Die besten Gold-/Silberminen auf der Welt

Echt schade da ich denke das Du soweit in Ordnung bist. Deine Ukraibeaktion hat mir auch sehr gut gefallen.

Wenn Du zurück ließt ist es leider genauso mit den ganzen Explorern gekommen wie gich geschrieben habe als die Explorer noch viel hiervon Kurs standen. Warum verkaufst Du soviel zu low Kursen jetzt?

Alles gute für Dich und uns.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Er hat die meisten Calls hier mit CEOs und bildet sich wie viele hier viel fort.

Trotzdem darf ich auch mal eine abweichende Meinung vertreten.

Daniel ist aber ein top Typ und manchmal auch tapfer mit mir ;)

Seine Meinung hat bei mir Gewicht

Optionen

| Boardmail an "Jacky Cola" |

Wertpapier: Gold |

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Gold |

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Habe zu 0.12-0.20 cad gekauft und bin im Schnitt zu 0.21 cad raus

Brauchte mal bisschen Cash für Uran und Lebensqualität (Urlaube)

Alles andere habe ich nicht verkauft und sitze gerade bei OPW auf mega Verlusten bei mittlerweile 1 mio Aktien im Bestand zum Durchschnittskurs von ca 0.25 cad. Habe ja sogar zu 8 Cent nochmal nachgelegt

Ob OPW sich nochmal erholen wird bevor ein roll back kommt ? Ich würde es mir wünschen

Optionen

| Boardmail an "Jacky Cola" |

Wertpapier: Gold |

Hört sich doch sehr vielversprechend an. Wird halt alles noch Zeit benötigen. Grundsätzlich wird hier jedoch gute Explorationsarbeit geleistet.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Optionen

| Boardmail an "Katzenpirat" |

Wertpapier: Gold |

Angehängte Grafik:

screenshot_2022-07-28_at_14-55-....png (verkleinert auf 53%)

screenshot_2022-07-28_at_14-55-....png (verkleinert auf 53%)

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Gold |

Aktueller Silberchart - erleben wir gerade eine Bodenbildung?

Optionen

| Boardmail an "Katzenpirat" |

Wertpapier: Gold |

Angehängte Grafik:

screenshot_2022-07-28_at_15-12-....png (verkleinert auf 88%)

screenshot_2022-07-28_at_15-12-....png (verkleinert auf 88%)

Jul. 28, 2022 6:02 AM ETAgnico Eagle Mines Limited (AEM)18 Comments15 Likes

Taylor Dart profile picture

Taylor Dart

24.98K Followers

Following

Summary

Agnico Eagle released its Q2 results this week, reporting quarterly production of ~858,200 ounces, a 71% increase from the year-ago period, driven by the recently closed merger with KL Gold.

While this production growth was to be expected, costs came in below my estimates at $1,026/oz, evidence of Agnico's superior business model that shines even in an inflationary environment.

Given this solid performance, AEM remains on track to meet or beat its FY2022 guidance, and costs will remain within guidance at industry-leading levels.

At a current valuation of less than ~7x cash flow, Agnico has rarely ever been this attractively valued, and I would be shocked if this valuation disconnect persisted, making this an attractive buying opportunity below $42.00 per share.

Fosterville Gold Mine

tracielouise

The Q2 Earnings Season kicked off with a whimper, with Newmont (NEM) raising its cost guidance and increasing upfront capex estimates at two major projects. Fortunately, for the sector, Agnico Eagle (NYSE:AEM) has swooped in with a large beat, reporting record production, industry-leading margins and strong cost controls, and strong mid-year reserve growth from its Detour Lake Mine. This has placed the company well on track to meet guidance, and the continued exploration success combined with a strong pipeline point to a very bright future. So, with the stock trading at one of its cheapest valuations in years, I see the stock as a Strong Buy below $42.00 per share.

Detour Lake Mine

Detour Lake Mine (Company Presentation)

Just over two months ago, I wrote on Agnico Eagle, noting that the stock was very attractively priced and that the pullback in the stock near its 52-week lows at $50.00 was a gift. In hindsight, this view that the stock was a Buy was brutally early and a terrible call. And in my opinion, whether "right" on the fundamentals or not, being brutally early is just as bad as being wrong. That said, my conviction regarding my thesis that this is the best producer to own in the current environment is even higher today than it was in June, reinforced by the company's exceptional results despite a challenging first half for much of its peer group. Let's take a closer look below:

Agnico Eagle Operations

Agnico Eagle Operations (Company Video)

Q2 Production

Beginning with production, Agnico had a record quarter on a consolidated basis, helped by adding three world-class operations to its portfolio from its recently closed merger. These three assets combined for more than 340,000 ounces in Q2, pushing Agnico's consolidated production to ~858,200 ounces (~1.52 million ounces year-to-date). However, even on an organic basis (ex-Kirkland contribution), Agnico's legacy mines performed just as impressively given the continued headwinds (labor tightness, supply chain headwinds). This was evidenced by a record quarter from Amaruq for production (Meadowbank: ~96,700 ounces), a quarterly record for mill throughput at Kittila, and strong production (~87,200 ounces) & exciting exploration results from Malartic.

