Immunocellular therapeutics WKN: A0MVAX

Seite 1 von 17 Neuester Beitrag: 25.04.21 02:02 | ||||

| Eröffnet am: | 28.08.11 07:47 | von: Chalifmann3 | Anzahl Beiträge: | 412 |

| Neuester Beitrag: | 25.04.21 02:02 | von: Mariaggjea | Leser gesamt: | 95.697 |

| Forum: | Hot-Stocks | Leser heute: | 12 | |

| Bewertet mit: | ||||

| Seite: < | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | ... 17 > | ||||

On the subject of Dendreon and Provenge, it's tough to leave Immunocellular Therapeutics (IMUC.ob) out of the conversation, as this company may be following in Dendreon's footsteps to become the leader of the next generation of cancer immunotherapy treatment.

Because Immunocellular views its technology as the next step in the realm of cancer immunotherapies, one should also consider the company as a perpetual candidate to either be bought out or land a major partnership.

IMUC's technology, from which lead candidate ICT-107 was devised for the treatment of glioblastoma (GBM), attacks the stem cells behind the growth and spreading of cancer. Maybe even more important than the step forward in the technology, however, may be the logistical advantages that the company has developed in production and manufacturing, which significantly reduces the costs associated with production.

Given that much of Dendreon's recent troubles stem from the high cost of Provenge treatment, IMUC's logistical advantage should be noted. Patients treated with ICT-107, for example, need to have their dendritic cells harvested only once, while those receiving Provenge need this process conducted three times during treatment, elevating the cost of treatment.

ICT-107 is still a Phase II product, but the development of this treatment and the technology should be monitored by investors of the sector, with DNDN being the example of what comes with a successful cancer immunotherapy stock.

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: ImmunoCellular Therapeu |

Angehängte Grafik:

a015.gif

a015.gif

vom Entwicklungspotential dieses Unternehmens wirklich begeistert.

Vorallem weil es das bekannte Krebsmittel Avastin von welchem sich die Chemiebranche

in weiteren Studienphasen viel verspricht (ein Milliardenmarkt), jetzt schon um Längen

schlägt, in Punkto Wirkungsgrad und Nebenwirkungen.

Immunocellular Therapeutics Ltd, ist ein kleines Onkologie-Unternehmen, dass sich

auf die Entwicklung der aktiven Immuntherapie und Impfstoffe gegen Krebs konzentriert.

Das Produkt-Portfolio umfasst zelluläre Immuntherapien gegen Krebs und auf Krebs-

stammzellen Antigenen basierenden Immuntherapien gegen Krebs.

Im weiteren wird auch auf dem Gebiet der Antikörper zur Diagnose und Behandlung

verschiedener Krebsarten geforscht.

Sein Spitzenkandidat ICT-107, hat kürzlich sehr erfolgreiche Aktivitäten in (GBM),

einer sehr agressiven Hirntumorart erzeugt.

Diese einzigartige Therapieform ist inzwischen zu einer grossen (Phase II Studie)

gelangt!

Die Ergebnisse der (Phase I Studie) von ICT-107 in (GBM), welche im Mai 2007 begannen,

waren sehr erfolgreich.

Die 2-Jahres Überlebensrate der Patienten konnte mit 80,2% im Vergleich zu den 26,5%

der Standard Versorgung (Chemo-Therapie, Bestrahlung etc.), extrem gesteigert werden.

Von 16 Tumorpatienten sind drei Patienten, seit 4 Jahren von der Erkrankung befreit.

Bei weiteren 6 Patienten konnte das Wachsum des agressiven Tumors gestoppt werden.

Im Gegensatz zum bekannten Krebsmittel Avastin, das Potential für schwere toxische

Nebenwirkungen hat, wurden bei der Behandlung mit ICT-107, von keinen grossen

Beschwerden berichtet.

Die Zukunft sieht vielversprechend für ImmunoCellular Therapeutics aus.

Die Studiendaten zur (Phase II Studie) von ICT-107, werden in der zweiten Hälfte

des Jahres 2012 erwartet.

