Die besten Gold-/Silberminen auf der Welt

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Gold |

Angehängte Grafik:

screenshot_2024-03-27_080924.jpg (verkleinert auf 45%)

screenshot_2024-03-27_080924.jpg (verkleinert auf 45%)

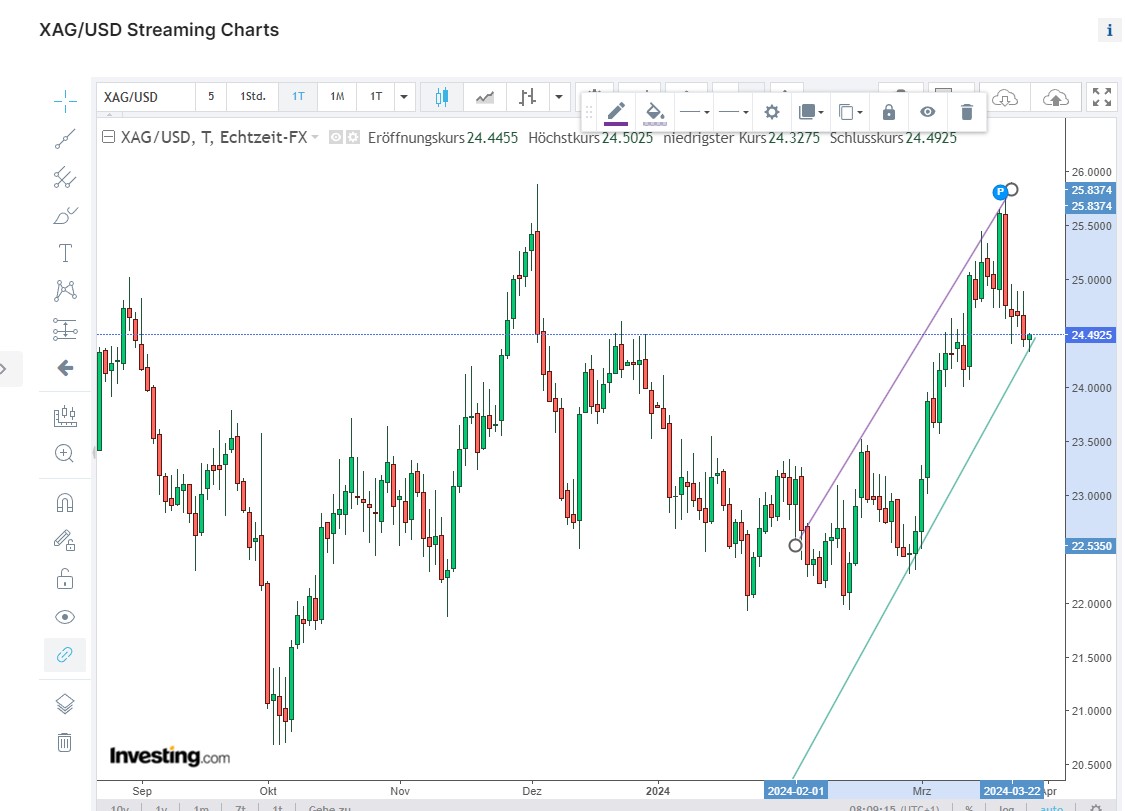

Ob es so kommt ist jedoch fraglich.

https://www.goldreporter.de/...ld-verstaerkt-sich/gastartikel/242441/

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Gold |

Seit 2016 von unter 5 cad auf in der Spitze 20 cad angestiegen. Es gibt die guten Minen die man jedoch erst mal finden muss und ein wenig Glück gehört natürlich auch dazu.

Gerade in den letzten Jahren gab es einige Vervielfacher über Jahre. Great Bear Resources und Kirkland waren da mit die besten gewesen.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Wenn ein ceo Aktien von seinem Unternehmen aufkauft und diese hält wo ist das rumgeschiebe.? Merke Dir eins wenn das Sentiment schlecht ist werden gute Unternehmen auch nicht gekauft. Ganz einfach. Gerade im Rohstoffreich leider ganz normal.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Außerdem hast du auch nichts gesagt das der alte CEO Kohle aus der Firma rausgeschafft hat.

