Deep Down Inc. - Aktie des Tages!!

Seite 1 von 8 Neuester Beitrag: 17.04.11 19:56 | ||||

| Eröffnet am: | 11.06.07 09:13 | von: HotStockGur. | Anzahl Beiträge: | 176 |

| Neuester Beitrag: | 17.04.11 19:56 | von: Schaunwirma. | Leser gesamt: | 44.710 |

| Forum: | Hot-Stocks | Leser heute: | 3 | |

| Bewertet mit: | ||||

| Seite: < | 2 | 3 | 4 | 5 | 6 | 7 | 8 8 > | ||||

Heute wolle man den Anlegern ein Unternehmen, das für den reibungslosen Aufbau und Betrieb von Bohrinseln sorge, präsentieren: Deep Down aus dem US-Bundesstaat Texas habe sich auf diesem Markt etabliert und schicke sich nun an, die Lücke zu den großen Namen der Branche zu schließen.

Gerade habe das Unternehmen hervorragende Geschäftszahlen für das Jahr 2006 bekannt gegeben. Demnach sei der Umsatz im Vergleich zum vorangegangenen Jahr um 62,8% auf 8,8 Mio. USD gesteigert worden. Der Nettogewinn belaufe sich auf 952.423 USD und liege damit 58,3% über dem Ergebnis des Vorjahres - ein Ergebnis, das sich sehen lassen könne und das Lust auf mehr mache. Der Gewinnsprung sei auf ein intelligentes Produktmanagement zurückzuführen. Mit der Einführung neuer Produktreihen wie "LARS" sei der Grundstein für das weitere organische Wachstum gelegt worden.

Das habe auch das Management so gesehen und wenige Tage nach Bekanntgabe der Zahlen für 2006 noch einmal nachgelegt. Die Offenlegung der Auftragseingänge im ersten Quartal des Geschäftsjahres 2007 sei mit Begeisterung aufgenommen worden. Schon in den ersten drei Monaten des laufenden Jahres seien Aufträge mit einem Gesamtvolumen von mehr als 3,25 Mio. USD eingegangen.

Die Technologien, die beim Aufbau von Offshore-Plattformen zum Einsatz kommen würden, seien außergewöhnlich komplex. Deep Down setze die von den Auftraggebern gewünschten Lösungen um, agiere aber auch als Berater oder unterstützender Partner bei Großprojekten. Zu den Dienstleistungen würden das Projektmanagement, die Projektumsetzung und das Storage Management zählen. Das benötigte Zubehör produziere das Unternehmen größtenteils selbst.

Ein großer Erfolg sei die "SeaStax"-Produktreihe. "SeaStax" sei entwickelt worden, um schwere Maschinen und Zubehör auf sicherem Weg in die Tiefe transportieren zu können. Die bislang auf dem Markt erhältlichen Produkte hätten aufgrund von gravierenden Sicherheitsmängeln wenig Anklang gefunden. Mit "SeaStax" biete Deep Down den Kunden eine sichere, umweltfreundliche und zugleich äußerst variable Lösung. Die einzelnen Komponenten seien beliebig kombinierbar und könnten daher individuell an die Bedürfnisse des Kunden angepasst werden.

Dies komme bei den Auftraggebern sehr gut an und sorge dafür, dass die Kundenliste von Deep Down immer länger werde. Branchengrößen wie Royal Dutch Shell, ExxonMobil, Texaco, Chevron, BP, Total, BHP und ENI habe das texanische Unternehmen in der Vergangenheit bereits überzeugen und dauerhaft als Kunden gewinnen können.

Wie viel Geld sich in diesem Geschäft verdienen lasse, verdeutliche das nachfolgende Beispiel: Die Fertigstellung der vom Unternehmen BP in Auftrag gegebenen Plattform "King" habe insgesamt rund 12 Mio. USD verschlungen. Auf die von Deep Down angebotenen Produkte und Dienstleistungen entfalle ein Anteil von 5,8%. Dies entspreche der Summe von 700.000 USD. Das Beispiel beziehe sich wohlgemerkt auf den Bau einer einzelnen Bohrinsel.

Hierdurch werde sehr schnell klar: das Umsatz- und Gewinnpotenzial von Deep Down sei gigantisch. Um das vorhandene Potenzial ausschöpfen zu können, sei das Unternehmen auch im Hinblick auf Übernahmen wachsam. Gerade erst sei der Zukauf von ElectroWave USA perfekt gemacht worden. ElectroWave stelle elektronische Mess- und Überwachungsgeräte her. Das Management gehe davon aus, dass sich die Übernahme unmittelbar positiv auf den Umsatz und den Gewinn von Deep Down auswirken werde. Langfristig solle ein Unternehmen entstehen, das alle Produkte und Dienstleistungen aus einer Hand anbiete.

Dabei sehe sich das Management insbesondere dem Shareholder Value verpflichtet. Im Verlauf des ersten Quartals sei die Zahl der im Umlauf befindlichen Aktien um 18% reduziert worden. Diese Nachricht werde die Investoren freuen, habe eine solche Reduzierung des Aktienangebotes doch zumeist steigende Kurse zur Folge.