Agnico Eagle - Quarterly Gold Production

Agnico Eagle - Quarterly Gold Production (Company Filings, Author's Chart)

After subtracting out the ~342,000 ounces contributed from Kirkland Lake's operations (now under Agnico Eagle following the merger), Agnico's production was up approximately 3% to ~516,000 ounces. This was helped by higher production at Goldex (improved productivity and grades), Meadowbank (higher throughput and grades), Meliadine (higher throughput), and Kittila (record throughput of 556,000 tonnes). When combined with higher grades, the Finnish asset enjoyed a record quarter with production of ~64,800 ounces, beating its prior record of ~63,200 ounces achieved in Q3 2021. Finally, La India was up against easy year-over-year comps due to low local water availability in Q2 2021, providing a further boost to quarterly production.

Agnico Eagle - Quarterly Production by Mine

Agnico Eagle - Quarterly Production by Mine (Company Filings, Author's Chart)

Moving over to the new mines in the portfolio, Macassa rebounded strongly in Q2 to produce ~61,200 ounces at cash costs of $582/oz, helped by strong grades of 22.02 grams per tonne of gold. This asset continues to have a very bright future, with the mine now benefiting from improved ventilation (connection of #4 Shaft) with the commissioning of Shaft #4 expected by year-end. The completion of this project will increase hoisting capacity to 4,000 tonnes per day and contribute to much lower unit costs.

However, this asset's future is even more exciting given the addition of Amalgamated Kirkland (AK - a previously orphaned deposit), which could contribute 40,000 ounces per annum beginning in 2024 to the production profile with the underground ramp from Macassa extended by 615 meters. Assuming this is the case, this should be able to support a 375,000+ ounce production profile at sub $500/oz cash costs post-2024, nearly 80% above the FY 021 production rate (~210,200 ounces). To date, drill highlights at AK have been encouraging, evidenced by the following intercepts from shallow drilling that can't be reached from the under round ramp:

6.7 meters of 6.9 grams per tonne gold (138-meter depth)

6.0 meters at 5.9 grams per tonne gold (147-meter depth)

9.2 meters at 9.0 grams per tonne gold (171-meter depth)

7.7 meters at 6.0 grams per tonne gold (125-meter depth)

Moving over to Detour Lake, Agnico had a solid quarter, reporting quarterly production of ~195,500 ounces, with ~6.52 million tonnes processed at an average grade of 1.01 grams per tonne gold. However, in addition to the strong operating results, there were several other pieces of exciting news. These were as follows:

mentions of 1.0 million-ounce per annum production potential long-term

a 38% increase in mineral reserves to 20.4 million ounces

continued exploration success outside of current reserves and resources

Detour Lake - Operating Metrics

Detour Lake - Operating Metrics (Company Filings, Author's Chart)

In terms of the 1.0 million-ounce per annum production potential, Detour is currently operating at ~27 million tonnes per annum but is permitted to operate at 32.8 million tonnes. At this higher throughput rate, which is being explored, and with the addition of higher-grade underground material, this could be a 1.0 million-ounce per annum producer at a feed grade of 1.05 grams per tonne of gold and a ~92% recovery rate. This is a later-in-the-decade opportunity, but this would translate to more than 30% production growth from current levels and make Detour a top-10 producer globally and a top-3 in Tier-1 jurisdictions (ahead of Cadia, Boddington, and Canadian Malartic, and just behind the Carlin Complex).

Top Mines by Production

Top Mines by Production (Visual Capitalist)

From a reserve standpoint, reserves now stand at 20.4 million ounces of gold, and the mine life has been extended to 2052, with 1.8 million ounces added between 2032-2042 and 3.0 million ounces added between 2043-2052. However, there are 16 million ounces of gold outside of reserves. This suggests the opportunity to increase the mine life even further and also fill in gaps within the mine life to boost the production profile from the current average of ~730,000 ounces (2023 through 2031). There's also the potential to boost the 2032-2042 production profile.

The assumed mill throughput across the mine life is based on only processing 28 million tonnes per annum (15% below permitted capacity), suggesting meaningful upside to this production profile. In addition, this mine plan does not include looking at the underground potential where there are much higher grades to augment feed grades, nor does it look at exploration upside on the property, which continues to beat expectations. In fact, regional exploration drilling in the West Pit Extension hit 32.3 grams per tonne over 4.8 meters at 955 meters depth, 2.7 meters at 3.2 grams per tonne gold at 592 meters depth, and 5.6 meters at 6.0 grams per tonne gold at 940 meters depth.