Das Managment hat nichts mitbekommen.Ja ne ist klar.

Optionen

| Boardmail an "silverfreaky" |

Wertpapier: Gold |

VIZSLA SILVER AGREES TO ACQUIRE NEWLY CONSOLIDATED PAST-PRODUCING SILVER DISTRICT IN THE EMERGING SILVER-GOLD-RICH PANUCO #CEOBriefBot

- Vizsla Silver Corp. hat sich bereit erklärt, den in der Vergangenheit produzierenden Distrikt La Garra-Metates in Mexiko zu erwerben, der für seine silber- und goldhaltigen Adern bekannt ist.

- Das Gebiet umfasst 16.962 Hektar und hat zwei bedeutende Adersysteme mit einer Streichenlänge von 2,6 km bzw. 1,8 km.

- Im La Garra-Metates-Distrikt wurden bisher nur minimale Explorationen und keine Bohrungen durchgeführt, obwohl die historische Produktion hier Jahrhunderte zurückreicht.

- Die von Vizsla Silver durchgeführten Probenahmen ergaben Silberäquivalentgehalte von mehreren Kilometern entlang des Streichens, was auf das Potenzial für hochgradige Ausläufer entlang des Streichens und in der Tiefe hinweist.

- Der Erwerb des La Garra-Metates-Distrikts erweitert das Portfolio von Vizsla Silver im Sinaloa-Silbergürtel um ein äußerst aussichtsreiches Gebiet mit vielen Edelmetallen und positioniert das Unternehmen für potenzielle größere Entdeckungen und eine wachsende Pipeline mit potenzieller Produktion.

Vollständige Pressemeldung: (https://ceo.ca/@newswire/...ver-agrees-to-acquire-newly-consolidated)

