declined about 10 percent in the past two weeks, extending their loss for the year to almost 20 percent. Frederick Searby and Jason Lowe, New York-based analysts at JPMorgan Securities Inc., this month cut their second-quarter revenue-growth forecasts for Moody's to 19.4 percent from 21.5 percent, and their earnings-per-share forecast to 68 cents from 69 cents.

``Should debt markets become less issuer friendly, CDO issuance could be adversely impacted, hurting Moody's results,'' they wrote in a research report.

The Fundamentals of Leverage

The global default rate among corporate borrowers with ratings below investment grade declined to 1.4 percent in the second quarter from 1.5 percent in the first quarter, according to Moody's. Just eight borrowers defaulted on $3.2 billion of debt in the first half of the year. The default rate is now at its lowest level in more than 12 years.

That hasn't prevented the iTraxx Crossover index, a barometer of creditworthiness for 50 European companies, from surging to as high as 440 basis points last week, up from about 260 basis points two weeks ago and a low for the year of 170 in February. The higher the index, the less confident investors are about the outlook for corporate bonds.

Once fear grips a leveraged market, the so-called credit fundamentals aren't worth the paper you print your spreadsheets on. The yield on the benchmark 10-year U.S. Treasury note has declined to about 4.8 percent from as high as 5.3 percent seven weeks ago, as investors seek the warm, comforting embrace of the U.S. debt market.

``While the fundamentals, such as global growth and corporate balance sheets, are at their best for arguably decades, the technicals are as bad as we've ever known them and arguably the worst in the era of leveraged finance,'' Jim Reid, a London- based credit strategist at Deutsche Bank AG, said in a research note last week. ``Never has so much money been thrown at and been levered up in credit and never has there been such a liquid derivatives market to hedge risk.''

It's Like Money in the Bank

After peaking at about 511 points on May 23, the Standard & Poor's index of 92 U.S. financial stocks declined more than 10 percent through July 26, while the S&P 500 index fell just 2.6 percent. In the five years through the end of 2006, the financial index posted a total return of more than 56 percent, outpacing the 34 percent delivered by the benchmark index.

Here's a scorecard of some of the world's biggest banks, from wherever the shares reached their high for this year compared with closing prices on July 26. Bear Stearns Cos. is down almost 28 percent. Royal Bank of Scotland Group Plc is down 21 percent. Deutsche Bank AG is down 18 percent. JPMorgan Chase & Co. is down 17 percent. Goldman Sachs Group Inc. is down almost 17 percent. Citigroup Inc. is down almost 14 percent. So much for the golden age of finance.

Not-So-Fizzy Drinks

Failing to finance deals that have already been agreed on is one thing. Struggling to find a buyer for a business with some of the world's best-known brand names is another. So last week's news that Cadbury Schweppes Plc extended the deadline for selling its U.S. drinks unit is a worrying sign that the cash to do a deal might not be there at an acceptable price, no matter how thirsty investors are for Dr Pepper and 7-Up sodas.

Every day brings a new failure. Borrowers ranging from Manchester United Plc, the world's fourth-biggest soccer club by revenue, to billionaire Barry Diller, chairman of Internet travel agency Expedia Inc., have failed to find lenders to refinance debt or fund share buybacks.

``The debate is whether this is simply a risk re-pricing in financial markets, or something that will spill over into the broader economy,'' says Charles Diebel, head of European rates strategy at Nomura International Plc. ``The more prolonged this credit event is, the more risks of a contagion.''

http://www.bloomberg.com/apps/...20601039&sid=ageDhNv.n1A4&refer=home

Deutsche Bank AG analyst Eugene Xu recognized a financial train wreck in the making two years ago when he predicted ``quite probable'' losses from the least creditworthy home loans in America's runaway property market.

Now Germany's largest bank is poised to reap a bonanza of at least $270 million and as much as $540 million from a strategy that enabled its traders to sell subprime mortgage loans with derivatives contracts that appreciated as the U.S. housing market suffered its worst slump in 16 years.

``It was definitely a good trade,'' said Thomas Radinger, who helps manage about $96 billion at Pioneer Investments in Munich and holds Deutsche Bank shares.

While mortgage-related losses staggered Zurich-based UBS AG and London-based HSBC Holdings Plc, Frankfurt-based Deutsche Bank may report Aug. 1 that second-quarter net income rose 19 percent, according to the median estimate of 19 analysts surveyed by Bloomberg. The fixed-income group, overseen by 44-year-old global markets chief Anshu Jain, produced about 33 percent of the company's revenue in the quarter, analysts said.

