K+S Faktenthread + Technische Analysen + News

"1. kaufsignal wurde heute generiert, bei € 18.85, bestaetigung wird am montag benoetigt"

RICHTIG

1. kaufsignal wurde heute generiert, bei € 21.85, bestaetigung wird am montag benoetigt

[url]http://www.fool.ca/2013/12/27/...n-2014/?source=c75yhocs0040001[/url]

Optionen

| Boardmail an "thairat" |

Wertpapier: K+S AG |

Im neuen Jahr ist viel mehr drin

http://www.sueddeutsche.de/wirtschaft/...ist-viel-mehr-drin-1.1852166

Optionen

| Boardmail an "thairat" |

Wertpapier: K+S AG |

Greenwich

Mitteilung von Netto-Leerverkaufspositionen

Zu folgendem Emittenten wird vom oben genannten Positionsinhaber eine Netto-Leerverkaufsposition gehalten:

K+S Aktiengesellschaft

ISIN: DE000KSAG888

Datum der Position: 27.12.2013

Prozentsatz des ausgegebenen Aktienkapitals: 3,19 %

London

Mitteilung von Netto-Leerverkaufspositionen

Zu folgendem Emittenten wird vom oben genannten Positionsinhaber eine Netto-Leerverkaufsposition gehalten:

K+S Aktiengesellschaft

ISIN: DE000KSAG888

Datum der Position: 27.12.2013

Prozentsatz des ausgegebenen Aktienkapitals: 0,55 %

1. Continental, +82,0 Prozent

2. Deutsche Post: +59,6 Prozent

3. Daimler: +52,2 Prozent

4. Deutsche Telekom: +44,6 Prozent

5. Bayer: +41,8 Prozent

6. Adidas: +37,6 Prozent

7. Henkel: +35,5 Prozent

8. Merck: +30,5 Prozent

9. Deutsche Börse: +30,3 Prozent

10. Fresenius: +28,1 Prozent

11. Infineon: +26,6 Prozent

12. Siemens: +24,7 Prozent

13. Allianz: +24,4 Prozent

14. HeidelbergCement:+20,3 Prozent

15. Beiersdorf: +19,0 Prozent

16. Volkswagen: +18,6 Prozent

17. Münchener Rück: +17,8 Prozent

18. BMW: +16,9 Prozent

19. Linde: +15,2 Prozent

20. Commerzbank +9,2 Prozent

21. BASF: +8,9 Prozent

22. Lufthansa: +8,3 Prozent

23. Deutsche Bank: +5,2 Prozent

24. SAP: +2,7 Prozent

25. ThyssenKrupp: -0,4 Prozent

26. FMC: -1,1 Prozent

27. E.on: -4,8 Prozent

28. RWE:-14,8 Prozent

29. Lanxess: -26,9 Prozent

30. K+S: - 36,1 Prozent

It is only a matter of time before China, the world’s largest potash importer, puts its foot on more resources around the world. Indian companies have been slow off the mark in this regard, but eventually they, too, will move...

- See more at: http://investorintel.com/market-commentary-intel/...ash.0pbOIbLO.dpuf

Optionen

| Boardmail an "thairat" |

Wertpapier: K+S AG |

By Henry Bonner (hbonner@sprottglobal.com)

In the next 40 years, the world’s population is projected to increase by 35%, from 7.1 billion to approximately 9.6 billion people1.

According to Megan Clark, the head of Australia’s national science agency, this means that “in the next 50 years, we will need to produce as much food as has been consumed over our entire human history.”2 This comes as existing eating habits around the world are changing from rice and plant-based foods to meat and high-protein food sources, which demand a greater production of grains to feed livestock.

Jason Stevens, an Investment Executive, joined Sprott Global Resource Investments Ltd. in 2002. He has made agriculture a key aspect of his focus within the resource sector. In this note below, he sheds some light on the picture for agriculture from an investor’s standpoint.

“Agriculture, as an investment sector, is in its infancy. Even though agriculture accounts for 3% of global economic activity3, the public markets are severely under-developed. In addition, the sector has recently been out-of-favor; so many investors are ignoring or overlooking the longer term potential.

More people, less arable land

“As a backdrop to any discussion, consider that the world is trying to feed more people with less arable land per capita. This issue alone will require major innovation in the sector. Other issues will only serve to exacerbate this challenge.

“Global population is growing by 80 million people per year4. This amounts to the population of Germany. With the average person eating a ton of food per year, the U.N. predicts global food production will need to increase 70% by the year 20505.

“Meanwhile, arable land is disappearing because of urbanization, water scarcity and pollution6. Most arable land that is available for development is either marginally productive or very far from infrastructure and requires large capital expenditures to bring online.

“Industry experts currently offer two solutions: advancing biotechnology and applying successes we have had in the developed world to the developing world. But, of course, we have seen global opposition to the use of GMO (Genetically Modified Organisms) technologies and even places already affected by food scarcity, such as certain regions of Africa, have set strict limitations to their use. There are ecological and political concerns with going into the most attractive areas for arable land.