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Gold |

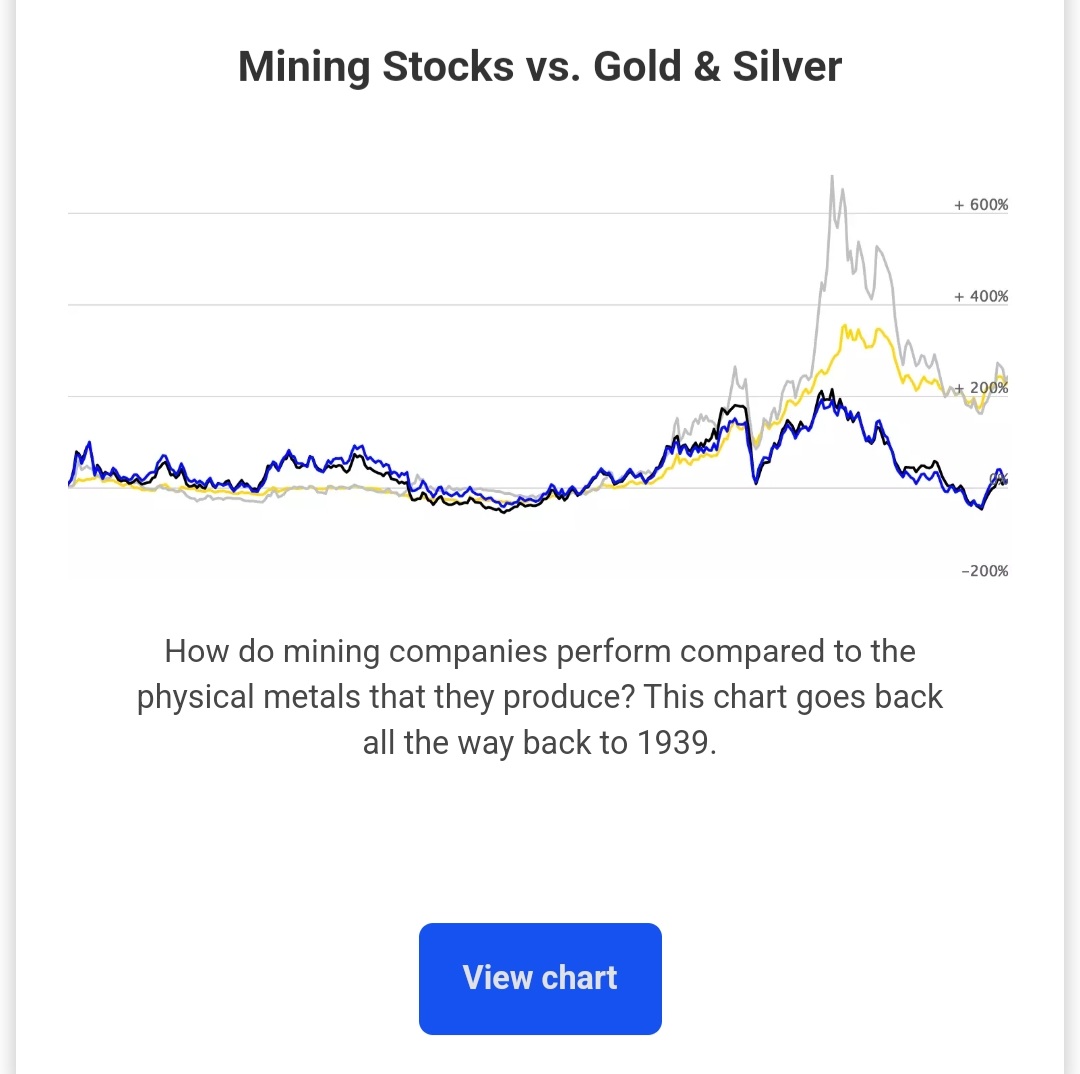

Hier ein paar gute Charts zum Thema:

https://www.longtermtrends.net/

https://www.longtermtrends.net/mining-stocks-vs-gold-and-silver/

Angehängte Grafik:

screenshot_20240328-....jpg (verkleinert auf 47%)

screenshot_20240328-....jpg (verkleinert auf 47%)

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Die Pennystocks natürlich nicht.Das ist aber normal, die kommen dann später, falls sie überleben.

Optionen

| Boardmail an "silverfreaky" |

Wertpapier: Gold |

https://www.miningmx.com/top-story/...ofit-from-sky-high-gold-prices/

The entire effort is a feat of engineering and human perseverance in punishing conditions. Because it’s so far underground, heat is a major problem. Virgin rock is about 52ºC. As a result, Harmony uses 265 tons of ice an hour for refrigeration purposes. Refrigeration, transport, ventilation and a host of other requirements require energy totalling 65,000MWh, equal to 80,000 households and burning a normal household’s monthly consumption every 22 seconds.

Optionen

| Boardmail an "silverfreaky" |

Wertpapier: Gold |

Interestingly, gold’s Open Interest has declined on this bullish move when one would expect a stampede of buying. From its peak on 21 March, in five trading sessions Open Interest declined by nearly 38,000 contracts. Clearly, the Swaps category comprised mostly of bullion bank trading desks are running for cover instead of riding it out with a view to taking out flaky speculators at the first sign of profit-taking.

The Swaps must know something to explain this behaviour, and that can only involve physical demand and supply. Further evidence has emerged from London this week, where jumps in the bullion price coincided with the morning fix, while for the rest of the time the price hardly moved.

This behaviour indicates that overnight and in the early morning London time, bullion banks have seen substantial demand from Asia, demand which is closed out on the fix driving prices sharply higher. With a general lack of physical liquidity, the bullion banks dare not play their normal pump-and-dump activities on Comex. Perhaps on Monday, when London will be closed, there will be an opportunity for the Swaps to hit prices hard.

