Canadian Solar- eine der grössten Solarfirmen

Summary

The company exceeds its own guidance on top and bottom lines.

YieldCo is key to the company's future success.

The stock is undervalued, but not based on multiples comparison.

What may worry investors

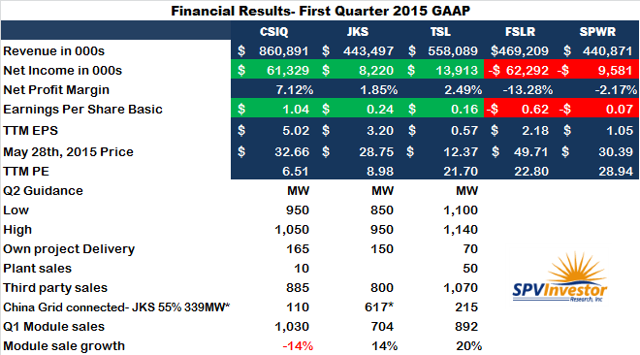

Despite the great first-quarter earnings, Canadian Solar offered a soft second quarter outlook, forecasting revenues between $570-620 million and a disappointing 13-15% gross margins. During the conference call, the company actually forecast stabilizing module ASPs in the second half of the year due to stronger demand. Moreover, the company has been consistently lowering its manufacturing cost.

According to the investor presentation, the manufacturing cost has decreased significantly from $1.32/W in 2011 to $0.49/W at the end of Q4 2014. The declining costs and stabilizing ASPs will all together help stabilizing the gross margins towards the end of 2015. The declining margins and profitability in the short term is mainly due to the fact that the company now focuses on retaining the solar projects rather than selling them upfront. From the scheduled list, we can see that the company only has one 14MW utility-scale project to sell in Ontario in the second quarter of 2015. By retaining the solar projects on the balance sheet, Canadian Solar will be better positioned to launching the long-awaited YieldCo, which has been favored by many investors....

The company has made it clear that it is going to evaluate all solar projects in its pipeline and drop them into the YieldCo in late 2015 or early 2016. Let us review the company's current late-stage project pipeline that is expected to be included in the YieldCo:

UK - 40.2MWp connected to grid. 52.5MWp to be completed by 2015

USA - 1,021MW, with expected COD in 2016

China - 340MW DC of projects, with 320MW DC expected to be connected in 2015

Japan - 720MW DC; 262MW DC of projects have full grid connection approval. 45MWp of projects are expected to be completed in 2015

Brazil - 114MW DC to be connected in 2016, and electricity generated will be purchased by the government under a 20-year PPA

Source: Investor Presentation, Apr 2015

The story does not end here as the above list only shows the company's late-stage pipeline. The company currently has a total project pipeline of 8.5GW given the Recurrent Energy acquisition. Given the quality pipeline and the upcoming YieldCo, Canadian Solar will have greater earnings visibility well beyond 2016.Investors will pay a premium for the earnings visibility and stability in the solar business, as the solar industry traditionally has been viewed as a volatile business with no earnings stability. For example, SunEdison (NYSE:SUNE) is currently trading at over $7 billion in market cap while the business has not had a positive earnings since 2012.

.......

Canadian Solar indeed looks quite undervalued based on all three measures. However, I personally disagree when investors claim the stock is undervalued based on these multiples alone. First of all, Canadian Solar, like it or not, is still perceived as a commodity solar module producer (the module ASPs will never return to the level we saw back in 2010) while solar companies like SunPower and First Solar are perceived to be operating in the higher-margin solar project and solutions business. The Street is not going to give a premium for the commodity module producer due to the declining average selling prices for solar modules.

You may argue that ASPs can stabilize starting in the second half of the year given a stronger demand. However, the general trend and consensus in the solar industry favors a sustained decline in solar PV prices in the next decade. As a result, the solar module producers will never be able to return to the same level of profitability they enjoyed in 2010......

I believe Canadian Solar is undervalued based on its existing project pipeline, the future YieldCo business plan, and its proven and successful business model transition and execution under the right leadership.

In summary, the company may indeed have a soft second quarter, but this should not matter if you believe in the success of its upcoming YieldCo and more importantly, the company's ability and ambition to be one of the best solar energy providers in the world.

http://seekingalpha.com/article/...ian-solar-and-you-will-not-regret?

http://static.cdn-seekingalpha.com/uploads/2015/6/...-Robert-Dydo.png

{kind=link}

beeindruckend Canadian Solar !

http://seekingalpha.com/article/...esting-after-first-quarter-results

...The Canadian Solar Yieldco will have 1.8GW of projects available for drop down in the next three years, and will probably start with 400MW as well for the initial transfer. I know of 155MW in the UK, 45MW in Japan, and 28MW in Canada. The rest could be assigned to the Yieldco from the US pool of Recurrent's projects in the unfinished state. There is no IPO registration done, and the company is still negotiating incorporation of the holding company with a preference for the UK. Under open door speculation, I can see Canadian listing in Hong Kong and as a partner in the listing with another company(s). In this case, the gap of projects would be filled by others. Canadian will consolidate the Yieldco, and thus will have a format similar to SunEdison's reporting, or at least what I foresee it to be right now....... Canadian went out of its way to definitely not have Chinese assets in the Yieldco IPO. The company claims curtailment and long (up to 2 years) periods of no FiT payments.Jinko describes six to nine months of DSO (days sales outstanding) on energy and currently collects unpaid, owed amounts in accounts payable....

