Thermogenesis

Seite 3 von 5 Neuester Beitrag: 25.04.21 02:29 | ||||

| Eröffnet am: | 19.03.11 15:29 | von: Chalifmann3 | Anzahl Beiträge: | 102 |

| Neuester Beitrag: | 25.04.21 02:29 | von: Michelleeeera | Leser gesamt: | 24.352 |

| Forum: | Hot-Stocks | Leser heute: | 9 | |

| Bewertet mit: | ||||

| Seite: < 1 | 2 | | 4 | 5 > | ||||

https://www.bamsec.com/companies/811212/thermogenesis-corp

Bitte Shareholder Lette vom 13.01.2014 beachten (filing vom 16.01.2014)

http://www.sec.gov/Archives/edgar/data/811212/...1214000003/ex991.htm

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Ansonsten: bin erstaunt einerseits, dass sich KOOL die letzten Tage so gut gehalten hat, andererseits spricht es m.E. für eine Stabilität insofern, als ich nun erheblich höhere Kurse für möglich halte. Könnte mir durchaus vorstellen, dass sie die nächsten Monate auf 10 zu/hochläuft.

Grundsätzlich könnte es auch sein, dass nach dem Lauf der Biotech die letzten Jahre die Stammzellen nun einiges an Aufholpotential bieten und insofern NAchhofbedarf haben.

Hier bin ich auf Cytomedix getossen.

Denke, dass ich meine nun doch nicht Cardiome verkaufen, sondern eher meine Real Goods Solar verkaufen werde um hier mit einer kleinen Posi einzusteigen.

Jemand sich mit Cytomedix bisher befasst oder eine Meinung?

Nochmal zu Chali: nach Deinem statement hab ich von Vical Abstand genommen und nicht gakauft, hast schon Recht mit Deinen Argumenten. Die Gentherapie ist wirklich absolut nicht berechenbar. Aber Stammzellen könnten nach dem Mini-P I von KOOL jetzt mehr Aufmerksamt anziehen lohnenswerte Investitionen der nächsten Monate sein.

Gruss an Alle

Wieso?

Habe die KE-News von heute ausgenutzt wg. diesem 1 Satz:

ThermoGenesis intends to use the aggregate net proceeds of the financing primarily for general corporate purposes, as well as for the continued advancement of its pipeline of clinical trials within the cardiovascular and orthopedic markets.

Heute gibts den Webcast über Details zu der Clinical Phase 1b.

die nächste Phase kostet eben ein wenig Geld. Vllt. gibt im Webcast heute genauere Erklärungen. Vllt. gibt zw. webcast heute und Kapitalbedarf einen Zusammenhang.

Vllt. fantasiere ich auch nur.

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Thats my opinion. Hab nicht verkauft, sondern werde, sobald das Börsenwetter einigermassen stabil, ggf. stepwise nachkaufen.

Gruss

Meinst du da kommt was heute in der Konferenz zur nächsten klinischen Phase?

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Geht aber jetzt grad derb runter, mein lieber mann.

Da heisst es jetzt hart bleiben!

Meine Ek ist bei etwa 2 $. Bei 1,80 würd ich die Reissleine ziehen. (darf gar nich dran denken, dass ich schon bei > 50% in 2-3 Tagen schon war, aber wie gesagt, sollten belohnt werden, m.M.)

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Man weis ja nie was so ab 23Uhr kommt. bin immerhin schon 0,1 im Plus. Sind die Transaktionskosten.

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Ich ziehe die Reißleine sicherlich schon früher. Bei 2,20. Wer weiß, ob dies vllt, schon recht zeitnah der Fall sein wird.

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Bin mit 6000 Stück in Cytomedix heute rein: die steigen irgendwie klamm und heimlich.

Gedanklichen SL hab ich hier bei ca. 0,50$ gesetzt.