The fist day of delivery for the Comex April contract was yesterday (28 March), and a massive 5,236 contracts were stood for delivery, representing 523,600 ounces (16.29 tonnes) for a total of 602,400 ounces for the week. It brings the total for the first quarter of 2024 to 37,201 contracts (115.71 tonnes). Silver deliveries this week were also high, amounting to 389 contracts representing 60.5 tonnes.

In previous market reports, I have pointed out the extraordinary situation where gold is going strongly into new high ground and the level of public participation and interest is as if gold was still in a bear market. The bullish position is clearly shown in the technical chart below.

The price and moving averages are in bullish sequence, and we are witnessing a break-out following a major consolidation, lasting 43 months so there is lots of catching up to do. Furthermore, the move into the consolidation is a guide for the extent of the subsequent move out, giving a price target of nearly $3000.

As I have also pointed out, it is not so much gold rising, as the dollar and all dependent currencies falling in their purchasing power. This is the motivation for central banks and sovereign wealth funds to accumulate bullion as a safe haven in their reserves. This leads us to question why is it that this safe-haven trade appears to be accelerating, when the consensus in western markets is that inflation is yesterday’s problem and later this year we should begin to see interest rate cuts.

It would appear that this view is not being shared in the “deep financial establishment”, particularly in Asia which every morning this week has been cleaning London out of bullion on the morning fix. It can only have concluded that there is a looming currency crisis, encouraging them to sell dollars and buy gold, irrespective of price.

Danke für die Erklärung klingt nach einem Tenbagger wenn man alle Probleme gelöst hat und selbst wenn es weniger wir vom Kurs geht es in die richtige Richtung

Hoffe schaust mal bei MMY vorbei die kommen langsam auch wieder in die Produktion und sind auch genau so am Boden wie Elevation Gold Mining bräuchten ja auch mehr aufmerksamkeit im Forum

genau so wenig los auf wallstreet online wie bei Elevation Gold Mining im Forum

Optionen

| Boardmail an "silverfreaky" |

Wertpapier: Gold |

Ein Problem ist die Geschäftsführung.Nicht nur hier.Generell mal mehr mal weniger.

aus https://stockhouse.com/companies/bullboard/t.aris/...?postid=35956195

RE:Aris Approaching 52 Year High

We need a solid close over 4.70 to get those underwater shorts nervous. It depends somewhat on whether or not, the shorts own the Aris B series warrants. They are 2.21 strike expiring April 30th with nearly 9 million outstanding. A B series warrant holder short has an automatic cover price of 2.21 no matter how high the stock goes. However, any other investor or institution does not have that fixed price point.

A week from Friday (April 5), the 4.75 strike convertible expires, which will add 3.8 million shares to the outstanding total. After thinking and researching about it, the Convertible expiration should be a nothing burger for the stock.

I do expect in May, after the B warrants are exercised and no more in-the-money cover point, that shorting intensity will be reduced. I've seen it before in miners after warrants are exercised, the stock tends to experience more bullish trade.

Comment on this Post

Optionen

| Boardmail an "silverfreaky" |

Wertpapier: Gold |

Interessant, normalerweise gibt es keine klaren Infos.

Angehängte Grafik:

screenshot_20240330-....jpg (verkleinert auf 47%)

screenshot_20240330-....jpg (verkleinert auf 47%)

https://www.youtube.com/watch?v=C1dCCo6ZG4A

Excelsior Prosperity w/ Shad Marquitz – 03/27/2024

MAR 28, 2024

2

I’m sending out this Special Report late today, because key sector news hit this morning. It threw a real monkey wrench in my intended [Part 6] update…. that I was planning to put out later this week on Argonaut Gold. I had recently pointed out that Argonaut was a really beaten up growth-oriented gold producer that I’d been starting to accumulate more seriously, since the recent fishing line selloff in late February; (as I’d messaged to you all in Part 5B in this series on growth-oriented gold producers).