...I prefer to look toward companies offering all-round abilities, with strong manufacturing, efficiency, project development and investment structures benefiting shareholders the most. In this circumstance, despite its lower efficiency and cost dependency on cell prices, Canadian offers that format. The company is trying to skip the middle man and get into the distribution markets, including macrogrids to gain extra percentiles in gross margin. They are buyers/developers of PERC cell structure design and have a nice, but still theoretical efficiency path. Their reluctance to spend now on efficiency is understandable due to a need for equity for projects, but they will get there in time.

http://investors.canadiansolar.com/...irol-newsArticle&ID=2060049

premaket +063%

Die zwei PV-Anlagen in Kanada haben jeweils eine Leistung von 10-Megawatt, ...

http://www.it-times.de/news/...bkommen-mit-der-deutschen-bank-111915/

Summary

Canadian Solar has shown an above-market price return and maintains top operating margins in its peer group.

Despite that, the stock receives below-market valuation. Some people attribute this to the company's commodity business and its "Chinese profile". I find a solution to that.

My DCF analysis showed that the stock is significantly undervalued and offers a tremendous risk-adjusted return to investors. Check my assumptions in the model.

..... As I went down the lines, I saw that, in the first time in the last five years, the company did not experience currency exchange losses, which amounted to 28% of operating income (median figure). Despite that, even if readers adjust the numbers for the currency exchange losses, the stock will remain the most undervalued company in the peer list....

Opinion

I issue a BUY recommendation on the shares of Canadian Solar Inc. with a target price range of $55-$70 per share, which represents a 66%-112% upside opportunity. I think that this stock is the most undervalued company I have analyzed in my 100 articles over the last two years.

...completed the sale of LunarLight, a 10 megawatt ("MW") AC solar power plant to a subsidiary of BluEarth Renewables Inc. ("BluEarth"). LunarLight, located in Belleville, Ontario, is the last in a series of power plants acquired by BluEarth from Canadian Solar. The facility is valued at approximately C$65 million (USD$53 million) and uses Canadian Solar'sCS6X-300/305P modules made in Canada. ....

http://www.nasdaq.com/press-release/...ant-to-bluearth-20150623-00173

Optionen

| Boardmail an "Skorp" |

Wertpapier: Canadian Solar Inc |

Habe keine Zeit sowas zu übersetzen aber Google hilft

Schon klasse, wie gut sich Canadian Solar damit in dem stark wachsenden indischen Solarmarkt aufgestellt hat.

http://renewables.seenews.com/news/...pv-parks-in-india-report-483831

Optionen

| Boardmail an "Juliette" |

Wertpapier: Canadian Solar Inc |

Summary

CSIQ is an industry leader in sales and earnings growth, generating consistently impressive returns.

The impact of US and EU tariffs on PV panels produced in China will be offset by growth in other markets.

Diversification into residential solar and the introduction of new products, such as a new battery offering similar to the Powerwall, will help fuel future growth.

........

http://www.prnewswire.com/news-releases/...erence-call-300119570.html

Optionen

| Boardmail an "Skorp" |

Wertpapier: Canadian Solar Inc |

Optionen

| Boardmail an "Skorp" |

Wertpapier: Canadian Solar Inc |

Optionen

| Boardmail an "Eskimoo" |

Wertpapier: Canadian Solar Inc |

The Obama administration has vowed for CO2 reduction of 28% by 2025 and 32% by 2030, from 2005 levels. This version turns out to be a little stronger than the draft proposal released last summer wherein the EPA had proposed total CO2 reduction of 29% by 2025 and 30% by 2030.

The plan sets carbon pollution reduction goals for power plants and requires states to implement plans to meet these goals. States have until Sep 2016 to submit plans, but all must comply by 2022.

Obama faces stiff opposition on climate issues from the Republicans in the Congress. The Republicans contend that the climate change deal will be economically damaging for the U.S. economy, middle-class families and struggling miners. Coal mining states such as Wyoming, West Virginia and Kentucky fear that their economies would suffer and people would be laid off.... Obama brushed off the notion that his plan was a "War on Coal" ruthlessly killing jobs. The President said that he is reinvesting in areas of the U.S. previously known as "coal country."

.....

Although it’s debatable whether Obama's broader climate plan can solve climate change, this is certainly one of the most historic and ambitious climate rules, given that power plants account for 31% of U.S. greenhouse gas emissions. The Clean Power Plan has unmistakably put renewable energy companies in sharp focus.

Sunedison,Sunpower ...

Canadian Solar Inc. CSIQ

Canadian Solar caters to a geographically diverse customer base spread across key markets in the U.S., Canada and Europe, as well as emerging markets like South Korea, Singapore and Brazil. The company, which has a strong pipeline of projects, continues to engage in acquisitions and adopt various strategies to further consolidate its position. During the first quarter of 2015, it acquired Recurrent Energy, LLC, a leading North American solar energy developer, thereby strengthening its hold in the business of ownership and development of solar power plants in North America.

Canadian Solar presently holds a Zacks Rank #3 (Hold) and is trading at a forward PE of 11.34x.