Nebenbei: Sage und schreibe hat es 13 min. ! gedauert, bis ich bei dieser comdreck bank endlich die Order durch hatte. Zuerst hiess es, finden wir nicht. Ach, muss Platz wechseln (hatte ja gesagt, wo ich kaufen will), dann ist im System nicht hinterlegt, können sie nicht kaufen. Nach Rücksprache mit anderer Abteilung: die letzten Kurse die wir haben sind von Dezember 2013, sie können nicht kaufen. Gegenargument, dass bis dahin heute schon > halbe mio schon gehandelt sind...hin und her und anstatt sie für 0,60 zu bekommen, musste ich 0,63 zahlen. Soviel zu diesem drecksbrocker. Jetzt ruf ich bei cortalc. an, um zu fragen, wie lang die für den Transfer brauchen (sorry Leute, aber das musste ich los werden).

Zurück zu KOOL: es muss irgendetwas faul sein, sonst würden sie bei dem Ergebnis nicht permanent fallen. Die Hälfte hab ich drin gelassen, weil es sein könnte, dass man an billigste Stücke kommen will.

Mal sehen. Jedenfalls ist bei 1,80 Schluss.

Gruss

ThermoGenesis Corp. Raises $6.67 Million in Private Placement Financing

RANCHO CORDOVA, Calif., Jan. 27, 2014 (GLOBE NEWSWIRE) — ThermoGenesis Corp. (Nasdaq:KOOL) today announced that it has entered into definitive agreements with institutional investors in connection with a private placement of common stock and warrants to purchase common stock. Upon the closing of this financing, ThermoGenesis will receive gross proceeds of approximately $6.67 million resulting from the issuance and sale of approximately 3.33 million shares of common stock at a price per share of $2.00. The purchasers will also receive warrants to purchase up to approximately 1.66 million shares of common stock at an exercise price of $2.81 per share. The warrants are non-exercisable for six months after the closing of the financing and have a term of 5 years.

012714 Private Placement Press release Final

Optionen

| Boardmail an "extrachili" |

Wertpapier: Thermogenesis |

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Thermogenesis |

Vorbörslich sah es ja gut aus mit 2,90$

Bei KOOL wird KE doch negativ aufgenommen. Bin heute bei 2,20€ wieder komplett raus. Ausser Spesen nichts gewesen und mal Verlust. Brauche den Verlust um auf Amarantus anzurechnen.

Dara: hatte ich letzte Woche auch mal kurz in Beobachtung. Kurs war da 0,80$.

Die 1,80$ könnten schneller kommen als du denkst.

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Thermogenesis |

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Die MK ist lächrerlich, das Produkt (Wirkstoff Tirofiban, Handelsname in Europa: Aggrastat) "kenne ich persönlich", es is exzellent insofern, als es oft zur Anwendung kommt im medizinischen Bereich in zumindest Deutschland.

Medicura hat die exclusiven Vertriebtsrechte für USA und Nordamerika.

Jedoch auch hier: wo ist der Haken. Es kann doch nicht sein, dass wir die einzigen, die um das Potential der Aktie wüssten/wissen.

Warum seht der Kurs nicht 10 mal höher?

Und schau die die Handelsvolumina an der Heimatbörse an: habs mir gerade angeschaut: bis soeben gerade mal ganz 3000 Stück gehandelt.

Und der Spread in D ist wahnsinn. Werd aber mal 500 Stück in Canada morgen ordern.

Danke nochmal für den Tipp.

Zu Cytomedix: die Bewertung ist schon ambitioniert, jedoch erhoff ich mir einen satten Sprung wg. ihrer stroke-Studie. Es braucht nur ein seeking a. Artikel zu kommen und wird sehen locker den einen $. Aber, bei Erreichen 0,5 würde sie sofortest rausfliegen.

nochmal zurück zu Medicure: hab in nem anderen Board gelesen, dass auch eine Übernahme spekuliert wird seitens Cardiome, die ja bekanntermassen Correvio, dem "Hauptverkäufer" von Tirofiban, schon 11/2013 übernommen haben.

So nun versteh jemand den Kurs: aktuell minus 18% in Canada.

Wieviele Stücke hast Du Chali, wenn man fragen darf. Ich werde morgen 500 kaufen, nicht mehr.