Detour Lake Exploration Map

Detour Lake Exploration Map (Company Presentation)

While not nearly as thick as traditional intercepts from the Main Pit, Saddle Zone, and West Pit, these are a big deal. This is because they suggest a further regional potential west of what's already one of the world's largest gold mines. It's still early days, and a few solid high-grade holes do not confirm a new major deposit, but this is certainly very encouraging. Meanwhile, closer to current resources in the West Pit zone to the west of the resource pit, Agnico intercepted 15.4 meters of 4.4 grams per tonne gold, 2.7 meters of 3.8 grams per tonne gold, and 3.6 meters of 24.1 grams per tonne gold. Overall, this looks to be a deposit that will keep on giving for decades to come, and the fact that Agnico is thinking big with "1.0 million-ounce per annum potential" is certainly encouraging, given that this will further improve already attractive unit costs (sub $900/oz all-in sustaining costs).

Fosterville Quarterly Production

Fosterville Quarterly Production (Company Filings, Author's Chart)

Finally, Fosterville had a decent quarter, producing ~86,100 ounces, though lower than previous quarters due to a decline in throughput (~122,000 tonnes vs. ~170,000 tonnes). This appears to be related to low-frequency noise constraints that may have impacted mining rates, leading to lower throughput in the period (Agnico cited primary ventilation operating restrictions). This is not a new issue (noise complaints), and Agnico is evaluating the potential installation of the primary fans underground longer-term. The good news is that grades were solid (~22 grams per tonne of gold), and it should be an exciting year of exploration ahead as the Robbins Hill and Lower Phoenix exploration declines were completed.

Before moving on, it's worth discussing the continued exploration success at Agnico's 50% owned Canadian Malartic [CM] Mine. During the quarter, the CM partnership reported incredible infill holes from East Gouldie, which included the following:

22.53 meters at 6.45 grams per tonne gold

33.24 meters at 5.03 grams per tonne gold

60.26 meters at 2.23 grams per tonne gold

27.50 meters at 6.93 grams per tonne gold

It also reported impressive results on the East Gouldie Extension, which could prompt the sinking of a second shaft later this decade, given the significant growth in resources and excess capacity at the CM mill. These were as follows:

5.98 meters at 3.85 grams per tonne gold

62.92 meters at 1.84 grams per tonne gold

7.9 meters at 4.11 grams per tonne gold

Finally, Odyssey South, which is a lower-grade deposit relative to East Gouldie, turned up phenomenal conversion drilling intercepts that included 7.4 meters at 19.11 grams per tonne gold, 6.62 meters at 28.66 grams per tonne gold, and 8.64 meters at 17.64 grams per tonne gold. Overall, the drilling success at CM continues to be very encouraging, suggesting a 20+ million-ounce resource potential at this mine on a 100% basis, which should support exploring a larger production scenario to pull ounces forward and leverage the existing infrastructure. While a second shaft isn't cheap, this project is shared on a 50/50 basis, with any potential capex focused on increasing underground mining rates shouldered by both parties.

Canadian Malartic Exploration

Canadian Malartic Exploration (Yamana Presentation)

Margins & Financial Results

Moving to the financial results, Agnico reported revenue of ~$1,581 million, translating to a 61% increase from the year-ago period. This was related to higher sales volumes (increased production) at higher gold prices, with an average realized price of $1,866/oz (Q2 2021: $1,814/oz). The sharp increase in revenue combined with similar operating costs year-over-year translated to a quarterly operating cash flow of ~$633.3 million, up from $419.4 million in the year-ago period. After subtracting ~$401.6 million in capex (capex + capitalized exploration expenditures), this translated to quarterly free cash flow of ~$231 million or ~$0.50 per share.

Agnico Eagle - Quarerly Revenue

Agnico Eagle - Quarterly Revenue (Company Filings, Author's Chart)

Looking at operating costs, Agnico had a strong quarter, reporting all-in sustaining costs of $1,026/oz, more than 15% below my updated industry average estimate of $1,230/oz for FY2022. This figure was down from $1,037/oz last year, with an additional benefit of up to $40/oz from planned synergies in coming years. This suggests that Agnico has a path towards getting costs back below $1,000/oz despite inflationary pressures, which is very impressive given the margin compression and rising costs we're seeing sector-wide. Given the higher gold price, Agnico's AISC margins increased to $840/oz from $777/oz, an 8% improvement from the year-ago period.

Agnico Eagle AISC

Agnico Eagle AISC (Company Filings, Author's Chart)

In addition to benefiting from the foresight to hedge a considerable amount of diesel exposure (43% hedged for the remainder of the year), Agnico benefits from being in a prolific region in Australia from a gold endowment standpoint (Victoria) but away from the labor tightness in Western Australia. This hurt Newmont in its Q2 results, with Western Australia having over 100 mines/projects, multiple commodities being exploited (iron ore, nickel, copper, gold), and 150,000 employees. This leads to companies fighting to secure workers and contracted services. In Agnico's case, it's the employer of choice in Victoria, with its only real competing mine being Costerfield from a labor standpoint.

