Die besten Gold-/Silberminen auf der Welt

Es gibt auf den Claim Grenzen von Pilbara genügend Plays die überhaupt nicht voran kommen. Auch das kann nicht njr Geologie sein.

Problem bei DeGrey, Entwicklung des Share Price quasi 0 seit 2020. Ist vergleichsweise nicht schlecht auf der Stelle zu treten, aber halt auch gewinnbringende Investition.

Lassonde Curve, Entwickler zum Produzenten, kleben geblieben. Gibt viele ähnliche Plays, die treten einfachbauf der Stelle, bis sie in Produktion gehen. Dieser Übergang ist dann genauso riskant wie Exploration.

Aus Sicht der Shareholder sollten sie das Projekt vertraglich übergeben, Premium / Zahltag. Wäre der beste Ausgang.

Optionen

| Boardmail an "GetGo" |

Wertpapier: Gold |

Ich selbst wünsche mir hier die eigene Produktion da dann das Potential komplett gehoben werden kann. Bisher läuft es wirklich gut. Werde hier mal die letzten Meldungen einstellen.

Ein Goldproduzent mit 300000 Unzen Goldproduktion mit niedrigen AISC aus Australien wird meiner Meinung nach, nach erfolgreicher Produktion deutlich höher bewertet sein als heute. Klar wird mein Szenario noch dauern und hat Risiken. Wenn es klappt wird es sich lohnen. Des Weiteren hatte ich hier das Glück zu Tiefstkursen zu kaufen. Die aktuellen noch 20000 Aktien haben mich gerade mal ca 600 Euro gekostet . Die restlichen Anteile 45000 Aktien hatte ich ab0,30 aud veräußert. Für mich ein Bombengeschäft. Für Investoren die erst 2020 oder kurz vorher eingestiegen sind ist es bitter. Sie müssen bis zur Produktion oder Übernahme warten um einen guten Schnitt zu machen. Gold Road ist jetzt neuer Großaktionär mit knapp 14,5 Prozent . Es gibt Gerüchte das evtl zum späteren Zeitpunkt ein Übernahmeangebot geben wird . Angeblich ab 2,30 aud könnte es auch klappen. Hatte ich ja letztens schon geschrieben.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://cdn-api.markitdigital.com/apiman-gateway/...094df02a206a39ff4

Malina Gold Resource

https://cdn-api.markitdigital.com/apiman-gateway/...094df02a206a39ff4

Recoverydaten sind sehr gut gewesen.

https://cdn-api.markitdigital.com/apiman-gateway/...094df02a206a39ff4

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://cdn-api.markitdigital.com/apiman-gateway/...094df02a206a39ff4

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://cdn-api.markitdigital.com/apiman-gateway/...094df02a206a39ff4

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://cdn-api.markitdigital.com/apiman-gateway/...094df02a206a39ff4

Das ist schon wichtig damit man auch im nächsten Jahr einen schönen Erlös aus dem Verkauf der Aktien generieren kann und muss um die Dilution der Aktien in Grenzen zu halten.

https://cdn-api.markitdigital.com/apiman-gateway/...094df02a206a39ff4

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Läuft aktuell alles nach Plan soweit.

Präsentation

https://www.argosyminerals.com.au/sites/default/...ements/2388417.pdf

Update

https://www.argosyminerals.com.au/sites/default/...ements/2387971.pdf

Aktionärversammlung

https://www.argosyminerals.com.au/sites/default/...ements/2388583.pdf

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://cdn-api.markitdigital.com/apiman-gateway/...094df02a206a39ff4

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Ich bin Anfängerin und möchte gerne Goldmünzen kaufen. Besonders interessant finde ich russische Goldmünzen. Es gab eine für mich attraktive Serie Rettet unser Welt,aber auch andere Goldmünzen, die ich leider direkt aus Russland im Moment nicht bekommen kann. Kann mir jemand bitte helfen, wo ich diese Münzen hier in Deutschland kaufen kann?