Ron Smith, CEO des Unternehmens, kenne sein Geschäft. Vor seinem Wechsel zu Deep Down habe er wichtige Management-Positionen bei der Ocean Drilling and Exploration Company sowie den Unternehmen Oceaneering Multiflex, Mustang Engineering und Kvaerner inne gehabt. Im Laufe seiner Tätigkeit habe Ron Smith alle relevanten Geschäftsbereiche des Onshore wie des Offshore-Geschäfts durchlaufen und könne so auf einen reichhaltigen Erfahrungsschatz zurückblicken.

Die Nachfrage nach Offshore-Pipelines und Zubehör werde den eingeschlagenen Pfad Prognosen zufolge weiter steigen. Die Zuwachsraten würden je nach Region schwanken, lägen aber durchweg im dreistelligen Bereich. In der Region Westafrika würden die Experten eine Verdreifachung des Marktvolumens erwarten, in Südost-Asien sei gar eine Verfünffachung zu erwarten. Für den südamerikanischen Markt werde eine Verdopplung prognostiziert.

Die bevorstehende Hurrikan-Saison verleihe der Aktie zusätzliche Kursfantasie. In den letzten Jahren sei zu beobachten gewesen, dass sich die Aktien jener Unternehmen, die von möglichen Hurrikan-Schäden profitieren würden, in den Monaten Mai und Juni spürbar verteuern würden. Deep Down sei in vielen Regionen tätig, für die Hurrikans vorausgesagt würden. Sollten die Schäden ähnlich gravierend ausfallen wie in den Vorjahren, dürfe Deep Down mit zusätzlichen Aufträgen rechnen.

Würden die kommenden Quartale ebenso gut wie die ersten drei Monate des Jahres verlaufen, werde Deep Down im Geschäftsjahr 2007 erstmals einen Umsatz in zweistelliger Millionenhöhe verbuchen und einen Gewinn jenseits der Millionengrenze bekannt geben können. Mit einer Marktkapitalisierung von unter 25 Mio. EUR und einem 2006-KGV von 25,7 erscheine die Aktie angesichts des gewaltigen Potenzials auch nicht zu teuer. Das Kursziel laute auf 0,45 EUR.

Die Experten des Börsenbriefs "Global SmallCap Report" raten den Anlegern bei der Aktie des Unternehmens Deep Down zum Kauf. (Analyse vom 11.06.07)

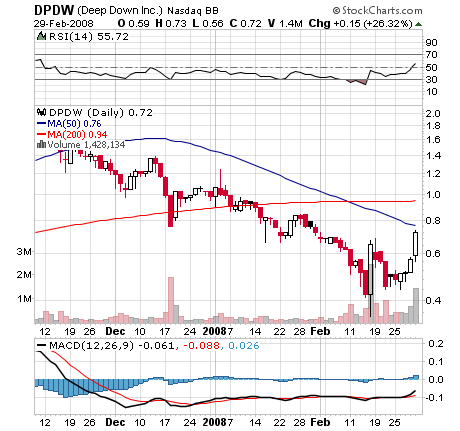

Korrektur nach unten sollte nach der Übertreibung beendet sein !

Ich werde Montag evtl nachkaufen !

Chart sieht sehr schön aus...

:)

2008 ist das Jahr von Deep Down !

Wer's genauer wissen will:

http://investorshub.advfn.com/boards/board.asp?board_id=7181

bbb

bbb

Angehängte Grafik:

deepdown.png (verkleinert auf 56%)

deepdown.png (verkleinert auf 56%)

Weitere informationen könnt ihr hier finden :

http://investorshub.advfn.com/boards/board.asp?board_id=7181

:):)

bbb

http://biz.yahoo.com/prnews/080122/aqtu212.html?.v=16

Deep Down Hires Corporate Controller

http://biz.yahoo.com/prnews/080124/aqth106.html?.v=32

Hier gehts nur noch aufwärts... !!!

http://investorshub.advfn.com/boards/board.asp?board_id=7181

bin erst seit einen Jahr am Markt aktiv dabei, werde weder noch irgendwelche Prognosen noch Kaufempfehlungen abgeben. Sollte jeder für sich entscheiden. Möchte mich aber gerne über das hier von Euch genannte Unternehmen austauschen.Bin selbst bei DD investiert und mir ist klar das es sich auch hier um ein Hot-Stocks handelt wo gerne mit gezokt wird.Meine Meinung ist aber, das bei DD fundamental was dahinter steckt, was mann bei vielen anderen heiss diskutierten Hot-Stocks hier nicht findet.Lese die aktuellen News immer bei finanznachrichten. Da mein Wirtschaftsenglisch nicht das beste ist, kopiere ich die Texte und füge dann den Text auf der Seite von Yahoo Babel Fich ein.Der spuckt mir dann alles in Deutsch aus.Hätte auch nicht gedacht, das sie noch mal soweit zurück kommt und das ohne Grund.Bin aber fest von überzeugt das uns DD noch jede Menge Freude und euros bescheren wird. Wünsche allen investierten ein schönes WE

Hier link zum ihub board, viel Info dort :

http://investorshub.advfn.com/boards/board.asp?board_id=7181

Angehängte Grafik:

dpdw_reversal.png

dpdw_reversal.png

Deep Down Focuses on Investor Relations and Market Awareness

PR Newswire "US Press Releases "

HOUSTON, March 27 /PRNewswire-FirstCall/ -- Deep Down, Inc. (OTCBB: DPDW) today announced recent activities it has engaged in to increase awareness to the institutional marketplace of its unique position in the offshore services industry.