``With the situation in the U.S. subprime market worsening, I can't imagine Deutsche Bank changing its position,'' said Radinger.

Mortgage defaults would surge as soon as price appreciation slowed, Xu wrote in September 2005. Since then, Deutsche Bank traders, led by Greg Lippmann, sold ABX index contracts, providing 200 million euros ($272 million) of revenue in the first quarter and possibly another 200 million euros in the past quarter, assuming the position wasn't changed, said Kinner Lakhani, the top-rated banking analyst at ABN Amro Holding NV in London.

Subprime `Contamination'

The ABX-HE-BBB- 06-1 index, tied to mortgage-backed bonds with the lowest investment-grade ratings, fell 17 percent last week, increasing this year's drop to more than 60 percent, according to London-based Markit Group Inc., administrator of the ABX indexes.

Jain, Lippmann and Xu declined to comment.

Trading profits may help Deutsche Bank overcome declines in fees from underwriting mortgage-backed securities and a potential revenue slide at the MortgageIT Holdings Inc. and Chapel Funding LLC units in the U.S., according to analysts. The bank has said it gets less than 2 percent of revenue from residential mortgage- backed securities.

After Deutsche Bank reports earnings, ``the question will be more about whether there is contamination of subprime to other areas,'' said Jean Sassus, a Paris-based analyst at Raymond James Financial Inc., who has a ``fair value'' rating on the company's stock.

Cracks in LBOs

Deutsche Bank was paid almost $550 million of fees by leveraged buyout firms in the first half for advising and financing takeovers, data compiled by New York-based Freeman & Co. and Thomson Financial show. That may drop in the second half as LBO firms scale back their record pace of acquisitions.

Last week, Deutsche Bank was among banks forced to hold on to 5 billion pounds ($10.1 billion) of loans for Kohlberg Kravis Roberts & Co.'s purchase of U.K.-based pharmacy chain Alliance Boots Plc as investors balk at riskier assets following losses in the U.S. subprime mortgage market.

Deutsche Bank's stock fell 5.8 percent last week on concern that debt market declines would hurt earnings in the second half of 2007. The company probably outperformed its European competitors in the second quarter, said Andreas Weese, a Munich- based analyst at UniCredit SpA, who recommends investors ``buy'' Deutsche Bank shares.

Dillon Read

``Deutsche Bank was well prepared for the subprime crisis,'' Weese said. ``Others clearly got caught on the wrong foot'' of loans to people with bad credit records, he said.

UBS, Switzerland's biggest bank, may report Aug. 14 that second-quarter net income fell 7.5 percent, excluding a one-time gain of 2 billion Swiss francs ($1.65 billion) from the sale of Julius Baer Holding AG shares, according to estimates by Matthew Clark, a London-based analyst at Keefe, Bruyette & Woods Ltd.

Dillon Read Capital Management LLC, one of UBS's hedge-fund units, collapsed in May after more than $120 million of losses from mortgage-related holdings. Dillon Read probably cost UBS another 150 million francs in the second quarter, said Clark, who has a ``market perform'' rating on UBS.

``We know UBS still had trading exposure to subprime at least at the start of May and they would have had difficulty unwinding those positions,'' Clark said. The debacle led to the ouster of Peter Wuffli as chief executive officer earlier this month.

Xu's Job Change

HSBC, Europe's largest bank by market value, reported today that first-half net income climbed 25 percent to $10.9 billion, helped by asset sales in China and lower taxes. Costs for potential bad loans rose 63 percent to almost $6.4 billion and pretax earnings in North America fell 35 percent to $2.4 billion.

Shares of Deutsche Bank advanced 7.4 percent during the past 12 months, compared with the 1.6 percent drop of UBS and the 9.6 percent decline of HSBC.

Xu, who was born in Shanghai and has a doctorate in mathematics from the University of California in Los Angeles, analyzed U.S. mortgage lending practices in August 2005. He found that banks were lowering their prices and standards as competition for new clients increased. Lower-rated mortgage- backed bonds were ``ripe for a correction,'' he wrote.

A year later, Xu moved to Lippmann's trading desk. Lippmann, 38, is Deutsche Bank's head of asset-backed securities trading in New York.

ABX Index

The traders started selling the ABX index contracts in late 2006 because they ``felt that the U.S. mortgage market was probably overheating and would potentially soften,'' Deutsche Bank Chief Financial Officer Anthony di Iorio said in May.

Deutsche Bank was among the firms that helped create the ABX.HE index in January 2006. The credit-derivatives index provides mortgage-backed bondholders with insurance against defaults on U.S. home loans. Bondholders can use the index to hedge against losses spurred by an increase in mortgage defaults or to bet on the credit quality of the debt.