Vielen Dank!

https://cdn-api.markitdigital.com/apiman-gateway/...094df02a206a39ff4

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://wcsecure.weblink.com.au/pdf/SHP/02526142.pdf

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Will ich Münzen, die möglichst nahe am Unzenpreis zu kaufen sind haben oder solche, die einen zusätzlichen Aufpreis für Seltenheit, Alter usw. haben und der bezahlt werden muß.

Die nächste Frage: Was will ich in der Zukunft damit machen. Schwere Stücke sind evt. billiger, aber wenn wir einen Unzenpreis von 5 oder 10.000$ haben, auch nicht beim Bäcker oder Metzger verkaufbar.

Kleine Gewichte haben einen zusätzlichen Herstell-Aufpreis ( 1 Gramm ist fast genau so teuer als Münze/Barren herzustellen wie eine 31x so schwere 1oz-Münze )

Willst Du die Münzen mal vererben stellen sich manche Fragen nicht oder ganz anders.

Erst wenn Du Dir über Deine Haltefristen und Ziele im Klaren bist, kannst Du die Beschaffung definieren.

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Gold |

https://www.minenportal.de/artikel/...ents-as-at-January-31-2022.html

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://www.youtube.com/watch?v=o3iEN0-cs2I

https://www.globenewswire.com/news-release/2022/...ech-Plc-to-19.html

Im Mai alleine 3800 Unzen Gold produziert und damit weiter das Produktionsniveau gesteigert. Jetzt kommt aber Cashflow rein ;-)

Auch gut stabil die Aktie und grün heute...

Der Laden ist gerade nicht mal 70 Mio. € an der Börse wert ;-)

Angehängte Grafik:

screenshot_20220528-133422_chrome.jpg (verkleinert auf 47%)

screenshot_20220528-133422_chrome.jpg (verkleinert auf 47%)

wechseln die Seiten. Von Bitcoin zu Gold ...

https://www.gold-eagle.com/article/...ast-bitcoin-investors-turn-gold

Kann man sich nur wünschen 😉

Interessant die Schlussfolgerung, dass kein privater Raub die Menschheit ähnlich ausgeplündert hat.

Viele Möglichkeiten sich zu schützen/wehren gibt's nicht Gold ist definitiv eine der logischsten. Umso bitterer dass uns die gleichen Verdächtigen auch dort beklauen.

Wenn man dann noch darüber nachdenkt, wer die größten Massenmörder waren und sind, da zum Ergebnis Staaten kommt, mit einem "Regierenden" auf dem alles gerechnet wird.