As many likely noticed this morning, Alamos Gold (TSX: AGI) (NYSE: AGI) announced an offer to take over Argonaut Gold (TSX: AR) (ARNGF). So we have another merger on our hands here. This makes putting out a big update on the investing thesis in Argonaut a moot point now, but we’ll still unpack this transaction together as an instructive investing lesson for readers here in Part 6.

Additionally, I’ll also feature some other key news from Karora Resources about a potential merger in the works, and tee up a different growth-oriented gold producer that also just announced a merger this week, further down in this article.

(Anybody else noticing a trend with all these quality growth-oriented producers and mergers lately. I feel like we just got done talking about Calibre Mining’s takeover of Marathon just a few issues back. This is where the value is.)

Synchronistically, I had just pointed out, in a recently published article last week on this channel called “Gold And Silver Popped – Now What About Your PM Stocks?”, that I considered Alamos Gold the “king of the Mid-tier gold producers.”

I had highlighted their incredibly strong price chart over the last 5 years compared to most other gold equities, and pointed out they were a well-run company, with quality assets, and a prior portfolio holding of mine until just last year. For those that missed that article, there were a number of other solid companies and sector charts showcased in it, (still worthy of review):

https://excelsiorprosperity.substack.com/p/...r-popped-now-what-about

So first off, let’s take a quick look at the news out today on this transaction where Alamos is scooping up Argonaut on the cheap. We can definitely say that Alamos Gold is growing their production profile on the back of this acquisition news, and that is very fitting for this series and focus on growth-oriented gold producers. I’d also like to give a hat-tip to the team at (AGI) for picking up a fantastic deal and future growth through the bolting on a Tier 1 asset in Tier 1 jurisdiction with the Magino Mine, in Ontario, Canada.

We should also mention that there is another interesting aspect of this merger transaction, where the other Argonaut Gold portfolio assets, the Florida Canyon Mine in Nevada and the La Colorada and El Castillo mines in Mexico, are being spun out into a new company. This means Argonaut shareholders will get the upside takeover premium from the Alamos takeover, as well as shares in the new spin-co. (Interesting)

Alamos Gold Announces Friendly Acquisition of Argonaut Gold - March 27, 2024

https://www.argonautgold.com/English/...of-Argonaut-Gold/default.aspx

“As part of the Transaction, Alamos will acquire Argonaut’s Magino mine, located adjacent to its Island Gold mine in Ontario, Canada. The integration of the two operations is expected to create one of the largest and lowest cost gold mines in Canada. The addition of Magino is expected to increase Alamos’ combined gold production to over 600,000 ounces per year, with longer term production potential of over 900,000 ounces per year. The combination materially enhances Alamos’ position as a leading, Canadian focused, intermediate producer, with growing production and declining costs.”

“Concurrently with the Transaction, Argonaut's assets in the United States and Mexico will be spun out to its existing shareholders as a newly created junior gold producer ("SpinCo"). SpinCo will own the Florida Canyon mine in the United States, as well as the El Castillo Complex, the La Colorada operation, and the Cerro del Gallo project, located in Mexico.”

“Under the terms of the Agreement, each Argonaut common share outstanding will be exchanged for 0.0185 Alamos common shares and 1 share of SpinCo. The Exchange Ratio implies estimated total consideration of C$0.40 per Argonaut common share, or US$325 million. This represents a 34% premium based on Argonaut's and Alamos' closing prices on March 26, 2024 on the Toronto Stock Exchange, and a 41% premium based on both companies' 20-day volume-weighted average prices. Total consideration includes C$0.34 of Alamos common shares, based on the closing price of Alamos common shares on the TSX on March 26, 2024, and SpinCo common shares with an estimated value of C$0.06.”