Die Ergebnisse sollten die Position von Immuno Cellular Therapeutics, als einer der

vielversprechendsten Immuntherapie gegen Krebs deutlich festigen.

Das Unternehmen ist derzeit mit einem share price von 1.7 $ und einer

Marktkapitalisierung von unter 60mio $ , deutlich unterbewertet, wenn man

vom enormen Entwicklungspotential ausgeht, welche durch die abgeschlossene

und fundamental sehr positiv ausgefallene (Phase I Studie) von ICT-107 schon

deutlich untermauert wird.

Immuno cellular therapeutics (OTC:IMUC)

(Quelle: proaktivinvestors australia / Jason Chew / 8. Juni 2011)

Optionen

| Boardmail an "bigbangbowler2" |

Wertpapier: ImmunoCellular Therapeu |

ich bin vor einigen wochen in einer science/medicine zeitschrift auf die gestossen.

es wurden die ICT-107 ergebnisse der pos. phase I studie ausführlich erläutert, aber auch ICT-121 u. - ich erinnere mich kaum - noch einige präparate der gruppe monoklone antikörper inkl. US-patenitiertem hautkrebspräparat ICT-69

weiters sehr gelobt wurde aufgrund enger kooperationen mit u.a. uni-einrichtungen die innovative forschungsarbeit auf diesem bislang noch nicht so erforschtem sektor.

sieht aus als wäre immuno cellular in der immuntherapie dem mitbewerb um lichtjahre voraus!

Optionen

| Boardmail an "lady luck" |

Wertpapier: ImmunoCellular Therapeu |

Optionen

| Boardmail an "lady luck" |

Wertpapier: ImmunoCellular Therapeu |

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: ImmunoCellular Therapeu |

Angehängte Grafik:

z.png (verkleinert auf 63%)

z.png (verkleinert auf 63%)

happy search and good luck

Optionen

| Boardmail an "lady luck" |

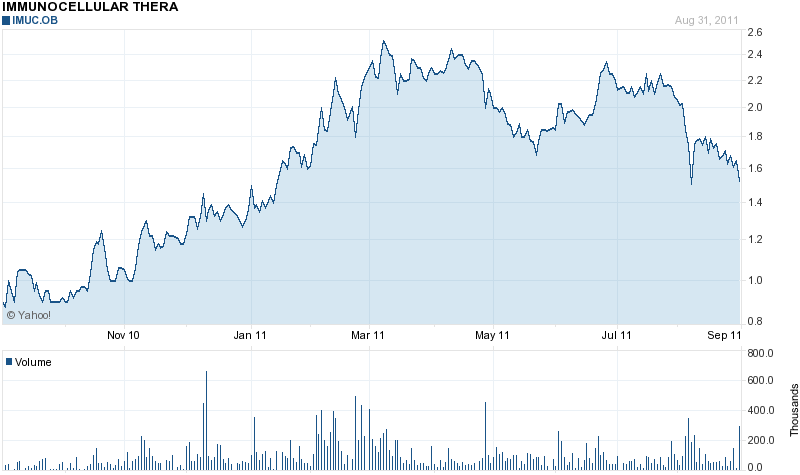

Wertpapier: ImmunoCellular Therapeu |

Angehängte Grafik:

imuc_090111_lalu.png (verkleinert auf 72%)

imuc_090111_lalu.png (verkleinert auf 72%)