Derivatives are financial instruments derived from bonds, loans, stocks, currencies and commodities, or linked to specific events like changes in the weather or interest rates.

Jain, who started his career as a derivatives strategist at Merrill Lynch & Co. and was brought to Deutsche Bank by Edson Mitchell in 1995, said earlier this month that he doesn't expect widespread panic in the subprime market.

``Most of the participants in this market are real money investors who don't employ irresponsible leverage ratios,'' he told the Financial Times on July 12. Losses are concentrated in subprime loans made in 2006, he said.

Beating Goldman

Deutsche Bank was the seventh-ranked underwriter of ``home- equity'' securities last year, most of which were backed by subprime or second mortgages, according to industry newsletter Inside MBS & ABS in Bethesda, Maryland.

The debt trading unit, which Jain has overseen since 2001, hasn't recorded a year-over-year decline in revenue for 11 straight quarters. Deutsche Bank may surpass New York-based Citigroup Inc., the biggest U.S. bank, and New York-based Goldman Sachs Group Inc. as the world's biggest fixed-income trader, when it reports a 10 percent gain in second-quarter revenue to 2.7 billion euros, analysts estimate.

Goldman, the biggest U.S. securities firm by market value, said last month that lower demand for mortgage-backed bonds caused the biggest quarterly drop in its fixed-income revenue in almost four years.

http://www.bloomberg.com/apps/...20601109&sid=a.Ttj0n4GmwI&refer=home

URL: http://www.spiegel.de/wirtschaft/0,1518,497271,00.html

FINANZAKTIEN IM MINUS

Sorge um Banken lähmt die Börsen

An der Börse geht die Angst um: Die Krise auf dem US-Immobilienmarkt hat erstmals auch ein deutsches Kreditinstitut erfasst - die Mittelstandsbank IKB. Ihr Aktienkurs fällt dramatisch, auch andere Finanztitel geben nach - und ziehen den Dax nach unten.

Frankfurt am Main - Die zunehmende Furcht vor einer Ausweitung der US-Hypothekenkrise auf die europäischen Märkte hat Börsenhändlern heute die Stimmung vermiest. Von den Bankentiteln im Dax notierte am frühen Nachmittag kein einziger im Plus. Am schlimmsten erwischte es die Commerzbank - sie gab bis 14.30 Uhr rund 3,7 Prozent ab. Auch die Deutsche Bank verlor fast 1,9 Prozent. Auch die Postbank verlor, ebenso wie die Dresdner-Bank-Mutter Allianz . Das Minus bei den Finanztiteln zog den Dax insgesamt nach unten, der 0,55 Prozent verlor und bei 7410 Punkten notierte.

"Nachdem IKB die Krise am US-Immobilienmarkt zum Anlass für eine Gewinnwarnung genommen hat, geht jetzt die Angst um", sagte ein Händler in Frankfurt. In der Nacht hatte die Düsseldorfer Mittelstandsbank IKB ihre Profitprognose gesenkt und einen überraschenden Wechsel an der Konzernspitze mitgeteilt: Stefan Ortseifen sei als Mitglied und Sprecher des Vorstands ausgeschieden. Neuer Vorstandschef sei das KfW-Vorstandsmitglied Günther Bräunig, teilte die IKB mit.

Die Krise war offenbar ernst. In der Mitteilung hieß es, wegen der Probleme am US-Immobilienmarkt und der damit einhergehenden Verunsicherung sei die Bonität der IKB gefährdet gewesen. Die KfW, die 38 Prozent der IKB besitzt, musste einschreiten. Sie habe "die notwendigen Maßnahmen getroffen", um die Bonität der IKB zu sichern, hieß es. Die KfW leiste "damit einen wesentlichen Beitrag zur Stabilisierung des Marktes".

Die Börsen straften die IKB heute ab, ihre Aktie verlor bis 14.30 Uhr fast 24 Prozent.

Warten auf den Branchenprimus

Die Probleme am US-Hypothekenmarkt belasten die Börsen seit Monaten. Mehr als 50 amerikanische Finanzierer sind Bankrott gegangen oder haben sich selbst verkauft. Am härtesten hat es Institute getroffen, die sich auf Kreditnehmer mit niedriger Bonität konzentriert haben - das sogenannte Subprime-Geschäft.

Mit Nervosität warten die Märkte nun auf die Deutsche Bank - sie wird am Mittwoch über den Verlauf des zweiten Quartals berichten. Nach Ansicht von Analysten hat der Branchenprimus zwar weiter von den lebhaften Kapitalmärkten profitiert. Vor allem getrieben von einem starken Handelsergebnis hat er wohl rund ein Fünftel mehr als im Vorjahr verdient.

