SHIP - golden cross on its way!

290.000k volumen

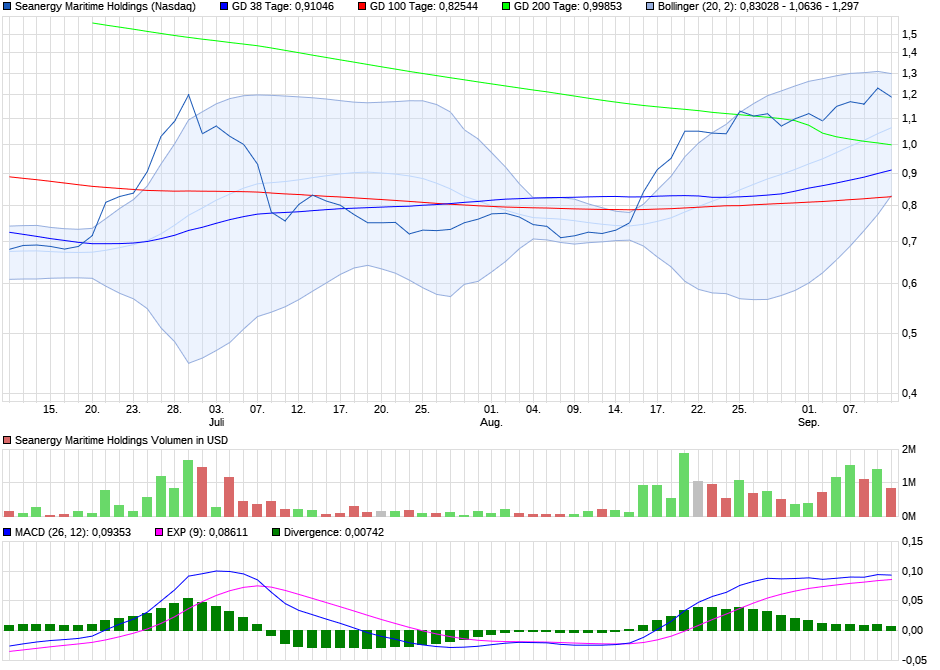

Und man merkt der Verkaufsdruck lässt spürbar nach, das ist die Chance um den Kurs wieder nach oben zu drücken

Angehängte Grafik:

chart_quarter_seanergymaritimeholdings.png (verkleinert auf 54%)

chart_quarter_seanergymaritimeholdings.png (verkleinert auf 54%)

Brokerage houses, on average, are recommending investors to buy Seanergy Maritime Holdings Corp. (SHIP)’s shares projecting a $2 target price. Analysts‟ target price forecasts are a prediction of a stock‟s future price, generally over the 12 months following the release date (Asquith et al., 2005). This forecast is a point estimate that provides investors with a benchmark against which to directly compare stock price in the short run.Target prices made by analysts employed by large brokers, who have access to a greater resource pool, are more likely to be met over the 12-month forecast period.

Mittagspause vorbei Volumen bei 360.000k

Mal schauen das wir heute noch über die 1,20$ kommen

In nächster Zeit wird die 1,20$ dauerhaft übersprungen werden

Aber das volumen ist wenigstens da mit 640.000k und das bedeutet das so langsam aber sicher Aufmerksamkeit erzeugt wird

Angehängte Grafik:

chart_quarter_seanergymaritimeholdings.png (verkleinert auf 54%)

chart_quarter_seanergymaritimeholdings.png (verkleinert auf 54%)

Buy volumen 320.000k Auch sehr gut :-)

50 tägliches Durchschnittsvolumen 440,035K

Eindeutig das Interesse steigt

DRYS Q2 Einnahmen von $ 16.38M (+ 4,0% Y / Y)

SBLK Q2 Einnahmen von $ 62M (+ 77,10% Y / Y)

EGLE Q2 Einnahmen von $ 68.68M (+ 109,83% Y / Y)

GNK Q2 Einnahmen von $ 45.37M (+ 44,21% Y / Y)

SB Q2 Einnahmen von $ 35.01M (+ 33.59% Y / Y)

Um nur einige zu nennen

Man erkennt das bei vielen zweistellige und bei einem sogar dreistellige Prozentzahlen auftauchen, das heißt das sich die Lage der Reedereien drastisch verbessert hat

Gutes gelingen allen Investierten vorwärts SHIP

Seanergy Maritime Holdings Corp. (the "Company") (NASDAQ: SHIP) announced today that it will release its financial results for the second quarter ended June 30, 2017 before the market opens in New York on Thursday, September 14, 2017.

On the same day, Thursday, September 14, 2017 at 9:00 a.m. Eastern Time, the Company's management will host a conference call to present the financial results.

Conference Call Details: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 1(866) 819-7111 (from the US), 0(800) 953-0329 (from the UK) or + (44) (0) 1452 542 301 (from outside the US). Please quote "Seanergy".