Optionen

| Boardmail an "lady luck" |

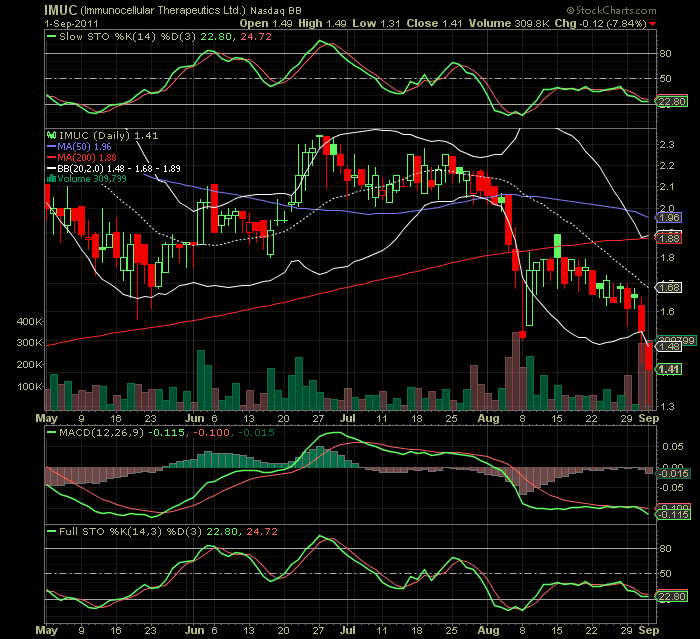

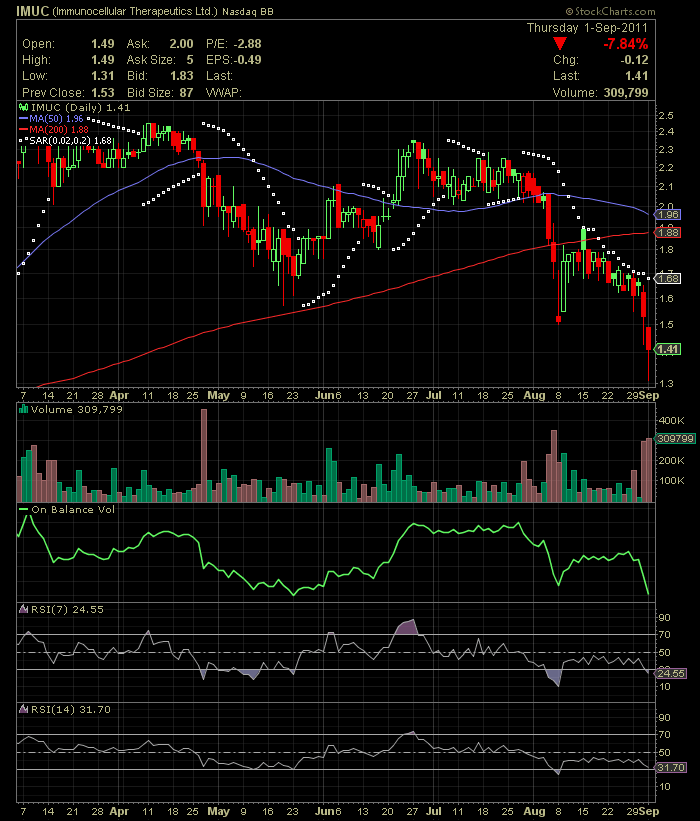

Wertpapier: ImmunoCellular Therapeu |

Angehängte Grafik:

imucii_090211_lalu.png (verkleinert auf 72%)

imucii_090211_lalu.png (verkleinert auf 72%)

Optionen

| Boardmail an "lady luck" |

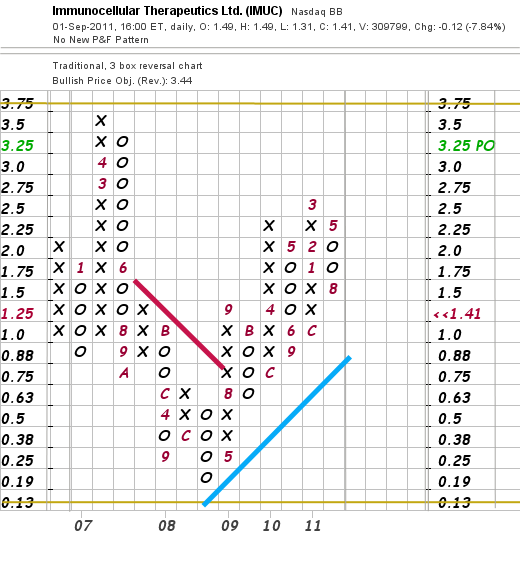

Wertpapier: ImmunoCellular Therapeu |

Angehängte Grafik:

imuc_p_f_0901.png (verkleinert auf 98%)

imuc_p_f_0901.png (verkleinert auf 98%)

Optionen

| Boardmail an "lady luck" |

Wertpapier: ImmunoCellular Therapeu |

MarKap 53 Mio $ find ich iMo mehr als ausreichend

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: ImmunoCellular Therapeu |

Angehängte Grafik:

k020.gif

k020.gif

According to the company, a joint venture named Neptune-SKFC Biotechnology will manufacture and commercialize Neptune's krill products in Asia, the world's largest market for such products.