Meanwhile, it certainly helps that Agnico operates several high-grade underground mines, which means higher production per tonne of material moved. Meanwhile, its high-volume mines benefit from economies of scale. Lastly, the company benefits from the availability of hydroelectricity (low emission public grid) in Ontario and Quebec at its mines, with these costs not spiking suddenly related to higher oil/gas prices, which has impacted more remote mines working off of diesel generators.

Long-term, the company should benefit from the Kivalliq Hydro-Fiber Link Project, endorsed in Canada's 2021 Federal budget. It could also benefit from the possibility of trolley assist for its haul trucks at Detour Lake long-term, and this could see some help from the government in funding this project. For those unfamiliar, trolley assist is a system for diesel-electric haul trucks at mines, pulling them along a trolley line with electric power, which translates to lower costs and emissions (bypassing the diesel engine entirely). This technology is already used at Cobre Panama, which is operated by First Quantum, a massive copper-gold mine.

An Industry Leader Across All Metrics

This differentiator of operating higher than average grade operations that benefit from economies of scale certainly helps when it comes to maintaining industry-leading margins. Meanwhile, Agnico's ~95% Tier-1 jurisdictional profile allows investors to sleep well at night without the negative surprises that some companies face in less attractive jurisdictions. However, safe jurisdictions or not, I'd be remiss not to note that the company's strict adherence to social responsibility and environmental standards is industry-leading, further elevating the investment thesis from an ESG standpoint.

Agnico Eagle - Jurisdictional Profile

Agnico Eagle - Jurisdictional Profile (Company Presentation)

For example, the company hires over 90% of its workforce locally (and 100% Mexican for its Mexico Operations) in addition to community programs and considerable local procurement spending (2021: $1.6 billion), enriching the communities where it operates. This attention to the communities where it operates is not only in the form of higher wages than would be otherwise available (assuming sourcing of ex-pats instead) and direct investments but by taking a superior approach in cases like its Pinos Altos Mine in Mexico. In fact, Agnico should be praised for listening to what the community needs and helping them achieve those goals in a non-paternalistic manner.

One example is the case of a school in Pinos Altos that needed to be expanded. Instead of building it for them, Agnico went a step further, providing materials, supervision, and training so that they could build it together with the people in the town building the new school rooms. This is an important distinction not only from a pride standpoint but also from a long-term standpoint, given that the town's people are now equipped with the expertise to continue to build their local economy and take on new projects. Carol Plummer pointed this out in the company's recent Sustainability Presentation, Agnico's EVP of Operational Excellence.

Nunavut Operations

Nunavut Operations (Company Presentation)

Meanwhile, in Nunavut, Agnico took care of its Nunavummiut workforce during the past two years by keeping them home with pay when necessary. From a safety standpoint, this was the right thing to do, recognizing the more fragile situation in Nunavut from a healthcare standpoint relative to more developed Canadian provinces. In my view, these steps to build lasting relationships with its communities increase the likelihood of Agnico operating in these communities for decades to come.

While taking care of the environment and social responsibility would appear to be the highest priority initiatives, this isn't always the case. This is a major advantage vs. operators less focused on these initiatives. One example is Goldcorp, with a profit-only focus at its Marlin Mine (Guatemala), which led to its shutdown and left behind extensive infrastructure while also giving the industry a bad rap. Of course, the major indirect benefit to being in jurisdictions for decades is less labor price volatility, with a higher ratio of employees to contractors. The result is much lower labor costs than the double-digit year-over-year price increases we're seeing in some cases for contracted services and specialized labor in prolific mining jurisdictions (Ontario, Western Australia).

GHG Emissions (Scope 1 & 2) vs. Peers

GHG Emissions (Scope 1 & 2) vs. Peers (Company Presentation)

From an environmental standpoint, Agnico continues to be a leader from a greenhouse gas intensity standpoint, and its investments in this category will allow it to maintain a leading position. Examples to help reduce emissions include automatic ore handling systems (RailVeyor at Goldex) and battery electric vehicles at Macassa. Notably, battery electric vehicles are being tested at LaRonde, Kittila, and Fosterville, potentially reducing emissions even further. In a period of rising energy costs, this renewable energy focus and ability to tap into hydroelectricity at some of its mines is a key advantage from a cost standpoint as well, with Agnico further insulated by its diesel hedging program.

Now that we've covered the necessary bases (the phenomenal operating/financial results, organic growth opportunities at existing assets), let's look at the valuation.

Valuation

Based on ~455 million shares outstanding and a share price of $39.50, Agnico trades at a market cap of ~$18.0 billion, a ridiculous valuation for a company with ~50 million ounces of mineral reserves (now valued at less than $370/oz). When we add in an additional ~40 million ounces of M&I resources, Agnico's resource/reserve combo (excluding inferred ounces) is being valued at just ~$200/oz. This metric might make sense if the company's all-in sustaining costs were above $1,400/oz. However, with all-in sustaining costs likely to come in below $1,000/oz in FY2023, this is the cheapest I recall seeing Agnico from a valuation per ounce standpoint in years.