Deep Down recently hired Steven M. Haag to serve full time as Vice-president of Investor Relations. Mr. Haag has extensive experience in investor relations, marketing, and advertising. Mr. Haag will be responsible for coordinating all aspects of investor relations and corporate communications including (1) the creation of sales, marketing and advertising materials, and investor kits, (2) website development and maintenance, (3) the dissemination of company information to existing and prospective retail and institutional shareholders, (4) the management of company participation in investor conferences and (5) the fielding of shareholder calls. Mr. Haag received his bachelor's degree in psychology, with a minor in organizational behavior, from Webster University in 1993, and his master's degree in education from the University of Missouri - St. Louis in 1995.

The Company recently attended the 2008 Oil & Gas Investment Symposium Small Cap Conference (2008 OGIS Small Cap) hosted by the Independent Petroleum Association of America (IPAA) on February 12-14, 2008, in Hollywood, Florida, where it hosted a breakfast roundtable. OGIS Small Cap is an outlet for publicly traded U.S. independent producers, and service and supply companies, with market caps of up to $1 billion to present their corporate profiles to the investment community.

Management recently made presentations to institutional investors during the Energy Supply Conference hosted by Dahlman Rose & Company, LLC on March 12-13, 2008, in Boston, Massachusetts, and New York City, New York. Dahlman Rose is a full-service investment bank offering value-added research, trading, and advisory services for growing companies operating along the energy and commodity supply chain. It is a leading boutique investment bank specializing in the marine shipping and energy industries with offices in New York, Houston, San Francisco, and New Orleans. On March 10, 2008, Dahlman Rose reiterated their BUY rating on our common stock with a per share price target of $2.50. Further information on Dahlman Rose may be obtained at http://www.dahlmanrose.com.

"Deep Down realizes the importance of corporate and shareholder communications and welcomes the contributions that Mr. Haag will bring to our efforts. We have a very unique position in the offshore services industry, and we believe the investment community will be interested in learning about it. Our story is not one that is widely known. Our objective is to change that over time," said Robert E. Chamberlain, Jr., Chairman and Chief Acquisitions Officer.

About Deep Down, Inc.

Deep Down specializes in the provision of innovative solutions, installation management, engineering services, support services, custom fabrication and storage management services for the offshore subsea control, umbilical, and pipeline industries. The company fabricates component parts of subsea distribution systems and assemblies that specialize in the development of subsea fields and tie backs. These items include umbilicals, flow lines, distribution systems, pipeline terminations, controls, winches, and launch and retrieval systems, among others. Deep Down provides these services from the initial field conception phase, through manufacturing, site integration testing, installation, topside connections, and the final commissioning of a project.

The Company's ElectroWave subsidiary offers products and services in the fields of electronic monitoring and control systems for the energy, military, and commercial business sectors. ElectroWave designs, manufactures, installs, and commissions integrated PLC and SCADA based instrumentation and control systems, including ballast control and monitoring, drilling instrumentation, vessel management systems, marine advisory systems, machinery plant control and monitoring systems, and closed circuit television systems.

The Company's Mako subsidiary serves the growing offshore petroleum and marine industries with technical support services, and products vital to offshore petroleum production, through rentals of its remotely operated vehicles (ROV), topside and subsea equipment, and diving support systems used in diving operations, maintenance and repair operations, offshore construction, and environmental/marine surveys.

The Company's strategy is to consolidate service providers to the offshore industry, as well as designers and manufacturers of subsea, surface, and offshore rig equipment used by major, independent, and foreign national oil and gas companies in deep-water exploration and production of oil and gas throughout the world. Deep Down's customers include BP Petroleum, Royal Dutch Shell, Exxon Mobil Corporation, Devon Energy Corporation, Chevron Corporation, Anadarko Petroleum Corporation, Marathon Oil Corporation, Kerr-McGee Corporation, Nexen Inc., BHP, Amerada Hess, Helix, Oceaneering International, Inc., Subsea 7, Inc., Transocean Offshore, Diamond Offshore, Marinette Marine Corporation, Acergy, Veolia Environmental Services, Noble Energy Inc., Aker Kvaerner, Cameron, Oil States, Dril-Quip, Inc., Nexans, Cabett, JDR, and Duco, among others. For further company information, please visit http://www.deepdowninc.com and http://www.electrowaveusa.com

Company information distributed through the Market Access Program is based upon information that Standard & Poor's considers to be reliable, but neither Standard & Poor's nor its affiliates warrant its completeness or accuracy, and it should not be relied upon as such. This material is not intended as an offer or solicitation for the purchase or sale of any security or other financial instrument.