We told our subscribers last Thursday (when shares were trading at $3.06) that Neptune shares had been dealing with 3 non-fundamental/artificial sources of downward pressure which were starting to dissipate. By Friday, when our report was released to the rest of our readership, shares had climbed to $3.39.

In our report on Friday, we said that we would follow up the story early this week "with more information on some of the upcoming catalysts that should spur more buying in the stock and leave shareholder happy; perhaps even pleasantly surprised." While today's news was welcome, we continue to expect even more positive catalysts for NEPT in the short term. That follow up report is being prepared and more details will follow.

As we promised last week, we're going to take some time to discuss some of the new companies, which stood out to us at the recent Rodman & Renshaw Healthcare Conference in New York - easily the single biggest healthcare/biotech investment conference of the year.

It was certainly nice to see that the conference was buzzing with activity. The markets may appear gloomy and unpredictable, but those sentiments appear to be a far cry from 2008 levels. There was definitely a sense of optimism and a certain upbeat atmosphere in the air, complete with plenty of investors and deal makers floating back and forth between presentation sessions. . While some commented that Rodman has not been doing as many money raises as it has in previous years, some of the fund and institutional types at the event seemed eager to not only take in the live presentations during the day, they were also eager to attend the after hour cocktail parties and mixers. We can report many standing-room only affaiirs of both flavors. In fact, institutional buyers were apparently quite interested in snagging some of the suddenly discounted shares of companies we actively cover here. Thus the recent strength of Immunocellular Therapeutics (IMUC.OB), whose shares have broken their recent downtrend and have become very active since the conference. Successful presentations and road shows will do that for you.

There were quite a few companies presenting for the first time at this year's conference, and as usual, we focused most of our attention some of the emerging names from the vast list of presenters - often asking small cap fund managers what companies they had heard what about.

One, focused on the battle against dyslipidemia (high blood cholesterol levels), which isn't even trading publicly, made people take notice when it took on Amarin Corporation (Nasdaq:AMRN) during its presentation. Omthera Pharmaceuticals President & CEO Jerry Wisler stated that Amarin has been using liquid paraffin, or mineral oil, as their placebo for the AMR-101 clinical trials. We scanned the room and saw a bunch of whispers and gasps flying after that statement, since one would think that the use of either liquid would definitely slant the clinical trial results. We contacted the firm afterward to make sure we had heard the statement correctly, and the helpful investor relations person verified the statement. Omthera recently announced that the first patient has been enrolled in its ESPRIT Phase III clinical trial of prescription Omega-3 free fatty acid, Epanova™, in patients with hypertriglyceridemia (TG level ≥200 and < 500 mg/dL) receiving statin treatment.

Interestingly, the trial has been granted a Special Protocol Assessment (SPA) from the U.S. Food and Drug Administration and the company now has two Phase III studies under way. The product, Epanova™ is an Omega 3 fatty acid containing a novel formulation of eicosapentaenoic acid (EPA) and docosahexaenoic acid (DHA), which is expected to provide superior absorption characteristics and bioavailability versus the ethyl ester form found in other prescription Omega 3s. Absorption characteristics of Epanova™ are enhanced via a proprietary capsule and capsule coating that delays absorption to the small intestine with "superior release kinetics."