Growing global middle class demands more meat

“The Brookings Institution estimates that the global middle class will grow from 1.8 billion people to 3.2 billion by the end of the decade and 4.9 billion by 2030. Asia will be responsible for most of this growth and will be home to a middle class of approximately 3 billion people within twenty years7.

“As people get richer, they consume more protein-dense food. There are three main reasons why people seek animal proteins when they can afford it: nutrient density, satiety (more appetite satisfaction), and energy (more calories).

“It takes considerably more grain to produce an equivalent amount of animal protein and the demand for meat alone could require 50% more grains and oilseeds. For example, it takes about seven pounds of grain to add one pound of beef to a conventionally-raised cow.8

“Even diet trends in the Western world have moved towards a protein-focused diet. Who has not heard of Paleo, Atkins, or Mediterranean diets?

Water scarcity threatens the food supply

“According to the U.N., close to 45% of the world’s population is currently affected by water scarcity in some way with another 500 million people approaching this situation. Over the last century, water use has grown at more than twice the rate of population growth9.

“Agriculture and water are inseparable. 70% of water used today is for agriculture10. There is nothing on Earth that will replace water in the role it plays to human life and, for the most part, it has no efficient market pricing mechanism.

“Today, water is virtually free to most consumers for political reasons. If we believe ‘free’ is mispriced, and expect that markets are eventually correct, we should expect a future full of localized water scarcity issues. I expect that we will see market-priced water on a broad scale in the next ten years which will add to the cost of producing every commodity, including food.

Biofuels are part of the problem

“Ethanol currently accounts for around 5% of the fuel we put in our cars11 and requires the US to divert nearly 40% of the annual corn crop into its production12. Ethanol production prevents this corn from going to human and animal consumption and drives up the price of a food staple in the process. As interests and production in biofuels increases, demand for all grain products and feedstock commodities increases as well.

“Many countries now have biofuels or ethanol mandates. The US is targeting 30% by 2030, the EU 10% and China 5%13. The push for biofuels has created more competition for arable land and water, diverting resources away from the production of food. The political support for biofuels will contribute to food price inflation and food scarcity in the future.

How do you invest in agriculture?

“Agriculture is not the most investor-friendly sector, but there are a few common ways to participate as an investor. Agricultural investments generally fall into one of three categories: land ownership, production and post-production. Ownership or leasing of farmland is perhaps the most basic type of exposure to the sector. The production category includes management services, and investments in agricultural inputs and equipment. Post-production businesses include grain processors, marketing, and retail branding.

“Our investment process includes looking for the following:

“Unique business models -- Most farmers operate on less than a 4% profit margin, leaving little room for investors to make money. Agricultural businesses we invest in must have innovative ways to produce higher margins.

“High margin assets – potash and phosphate deposits, for instance, can offer attractive returns if they are able to be developed into economic mining operations. Attractive attributes that we look for in potash and phosphate deposits are high grades, low all-in sustaining costs, and good access to infrastructure. Why potash and phosphate? Both provide primary macronutrients in industrial fertilizers.

“Compelling valuations – understanding that good businesses can be poor investments, we attempt to use methods (such as net present value models) to objectively value the business’ future cash flows and factor in an appropriate margin of safety to our entry price.

“Favorable return potential for the inherent risks - we seek to take appropriate risk for the corresponding stage, size, and potential future rates of return of the investment.

“The world is seeking to provide more resource-intensive food to more people with less water in an increasingly difficult environment. We believe this potential crisis offers opportunity for investors to fund solutions.

“Over the last five years, Sprott Global and its affiliates have invested over $125 million in agriculture. Our last investment was a small pre-IPO company that provides alternative financing to farmers in consideration for the right to purchase a share of the crop production at a fixed price for an extended period of time into the future.”

As Jason points out, to meet the growing demand for higher-quality food in both developed and developing countries, new capital will be needed in the sector of agriculture over the coming years. This may represent an opportunity for investors interested in the sector with the ability to afford the risk inherent in these investments.

Investors in agriculture have historically faced risks posed by food prices, weather patterns, and political entities around the world. Indeed, governments have long used the supply and pricing of food and water as a political tool. Jason’s guidelines, however, may provide a starting point for your investment decisions regarding the sector.

Questions? Contact Jason Stevens

Jason Stevens is an Investment Executive at Sprott Global Resource Investments Ltd. and has spent the last 11 years working with mining and petroleum engineers, influential industry executives, investment newsletter writers, and economic geologists. He has extensive experience with private placements, short selling, equity derivatives and option strategies. To contact Jason, e-mail him at jstevens@sprottglobal.com or call 1.800.477.7853.