Agnico Eagle Mines - Historical Cash Flow Multiple

Agnico Eagle Mines - Historical Cash Flow Multiple (FASTGraphs.com)

Meanwhile, from a cash flow standpoint, Agnico now trades at just ~7.3x FY2022 cash flow per share estimates based on a more conservative estimate of $5.40. This is a massive discount to its historical cash flow multiple of ~26.0 and its 20-year average cash flow multiple of 19.0. Even if we used a 50% discount to its historical multiple and a 30% discount to its 20-year average (13x cash flow vs. 19x cash flow), Agnico's fair value would come in at $70.20 - nearly 80% upside from current levels. Importantly, this assumes no upside in the gold price and represents conservative estimates. Given the ~$480 million available for buybacks which could eliminate over 2% of the float, I would argue that FY2023 estimates of $5.30 in cash flow per share could be conservative.

Summary

Companies rarely check all the boxes for investment, with there often being at least one glaring weak spot. However, Agnico Eagle is an exception to the rule, and its discipline and attention to detail allowed it to shine in the current environment. These key attributes are an ultra-low cost profile, safe jurisdictions, strong sustainability metrics, and a near unrivaled organic growth profile among its peer group. Most importantly, though, is its ability to consistently over-deliver on its promises, being laser-focused on per share growth, not solely absolute metrics. This is a crucial metric for investors in the sector to watch because if a company is not growing or maintaining production per share, it's often better just to hold the metal itself.

Agnico Eagle and Kirkland Lake - Gold Production Per Share

Gold Production Per Share (Company Presentation)

The issue with Agnico from an investment standpoint was that outside of March 2020 and September 2018, the stock commanded a massive (though deserved) premium for its near flawless track record relative to its peers. That attribute made it difficult to invest in the stock with a significant margin of safety and be comfortable building a large position. However, this violent correction has left it trading at a valuation reserved for an industry laggard, which makes zero sense. This is because, across nearly every metric, the company is an industry leader. So, with AEM being a rare case of growth and value, I see it as a must-own name for those looking to add precious metals exposure, so I've continued to accumulate an overweight position in the stock.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

GCM Mining: Toroparu Project, A Good Bet For The Company's Future

Jun. 28, 2022 10:11 PM ETGCM Mining Corp. (TPRFF), GCM:CA49 Comments9 Likes

Fun Trading profile picture

Fun Trading

Marketplace

Follow

Summary

The company announced first-quarter revenues of $101.32 million, down slightly from the same quarter a year ago and up 8.2% sequentially.

GCM’s gold production from its Segovia Operations was 49,951 ounces in 1Q22, up 2% over the first quarter of last year.

I recommend buying TPRFF at or below $2.75 with potential lower support at $2.55.

Gold nugget on black background.

scyther5/iStock via Getty Images

Investment Thesis

1 - Presentation

The Canada-based GCM Mining (OTCQX:TPRFF) owns Segovia operations in Colombia, the company's principal producing asset. GCM Mining is also involved in Guyana with the Toroparu Project.

Important note: This article is an update of my article published on April 13, 2022. I have been following TPRFF on Seeking Alpha since 2021.

Recent news: On June 27, 2022, posted encouraging drilling program results at Sandra K and El Silencio at its Segovia operations in Colombia.

Announced today multiple high-grade intercepts from the latest 32 diamond drill holes, totaling 8,299 meters, from the 2022 in-mine and near-mine drilling programs, as well as a further 28 diamond drill holes, totaling 7,735 meters, from the 2022 brownfield drilling programs at its Segovia Operations, Colombia.

Approximately 32% of the brownfield exploration drilling programs for this year were completed by the end of April

GCM Mining could be considered a long-term potential in the gold segment. Strong balance sheet and an exciting project in Guyana on the way called Toroparu with secured financing from Wheaton.

2 - 1Q21 results snapshot and commentary

The company reported its first-quarter 2022 results on May 12, 2022.

Table

TPRFF 1Q22 highlights (GCM Mining)

Lombardo Paredes, Chief Executive Officer of GCM Mining, commenting on the first-quarter 2022 results:

We have started o 2022 on a positive note, meeting our expectations for production, costs, and cash ow in the first quarter. We are on track to once again meet our annual production guidance for 2022.

GCM's gold production from its Segovia Operations was 49,951 ounces in 1Q22, up 2% over the first quarter of last year.

The company indicated a gold production of 18,321 ounces for April, bringing Segovia's trailing 12 months' total gold production to 208,130 ounces, up 1% over 2021.

Expansion of the Company's processing plant at Segovia to 2,000 TPD is proceeding well and is expected to be completed by mid-2022. Moreover, the Company is on track to meet its annual production guidance for 2022 of between 210K and 225K ounces of gold.

Finally, the new polymetallic recovery plant constructed in 2021 at Segovia produced approximately 252K lbs of payable zinc and 338K lbs of payable lead in the first quarter of 2022.