One of our most important responsibilities is to communicate with shareholders in an open and direct manner. Comments are based on current management expectations, and are considered "forward-looking statements," generally preceded by words such as "plans," "expects," "believes," "anticipates," or "intends." We cannot promise future returns. Our statements reflect our best judgment at the time they are issued, and we disclaim any obligation to update or alter forward-looking statements as the result of new information or future events. Deep Down urges investors to review the risks and uncertainties contained within its filings with the Securities and Exchange Commission.

Tuesday April 1, 8:54 am ET

HOUSTON, April 1, 2008 /PRNewswire-FirstCall/ -- Deep Down, Inc., a Nevada corporation (OTC Bulletin Board: DPDW - News), today announced it has filed its Form 10-KSB for the period ending December 31, 2007, with the Securities and Exchange Commission. Under purchase accounting rules, the financial results of operations for 2006 include the operations of Deep Down only for the period beginning November 21, 2006 and ending December 31, 2006, the period after which its Deep Down (Delaware) subsidiary was acquired. During this period in 2006, Deep Down reported revenues of $978,047. In order to present a more complete view of full-year operations for Deep Down during 2006 and to present more meaningful comparable results, management also presented unaudited pro forma consolidated results of operations for 2006 as if the acquisition of Deep Down had occurred on January 1, 2006. The discussion below compares audited financial information for the fiscal year ended December 31, 2007 with unaudited pro forma financial information for the year ended December 31, 2006.

ADVERTISEMENT

Revenue for the year ended December 31, 2007, was $19,389,730, an increase of $10,568,581 or 119.8%, compared to revenue of $8,821,149 for the comparable period in 2006. Gross profit for 2007 was $6,369,361, an increase of $2,703,611 or 73.8%, compared to gross profit of $3,665,750 for 2006. Gross profit dropped from 41.6% to 32.8%, primarily as the result of increased expenses associated with the development of new products during the year. Management expects margins to improve with wider acceptance of these recent product introductions. Operating income for 2007 was $1,657,844 for 2007, an increase of $3,868,886 compared to a loss of $2,211,042 for the comparable period in 2006. Net income for 2007 was $952,509, an increase of $3,764,136 compared to a loss of $2,811,627 for the comparable period in 2006.

Deep Down uses EBITDA as an unaudited supplemental financial measure to assess the financial performance of its assets without regard to financing methods, capital structure, taxes or historical cost basis. The Company defines EBITDA as net income plus interest expense, income taxes, depreciation, amortization and other non-cash, non-operating expense. The term EBITDA is not defined under generally accepted accounting principles, and EBITDA is not presented as an alternative measure of operating results or cash flow from operations. EBITDA does not give effect to cash used for debt service requirements, and thus, does not reflect funds available for investment, distributions or other discretionary uses. When assessing Deep Down's operating performance or liquidity, investors and others should not consider this data in isolation or as a substitute for net income, cash flow from operating activities, or other cash flow data calculated in accordance with generally accepted accounting principles. However, Deep Down also understands that such data are used by some investors, equity analysts, and others to make informed investment decisions. EBITDA is used as an analytical indicator of income generated to service debt and fund capital expenditures. In addition, multiples of current or projected EBITDA are used to estimate current or projected enterprise value. EBITDA for 2007 was $2,272,202, up 43.0% compared to $1,296,218 for 2006.

"Our management team is extremely proud of our first full year's results of operations as a public company. The income statement is primarily reflective of growth in our core operations and includes only one month of financial results for our most recent acquisition, Mako Technologies. We expect the full impact of this acquisition to manifest itself in future periods," commented Robert E. Chamberlain, Jr., Deep Down's Chairman and Chief Acquisitions Officer. "We are committed to the continued fulfillment of our strategic acquisition objectives to position Deep Down as a preferred provider of services and products in support of deepwater exploration, development and production of oil and gas, and other maritime operations," Chamberlain added.

"Our significant revenue growth is reflective of Deep Down's commitment to offer innovative services, products, and solutions to support major oil and gas operators, installation contractors, and umbilical and control suppliers in their continual effort to enhance the progression and completion of major offshore oil and gas exploration and production projects. Our goal is to deliver innovative solutions to our customers quicker, more cost-effectively, and more safely. We are also focused on protecting our innovations more effectively as we venture into the uncharted frontier of deeper water," commented Ronald E. Smith, Deep Down's President and Chief Executive Officer.

"We are particularly proud of the balance sheet improvements experienced during 2007. We have simplified the capital structure by redeeming for cash or exchanging for common stock various series of preferred stock. Deep Down experienced significant balance sheet improvements over the period with an increase in shareholders' equity of $15.9 million. This dramatic increase does not reflect the recent conversion of the Series D Preferred Stock or the final payment for the Mako acquisition. We believe our liquidity to be healthy as well. Compared to the prior period, our accounts receivable have increased by $5.9 million to $7.2 million. Our accounts payable have only increased by $2.8 million to $3.6 million. We will continue to focus on simplifying the capital structure, reducing capital costs, and positioning the company to finance future acquisitions," said Eugene L. Butler, Deep Down's Chief Financial Officer.

About Deep Down, Inc.

