Pfizer - zu Unrecht im Keller

Seite 91 von 199 Neuester Beitrag: 07.08.25 15:29 | ||||

| Eröffnet am: | 21.10.04 12:39 | von: Anti Lemmin. | Anzahl Beiträge: | 5.956 |

| Neuester Beitrag: | 07.08.25 15:29 | von: Highländer49 | Leser gesamt: | 1.595.588 |

| Forum: | Börse | Leser heute: | 134 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 88 | 89 | 90 | | 92 | 93 | 94 | ... 199 > | ||||

Hoffe ihr seit nicht Standhaft gebleiben und habt die Notbremse bereits gezogen?

Ansonsten viel Glück.

Und ob da Pillen helfen?

fällt."

"Das Ziel dürfte eher in der Mitte der Möglichkeiten liegen: bei etwa 22,-Dollar..."

Das Eine habe ich geschrieben, das Andere Du. Wer was geschrieben hat, ist egal.

Es ist bis auf Marginalien das selbe.

Deine (rationalen) Erörterungen zu PFIZER in Ehren; ich will sie auch gar nicht

kritisieren - aber die Börse tickt nicht rational. Häufig genug wird sie bestimmt

von irrationalen "Selbstverstärkungs"-Faktoren, die dem Kurs einen eigendynami-

schen Drall geben. Eine "Überwachungsbehörde", die sagt "nun ist genug", gibt es

nicht. - Deswegen sprach ich ja von der Rolle der "Meinungsmacher": das sind

Analysten, Experten, Journalisten und...das Unternehmen selbst.

Folgendes ist in Deinem Beitrag #2246. nicht zutreffend:

-TUI ist kein Favorit von mir. Ich hatte und habe TUI untergewichtet. Insgesamt

hatte ich nie mehr als 4%. Andere Positionen sind bei mir mehrfach größer. Es

mag lediglich der (falsche) Eindruck entstehen, TUI sei ein Favorit von mir, weil

ich relativ viel und engagiert darüber schreibe. Das hat aber einen ganz anderen

Grund: kaum eine Aktie wird derart falsch eingeschätzt; das reizt zum Wider-

spruch.

-der die Netto-Verschuldung TUIs (2,9 Mrd.) übersteigende Substanzwert ist un-

ter "Experten" keineswegs umstritten. Dazu bedarf es lediglich eines Blicks in die

Bilanz; und dazu braucht man kein Experte sein. Umstritten ist hingegen der sog.

innere Wert. Bei diesem sind u.a. die materiellen stillen Reserven dazuzuzählen;

und da haben die meisten ihre Schwierigkeiten. Nach meiner Einschätzung (ich

hatte selbst jahrelang mit Bilanzen, Bewertungen etc. zu tun), bewegen sich

alleine die stillen Reserven der Schiffe und Flugzeuge im Milliardenbereich.

Justin Ferayorni

Pfizer: worst case scenario

12/4/2006 8:00 AM EST

Pfizer dropped a bomb on Saturday - Torcetrapib development has been dropped due to adverse event rates in the drug group, namely higher mortality and cardiovascular events. The independent Data Safety Monitoring Board (DSMB) notified Pfizer of the side effects. This pulls the rug out from under Pfizer's defense and conversion strategy for Lipitor. We can now say with near certainty that Lipitor and its $12+ billion in annual sales will be lost at the turn of the decade. I estimate the drug contributes between 65 and 80 cents of earnings per share per year currently. It's anybody's guess, but I'd argue the stock should trade in the $18-22 range after this announcement. I hope to get an article out shortly on what I think the stock is worth now. The dividend yield will certain help keep the floor on it for certain.

As for the rest of the drug group and the market more broadly, there should be little real impact. If you are interested in owning other drug stocks I'd use weakness associated with this announcement as an opportunity.

Pfizer's Quiver Now Shockingly Bare

By Jim Cramer

Street.com Columnist

12/4/2006 7:23 AM EST

Maybe they really are a bunch of jokers at Pfizer (PFE). Either that, or their timing is just nightmarish. I can't believe that two days after the company extolled its new cholesterol drug at its analyst day that they scrap it.

I know most people who peripherally follow this company may ask how one far-away drug could be so important. But frankly, I didn't see anything else at Pfizer that could make up for even a fraction of the lost revenues for Lipitor.

You are now in Bristol-Myers (BMY) mode for Pfizer, meaning that BMY post-Plavix going generic had surprisingly little going on. I still believe BMY may have to cut its dividend when the full brunt of 2007 losses at Plavix get realized. (Either that or sell itself to Pfizer now that Pfizer has lost its future.)

The truly nutty thing about all of this is that Pfizer's meeting last week now appears to be much ado about nothing, a manufactured guide-up that was really about one thing: Don't lose faith in Pfizer, we have this new cholesterol drug!

I panned [verreißen - A.L.] Pfizer aggressively in these pages and the airwaves, in part because I just believe that companies with no real sales growth don't belong in peoples' portfolios. I was bombarded by people reminding me that Pfizer's about to launch this new drug that would save them.

Man, those critics must be quiet right now. As for me, as I said at the end of Confessions of a Street Addict: better to be lucky than good.

Analysten rechnen für 2007 mit einem Pfizer-Gewinn von rund 2 Dollar pro Aktie. Daran wird sich vorerst auch nichts ändern, da Lipitor ja noch bis 2011 am Markt bleibt. Die 65 Cents Gewinnanteil von Lipitor entsprechen daher dem von mir in # 2255 geschätzten Gewinnanteil von ca. 33 %. (80 Cents, das obere Ende von Ferayornis Spanne, halte ich für zu hoch angesetzt).

Zurzeit steht PFE in NY vorbörslich bei 23,78 USD (minus 14,6 %). Das entspricht bislang den von mir gestern geschätzten minus 15 %.

Das sind schon fast wieder Kaufkurse. Mir persönlich ist Pfizer "ohne" Lipitor (und die ganze Zocor-Angst...) zu 23,70 Dollar lieber als Pfizer "mit" Lipitor zu 28 Dollar (zumal wenn Lipitor als Umsatzbringer ohnehin noch drei Jahre erhalten bleibt). Mal sehen, wie (und ob) der Ausverkauf in New York heute weiter geht...

Biomedi: Ich kenne mich mit Zertis leider nicht so gut aus. Bei Cotralconsors.de gibt es einen Zerti-Finder. Ich würde eins nehmen, dass einen deutlichen Abschlag zum Kurs hat, weil dann der Derivate-Anteil (Short Call) hoch ist, was bei Seitwärtsbewegung den Gewinn erhöht.

"PFIZER kommt heute morgen unter die Räder. Grund ist die Zurücknahme eines Herz-Kreislaufmittels. Wie üblich gleich minus 8 %. Wer ganz kurzfristig denkt,

geht raus. Wer ein bißchen weiter denkt, hält dagegen die Hand auf. Das können

Sie am Chart gut ablesen. So um 24/25 $ liegt die neue Kaufbasis, denn PFIZER

erhöhte die Gewinnprognose für dieses Jahr auf 2,05 $ je Aktie. Für 2007 gelten

2,14 $, was dann einem KGV von 11,7 entspricht."

Wie meistens, ist Bernie hier für meinen Geschmack zu vorschnell. Ich würde ihn

deshalb eher als Kontraindikator sehen. Im übrigen bin ich köstlich amüsiert:

Bernie und Anti: im Geiste vereint...öhm, sagen wir besser: im Ziel.

Zumindest auf den ersten Blick. Auf den zweiten Blick (das ist der, den Bernie-

Kenner haben) sieht die Sache leicht anders aus: Bernecker sagt NICHTS zum

Kursziel; soweit wie wir hier, lehnt der sich nicht zum Fenster raus. Er spricht

vornehm von KAUFBASIS - und das ist etwas ganz anderes.

Ich glaube allerdings, dass den US-Märkten noch eine größere Korrektur bevorsteht, die auch Pfizer weiter nach unten schicken sollte. Zwischen 20 und 22 USD würde sogar ich bei Pfizer wieder einen Kauf ins Auge fassen. Pfizer bleibt daher für die Zeit nach der überfälligen Index-Korrektur auf meiner "Beobachtungsliste".

Ob Bernecker diese Ansicht teilt oder nicht, kratzt mich nicht weiter. Meist ist er bekanntlich zu früh (ich auch). Wer auf 22 USD und darunter wartet (falls das überhaupt noch kommt), ist in jedem Fall auf der sichereren Seite.

Justin Ferayorni

Pfizer

12/4/2006 9:53 AM EST

The day is still young, but PFE has settled in around $24 - works out to a 4% yield on the current dividend. Maybe that will be the floor in the stock considering the yield environment today, though I wouldn't put new money to work until $20-22. The company indicated accelerated restructuring as a result of this news. I'd expect higher dividends and buybacks to follow, which seems to be the street consensus as well.

Moody's may downgrade Pfizer 'Aaa' long-term debt rating

By Gabriel Madway

Last Update: 11:22 AM ET Dec 4, 2006

SAN FRANCISCO (MarketWatch) -- Moody's Investors Service on Monday placed Pfizer's Aaa long-term debt rating under review for possible downgrade. At the same time, the agency affirmed Pfizer's Prime-1 commercial paper rating. Moody's said the actions follow Pfizer's announcement that it has suspended all clinical development of torcetrapib. The agency said that without torcetrapib, Pfizer's credit profile may no longer be consistent with the Aaa rating. "This major pipeline setback also increases Moody's concerns that Pfizer may pursue larger acquisitions involving incremental debt, or more aggressive shareholder policies," said Moody's senior credit officer Michael Levesque in a statement.

Danke nochmals für Deine Meinung!

![]()

greetz nuessa

Optionen

| Boardmail an "nuessa" |

Wertpapier: Pfizer Inc |

![]()

greetz nuessa

Optionen

| Boardmail an "nuessa" |

Wertpapier: Pfizer Inc |

Angehängte Grafik:

Pfe_1.png (verkleinert auf 49%)

Pfe_1.png (verkleinert auf 49%)

Salt in Pfizer's wound

12/4/2006 10:50 AM EST

Moody's just just said that it's placed Pfizer's (PFE) Aaa long-term debt rating on review for a potential downgrade. Look for similar notices from the other three credit ratings agencies.

As just a handful of companies in the market still receive the highest rating, this could be another psychological negative for the stock.

Yes, Pfizer seems to have bottomed out at a level that's on par with a 4% yield... but note that the yield was as high as 4.7% last December, when the stock was in the low-20's.

And that's when torcetrapib was still a viable part of Pfizer's pipeline. With that in mind, the ultra-conservative part of me wants to stay on the sidelines at current levels.

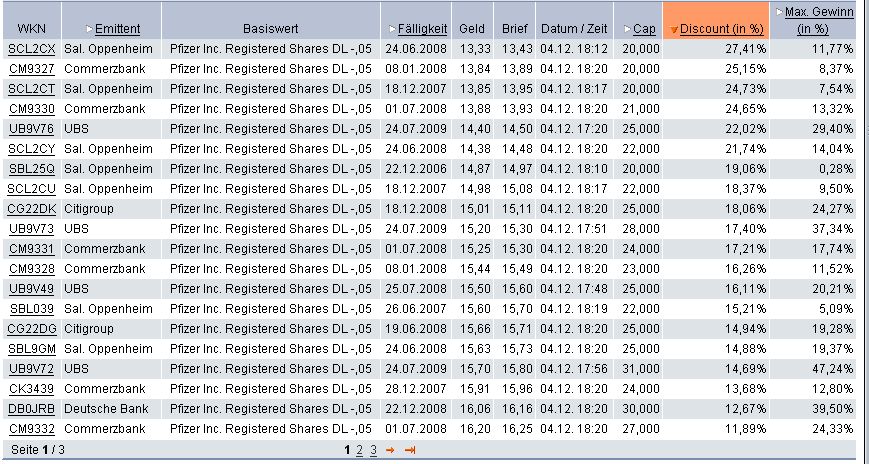

Desh. wollte ich von Dir mal einen Vorschlag, welches Dicount Zertifikat Du empfehlen würdest!

![]()

greetz nuessa

Optionen

| Boardmail an "nuessa" |

Wertpapier: Pfizer Inc |

Angehängte Grafik:

Screen_00077.jpg (verkleinert auf 58%)

Screen_00077.jpg (verkleinert auf 58%)

Ich weiß gar nicht, ob es auf Zertis Dividende gibt (kenn mich mit dem Zeug wie gesagt nicht aus). Falls nicht, würde ich bei 4 % Div. lieber die Aktie kaufen.

![]()

greetz nuessa

Optionen

| Boardmail an "nuessa" |

Wertpapier: Pfizer Inc |

konnte sich -bis Freitag- über gerade mal 4 Dollar Kursgewinn "freuen". Seit

heute haben sich auch die in Luft augelöst. Mit einem stinklangweiligen Dax- Indexpapier stellt man sich besser.

Wer aber Anfang 2005 gekauft hat, hat gar nichts verdient; wer Anfang 2004

gekauft hat, hat rund ein Viertel eingebüßt. Auch weiter nach hinten ergeben

sich negative Bilanzen. - So sieht KEIN attraktives Langzeitinvestement aus!

Nur wer im Dezenber 2005 auf dem absoluten Tief eingestiegen ist, hat noch

einen einigermaßen erträglichen Überschuß. Aber der sieht mit rund 20% eher

mau aus. Nun aber hat sich die Lage deutlich eingetrübt. Mag sein, daß der

Laden noch ein paar Jahre halbwegs brummt - aber 2011 rückt näher. Und

dann?

So sieht jedenfalls keine Zukunftsperspektive aus, die mich zu größeren

Investmentrauschzuständen hinreißen könnte.

PFIZER fiel in erster Linie -AAAAAAA hin oder her- seit Jahren als Rohrkrepie-

rer auf. Frage: warum sollte sich das gerade JETZT grundlegend ändern?

Von einem Discount-Zertifikat rate ich ab; ein Investment für Verunsicherte.

Aktien, von denen ich schwache Performance erwarte, kaufe ich nicht. Weder

als Aktie, noch als Discount-Zertifikat.

Maven: Pfizer's Painful Spin

By Marek Fuchs

Special to TheStreet.com

12/4/2006 12:17 PM EST

URL: http://www.thestreet.com/newsanalysis/maven/10325720.html

If you are anything like the many readers who emailed The Business Press Maven this weekend, you are probably wondering if I'm possessed of some sort of mystical energy field that allows me to see the business future, especially those times when the fatheads of business media can't even see the recent past.

The answer, at least when it comes to Pfizer (PFE), is apparently yes. I have mystical powers.

But my startling clarity aside, let's look at what has happened to Pfizer over the past week and why it shows both how you should avoid the stock until further notice (issues of trust and competence -- see: the lack thereof -- abound) and, more importantly, how you cannot make any investment decision without a firm understanding of what the business media are thinking, doing, writing and saying about your company -- and why.

It is an ancient foundation of Business Press Maven thought and has never been made clearer in such short order: If there is a spread between the published perceptions of the business media and reality, reality will always win out. Though admittedly, not always as quickly as it did in the case of Pfizer.

The Pfizer train wreck left the station on Tuesday, when the company announced that it was laying off 2,000 salespeople, about 20% of its once-vaunted force. Though the kind hearts on Wall Street usually cheer layoffs for the cost savings involved, there was a sense here, well deserved, that a change in era was being signaled. Pfizer, like many of the drug companies, had always ridden its sales force to reliable success.

Typically, adding to a sales force was a harbinger of increased future sales. Now, with flat revenue looking out as far as the eye can see, thanks to disappearing patents with nothing to replace them, Pfizer had probably, Wall Street saw, become that most endangered beast: one that could move forward only if it cut costs well enough.

Could there have been an upside besides cost cuts going on with the employment cuts? Sure. Or maybe. But Pfizer had some 'splainin to do.

Instead of 'splainin, Pfizer started spinning. In fact, it took spin to the level of performance art on Thursday, just two days after the announcement of layoffs, when company management spoke with surefootedness to assembled analysts, reporters and investors at a research facility, touting the greatness of its drug pipeline, using language that would appear comical only two days later.

As The Business Press Maven made clear, this was treading dangerous territory. The drug approval process is always a bit of a crapshoot, especially for a company like Pfizer that had done such soft trade in approvals in the past decade. To speak with such large-scale excitement about future developments, even talking in vaguely vain terms of a "hunger for more," as Pfizer's CEO Jeffery Kindler, now facing a future of less, famously did, was foolhardy.

But the real fools, as I pointed out, were the business media. They essentially wrote about Thursday's meeting with washrags over their eyes, not pressing -- or, in most cases, even touching -- the point that if things were so good on Thursday, why the desperate move on Tuesday? If all these drugs are really coming down the pipeline, uh, won't you need people to sell them?

Forbes swallowed Pfizer's claims hook, like and sinker. It published articles titled "Six Pfizer Drugs to Watch" and "Pfizer Fights Back."

The real answer, of course, came Saturday when Pfizer announced that it was forced to stop development of torcetrapib, its showcase, big-ticket good-cholesterol drug, because it was killing people.

Though I cannot imagine how Pfizer officials did not know by Thursday that torcetrapib was at least causing enough higher blood pressure to temper their excited talk, I'll leave it to others to figure out what they knew and when they knew it.

The larger point is that when there is a spread between the business media's perception of events and reality, it means that there is a clear and present danger for investors.

And investors are the ones left holding the bag. The business media fatheads just ride the other side of the story. What, you ask, is Forbes writing today?

"Behind Pfizer's Failure."

The danger to investors, in this case, came neatly packaged within a week. But when companies try to manage and massage news and the fatheads of the business media do not note underlying truths, such is always the end result.

wichtigen Medikamenten in den kommenden Jahren Patentschutz."

Das hört sich nun wirklich nicht vertrauenerweckend an. - Wer kann angeben,

welche Patente wann auslaufen?