1 http://www.un.org/apps/news/story.asp?NewsID=45165#.UrCZbtJDuYQ

2 http://abcnews.go.com/Technology/...ars-food-history/story?id=8736358

3 http://data.worldbank.org/indicator/...OTL.ZS/countries?display=graph

4 http://data.worldbank.org/indicator/SP.POP.GROW/...ries?display=graph

5 http://www.un.org/waterforlifedecade/food_security.shtml

6 http://www.upi.com/Science_News/2010/10/21/...ing/UPI-91971287705559/

7 http://www.bbc.co.uk/news/business-22956470

8 http://www.earth-policy.org/data_highlights/2011/highlights22

9 http://www.un.org/waterforlifedecade/scarcity.shtml

10 http://www.unwater.org/statistics_use.html

11 http://www.worldenergyoutlook.org/media/...012/WEO2012_Renewables.pdf

12 http://money.cnn.com/2012/08/06/news/economy/ethanol-drought/

13 http://www.afdc.energy.gov/fuels/ethanol_fuel_basics.html

Optionen

| Boardmail an "thairat" |

Wertpapier: K+S AG |

Optionen

| Boardmail an "Mr.Looong" |

Wertpapier: K+S AG |

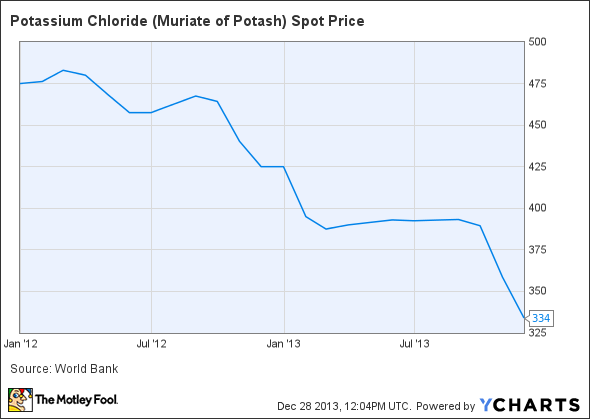

http://ycharts.com/indicators/...hloride_muriate_of_potash_spot_price

Optionen

| Boardmail an "noogman" |

Wertpapier: K+S AG |

Angehängte Grafik:

6440a3191c0231e84cfaf78812fb9c7c.png (verkleinert auf 86%)

6440a3191c0231e84cfaf78812fb9c7c.png (verkleinert auf 86%)

Published time: December 27, 2013 14:19

"After the change of owners - shareholders were replaced by Uralchem [the world's second largest ammonium nitrate producer] and interests of Prokhorov [Russian tycoon-turned-politician] - Uralkali is ready to restore cooperation with Belaruskali," the Russian ambassador to Belarus Alexander Surikov told a news conference on Friday.

The Russian side "acted thoughtlessly and did not calculate all the consequences" from the collapse of the potash cartel, but "both sides were to blame," he said.

"The joint marketing of potash fertilisers should be restored. Most probably this would happen," Surikov said, adding that this would be advantageous for both sides.

http://rt.com/business/russia-belarus-potash-cartel-868/

Optionen

| Boardmail an "thairat" |

Wertpapier: K+S AG |

NY

Mitteilung von Netto-Leerverkaufspositionen

Zu folgendem Emittenten wird vom oben genannten Positionsinhaber eine Netto-Leerverkaufsposition gehalten:

K+S Aktiengesellschaft

ISIN: DE000KSAG888

Datum der Position: 30.12.2013

Prozentsatz des ausgegebenen Aktienkapitals: 0,35 %

-See more at: http://investorintel.com/potash-phosphate-press/...hash.IGMBQhVF.dpuf

Optionen

| Boardmail an "thairat" |

Wertpapier: K+S AG |

Greenwich

Mitteilung von Netto-Leerverkaufspositionen

Zu folgendem Emittenten wird vom oben genannten Positionsinhaber eine Netto-Leerverkaufsposition gehalten:

K+S Aktiengesellschaft

ISIN: DE000KSAG888

Datum der Position: 02.01.2014

Prozentsatz des ausgegebenen Aktienkapitals: 2,58 %

ebenfalls wird empfohlen, den kurs auf tagesbasis zu beobachten.

Market Outlook

The market is uncertain with a negative tilt. The traders seem to be in disagreement. The negative sentiment, however, is increasing as evident from the last bearish pattern. So, it is better to be on alert. The share price is still not below the confirmation level and the signal is suggesting to STAY LONG, but the chance of a bearish confirmation that will change the signal to SELL is quite high. The Delayed Intraday Module is ON. We strongly suggest you to follow the price action on an intraday basis, given the downside risks involved.

WC2N 6HT

Mitteilung von Netto-Leerverkaufspositionen

Zu folgendem Emittenten wird vom oben genannten Positionsinhaber eine Netto-Leerverkaufsposition gehalten:

K+S Aktiengesellschaft

ISIN: DE0007500001

Datum der Position: 03.01.2014

Prozentsatz des ausgegebenen Aktienkapitals: 0,98 %