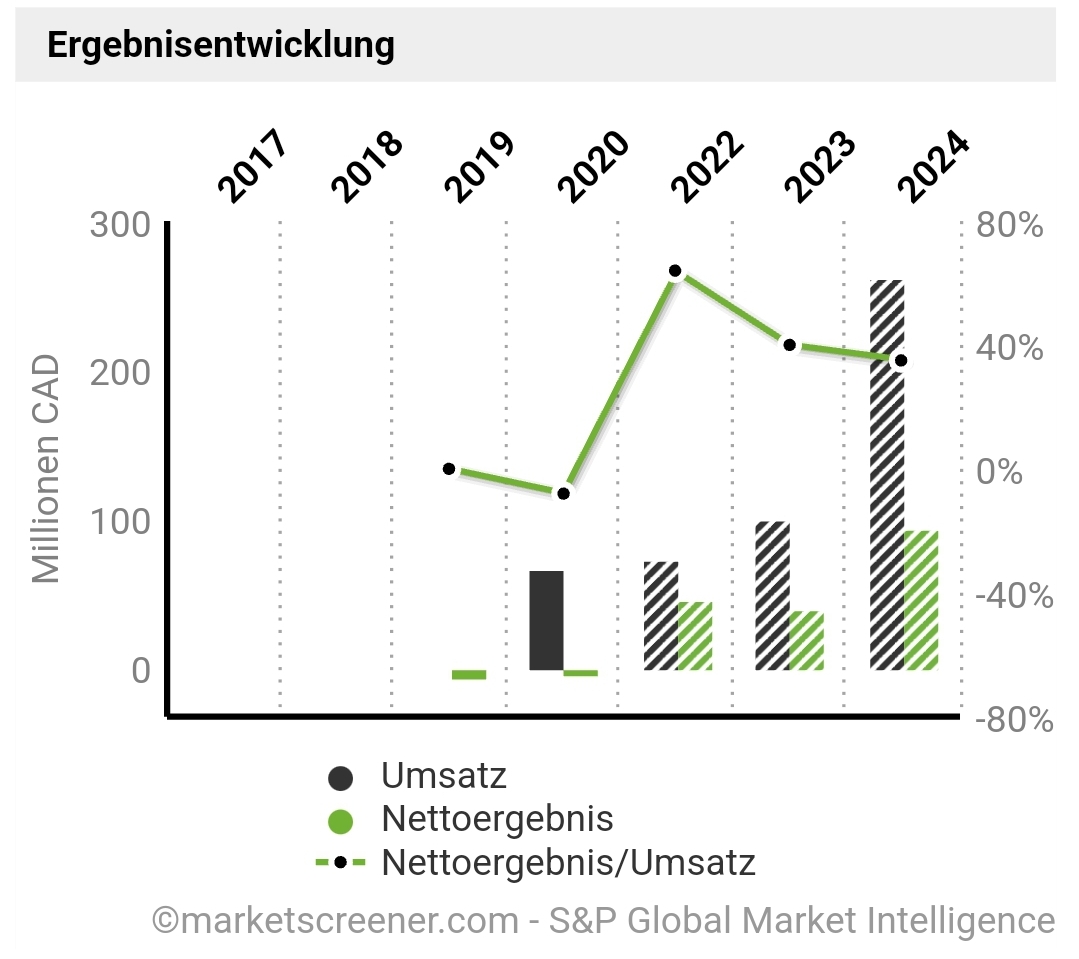

Wachstum bis 2030 soll bei ca 30 Prozent Produktionsteigerung liegen.

Die AISC sollen ab 2023 bis 2025 deutlich unter 1000 US Dollar sein.

Premiumbewertung mit ca 284 US Dollar pro Feinunze Gold

Laut der Analyse aktuell ca 50 Prozent unterbewertet. Aktuelles Kursziel ca 75 US Dollar.

Dazu kommt das die Insider in letzter Zeit für satte über 1,5 Mio US Dollar eigene Aktien gekauft haben. Das ist ein Statement. Dazu sollen in diesem bis zum nächsten Jahr immerhin ca9 Millionen Aktien zurück gekauft werden.

Da kommen wir dann langsam in Richtung 120 CAD Alltimehoch.

Sehr wichtig das dieses Kursziel bei einem durschnittlichen Goldpreis von 1900 US Dollar gilt. Wenn der Goldpreis mal ausbricht über die 2000 US Dollar und das nachhaltig geht hier dann die POS ab.

Wer ist noch Premium in Kanada und gehört zu den Topminen bzw zu den Toproyaltiefirmen?

Auf jeden Fall

Westdome Gold und Wheaton Precious Metals sowie Osisko Gold Royaltie.

Hat jemand hier aus dem Forum eine der Topaktien?

Dazu gehören auch Royal Gold,Sandstorm Gold und der Primus im Royaltiesektor. Leider fällt mir spontan der Name nicht ein.

Dazu gibt es natürlich auch noch sehr gute Minen in Australien und Russland. Letzteres aktuell mehr oder weniger nicht investierbar.

Dazu aus dem Juniorsektor eine Gold Royaltie mit sehr guten Wachstumsprofil und erstklassigen Portfolio .

Agnico Eagle Mines: Post-Earnings Slide Is A Gift

May 17, 2022 11:44 AM ETAgnico Eagle Mines Limited (AEM)41 Comments44 Likes

Taylor Dart profile picture

Taylor Dart

24.65K Followers

Following

Summary

Agnico Eagle Mines released its Q1 results last month, reporting quarterly production of ~660,600 ounces of gold, or ~806,300 ounces when adjusting for the date of the merger closing.

This translated to significant growth from pre-merger levels, and the company is set up for a strong second half due to back-end weighted production.

While the improved unit costs due to synergies and improved labor position are good news short term, it's the long-term potential that makes Agnico stand head and shoulders above its peers.