Again, as most readers here will recall, I was personally accumulating shares in Argonaut Gold a few weeks back, after the wild waterfall decline in AR shares in late February. Just for a frame of reference, on Friday February 23rd (AR) opened at CAD $0.375 and closed at CAD $0.36. Then on Monday February 26th, after issuing a very disappointing news release to kick off the day, the shares opened at CAD $0.305 (already down bigly from pre-market trading), then putting in an intraday low at CAD $0.225, and then closing that day at CAD $0.235. On February 20th (AR) had been a CAD $0.395 stock and in January over CAD $0.40, but now it had essentially been cut in half just a week later.

While I definitely recognized the challenges the Argonaut operations team was having at Magino, it seemed really extreme for the company to have lost so much of it’s valuation in such a brief amount of time, (especially after the horrid 2 years of stock performance leading up to that). This news was front and center for me, because I had taken out an initial starter position in Argonaut on Nov 22nd last year, and even though the position size was very small in my portfolio, I didn’t like seeing the big haircut in share price.

The move just seemed so overdone, that after parsing that news and mulling over the risk/reward potential, I couldn’t help starting to buy 3x more shares on Wednesday Feb 28th, just 2 days after the crash in share price, (the day after it had made an even lower low on Feb 27th down to CAD $0.215).

Over that weekend, I wrote the article here on this channel, where I teased that Argonaut Gold would be the next company featured in that series, due to this chain of events and share price smash down, and that I had started to accumulate the weakness that prior week.

Opportunities With Growth-Oriented Gold Producers – Part 5B

Excelsior Prosperity w/ Shad Marquitz - 03/03/2024

https://excelsiorprosperity.substack.com/p/...ith-growth-oriented-f28

Here is the section on Argonaut that I teased at the end of Part 5B on March 3rd:

“OK. Time for the next company in this series. After already having a really tough 2 years prior, and becoming the poster child for cost overruns and missed timelines, this company has been severely punished for it’s sins. However, when more news broke about challenges with selective mining, 5-10% lower grades expected for throughput, lower anticipated ounces in guidance, and the reality that they’ll need more money… the share price was further chopped in half. I’m talking of course about Argonaut Gold (TSX: AR) (OTC: ARNGF). (Yes, that’s right, I said Argonaut Gold).”

“Please… before you throw pies and rotten tomatoes at me though, at least suspend passing judgement on this provocative and likely polarizing selection, until you read Part 6 in this series where we’ll unpack together the good, the bad, and the ugly about Argonaut Gold. I’m happy to freely share my thinking and rationale behind the decision to accumulate more shares this last week into the recent weakness and market carnage. I also acknowledge that while this is definitely risky, it may not be as risky as it is being currently perceived (especially after the recent waterfall decline).”

“Yes, their key new mine, Magino, has been a complete mess getting developed and constructed for the last 2+ years, with more problems surfacing again 2 weeks back. We’ll get into the big picture view of where things are going, and address some specifics in that recent news announcement that has led to the stock being essentially chopped in half in market cap valuation, once again, over the last 2 weeks.”

“That aside, Argonaut Gold is going to be a legitimate growth-oriented gold producer at the end of this saga. It is run by a much more solid management team and board now than in the past, and Magino is absolutely still going to be transformative to the company, in a similar way that Greenstone is going to be transformative for Equinox. These things take time to play out though, and we’ll discuss warts and all in the next Part 6 of this series, so stay tuned for that down the road.”

So, again, it does not really make sense at this point to do a deep dive in Argonaut Gold investing thesis, because now it has spiked up due to the takeover news premium. However, I’d point out (and was planning to point out in the article I was already working on for release later this week) that AR had already started to ratchet higher in share price and valuation, just 3 days after I put out that missive teasing taking advantage of the selloff in Argonaut. This was because on March 6th, the company published the 4th quarter and 2023 year-end operations report, and then it suddenly dawned on many investors that the market had definitely over-reacted to the downside all things considered. (Geeze, do ya think?)