Deep Down specializes in the provision of innovative solutions, installation management, engineering services, support services, custom fabrication and storage management services for the offshore subsea control, umbilical, and pipeline industries. The company fabricates component parts of subsea distribution systems and assemblies that specialize in the development of subsea fields and tie backs. These items include umbilicals, flow lines, distribution systems, pipeline terminations, controls, winches, and launch and retrieval systems, among others. Deep Down provides these services from the initial field conception phase, through manufacturing, site integration testing, installation, topside connections, and the final commissioning of a project.

The Company's ElectroWave subsidiary offers products and services in the fields of electronic monitoring and control systems for the energy, military, and commercial business sectors. ElectroWave designs, manufactures, installs, and commissions integrated PLC and SCADA based instrumentation and control systems, including ballast control and monitoring, drilling instrumentation, vessel management systems, marine advisory systems, machinery plant control and monitoring systems, and closed circuit television systems.

The Company's Mako subsidiary serves the growing offshore petroleum and marine industries with technical support services, and products vital to offshore petroleum production, through rentals of its remotely operated vehicles (ROV), topside and subsea equipment, and diving support systems used in diving operations, maintenance and repair operations, offshore construction, and environmental/marine surveys.

The Company's strategy is to consolidate service providers to the offshore industry, as well as designers and manufacturers of subsea, surface, and offshore rig equipment used by major, independent, and foreign national oil and gas companies in deep-water exploration and production of oil and gas throughout the world. Deep Down's customers include BP Petroleum, Royal Dutch Shell, Exxon Mobil Corporation, Devon Energy Corporation, Chevron Corporation, Anadarko Petroleum Corporation, Marathon Oil Corporation, Kerr-McGee Corporation, Nexen Inc., BHP, Amerada Hess, Helix, Oceaneering International, Inc., Subsea 7, Inc., Transocean Offshore, Diamond Offshore, Marinette Marine Corporation, Acergy, Veolia Environmental Services, Noble Energy Inc., Aker Kvaerner, Cameron, Oil States, Dril-Quip, Inc., Nexans, Cabett, JDR, and Duco, among others. For further company information, please visit http://www.deepdowninc.com, http://www.electrowaveusa.com and http://www.makotechnologies.com.

One of our most important responsibilities is to communicate with shareholders in an open and direct manner. Comments are based on current management expectations, and are considered "forward-looking statements," generally preceded by words such as "plans," "expects," "believes," "anticipates," or "intends." We cannot promise future returns. Our statements reflect our best judgment at the time they are issued, and we disclaim any obligation to update or alter forward-looking statements as the result of new information or future events. Deep Down urges investors to review the risks and uncertainties contained within its filings with the Securities and Exchange Commission.

Deep Down, Inc.

Consolidated Statements of Operations

For the Year Ended December 31, 2007 and

For the Period Since Inception (June 29, 2006) to December 31, 2006

Historical Results Unaudited Pro forma

Year Ended Year Ended

December 31, 2007 December 31, 2006

Revenues $19,389,730 $ 8,821,149

Cost of sales 13,020,369 5,155,399

Gross profit 6,369,361 3,665,750

Operating expenses:

Selling, general & administrative (1) 4,284,553 5,710,324

Depreciation 426,964 166,468

Total operating expenses 4,711,517 5,876,792

Operating income 1,657,844 (2,211,042)

Other income (expense):

Gain on disposal of assets - -

Gain on debt extinguishment 2,000,000 -

Interest income 94,487 -

Interest expense (2) (2,430,149) (578,335)

Total other income (335,662) (578,335)

Income from continuing operations 1,322,182 (2,789,377)

Income tax expense (369,673) (22,250)

Net income (loss) $952,509 $(2,811,627)

Basic earnings per share $0.01 $(0.04)

Shares used in computing basic

per share amounts 73,917,190 75,862,484

Diluted earnings per share $0.01 $(0.04)

Shares used in computing diluted

per share amounts 104,349,455 75,862,484

(1) Includes $3.3 million compensation expense from the issuance of

Series F and G preferred shares.

(2) Includes approximately $423,258 additional interest expense from the

accretion of the Series E preferred shares.

Calculation of EBITDA

2007 Pro Forma 2006 Change %

Net income (loss) $952,509 $ (2,811,627) $3,764,136 395.20%

Tax expense 369,673 22,250 347,423 94.00%

Gain on debt

extinguishment (2,000,000) - (2,000,000) 100.00%

Interest 2,335,662 578,335 1,757,327 75.20%

Other income (expense) - - - NMF

Depreciation and

amortization expense 426,964 166,468 260,496 61.00%

Stock based compensation

expense 187,394 3,340,792 (3,153,398) NMF

EBITDA $2,272,202 $1,296,218 $975,984 43.00%

Deep Down, Inc.