The good: Funded in 2008, the company has been able to push the clinical ball quite a way up the field - raising an estimated $40 million along the way (pdf) - without having to go public. The bad: They aren't publicly traded (at least not yet). Going forward: The firm believes superior bioavailability and greater dosing flexibility will enable its Epanova omega-3 fatty acid to compete in the $1 billion market for lipid-lowering drugs now occupied by Lovaza. Co-founder Michael Davidson says (pdf) Epanova™ is a mixture of the free fattyacid forms of the omega-3 fatty acidseicosapentaenoic acid (EPA) and docosahexaenoicacid (DHA), both of which lower triglycerides by mechanisms that are not well understood. “Free fatty acid is already ‘digested’ so to speak, so it’s more easily absorbed” than an ethyl ester fatty acid like Lovaza, which is the only approved prescription omega-3 product.This means Epanova does not need toaccompany a high-fat meal for better absorption and bioavailability.

The idea that one can use novel stomach bile compounds in order to reduce or eliminate atherosclerotic plaque deposits (blocked or clogged arteries) certainly caught the attention of many speculators at this year's conference. AtheroNova (AHRO.OB) is proposing that it has the potential to produce drugs that will regress or eliminate atherosclerotic fatty plaques. The company says that the existing classes of cholesterol reduction drugs, including statins, have demonstrated market success, rapidly achieving blockbuster status and billions of dollars in sales without demonstrating any efficacy at reducing atherosclerosis at commonly used dosage levels.

The Good: The company’s focus on compounds to reduce or eliminate atherosclerotic plaque deposits addresses the most lucrative segments of the multi-billion dollar prescription drug market: cardiovascular disease and stroke prevention, has produiced some great results in animal models. The Bad: Too often animal model data doesn't translate to humans the way we'd like it to. Going Forward: While we certainly love the outside-the-box idea that bile salts can solve all kinds of circulatory problems including those related to hypertension, diabetes and strokes, most investors are likely to wait to see more clinical results before jumping in. They may not have to wait too long, however, as the company recently announced that it has signed a binding term sheet with the Maxwell Biotech Group (with "Russia's premier biotech venture capital firm") to fund those clinical trials, and become an equity investor in AtheroNova. In return, Maxwell gets the commercialization rights for AtheroNova's AHRO-001 lead atherosclerotic plaque regression compound for Russia.

After almost completely re-inventing itself, its share structure and core business, the fully reporting, currently pink listed Catasys (CATS.OB) actually looks like it will finally turn around and start making money for investors. The firm, which found it incredibly difficult to get off the starting block with its previous innovative medical treatment approach looks like it is finally close to actually cracking and solving a $21 billion problem posed to insurance healthcare plans by substance abusers - this time by using analytics and closely guarded data from those firms themselves.

According to its President and CEO, Rick Anderson-- who made his way up the ranks within the company by making noise and convincing management that he could help implement some of these major changes himself -- Catasys is finally ready to start churning profits. Anderson told investors that high-cost substance dependent members cost health plans up to eight times more than other members. Under his direction, Catasys has now been re-designed to save those same health plans $19 to $40 million per million members. If the software and HIPAA Privacy protected data that Catasys is starting to gather from various existing clients (including the Ford Motor Company) is correct, then the firm may not only be positioned to save those group plan operators money, it may be positioned in a very unique way to start interpreting other important data (which can also be monetized) within the healthcare space. Imagine being able to identify previously obscure trends in healthcare from the vast amounts of data provided by some of the largest health insurance providers.

In addition, the firm has a proprietary outreach program that convinces substance abuse users to seek treatment before they run up huge bills for their own healthcare plans. Until now, each step of the way, Catasys has had to convince clients like Healthcare of Nevada, and Coventry Healthcare of Kansas, that they will experience success by using the scalable system. The adoption process has effective but slow and far from efficient, until now.

The Good: The company anticipates that it will finally move into profitability during 2012 and that models show that profitability will grow exponentially as more and more members are covered. The Bad: Haven't we heard this before? Investors who believed the Hythiam, Inc. model feel they got badly burned and that the entire company was a huge scheme of empty promises. Going Forward: It would take far too much space to go into the necessary details here, but we are certainly willing to re-visit Catasys' proposition if we start to see more of these major healthcare companies start to sign on the contract line with Catasys. We're told to anticipate that very trend starting shortly. In the meantime, it appears shares are starting to wake up as only one third of the available number is in the float and the rest are locked up by insiders who can't sell for a quick profit.