Argonaut Gold Announces Fourth Quarter and Year End Financial and Operating Results

https://s22.q4cdn.com/115151820/files/...press-release-2024-03-05.pdf

Really, this bounce up after the March 6 news release is still a key takeaway to pick up from the Argonaut saga during the month of March 2024. There are often fantastic value-accretive moments, for us as contrarian investors, after an insane fishing line selloff.

So often in this small universe of junior mining stocks, (especially when coming out of a very bearish period in the sector the last 3-4 years), when the retail and institutional markets sense bad news, these companies tend to overcorrect in a massive way. The converse is also true, that things tend to get way overbought on good news, especially during more bullish sentiment periods. This sector loves to go to extremes on both sides of the trade.

I had highlighted those same types of fishing line sell-off over-reaction moments in the prior gold article “Gold And Silver Popped – Now What About Your PM Stocks?” with regards to both Calibre Mining on the Nicaraguan sanction news, and on Gatos Silver on the resource estimation mistake swan dive in valuation. Those were other fantastic contrarian accumulation periods, when stocks got so oversold down to ridiculous valuations. As the saying goes, “buy when there is blood in the streets.”

That same type of over-reaction was most assuredly the case here with Argonaut Gold, where the selloff had gotten down to ridiculous valuation levels in late February. I sure felt confident buying on February 28th, when the backdrop was a chorus of several days of hateful messages on chatboards, suggesting the company was going bankrupt and thoroughly trashing the company management, existing shareholders, and the PM sector overall.

Emotional human beings (especially resource investors) love to take things to extremes. Retail hordes, often commiserating on all things negative, love to come up with worst-case scenarios, selling first and asking questions later (or not even asking questions). I’m sympathetic to those selling at a huge loss, but often they sell at precisely the wrong time, (like so many did on Feb 26th - Feb 29th), asking for management’s head on a stake, and yelling into the clouds about how terrible investing in this gold sector is.

Like all investing, it totally depends on what pricing level one buys any stock at, their timeframe, and then what price level one sells it at. That is a completed trade; and by default, all investors are traders at one point in the process. Question: Was Argonaut a terrible trade for all those investors buying the last week of February or early March in the low CAD $0.20’s, only to see (AR) close a few weeks later this afternoon at CAD $0.40?

It’s all relative, and sometimes the very best trades occur during a very short period of time, and retail investors need to act quickly during over-reactions to the downside or upside to get an edge over institutional investors.

My personal plan now (always subject to change if the data changes) is to hold my Argonaut Gold shares for the merger into Alamos Gold, so that I can pick up the “SpinCo” shares on the Nevada/Mexican assets. I have a lot of respect for Alamos Gold, as already mentioned, but I’ll likely sell out of those converted shares, on the next strong upleg in the gold mid-tier producers to ring the register on this trade. Alamos Gold has done fantastic over the last 5 years, but it is far more fully valued now, especially with so many eyeballs on it. I’d rather pick up the Spinco, let the Argonaut shares become Alamos shares, sell them, and then rotate those funds into so many other gold names in the space that are still hammered down to silly valuations.

Alright, enough said with this one, but hopefully folks reading got some investing and trading ideas out of diagnosing this March Madness saga with Argonaut Gold.

OK, so here are 2 more updates on different growth-oriented gold producers, as we finish out Part 6 in this series.

1) Another growth-oriented gold producer that I’ve written about in a few these articles and provided updates on is Karora Resources. Well, they put out a key piece of news today, regarding all the market speculation about what may happen to them potentially combining forces with Ramelius Resources. It looks like that deal is now off the table.

However, the news today does importantly state that Karora is in talks with a “new third-party regarding a potential business combination.” I’m not sure (and nobody is really) if this will be a takeover of Karora, them taking over another company, or more of a merger of equals. The point is that Karora resources has options as solid growth-oriented gold & nickel producer hitting their stride. I could definitely see why a larger company would want to acquire (KRR) for both their gold and nickel endowment, and huge exploration upside. Likewise, I could see how Karora has the leverage now to acquire a smaller company or transact in a merger with a comparable company.