Statements of Stockholders' Equity

For the Year Ended December 31, 2007 and

For the Period Since Inception (June 29, 2006) to December 31, 2006

December 31, December 31,

2007 2006

Assets

Cash and equivalents $2,206,220 $ 12,462

Restricted cash 375,000 -

Accounts receivable, net of allowance of

$139,787 and $81,809 7,190,466 1,264,228

Prepaid expenses and other current assets 312,058 156,975

Inventory 502,253 -

Lease receivable, short term 414,000 -

Work in progress 945,612 916,485

Receivable from Prospect, net 2,687,333 -

Total current assets 14,632,942 2,350,150

Property and equipment, net 5,172,804 845,200

Other assets, net of accumulated amortization

of $54,560 and $0 1,109,152 -

Lease receivable, long term 173,000 -

Intangibles, net 4,369,647 -

Goodwill 10,594,144 6,934,213

Total assets $36,051,689 $10,129,563

Liabilities and Stockholders' Equity (Deficit)

Accounts payable and accrued liabilities $3,569,826 $816,490

Deferred revenue 188,030 190,000

Payable to Mako Shareholders 3,205,667 -

Current portion of long-term debt 995,177 410,731

Total current liabilities 7,958,700 1,417,221

Long-term debt, net of accumulated

discount of $1,703,258 and $0 10,698,818 757,617

Series E redeemable exchangeable preferred

stock, face value and liquidation preference

of $1,000 per share, no dividend preference,

authorized 10,000,000 aggregate shares of all

series of Preferred stock 500 and 5,000 issued

and outstanding, respectively 386,411 3,486,376

Series G redeemable exchangeable preferred

stock, face value and liquidation preference

of $1,000 per share, no dividend preference,

authorized 10,000,000 aggregate shares of all

series of Preferred stock 0 and 1,000 issued

and outstanding, respectively - 697,275

Total liabilities 19,043,929 6,358,489

Temporary equity:

Series D redeemable convertible preferred

stock, $0.01 par value, face

value and liquidation preference of $1,000 per

share, no dividend preference, authorized

10,000,000 aggregate shares of all series of

Preferred stock 5,000 issued and outstanding 4,419,244 4,419,244

Series F redeemable convertible preferred stock,

$0.01 par value, face value and liquidation

preference of $1,000 per share, no dividend

preference, authorized 10,000,000 aggregate

of all series of Preferred stock 0 and 3,000

issued and outstanding, respectively - 2,651,547

Total temporary equity 4,419,244 7,070,791

Stockholders' equity (deficit):

Series C convertible preferred stock,

$0.001 par value, 7% cumulative dividend,

authorized 10,000,000 aggregate shares of

all series of Preferred stock 0 and 22,000

shares issued and outstanding, respectively - 22

Common stock, $0.001 par value, 490,000,000

shares authorized, 85,976,526 and 82,870,171

shares issued and outstanding, respectively 85,977 82,870

Paid in capital 14,849,847 82,792

Accumulated deficit 2,347,308 3,299,817

Total stockholders' equity (deficit) 12,588,516 3,299,717

Total liabilities and stockholders' equity $36,051,689 $10,129,563

--------------------------------------------------

Source: Deep Down, Inc.

PR Newswire "US Press Releases "

HOUSTON, April 7, 2008 /PRNewswire-FirstCall/ -- Deep Down, Inc. (OTC Bulletin Board: DPDW) announced today that it has shipped $1.5 million worth of products for the Phoenix project, including six next generation Loose-tube Steel Flying Leads (LSFLs). Additional revenue will be generated through installation support at a later date.

Several of these LSFLs contain fifteen (one-half inch) Super Duplex steel tubes. The LSFLs were delivered to the customer and incorporated into a successful Systems Integration Test program. The LSFLs possess newly engineered and improved features that are so significant in the evolution of steel flying leads that Deep Down is applying for patents. The newly improved design of the LSFLs makes these much easier to install. Quicker, easier, ROV-based installations translate into significant cost savings for Deep Down's customers.

Deep Down also delivered four Electrical Hydraulic Compliant Moray(TM) Umbilical Termination Heads, which were terminated to the end of steel tube umbilicals. The use of Electrical Hydraulic Compliant Moray Umbilical Termination Heads allows full sized umbilicals to be plugged directly into subsea trees by a remote operated vehicle, thus eliminating the need for large Umbilical Termination Assemblies (UTA). The unique Umbilical Termination Head design translates into additional cost savings and is ideal for single well tie-backs or long extension umbilicals.

Deep Down will deliver the LSFLs on its proprietary Subsea Deployment Baskets (SDB). The installation contractor is considering installing the LSFLs with Deep Down's recently introduced subsea deployment method because of its effectiveness in reducing installation time. The use of SDBs also reduces the risk for safety incidents by reducing the amount of personnel time needed to deploy LSFLs over a lay chute versus the seconds it takes to overboard a SDB into the water.

"Our personnel have been instrumentally involved in the design, manufacture, and installation of steel flying leads since the initial concept. We are committed to the introduction of new concepts to improve the design, function, and cost of steel flying leads to assist our customers in the production of deepwater reserves," commented Ronald E. Smith, Deep Down's President and Chief Executive Officer.

About Deep Down, Inc.

Deep Down specializes in the provision of innovative solutions, installation management, engineering services, support services, custom fabrication and storage management services for the offshore subsea control, umbilical, and pipeline industries. The company fabricates component parts of subsea distribution systems and assemblies that specialize in the development of subsea fields and tie backs. These items include umbilicals, flow lines, distribution systems, pipeline terminations, controls, winches, and launch and retrieval systems, among others. Deep Down provides these services from the initial field conception phase, through manufacturing, site integration testing, installation, topside connections, and the final commissioning of a project.