3 - The Toroparu Project - One of the most significant Gold/Copper projects in the Americas

It is an exciting project that will make a big difference for the company when completed. Shareholders will have to use weakness to accumulate and be patient.

Table

TPRFF Toroparu Project1Q22 (GCM Mining)

Gran Colombia has already started pre-construction activities on the camp, airstrip, and an access road, carrying out additional infill drilling.

The bid process for the mine, power plant, and main civil works contractors has started.

4 - Stock Performance

TPRFF has underperformed the VanEck Vectors Gold Miners ETF (GDX) and is down 31% on a one-year basis.

Chart

Data by YCharts

GCM Mining - Financial Snapshot 1Q22 - The Raw Numbers

Gran Colombia 1Q21 2Q21 3Q21 4Q21 1Q22

Total Revenues In $ Million 99.67 96.35 90.72 93.62 101.32

Net Income in $ Million 124.56 29.80 25.26 6.61 5.24

EBITDA $ Million 143.45 53.69 50.90 32.14 35.18

EPS diluted in $/share 1.28 0.28 0.20 0.07 0.05

Operating Cash flow in $ Million 13.62 12.79 26.74 27.41 24.21

Capital Expenditure in $ Million 11.12 15.77 14.61 21.97 20.26

Free Cash Flow in $ Million 2.50 -2.98 12.13 5.44 3.95

Total Cash $ Million 73.71 57.80 331.31 328.04 315.06

Total Long term Debt (incl. current) In $ Million 57.00 40.86 307.67 314.27 311.31

Shares outstanding -(diluted) in Million 61.67 83.90

109.35

94.89

99.96 (with fully diluted at 109.89 million)

The dividend is paid per month now/ Quarterly dividend in $/share.

0.034

0.034

0.034

0.034

0.034§

Click to enlarge

Data Source: Company release. (More data available for subscribers only).

Analysis: Revenues, Earnings Details, Free Cash Flow, Debt, And Gold Production

1 - Total Revenues and others were $101.32 million in 1Q22

chart

TPRFF Quarterly revenues history (Fun Trading)

Note: Gold sale represents $99.783 million and $1.539 million for silver.

The company announced first-quarter revenues of $101.32 million, down slightly from the same quarter a year ago and up 8.2% sequentially. The company posted a net income of $5.24 million compared to $124.56 million last year.

The spot gold price in the first quarter of 2022 was higher than the same quarter a year ago to an average of $1,860 per ounce sold in the first quarter of 2022 compared with an average of $1,812 per ounce sold in 1Q21.

The first-quarter adjusted EBITDA was $45.218 million compared to $46.323 million in 1Q21.

2 - Free cash flow was a loss of $3.95 million in 1Q22

Chart

TPRFF Quarterly Free Cash Flow history (Fun Trading)

Note: Generic free cash flow is cash flow from operations minus CapEx. GCM Mining uses another calculation that indicated $10.7 million in free cash flow in 1Q22. GCM Mining is adding the CapEx for Toroparu.

The trailing 12-month free cash flow is now $18.54 million, with free cash flow in 1Q22 of $3.95 million.

As of March 31, 2022, the company's investments in associates totaled $159.86 million, primarily representing Aris (OTCQX:ALLXF).

GCM Mining repurchased approximately 0.3 million shares for $1.1 million in 1Q22. Also, in April 2022, the Company purchased and canceled 100,000 common shares.

GCM Mining may purchase up to 9,570,540 common shares over 12 months ending October 19, 2022. As of May 12, 2022, the Company has purchased 957,402 common shares.

3 - Gran Colombia was net debt-free at the end of the 1Q22

Chart

TPRFF Quarterly Cash versus Debt history (Fun Trading)

At the end of March 2022, GCM Mining had a cash position of approximately $319.75 million (including bullion), and the total debt was $311.31 million, including current.

Chart

TPRFF Quarterly Debt profile Presentation (GCM Mining)

The Company's balance sheet is solid and enjoys $138.0 million of funding available for constructing its Toroparu Project in Guyana through a precious metals stream facility with Wheaton Precious Metals (WPM).

Also, on April 12, 2022, the Company acquired a $35 million convertible senior unsecured debenture issued by a wholly-owned subsidiary of Aris at 7.5%.

The Aris Debenture will be due, in cash, 18 months from closing of the Soto Norte Acquisition. At any time after 12 months from closing of the Soto Norte Acquisition, the Aris Debenture may be converted, in whole or in part, at the Company's sole discretion into common shares of Aris at a conversion price of $1.75 per share.

4 - Production was 49,951 Au Oz and 89,782 Ag Oz in 1Q22

Note: Including production from the Marmato Project up to February 4, 2021, the date of loss of control of Aris.

4.1 - Gold and Silver production: Historical chart

Chart

TPRFF Quarterly gold and silver production history (Fun Trading)

Note: Gold sold in 1Q22 was 53,645 Au Oz and silver 67,611 Ag Oz.