Die Analysten erwarten aber vor allem nähere Informationen zu den Auswirkungen der US-Immobilienkrise auf die Deutsche Bank. Ihr Risikovorstand (Chief Risk Officer), Hugo Bänziger, hatte allerdings schon Anfang des Monats darauf verwiesen, dass man die Anzeichen für die Probleme auf dem Subprime-Markt frühzeitig gesehen und Konsequenzen gezogen habe.

Analyst Andreas Weese von der UniCredit-Tochter HVB hält die momentane Stimmung für übertrieben. Die wachsende Nervosität im Markt dürfte sich nach den guten Quartalszahlen der Deutschen Bank etwas beruhigen, erwartet er. Auch die Entwicklung bei den US-Investmentbanken habe gezeigt, dass das Umfeld nach wie vor sehr günstig ist, schreibt der HVB-Experte.

Ein Commerzbank-Sprecher sagte der Nachrichtenagentur AP auf Anfrage, weder die Commerzbank noch ihre Tochter Eurohypo gäben direkte Kredite an Privatkunden in den USA. In überschaubarem Umfang sei man am Verbriefungsgeschäft mit diesen Krediten beteiligt. Bei der Verbriefung wird ein Kredit oder sein Risiko am Kapitalmarkt verkauft.

Immerhin die Aktie der britischen HSBC stemmte sich heute gegen den Negativtrend. Sie hat in der ersten Hälfte des Jahres gut verdient - die Aktie verteuerte sich um knapp 2,5 Prozent.

itz/dpa/dpa-AFX/Reuters/AP

Am Freitag bin ich Long gegangen, habs aber wegen falscher Ein- und Ausstiege vermasselt. Heute habe ich bei Dax 7400 alle meine Shorts glattgestellt und bin wieder Long gegangen. Das war deutlich besser gelaufen. Mein Eindruck beim Beobachten des Marktes "Tick für Tick" war, dass er nach oben "will". Selbst schlechte News haben ihn nicht mehr gedrückt, was sentimenttechnisch zu erwarten war (s.o.)

Natürlich muss in der jetzigen Situation klar sein, dass eine Longspekulation zwar sehr lukrativ sein, aber binnen Minuten in die Hose gehen kann. Extreme Vorsicht ist also angesagt.

Sowood, which manages $3 billion, said July 27 that returns fell as investors fled riskier debt such as subprime-mortgages and bonds used to fund leveraged buyouts. The risk of owning corporate bonds soared today to the highest on record in the U.S. and Europe, credit-default swaps show.

``This transaction provides for an orderly transference of risk between the parties,'' Kenneth Griffin, Citadel's president and chief executive officer, said today in a statement.

Bryan Locke, a Citadel spokesman, declined to comment. Megan Kelleher, Sowood's general counsel and a managing partner, didn't immediately return calls seeking comment.

Citadel, which manages $14 billion, and JPMorgan Chase & Co. took over the energy trades of Amaranth Advisors LLC when the Greenwich, Connecticut-based hedge fund collapsed under the weight of more than $4.6 billion in losses on natural gas. Citadel later bought the positions held by New York-based JPMorgan.

Sowood, started by former Harvard University endowment manager Jeff Larson, uses a variety of strategies in trading convertible bonds, commodities, bonds and stocks. As of March 31, the fund owned about $6.4 billion in stocks, according to a U.S. Securities and Exchange Commission document.

Harvard a Client

Larson, 49, opened Sowood in 2004 and early investors included his previous employer, Harvard, which put in $500 million. He joined the university's investment unit, Harvard Management Co. of Boston, in 1991 from the finance division of Cargill Inc., the largest U.S. agricultural company. He started at Cargill in 1979 as an economic analyst.

At Harvard, Larson managed foreign stocks and a commodities portfolio and ran about $3 billion of the endowment of the Cambridge, Massachusetts, university. He earned $17.3 million in 2003, a year when Harvard paid more than $100 million to internal money managers, raising the ire of alumni.

Harvard's $30 billion endowment, the largest for a university, was to increase its allocation to Sowood's hedge fund and a separate private-equity fund this year, according to a December statement from Sowood. The private-equity fund was spun off this month as Boston-based Denham Capital Management LP.

John Longbrake, a university spokesman, declined to comment. Mohamed El-Erian, CEO of Harvard Management, didn't immediately return phone calls.