The Company's ElectroWave subsidiary offers products and services in the fields of electronic monitoring and control systems for the energy, military, and commercial business sectors. ElectroWave designs, manufactures, installs, and commissions integrated PLC and SCADA based instrumentation and control systems, including ballast control and monitoring, drilling instrumentation, vessel management systems, marine advisory systems, machinery plant control and monitoring systems, and closed circuit television systems.

The Company's Mako subsidiary serves the growing offshore petroleum and marine industries with technical support services, and products vital to offshore petroleum production, through rentals of its remotely operated vehicles (ROV), topside and subsea equipment, and diving support systems used in diving operations, maintenance and repair operations, offshore construction, and environmental/marine surveys.

The Company's strategy is to consolidate service providers to the offshore industry, as well as designers and manufacturers of subsea, surface, and offshore rig equipment used by major, independent, and foreign national oil and gas companies in deep-water exploration and production of oil and gas throughout the world. Deep Down's customers include BP Petroleum, Royal Dutch Shell, Exxon Mobil Corporation, Devon Energy Corporation, Chevron Corporation, Anadarko Petroleum Corporation, Marathon Oil Corporation, Kerr-McGee Corporation, Nexen Inc., BHP, Amerada Hess, Helix, Oceaneering International, Inc., Subsea 7, Inc., Transocean Offshore, Diamond Offshore, Marinette Marine Corporation, Acergy, Veolia Environmental Services, Noble Energy Inc., Aker Kvaerner, Cameron, Oil States, Dril-Quip, Inc., Nexans, Cabett, JDR, and Duco, among others. For further company information, please visit http://www.deepdowninc.com, http://www.electrowaveusa.com and http://www.makotechnologies.com.

One of our most important responsibilities is to communicate with shareholders in an open and direct manner. Comments are based on current management expectations, and are considered "forward-looking statements," generally preceded by words such as "plans," "expects," "believes," "anticipates," or "intends." We cannot promise future returns. Our statements reflect our best judgment at the time they are issued, and we disclaim any obligation to update or alter forward-looking statements as the result of new information or future events. Deep Down urges investors to review the risks and uncertainties contained within its filings with the Securities and Exchange Commission.

SOURCE Deep Down, Inc.

http://biz.yahoo.com/bw/080408/20080408006490.html?.v=1

Standard & Poor's Initiates Factual Stock Report Coverage on Deep Down, Inc.

Tuesday April 8, 4:23 pm ET

NEW YORK--(BUSINESS WIRE)--Standard & Poor’s announced today that it has commenced Factual Stock Report coverage on Deep Down, Inc.

Deep Down, Inc. (OTCBB:DPDW - News) is an installation engineering and management company focused on the offshore segment of the energy industry. It provides installation management, engineering services, support services, custom fabrication and storage management services for the offshore subsea control, umbilical, and pipeline industries.

The company's products include flying lead installation, maintenance and termination systems; buoyancy and rigging systems; high and low pressure testing and monitoring systems; latch systems; lay chutes; rollers; tensioners; and offshore storage and space management systems.

Deep Down fabricates component parts of subsea distribution systems and assemblies that specialize in the development of subsea fields and tie backs. These items include umbilicals, flow lines, distribution systems, pipeline terminations, controls, winches, and launch and retrieval systems, among others

This report will also be accessible on an ongoing basis to the investment community ---- scores of buy-side institutions and sell-side firms that utilize S&P research and information platforms daily. Millions of self-directed investors also have access to the report via their e-brokerage accounts.

About Standard & Poor's Factual Stock Reports

This Standard & Poor’s service provides factual research coverage enabling information about Deep Down, Inc. and other securities to reach a wide investor audience of Buy and Sell-side investors, helping them understand a company’s fundamentals and business prospects. Currently profiling over 1,000 issuers, S&P Factual Stock Reports increase market awareness for issuers in the investment community with insightful commentary and key statistics/information. Updated weekly with the latest pricing, trading volume, and other data, the reports include recent developments, a financial review, key operating information, Industry and peer comparisons, institutional holdings analysis, Street Consensus and opinions, performance charts, business summary, fundamental data, and news. Because coverage of these reports is sponsored by the issuer, S&P does not offer investment opinions concerning the advisability of investing in these stocks.

Standard & Poor’s Factual Stock Reports are produced separately from any other analytic activity of Standard & Poor’s. Standard & Poor’s Factual Report research has no access to non-public information received by other units of Standard & Poor’s. Standard & Poor’s does not trade on its own account.

Note: All U.S. and Canadian Companies listed on a National Exchange (not covered by S&P’s STARS research) are eligible to obtain this coverage.

About Standard & Poor's

Standard & Poor's, a division of The McGraw-Hill Companies (NYSE: MHP - News), is the world's foremost provider of financial market intelligence, including independent credit ratings, indices, risk evaluation, investment research and data. With approximately 7,500 employees, including wholly owned affiliates, located in 21 countries, Standard & Poor's is an essential part of the world's financial infrastructure and has played a leading role for more than 140 years in providing investors with the independent benchmarks they need to feel more confident about their investment and financial decisions. For more information, visit http://www.standardandpoors.com.