Karora Resources Provides Update On Exclusive Discussions

March 27, 2024

“Karora Resources Inc. (TSX: KRR) (OTCQX: KRRGF) notes the announcement today by Ramelius Resources Ltd (ASX: RMS) that it is no longer in exclusive discussions with Karora regarding a potential transaction. Karora confirms that it has exited such discussions.”

“Karora also confirms that it is currently engaged in exclusive negotiations with a new third party regarding a potential business combination. No definitive agreement has been reached and there can be no assurance that any transaction will result from these discussions.”

https://www.karoraresources.com/...es-Update-on-Exclusive-Discussions

So, we’ll need to keep tabs on how this story with Karora unfolds, which company is the new 3rd-party entity, and what the new combined company will be. Any way one slices it though, they’ll be growing into a larger story, and again this perfectly aligns with the theme of growth-oriented gold producers we’ve been discussing.

2) I’ll go ahead and tease the next company that will be featured in full in Part 7 of this series – Mako Mining (TSX.V:MKO – OTCQX:MAKOF). Speaking of all this M&A, they also announced an acquisition this week of Goldsource Mines for their 100% owned Eagle Mountain Gold Project in Guayana, South America.

At the very end of Part 4 in this series I mentioned we’d cover Mako Mining. The reason for the delay was that then there was a flood of news from the first 4 companies discussed (i-80 Gold, Calibre Mining, Equinox Gold, and Karora Resources), so all of part 5A & 5B was consumed with those updates, and then the crash in Argonaut Gold that had just happened.

Mako Mining is demonstrating this week that they are not just growing through organic exploration and production, but also now growing through acquisition.

Mako Mining to Acquire Goldsource Mines Creating a Scalable Diversified Gold Producer with a Platform for Growth - March 26, 2024

https://makominingcorp.com/news/index.php?content_id=348

Synchronistically for this article, over at the KE Report yesterday we were able to speak with Akiba Leisman, President and CEO of Mako Mining, just after the news broke. In the interview linked below, we review the key synergies and scalable diversified growth potential with the announced agreement to acquire Goldsource Mines (TSXV:GXS)(OTCQX:GXSFF) and their 100% owned Eagle Mountain Gold Project in Guyana, South America. This project and team will complement the existing Mako operational team, currently exploring for and producing gold at the San Albino Project in Nicaragua.

We have Akiba outline how the combined company will bring together two experienced management teams, that have worked together as colleagues going back nearly two decades, which is expected to make integration of the two companies more seamless in a true “hand-in-glove” partnership. In addition to the geographical and asset diversification, the district-scale exploration potential in Guyana will enhance Mako’s current growth trajectory and exploration upside already found in Nicaragua.

Akiba mentioned the scalability of Goldsource’s Eagle Mountain is very much a direct analogue to that of Mako’s San Albino mine, and that there are a number of similarities between the two projects, thus highlighting the proven experience that the Mako Mining operations team can bring to the table. The new pro-forma Mako will have the cash flow and project pipeline to establish a platform for growth, operated by teams proven in the construction and operation of scalable mines with low capital intensity profiles.

Mako Mining – Key Synergies & Diversified Growth Through The Acquisition Of Goldsource Mines

Well this was a wild update here in Part 6, and again, whether readers were invested in Argonaut Gold or Alamos Gold or not, hopefully there were still some good junior mining stock investing nuggets and takeaways.

One of my big takeaways is that so far in this series we’ve only discussed 6 companies and 4 of them (Calibre, Karora, Argonaut, and Mako) have become involved in the latest mergers and acquisition deals. In the most recent article on gold, I also mentioned 3 gold stocks and one silver company, and one of those companies (Alamos Gold) was also involved in one these M&A deals. This just demonstrates the huge value stored up in these growth-oriented gold producers.

Thanks for reading and wishing you all prosperity in your trading and in life!

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Sogar unsere Sibayne verdient endlich Geld mit Gold.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |