Thompson Creek Metals (Blue Pearl Mng)

Seite 871 von 883 Neuester Beitrag: 24.04.21 22:58 | ||||

| Eröffnet am: | 18.01.07 07:23 | von: CaptainSparr. | Anzahl Beiträge: | 23.072 |

| Neuester Beitrag: | 24.04.21 22:58 | von: Lenaldbqa | Leser gesamt: | 2.692.379 |

| Forum: | Hot-Stocks | Leser heute: | 601 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 869 | 870 | | 872 | 873 | ... 883 > | ||||

kleiner Auszug:

Thompson Creek Reports 2011 Record Molybdenum Sales of 40.1 Million Pounds and Revenue of $669.1 Million

* GAAP net income of $292.1 million, or $1.73 per diluted share

* Non-GAAP adjusted net income of $122.9 million, or $0.73 per diluted share

* Cash flow from operations of $202.7 million

Denver, CO -- Thompson Creek Metals Company Inc. ("Company" or "Thompson Creek"), a growing, diversified North American mining company, today announced financial results for the three months and year ended December 31, 2011, prepared in accordance with United States generally accepted accounting principles ("US GAAP"). All dollar amounts are in United States ("US") dollars unless otherwise indicated.

The Company met its 2011 production and cost guidance, despite lower production and higher costs in the second half of the year, primarily due to the planned mine pit sequencing, increased waste stripping activities, and lower-grade ore and mill recovery at its Thompson Creek mine. Although operating results for the Thompson Creek mine were much lower in the second half of the year, total annual production from the mine was 21.4 million pounds of molybdenum with average cash costs for the year of $6.66 per pound. Production has moved into a new phase of higher-grade ore and the Thompson Creek mine is now on track to achieve previously announced 2012 production guidance of 16 -- 17 million pounds of molybdenum.

Thompson Creek made significant progress in advancing its growth projects throughout 2011. Construction of the Endako mill expansion project was near completion by year end, a staged start-up of the mill began in early January, and commercial production was reached on February 1, 2012. Production will continue to ramp up through the first quarter, with full production anticipated in the second quarter of 2012. The Endako mine is expected to meet previously announced 2012 production guidance of 10 -- 11 million pounds of molybdenum. Construction and development of the Mt. Milligan copper-gold mine remained on schedule in 2011, with commissioning and start-up expected to commence in the third quarter 2013 and commercial production of copper and gold in the fourth quarter of 2013. "Once operational, the Mt. Milligan mine is expected to produce approximately 81 million pounds of copper in concentrate and 194,000 oz of gold in concentrate per year, which we anticipate will contribute significantly to the Company's revenue, net income and cash flow," said Kevin Loughrey, Chairman and Chief Executive Officer.

The Company produced 28.3 million pounds of molybdenum in 2011 and sold 31.8 million pounds of molybdenum from its mines, for an average realized molybdenum sales price per pound for the year of $16.28, up from $15.67 in 2010. While the average realized molybdenum price as reported by Metals Week declined from $15.72 per pound in 2010 to $15.49 per pound in 2011, the Company's average realized molybdenum sales price in 2011 increased 3.9% from its 2010 average.

"We are encouraged by the recent upturn in the molybdenum price over the past several weeks and continue to expect a sustained recovery in molybdenum demand and prices in the medium-term as the world economy recovers," added Mr. Loughrey.

Und die Börse sagt abwärts...

Optionen

| Boardmail an "perlentaucher74" |

Wertpapier: Thompson Creek Metals |

Optionen

| Boardmail an "bull2000" |

Wertpapier: Thompson Creek Metals |

Optionen

| Boardmail an "bull2000" |

Wertpapier: Thompson Creek Metals |

Aber "alle Aktien" rennen nun wirklich nicht davon, der Rohstoffsektor leidet insgesamt unter den erwarteten schwächeren Konjunkturaussichten, insbesondere für China. Gleichwohl, wer an eine weiterhin zunehmende Inflation bei offenen Geldschleusen der Zentralbanken glaubt, der kommt mittelfristig kaum daran vorbei!

Optionen

| Boardmail an "bull2000" |

Wertpapier: Thompson Creek Metals |

Optionen

| Boardmail an "bull2000" |

Wertpapier: Thompson Creek Metals |

noch vor monaten getönt haben, geblieben sind. Im

Nachbarforum wird jetzt auch langsam den tatsachen

ins auge geschaut.wie die zeiten sich doch ändern.

Bin mal gespannt wann der zug zum stehen kommt.

Traurig,traurig wenn man sich den chart anschaut.

Diejenigen,die bei 15 euro und mehr eingestiegen sind,

dürften langsam ein problem bekommen.

Optionen

| Boardmail an "bull2000" |

Wertpapier: Thompson Creek Metals |

Der Dampfer schwimmt doch. Er hat nur gerade etwas Schlagseite. Liegt wohl an den vielen Rumfässern, die alle nach Luv gerollt sind.

Optionen

| Boardmail an "bull2000" |

Wertpapier: Thompson Creek Metals |

Und gib mir auch bescheid, wann "zuletzt" ist!

Optionen

| Boardmail an "bull2000" |

Wertpapier: Thompson Creek Metals |

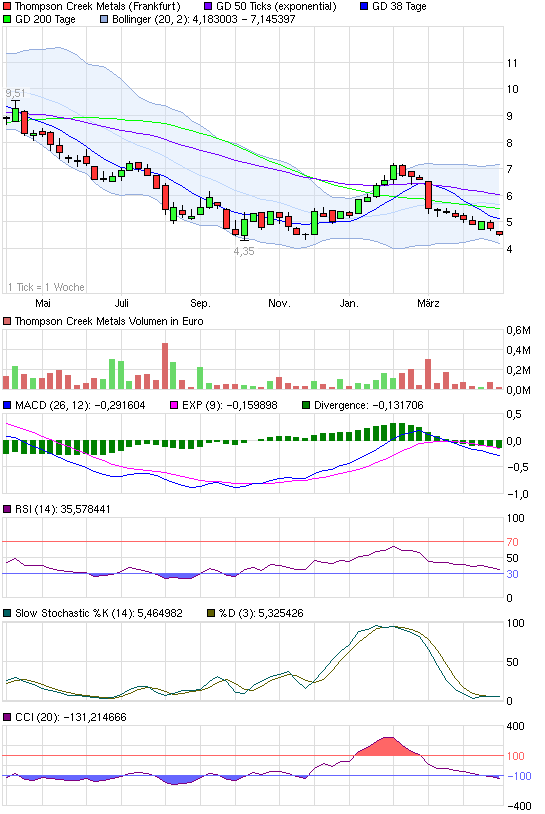

Die einzige Unterstützungslinie, die aktuell angepeilt wird, liegt bei ca. 4,35. Da einzelne Indikatoren noch nicht am Tiefstpunkt angelangt sind, liegt das Antasten dieses Widerstandes im Bereich des Möglichen.

Sollte die Widerstandslinie halten und ein nachhaltiger Turnaround starten, wäre die Empfehlung KAUFEN.

Wird 4,35 signifikant durchbrochen, geht es ans VERKAUFEN weil der nächste massive Widerstand erst bei 2 vorhanden ist und dort wieder eine Kauf-Chance entstehen könnte.

Dieses "Ziel" erscheint momentan aber doch überaus utopisch, da TCM keine Solaranlagen produziert

Optionen

| Boardmail an "proxima" |

Wertpapier: Thompson Creek Metals |

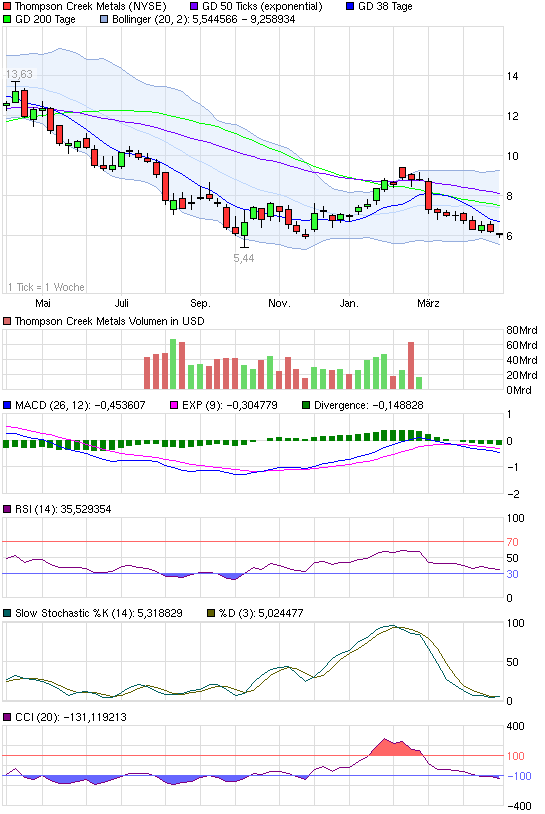

Angehängte Grafik:

chart_year_thompsoncreekmetals.png (verkleinert auf 93%)

chart_year_thompsoncreekmetals.png (verkleinert auf 93%)

Optionen

| Boardmail an "bull2000" |

Wertpapier: Thompson Creek Metals |

Optionen

| Boardmail an "proxima" |

Wertpapier: Thompson Creek Metals |

Angehängte Grafik:

chart_year_thompsoncreekmetals.png (verkleinert auf 93%)

chart_year_thompsoncreekmetals.png (verkleinert auf 93%)