Gruss

Medicure:

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Thermogenesis |

Angehängte Grafik:

z.png (verkleinert auf 79%)

z.png (verkleinert auf 79%)

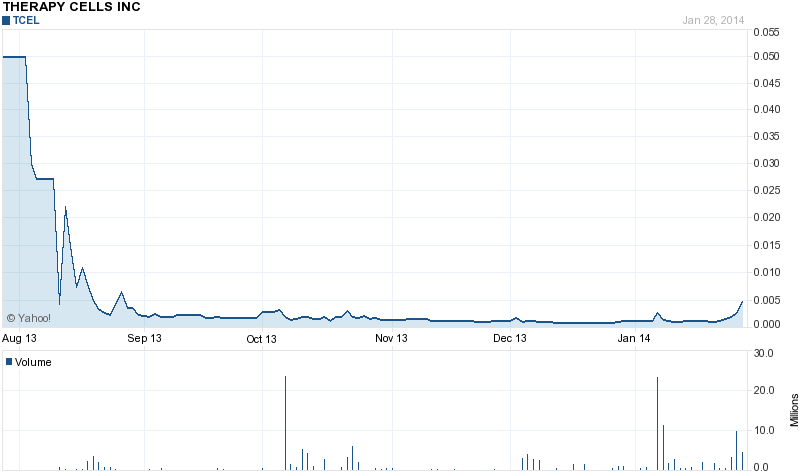

Therapy Cells inc.

Dagegen ist Medicure richtig teuer !! TCEL hat nur eine million aktien und steht bei 0,0047 Dollar,gestern 75% gestiegen,Börsenwert 8000 dollar !! Die haben sogar eine zugelassene Zelltherapy für Rennpferde,die verletzt waren und so wieder fit gemacht werden,es funtionioert offenbar und die Zelltherapy soll jetzt auch für human clinical Trials genutzt werden ......... Lust ein kleiner zock ??!!

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Thermogenesis |

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Thermogenesis |

Angehängte Grafik:

z.png (verkleinert auf 63%)

z.png (verkleinert auf 63%)

Optionen

| Boardmail an "extrachili" |

Wertpapier: Thermogenesis |

Pre heute 9% Plus mit 500 Stücke.

Sabby war 2 Wochen in Oramed aus KE investiert (ersten 2 Januarwochen). Hier könnte es auch so laufen!

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Sobald das Filing von Sabby kommt, dass sie keine Stücke mehr haben stürzt das Teil ab

Optionen

| Boardmail an "ManuBaby" |

Wertpapier: Thermogenesis |

Twentieth Patient Transplanted at the Fortis Memorial Research Institute ("FMRI")

GlobeNewswire

ThermoGenesis Corp. 41 minutes ago

RANCHO CORDOVA, Calif., LOS ANGELES and NEW DELHI, India, Feb. 3, 2014 (GLOBE NEWSWIRE) -- ThermoGenesis Corp. (KOOL) a cellular therapy medical device company and TotipotentRX Corporation, a clinical-stage regenerative medicine company developing novel therapies for cardiovascular and orthopedic disease, announced the TotiPotentRX cellular therapy clinical team in partnership with Fortis Healthcare, Gurgaon (New Delhi) has achieved its 20th pediatric bone marrow transplant (BMT). This haploidentical BMT was performed from a mother as a donor for a 10 year old child suffering from combined immunodeficiency due to a DOCK-8 gene mutation. The Fortis Centre has so far performed 15 allogenetic BMT including five haploidentical and one double unrelated cord blood transplants, and 5 autologous transplants. This transplant was completed on February 1, 2014 at the Pediatric Hematology and Bone Marrow Transplant department led by Dr. Satya Yadav, M.D., Head of the Department for Pediatric Hematology and Bone Marrow Transplant, and with scientific and laboratory support by the TotipotentRX's cell therapy GMP laboratory facility. This 20th transplant is a significant milestone in the pursuit of developing the new FMRI BMT program into one of the leading stem cell transplant centers in Asia.