A replay of the conference call will be available until Thursday, September 21, 2017. The United States replay number is 1(866) 247-4222; from the UK 0(800) 953-1533; the standard international replay number is (+44) (0) 1452 550 000 and the access code required for the replay is: 2094507#.

Audio Webcast: There will also be a simultaneous live webcast over the Internet, through the Seanergy website (www.seanergymaritime.com). Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

in Dry Bulk Market,Hellenic Shipping News 13/09/2017

Ship owners of dry bulk carriers are cheering the latest surge of the Baltic Dry Index (BDI), which reach a 34-month high on Monday. However, market observers and shipbrokers alike are warning that there’s still quite some way to go, before one can declare that the market is back to its former form. In a tweet yesterday, BIMCO’s Chief Shipping Analyst, Mr. Peter Sand, noted that it would take the BDI to reach 1,200 points, before profitability is achieved for dry bulkers across the board.

Similarly, in its latest weekly report, shipbroker Allied Shipbroking said that “with the Baltic Dry Bulk Index having reached a 34 month high and with some routes on the Capesize Index having reached a three year high, sentiment amongst dry bulk ship owners seems to be at a new high. The spark in trade that lit the market on fire in the midst of the summer period seems to be still firmly driving the market. Most of the market increase has been driven by the increased activity noted in the coal and iron ore trade, with China having driven this demand as they ramped up operations and kept their production levels at an all-time high”.

According to Allied’s George Lazaridis, Head of Market Research & Asset Valuations, “things haven’t been as clear cut though when one notes the details under which these trends have evolved. Most of this increase in imports of both coal and iron ore has been driven by the decision made one year back by the Chinese government to reduce production levels of its coal and steel production, with the former set to be cut by roughly 800m tonnes (25% of its production in 2016) and the latter set to be cut by around 100-150m tonnes (nearly 20% of its production in 2016). In the case of coal, the gain has been relatively simple and direct. The cutting back in local coal production has made China more reliant on seaborne imports which in some cases is sourced by as far away locations as U.S. and Canada. This has helped reverse the affect that had been brought about by the smaller reliance on coal that had been undertaken by China, having pushed imports back to normal levels. This has been equally reflected by the increases over the past year and a half in the price of coal”.

Lazaridis added that “in the case of steel products, things have been slightly more complicated. The steel and iron ore industry has seen an equally impressive recovery in terms of the prices, however the above-mentioned production cuts by China would indicate a softening in import volumes of iron ore and metallurgical coal. As the current efforts stand, most of the production cuts have focused on the more troubled steel producers, closing down excess capacity which was already having difficulties in competing in the current market. Through these measures most of the remaining producers have had the opportunity to grasp a better share out of the high-end market, while also focusing on getting their hands on higher -end quality iron ore and coal in the market, both of which are typically sourced from outside China”.

Allied’s analyst added that “at the same time, the Chinese government has tried to cap steel mill production levels in several provinces during the winter months in an effort to curb air pollution in some of its major cities. Both of these efforts however seem to have pushed for higher utilization levels of the remaining steel mills, as they try to ramp up production during the rest of the year and have taken up the market slack left behind by the closure of the lower tier mills. This could mean that we may well see the seasonal trends of this market radically change during the next couple of years. There are signs of caution in the wind as always, with talks of a curb in coal imports by the Chinese government in order to boost the performance of the remaining coal mines, something that could cut back some of the recent trends in import volumes that have been noted over the past couple of months. At the same time, we are seeing a slowdown in the main drivers for local steel products, namely the propertymarket rally and the government’s sustained splurge in infrastructure. Both of these have shown some initial signs of a slow-down, though these may turn out to only be a temporary correction and against the overall trend”, Lazaridis concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide

in Dry Bulk Market 13/09/2017

The Baltic Exchange’s main sea freight index, tracking rates for ships carrying dry bulk commodities, snapped a six-day winning streak on Tuesday, weighed down by weaker rates for capesize vessels.

The overall index, which factors in rates for capesize, panamax, supramax and handysize shipping vessels, ended down 11 points, or 0.81 percent, at 1,344 points.

It had touched near three-year highs on Monday.

The capesize index broke a five-session gaining streak to close down 89 points, or 3.16 percent, at 2,724 points.

Average daily earnings for capesizes, which typically transport 150,000-tonne cargoes such as iron ore and coal, were down $889 to $19,942.

The panamax index was up 35 points, or 2.51 percent, at 1,429 points.

Average daily earnings for panamaxes, which usually carry coal or grain cargoes of about 60,000 to 70,000 tonnes, increased $285 to $11,477.

Among smaller vessels, the supramax index fell ten points to 908 points, while the handysize index rose four points to 513 points.

Source: Reuters