MULTIMEDIA AVAILABLE: http://www.businesswire.com/cgi-bin/mmg.cgi?eid=5653339

Contact:

Deep Down, Inc.

Steven Haag, 281-862-2201

ir@deepdowninc.com

or

Standard & Poor's

Customers:

Richard Albanese, 212-438-3647

richard_albanese@standardandpoors.com

or

Media Relations:

Michael Privitera, 212-438-6679

michael_privitera@standardandpoors.com

Wall Street Consensus vs. Performance

For fiscal year 2008, analysts estimate that DPDW

will earn $0.07. For fiscal year 2009, analysts

estimate that DPDW's earnings per share will

grow by 86% to $0.13.

Press Release Source: Deep Down, Inc.

Deep Down Delivers Second 4000 Meter Rated LARS

Friday April 11, 2:13 pm ET

HOUSTON, April 11 /PRNewswire-FirstCall/ -- Deep Down, Inc. (OTC Bulletin Board: DPDW - News) announced today that it has shipped the second of what is believed to be the deepest class rated Launch and Retrieval System ("LARS") in the world.

(Photo: http://www.newscom.com/cgi-bin/prnh/20080411/LAF029-a)

(Photo: http://www.newscom.com/cgi-bin/prnh/20080411/LAF029-b)

Source: Deep Down, Inc.

· Deep Down Delivers Second 4000 Meter Rated LARS

· Click Here to Download Image

The 4,000 meter rated LARS was specially designed for subsea load handling, lifting and tensioning, and launch and retrieval of specialized undersea equipment, including Remote Operated Vehicles ("ROV"), in ultra-deep and harsh subsea environments. Special functions include auto-variable speed control (load dependent), wire spooling and guide systems, grooved drums, emergency release capabilities, gravity lowering, emergency hoisting abilities, and a water-cooled drum to reduce heat on the umbilical. The safe working load of the LARS is 28 tonnes, and the system is capable of delivering payloads at speeds of up to 76 meters per minute. Another unique feature of this LARS is the specially designed wraparound level wind sensor system which allows for more sensitive yet smoother operation in rugged, high-load, ultra-high deepwater applications. At the customer's request, Deep Down was storing the system at its facilities in Channelview until a vessel was ready to receive it.

About Deep Down, Inc.

Deep Down specializes in the provision of innovative solutions, installation management, engineering services, support services, custom fabrication and storage management services for the offshore subsea control, umbilical, and pipeline industries. The company fabricates component parts of subsea distribution systems and assemblies that specialize in the development of subsea fields and tie backs. These items include umbilicals, flow lines, distribution systems, pipeline terminations, controls, winches, and launch and retrieval systems, among others. Deep Down provides these services from the initial field conception phase, through manufacturing, site integration testing, installation, topside connections, and the final commissioning of a project.

The Company's ElectroWave subsidiary offers products and services in the fields of electronic monitoring and control systems for the energy, military, and commercial business sectors. ElectroWave designs, manufactures, installs, and commissions integrated PLC and SCADA based instrumentation and control systems, including ballast control and monitoring, drilling instrumentation, vessel management systems, marine advisory systems, machinery plant control and monitoring systems, and closed circuit television systems.

The Company's Mako subsidiary serves the growing offshore petroleum and marine industries with technical support services, and products vital to offshore petroleum production, through rentals of its remotely operated vehicles (ROV), topside and subsea equipment, and diving support systems used in diving operations, maintenance and repair operations, offshore construction, and environmental/marine surveys.

The Company's strategy is to consolidate service providers to the offshore industry, as well as designers and manufacturers of subsea, surface, and offshore rig equipment used by major, independent, and foreign national oil and gas companies in deep-water exploration and production of oil and gas throughout the world. Deep Down's customers include BP Petroleum, Royal Dutch Shell, Exxon Mobil Corporation, Devon Energy Corporation, Chevron Corporation, Anadarko Petroleum Corporation, Marathon Oil Corporation, Kerr-McGee Corporation, Nexen Inc., BHP, Amerada Hess, Helix, Oceaneering International, Inc., Subsea 7, Inc., Transocean Offshore, Diamond Offshore, Marinette Marine Corporation, Acergy, Veolia Environmental Services, Noble Energy Inc., Aker Kvaerner, Cameron, Oil States, Dril-Quip, Inc., Nexans, Cabett, JDR, and Duco, among others. For further company information, please visit http://www.deepdowninc.com, http://www.electrowaveusa.com and http://www.makotechnologies.com.

One of our most important responsibilities is to communicate with shareholders in an open and direct manner. Comments are based on current management expectations, and are considered "forward-looking statements," generally preceded by words such as "plans," "expects," "believes," "anticipates," or "intends." We cannot promise future returns. Our statements reflect our best judgment at the time they are issued, and we disclaim any obligation to update or alter forward-looking statements as the result of new information or future events. Deep Down urges investors to review the risks and uncertainties contained within its filings with the Securities and Exchange Commission.

--------------------------------------------------

Source: Deep Down, Inc.

In reply to: None Date:4/11/2008 4:51:17 PM

Post #of 60366

Mako Technologies is hiring ROV Operator personnel (if already posted, apologies)

http://www.makotechnologies.com/Mako_ROV/ROV_employment.pdf