Seeking Higher Returns

El-Erian said in the December statement that splitting the hedge-fund and private-equity businesses would boost returns for both. The Harvard fund was the sole initial investor in the Sowood private-equity fund, whose assets increased 10-fold in two years to $2.3 billion as of December.

Sowood's name came from ``South Woodside Avenue,'' the street in Wellesley, a suburb of Boston, where Larson lived when he started at Harvard Management. The fund raised $2 billion before closing to new investors.

Hedge funds are largely unregistered pools of capital that cater to wealthy individuals and institutions and allow managers to participate substantially in profits from investments. They control about $1.74 trillion, more than double the amount five ago.

http://www.bloomberg.com/apps/...20601087&sid=aT31Y.pPjvAs&refer=home

American Home Mortgage Investment Corp. shares plunged 45 percent, the most in at least three years, after the lender delayed its quarterly dividend and raised doubts about whether it has enough cash to stay in business.

Shares of the Melville, New York-based mortgage company, which specializes in loans to people who fall just short of top credit scores, fell to $5.80 as of 9 a.m. today. Trading was halted before the regular opening of the New York Stock Exchange. The stock closed at $10.47 on July 27. As recently as December, the shares sold for about $36.

American Home said in a statement it needs a ``better understanding'' of how it will be affected by weak mortgage markets. The delay may add to investor concern that bad loans in the U.S. have spread beyond subprime borrowers who have the worst credit records. The company's credibility may be in doubt, and its survival ``is not a foregone conclusion,'' RBC Capital Markets analyst James Ackor wrote today.

``The writedowns this quarter were pretty significant,'' said Bose George, an analyst at KBW Inc. ``The $1 billion of cash they started the quarter with has gone down pretty materially.''

American Home said in a statement after trading ended last week that the board delayed common dividends and may halt preferred-share payouts. The quarterly common dividend was cut in April by 38 percent to 70 cents.

More Collateral

The company said it reduced the value of assets on its books and that Wall Street firms and lenders are demanding more collateral. Delaying the dividends will allow American Home to retain about $42 million in cash each quarter, George wrote in a note. He reduced his estimate of full-year earnings to a loss of $269 million, compared with a previous estimate for a profit of more than $70 million.

``The recent and severe erosion in the global debt markets was rapid and unforeseen,'' RBC's Ackor wrote. ``We are increasingly concerned that American Home's management does not have a firm grasp on the external issues facing the company.'' Ackor cut his rating to ``sector perform-speculative'' from ``outperform-average.''

The lender specializes in Alt-A mortgages, an alternative for A-rated borrowers who can't satisfy all the terms for a regular ``prime'' mortgage. The company was the 20th-largest Alt- A lender in 2006, according to March data from trade publication Inside Mortgage Finance.

Falling Profit

The company said in June that second-quarter profit would be lower because homeowners didn't keep up with payments, forcing the company to buy back loans that had been sold to investors.

Bids from investors began falling earlier this year as defaults on U.S. subprime mortgages were rising to the highest level since 2002.

American Home is organized as a real estate investment trust. Such companies are required by law to pay out most of their profit in dividends, with individual shareholders bearing the tax burden.

Earlier this month, American Home disclosed it fired 200 people as business slowed. The company employed 7,409 at the end of last year, according to Bloomberg data.

Mary Feder, a spokeswoman for American Home, didn't immediately return a call seeking comment.

Shares of rival home lenders fell today, with Impac Mortgage Holdings Inc. down as much as 13 percent and NovaStar Financial Inc. falling almost 17 percent. IndyMac Bancorp Inc., the largest U.S. Alt-A lender, fell as much as 12 percent. IndyMac reports earnings tomorrow.

http://www.bloomberg.com/apps/...20601087&sid=aLQDu0lpHv3E&refer=home

[...]

Certainly, these are all issues that demand out attention, and the fact that investors were more eager to protect their capital into the weekend than loading up in hopes of catching the next mega-merger announcement indicates that this market may have undergone a fundamental shift in character. Still, the serious technical damage that the major indices took this past week happened so quickly that there will likely be some sort of reflexive bounce pretty soon. However, just because the stock market cheerleaders will be doing their “I Told You So” dance if that does happen, we need to watch how high we bounce as well as the degree to which it holds. That, in turn, will give us pretty good clue as to where we may be headed as we move forward. Regardless, prudent investors will resist the temptation to succumb to the sturm und drang of emotion out there and keep an even keel until there are definite signs that things have stabilized.

[...]

Wohl geschrieben!

P.S.

1) market cheerleaders = Raimund Brichta? Der "ahnte" es ja auch vorher - zumindest schrieb er das heute.

2) "Sturm und Drang" - ein Germanismus im Englischen. Herrlich!