Finally, investors in Cytori Therapeutics (Nasdaq: CYTX) may want to pay close attention as we look at the intriguing presentation by Intellicell (SVFC.PK) a regenerative medicine stem cell play that - unlike a vast majority of others in the space - is already starting to generate revenue.Forbes recently featured a story about the company. Dr. Steven Victor, CEO and founder of Intellicell BioSciences, is a practicing celebrity dermatologist and author with over 20 years experience who came up a technology process which efficiently and painlessly yields Stromal Vascular FraCtion (thus the ticker symbol), a functionally diverse cell population that he has branded "IntelliCell™." These cells have multiple functions, are highly integrated and are reportedly more potent than adipose stem cells themselves. Doctors, dermatologists and surgeons are starting to use a patient's own (autologus) Adipose (Fat) Stem Cells using Intellicell's process within FDA 361 guidelines. These guidelines make the use of these stem cells FDA Compliant and will basically allow patients in the U.S. and their doctors decide whether they can use their own stem cells for any number of regenerative applications without having to leave the country or wait for specific FDA approvals.

The Good: The IntelliCell™ process is yeilding a much higher number of stem cells by using their harvesting technology. Because patients are using their own cells, there appears to be no risk of disease transfer, no risk of rejection or allergic reaction and so long as the procedure takes place on the same day within the same clinic, under the minimal manipulation rules afforded by FDA 361 guidelines, the doctors and patients can infuse or inject these cells as they see fit.

Unlike Cytori, which uses chemicals to free the adipose stem cells, Intelicell uses a proprietary process which does not employ any chemicals. Stem cells isolated from fat could be used to generate soft tissue and bone and may even help in the treatment of ailments such as heart disease. As we report this doctors are already using intradermal injections of SVF (IntelliCell™) for the treatment of wrinkles, skin tightening, acne scars, burns, scars, hair growth and gum recession.

The Bad: Worries about quackery began to spread among stem cell researchers and others after presidential candidate, Texas Gov. Rick Perry recently received experimental stem cell surgery on his own back. Some are wondering whether Intelicell is on the verge of leap-frogging over a vast number of others in the stem cell space or simply getting ready to fall flat on their face without the type of clinical data biotech firms need to survive on the Street. Going Forward: Researchers and third-party scientists are begining to study the IntelliCell™ process. While this already looks like a high-risk/high-reward play at this point, I can't help but notice the $30+ million in revenues generated by a privately held company based in Plymouth, Mass., called Harvest Technologies Corporation last year. That company was in the process of commercializing a similar, yet far more painfull, point-of-care technology, which harvested stem cells from a patient's own bone marrow. It was recently aquired by a U.S. subsidiary of Japan's Terumo Corporation -- one of the world's leading medical device manufacturers with $3.4 billion in sales and operations in more than 160 countries in a stock-for-stock transaction worth $70 million. If Intelicell executes its game plan and generates the $30-$40 million in revenue it is anticipating this year, the extremely low-float, low price shares won't stay at these levels for long.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

This article is tagged with: Long & Short Ideas, Quick Picks & Lists

More articles by M. E. Garza »

Optionen

| Boardmail an "lady luck" |

Wertpapier: ImmunoCellular Therapeu |

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: ImmunoCellular Therapeu |

Angehängte Grafik:

g060.gif

g060.gif

doppeltem Interesse!

Optionen

| Boardmail an "bigbangbowler2" |

Wertpapier: ImmunoCellular Therapeu |

z.Zt. bei opxa wie auch bei imuc schönes rein-/raus-traden möglich;

für longterminvest gegenwärtig wieder mal die story mit dem boden (ist IMO n.n. ganz erreicht)

chalif, hab nun ein wenig recherche betrieben, opxa aber wirklich hoch interessant.

will ergebnisse u. backgroundinfos aber nicht im imuc-thread posten, hat hier nix verloren, daher opxa thread einrichten...

gLTY

Optionen

| Boardmail an "lady luck" |

Wertpapier: ImmunoCellular Therapeu |

P.S. Bin seit Kurzem mit grossem Erfolg in Cyclacel investiert,vielleicht mach ich da mal einen Thread auf ......