Production comes from Segovia operations mainly. Segovia operations include:

Sandra K mine - 7,346 Oz

Providencia mine - 14,867 Oz

El Silencio mine - 18,862 Oz

Carla is a potential with a probable reserve of 33K Au Oz - 1,253 Oz

Polymetallic Zinc and Lead - 87 GEOs (86 days only).

With Maria Dama Processing Plant, "El ChoCho" Tailings Storage and Polymetallic plant update for 1Q22.

Table

TPRFF Segovia Details (GCM Mining Presentation)

In April 2022, the Company processed 50,802 tonnes, equivalent to 1,693 TPD, at an average head grade of 12.4 g/t resulting in gold production of 18,321 ounces.

One issue is the head grade which has been dropping since 2020 from a high of 16.86 G/T 2020 to 12.4 G/T.

4.2 - Quarterly AISC (consolidated) and the gold price received: Chart history

Chart

TPRFF Quarterly gold price and AISC history (Fun Trading)

The AISC decreased sequentially to $1,187 per ounce but was still uncomfortably high. It is up 6% from 1Q21.

4.3 - Reserves

Chart

TPRFF Reserves Presentation (GCM Mining)

The company's ongoing exploration is extending significantly Segovia's mine LOM. Total M&I jumped 14% from 2020 to 1.6Moz.

4.4 - Great Pipeline projects (unchanged)

Zancudo Project - Colombia 100%

Juby Project - Ontario, Canada, with Aris Gold

Toroparu Project - Guyana to be 100%

Meadowbank - Nunavut 26%

Technical analysis (short term) and commentary

Chart

TPRFF TA Chart short-term (Fun Trading)

TPRFF forms a descending wedge pattern, or a falling wedge, with resistance at $3.10 and support at $2.75. The trading strategy is to sell about 30% between $3.10 and $3.61 and accumulate between $2.80 and $2.70.

For those who have decided to keep a long-term position, I strongly recommend trading LIFO while holding a core long-term position for a potential test of $5s or higher.

In a bearish case, TPRFF could cross the support and drop at or below $2.55.

Conversely, if the gold price turns bullish and can trade above $1,880 and $1,920 per ounce, I see TPRFF trading between $5 and $5.50.

Thus, watch the gold price like a hawk.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

{kind=link}

Sentiment Optix für Gold vom 25. Juli 2022. Quelle: Sentimenttrader

Die neuesten Sentiment-Daten für den Goldpreis fördern erstmals seit dem Herbst 2018 wieder ein extrem pessimistisches Stimmungsbild zu Tage! Fast vier Jahre lang mussten geduldige Goldbugs auf dieses antizyklisch vielversprechende Setup warten!

Das klingt doch gut. Es besteht realistisch die Chance das wir das Tief erstmal gesehen haben und es nun vom low Punkt 1680 US Dollar längere Zeit aufwärts geht und neue Hochs generiert werden können. Florian

Grummes mit einer ausführlichen Analyse zu Gold

Hier ist etwas, das Sie vielleicht interessieren könnte: - http://de.investing.com/analysis/...mmerrally-kann-beginnen-200475245

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Zu CREST, abschliessend von mir, die Bude gefällt mir ebenfalls gar nicht. Auch der Grund warum ich Volatus super vorsichtig betrachten werde. Das Konzept ist den Preis drücken, sich selber günstige Financings zuschieben, nur sich selbst und damit Kontrolle gewinnen. Die Altaktionäre werden in der Holding verwässert. Solange bis das Ding gepusht wird. Werde ansteurn aus Volatus mehr und mehr raus zu gehen, wenn ein Aufschwung kommt. Landstücke sind mit die besten in CAD, nur das Mgmt hat eine Scheiß Taktik.

Somit auch zu ORGN / OPW, die bekanntlich eine andere Führung haben. Ganz anderer Stil, ganz andere Ausrichtung. Die kommen echt nicht gut miteinander aus.

OPW Bohrt in Quebec wie ein Käseraspler, die Explorieren durchgehend und steuern weitere Programme an, können noch 5-10 Mio mit den NF Assets machen und haben sogar noch Kohle. Das ist kein Hoax, tatsächlich Drill sie super aggressiv. Das wird so weiter gehen! OPW soll ruhig nochmal auf 5 Cent gehen.

Gleiches für ORGN. Ausserdem hat Blake Morgan noch 2 weitere Plays die erst noch kommen. Alles Top Zusammenstellung und werden von der gleichen Führung nach vorne gebracht.

Volatus und Forty Pillars stehen unter der Macht von Crest, agieren mehr als Real estate Agent und haben mehr einen 5-10 Jahres Plan. Super slow und arbeiten für sich selbst. Musste ich auch alles erst rausarbeiten.

*********************************

Genießt die Sonne, der nächste Schwung kommt. Stay away from CREST.