TotipotentRX provides laboratory services and scientific support to Fortis' cutting edge program at FMRI, some of which employs a proprietary approach to the transplant using the ThermoGenesis AutoXpress AXP(R)and MarrowXpress MXP(R)platforms when the processing of the donor's mobilized peripheral blood or bone marrow is required. These technologies allow for a proprietary transplant approach that increases pediatric patient access to this life saving treatment by enabling the following types of transplants that might otherwise not be an option for the patient:

ABO Major Mismatched Transplants: The AXP/MXP systems effectively remove the undesired red blood cells without compromising the quantity and viability of targeted transplant cells (the "stem cells").

MUD Program: Volume debulking of red blood cells and plasma of matched unrelated donor cells.

Haploidentical Program: Volume debulking of the red blood cells and plasma of a haploidentical donor's cells for improved efficiency of T cell depletion.

Cord Blood Transplant Program: Cord blood processing and storage for the cutting edge double cord blood transplant.

Dr. Yadav remarked, "this 20th transplant is a significant milestone for our patients, our research hospital and our transplant team. Achieving 15 allogenetic and 5 autologous transplants in the first half year of our program is remarkable for any leading academic institution. Our goal is to have the most advanced pediatric bone marrow transplant program in India, whilst taking a global leadership role in advanced therapy like the haploidentical transplant approach. We look forward to continuing our cutting edge program with TotipotentRX as a scientific collaborator."

"This transplant completed on February 1st, propels the FMRI -- TotipotentRX program into the leading center in India for performing Haploidentical transplants, which are the newest advancement in blood-based cancer and genetic disorder treatments," said Ken Harris, Chief Executive Officer of TotiPotentRX. "It is estimated that more than 6,000 BMT procedures per annum in India alone may be enabled with Haploidentical donors, and TotipotentRX is working with Fortis to develop proprietary processes with low mortality and co-morbidity rates. Similar processes are also being developed at leading academic hospital centers in the U.S. and Europe, and we are excited by the global market potential of our proprietary program and devices."

Dr. Venkatesh Ponemone, Director of Laboratory and Clinical Research at TotipotentRX's Indian subsidiary, commented that TotipotentRX's success with Fortis is gaining additional recognition as more hospital chains are contracting their bone marrow laboratory processing with the Fortis-TotipotentRX Centre for Cellular Medicine. The latest services agreement to provide BMT services was signed by TotipotentRX on January 9, 2014 with Artemis Hospitals (Gurgaon).

TotipotentRX Corporation, a U.S. private based cellular therapy research and therapeutics organization (www.totipotentrx.com) develops rapid bedside autologous cellular therapies for cardiovascular and orthopedic indications. They operate world-class clinical research and cellular therapy GMP infrastructure with their clinical partner Fortis Healthcare.

ThermoGenesis Corp., (KOOL) (www.thermogenesis.com) is a U.S. based leader in developing and manufacturing automated blood processing systems and disposable products that enable the separation, preservation and delivery of cell and tissue therapy products.

In July 2013, TotipotentRX and ThermoGenesis Corp. announced they entered into a merger agreement which will operate under the name Cesca Therapeutics. The merger is subject to TotipotentRX and ThermoGenesis stockholder approval, among other condition

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Thermogenesis |

Background of the Deal

On July 16th, KOOL announced the merger with TotipotentRx, a private California company that develops cell-based therapies for regenerative medicine. The terms of the deal were that KOOL would issue stock equal to $18.6m (based on a price of $1.49) and that the new company would be called CESCA which stands for Clinical Excellence in Stem Cell Applications. While the merger was set to close before year end, the deal is now slated to close in Q1/14.

Thesis on the Combined Company

Some of the points below were outlined by KOOL in its proxy; my assessment of the most compelling merits are as follows:

the company will be one of the first to combine cell therapy devices, with patented technology, proprietary cell formulations, and treatment protocols.