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: ImmunoCellular Therapeu |

wenn keiner was dagegen hat, könnten wir diesen thread schon als biotech/pharmaceutical forum verwenden, zumindest bis sich bei IMUC was tut.

nun, CYCC - die sind doch u.a. am Sapacitabine zur oralen verabreichung dran (Ph.II), ohja, das große geschäft mit dem krebs. traditionsunternehmen seit 1992/NJ

CYCC hat vorerst den downtrend durchbrochen, gestern kam da erstmal seit langem volumen rein, ob dies das reversal für longies ist (?)... wird man sehen. technisch siehts interessant aus, gegenwärtig in startposition (alles nur m.M. / IMO)

falls dir n.n. bekannt hier ein interessanter link:

http://www.lookformedicine.com/...-orphan-drug-status-by-the-fda.html

GLTY, chalifmann III

LaLu

Optionen

| Boardmail an "lady luck" |

Wertpapier: ImmunoCellular Therapeu |

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: ImmunoCellular Therapeu |

Angehängte Grafik:

a015.gif

a015.gif

Was hälst du davon ?

P.S. Galena ist relativ günstig mit Mkap von 37 Mio.-$

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: ImmunoCellular Therapeu |

galena biopharm kann ich momentan nix zu sagen. müßte man mal so richtig in die tiefenanalyse gehen und auch ordentlich charten.

war alles ein wenig undurchsichtig, die umwandlung von RXI pharma. > Galena bio.

wenn ich mich recht erinnere hatten da auch CYTR anteile gehalten (schon raus), RXII aber wiederum war/ist bei ANX aufgrund eines gemeinsamen projektdeals beteiligt. dann war noch die Dillution mit ca. 40mio aktien für 19mille dollars + resultierend in 149 mio OS shares und ca. 50 mille in cash & securities), plus mangel an flüssigen mitteln (R&D bio tech stocks)....alles ein wenig chaotisch (für mich zumindest).

ein linkchen gefällig?

http://links.mkt1985.com/servlet/...=MTE1MDkyOTQ4S0&mt=1&rt=0

aber hast recht, chali, in diesem sektor gibt es tatsächlich einige interessante titel.

bei der gegenwärtigen marktlage ist die aussage "relativ günstig" wirklich zu relativieren, da wirtschaftliche hintergründe oft höher bewertet werden als die tatsächlichen kompetenzen/assets der unternehmen.

vielleicht wartest noch zu. dein invest solltest auch immer abhängig davon machen, ob du die swingtraden oder wirklich ultralong gehen willst.

best

LaLu

Optionen

| Boardmail an "lady luck" |

Wertpapier: ImmunoCellular Therapeu |

"Sorry,aber jetzt hab ich wieder nichts zu IMUC gepostet,aber eins noch :"

chalimann III, ist doch dein thread, auf dem du posten kannst was DU magst.

ev. ist meine sicht nicht ganz regelkonform, aber so seh´ ich das nunmal.

bigbäng wird uns doch wohl nicht verpetzen!!? :-)))

sonst issja kaum einen hier im IMUC-room.

happy trades & GLTY

Optionen

| Boardmail an "lady luck" |

Wertpapier: ImmunoCellular Therapeu |

GoodN8GoodF(l)ight

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: ImmunoCellular Therapeu |

mal abwarten wie die reaktionen sein werden.

Immunocellular therapeutics starten danach eine promo-roadshow. d.h. für die eine oder andere swinggelegenheit (wie meine +30% binnen 14 tagen vor ca. 3 wochen) kann das helfen...augen auf!

http://w3.cns.org/dp/2011CNS/987.pdf

p.s.: chali, IMUC ist im übrigen auch an der nasdaq BB für jedermann/frau handelbar.

Optionen

| Boardmail an "lady luck" |

Wertpapier: ImmunoCellular Therapeu |