Optionen

| Boardmail an "GetGo" |

Wertpapier: Gold |

https://www.juniorminingnetwork.com/...or-mining-brief-for-date-b-j-y

Lundin Gold mit Verlustzahlen

https://www.juniorminingnetwork.com/...or-mining-brief-for-date-b-j-y

Kinross Gold mit schlechten Zahlen. Wie so oft gehören Sie zu den Minen mit sehr hohen AISC. Durschnitt ca 1230-1240 US Dollar und Kinross mit 1341 US Dollar pro Feinunze. Trotz einer Marge von satten 845 US Dollar schafft man keinen Gewinn sondern ein Verlust von 9,3 Millionen US Dollar. Hier taugt das Management leider nicht. Seit Jahren nur Probleme. Gurkentruppe.

https://www.juniorminingnetwork.com/...or-mining-brief-for-date-b-j-y

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Was sagt unser Ceo dazu? Bin seit Exploits sehr skeptisch diesbezüglich. Da ist leider klar geworden das die ewig gewartet haben bis Sie auf was signifikantes Treffen. Als nichts getroffen wurde haben Sie dann endlich veröffentlicht. Allerdings kam jetzt von New Found, Sokoman und Labrador auch länger keine Golddrillergebnisse mehr. Im Gegensatz aktuell zu Endurance Gold mit 11 Tagen für die Auswertung eines Bohrlochs laut Angaben vom CEO.

Hast Du eventuell eine Meinung bzw Erklärung dazu?

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Für meine Ausrichtung, glaube ich das Mgmt zieht etwas mit Bazooka hoch und Arrowhead wird ebenfalls spannend.

Ist nur ne Idee - selbst studieren und nachforschen.

Die können ebenfalls mit den Holes erstmal wenig treffen. Einfach Schatz-sucher, extrem Risky. Opawica stellt sich der Aufgabe auf jeden Fall einen Schatz zu finden.

*****

Bon giorno a tutti. Bin jetzt im Urlaub.

Optionen

| Boardmail an "GetGo" |

Wertpapier: Gold |

War total overscribed. Aktueller Kurs 0.195 cad

Denke nach closing in den nächsten Stunden/Tagen könnte der Kurs anziehen in den nächsten Wochen/Monaten, da man nur noch Open market reinkommt.

Aber Achtung : in 4 Monaten werden 11 Cent Tickets fällig. Ggf eine Tradingopportunität

Ich kann mir vorstellen, dass der Uransektor bald nochmal sehr explosiv werden könnte

Keine Empfehlung

Optionen

| Boardmail an "Jacky Cola" |

Wertpapier: Gold |

Was ist eigentlich mit Sprott. Der wollte doch für 0,30 cad rein?

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

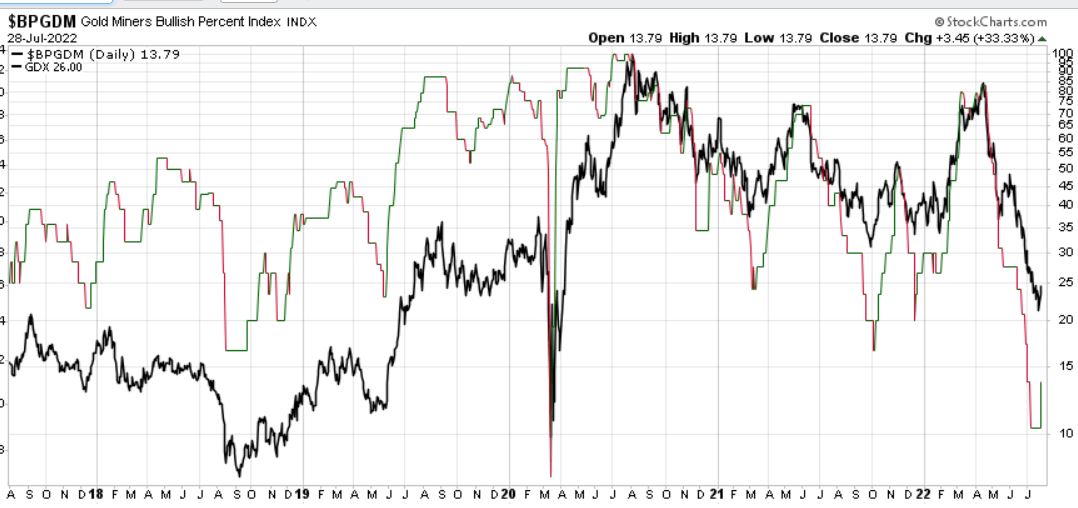

https://www.finanzen.net/realtimekurs/petrobras@lus

Die kommt jetzt tatsächlich auf über 50% Jahres-Dividende. Feine Sache, da rollt demnächst die Kohle.

Ein Wert von 10 ist im 5 Jahreschart extrem tief. Phase grün: Kaufsignal.

Angehängte Grafik:

bpgdm_20220728.jpg (verkleinert auf 47%)

bpgdm_20220728.jpg (verkleinert auf 47%)