KOOL now carries 8 clinical trials (from TotiRx) across various indications, including osteoarthritis, avascular necrosis, cardiac and critical limb ischemia. Specifically, TotiRx is the world's only clinical research organization (CRO) specializing solely in cellular therapeutic development services

KOOL can tap into the existing revenue stream of TotiRx's established cord blood banking business (and its partnership with Fortis Healthcare- a chain of hospitals across India and Asia). Recall that KOOL has its BioArchive System (an automated cryogenic device), which is already used by cord blood stem cell banks in 30 countries for cryopreservation and archiving of cord blood stem cell units for transplant. Further, KOOL's AXP, used for the processing of cord blood (preparing cell concentrates, including stem cells for bone marrow aspirates), should be synergistic with Toti's offering. Management has recently signed long term supply agreements, including one struck earlier in January for 5 years with the San Bruno based Cord Blood Registry.

Established footprint in emerging markets- due to KOOL's legacy US presence, and Toti's Asia core.

Risks to the Thesis

As with any deal particularly those involving development stage companies, there are a few notable risks that investors should watch out for, including:

Clinical Trial Risk- the completed data from the 10 pilot and Phase 1B clinical trials, while proven safe, is still very early and yields substantial risk to commercialize

Autologous cell therapy, in general, has many 'bodies littered on the road' even after safe & effective initial therapies

Cash burn will likely necessitate additional equity raises within the next 24 months, depending on how the cord blood business can ramp

Management execution across geographies (US and Asia) as well as oversight on the clinical programs will require coordination that heretofore had been done by 2 different entities

Why is this an interesting setup?

Today, KOOL trades at $2.20 a share, giving the company a market cap of $37mm, with average trading volume of 2.65m shares a day (or $5mm notional), a decent trading volume given its current market cap. The company currently exhibits low institutional ownership (only 9%), a high beta (1.5), and is still losing money.

Since the day the deal was announced (July 2013), the stock is up 46%, vs. the S&P up 7% over this period. Since mid-January, KOOL stock has risen from $1 to as high as $3, before settling on $2.20; this excitement has been driven by the January 27th announcement that the company has raised $6.67m in a private placement with investors at a price per share of $2, with another 1.66m shares available to purchase at a strike price of $2.81 per share.

This strength of the stock price on the secondary (that the deal was able to be struck at $2 with shares at $1 only a few weeks prior), coupled with the unusually strong liquidity and trading volume for a stock with this market cap indicates that there is a great deal of pent up enthusiasm for the merger profile.

On a risk/reward framework, I look at the shares outstanding (16.7m as per Google Finance) with $6.7m in the bank today, as $0.40 per share, plus the pipeline and patents at $1 per share, to yield $1.50 per share downside; relative to today's $2.20 stock price, this yields a downside risk of 31%. Realistically, it is likely that the shares have strong support at the $2 level, which is only 10% down from current levels.

On the upside, I look at a few factors: the strength of the supply agreements, revenue outlook for the cord blood business, which management disclosed to be $18m annually (in its deck presentation on the website), penetration into the potential $16b market for target therapies. Combined with capital efficiency ($29m in non dilutive clinical trial funding benefits to date) and a peer group selection based on current multiples, it is conceivable that a path to $6 target can be achieved, which would be on the low end of the peer group multiple.

Specifically, when looking at peers such as Cytori (CYTX), Aastrom (ASTM), Athersys (ATHX), Neostem (NBS), Cytomedix (OTCQX:CMXI), Mesoblast (MSB), BioTime (BTX), and Osiris (OSIR), one sees a median revenues of $12m, market cap of $112m, and revenue multiplier of 12x.

When applying this revenue multiplier to Cesca's pro forma run rate of $25m (2014), you arrive at a market cap of $300m, which is ~$6.00 per pro forma share.

Investors would likely gravitate towards the closest comp as Neostem given its dual path of revenue generating businesses (via its PCT) and upside via clinical trial driven product launches. NBS has a market cap of $200m currently vs. KOOL at $37m.

On a $6 target, this would represent a 3x return with ~10-30% downside at risk. I will await more indication as trial data comes in later this year to validate the execution pathway, but it's one that is worthwhile to keep on the radar.

MFG

Chali

Optionen

| Boardmail an "Chalifmann3" |

Wertpapier: Thermogenesis |