Given the rare mix of growth and value here, with Agnico able to grow production ~30% by 2030 and trading at barely 1.0x P/NAV, I see this post-earnings swoon as a gift.

Fosterville Gold Mine

tracielouise/E+ via Getty Images

The Q1 Earnings Season for the Gold Miners Index (GDX) is nearly over, and one of the first companies to report its results was Agnico Eagle Mines (NYSE:AEM). Unfortunately, despite a solid report with lower than expected cost creep, the stock has slid another 10%, being dragged down by a risk-off environment due to volatile global markets and softness in the gold price (GLD). This post-earnings swoon is a gift, with Agnico having the best growth profile among the 2.0+ million-ounce producers by a wide margin yet trading at barely 1.0x P/NAV and just ~8.5x FY2023 cash flow with a ~3.0% dividend yield.

All figures are in US Dollars unless otherwise noted.

Detour Lake Operations

Detour Lake Operations (Company Presentation)

Just over three weeks ago, I wrote on Agnico Eagle Mines, noting that the 18% pullback in the stock had set up a buying opportunity. This was because the stock had put out solid production results at Detour Lake, Fosterville, and LaRonde and had an even stronger H2 ahead given its back-end weighted production. Unfortunately, the post-earnings gains in the stock were quickly erased. This reversal can partially be attributed to the risk-off environment in global markets, the softness in the gold price, and negative sentiment surrounding gold producers due to the tight labor market and climbing diesel prices.

Specifically, the gold price briefly slid below $1,800/oz, crude oil prices are well above $100/barrel, and many gold producers have reported higher labor costs due to a very competitive environment for both contractors and skilled workers. For investors in Agnico Eagle, the warnings of lower profitability and guidance revisions for costs on other conference calls may be concerning. Given this more negative outlook, I believe it's worth discussing how Agnico Eagle stacks up in this inflationary environment and whether investors should be concerned about their investment in the stock.

Inflationary Pressures

Although the weaker gold price, higher fuel prices, and higher labor costs are undoubtedly valid negative talking points for producers, investors must discern between producers at serious risk and those that could see short-term pressure but limited long-term effects. In the case of operators like Victoria Gold (OTCPK:VITFF) or Argonaut Gold (OTCPK:ARNGF) that move a significant amount of material at relatively low grades and don't benefit from economies of scale, the inflationary pressures are a serious problem.

However, the inflationary pressures are merely a speed bump for companies like Newmont (NEM) and Agnico that operate massive mines and have high-margin projects in their pipeline. This is especially true given that they're investing heavily in exploration, automation, and technology. For smaller producers moving a significant amount of material at lower grades that don't have the balance sheet strength to invest aggressively, the inflationary pressures are a roadblock, impeding them from past profitability levels unless they get help from the gold price.

In fact, Agnico is in a unique position from a labor standpoint, given its 20+ year mine lives at Canadian Malartic and Detour Lake that it's the employer of choice. Hence, it shouldn't have to fight tooth and nail to secure/retain skilled workers, and workforce availability is even more important than short-term cost pressures or supply chain headwinds. This is because while higher costs for consumables and fuel drive costs higher, it's even more costly to have equipment sitting idle due to elevated absenteeism. The latter means not meeting projected mining/development rates, and it results in the processing plant relying on lower-grade stockpiles in many cases.

Meanwhile, the company is looking at ways to drive unit costs lower at its operations, including the possibility of trolley assist at Detour Lake and a higher throughput rate. In addition, Agnico benefits from corporate G&A synergies from its recent merger with Kirkland Lake, with $400 million in expected synergies over 10 years, up from $320 million previously. In addition to this, the company expects $1.1 billion in operational synergies. This combination of optimizing operations and the benefit of synergies combined with a loyal workforce should help Agnico to be better insulated from the inflationary storm than its much smaller peers and even some other million-ounce producers.

Costs and Margins

If we dig into costs and margins, it's understandable that some investors might be a little nervous, especially with inflation readings continuing to trend above estimates. For those unfamiliar, this has affected fuel costs, labor costs, consumables costs, and materials costs in the sector, making it more expensive to get each ounce of gold out of the ground and tacking on some additional costs to new projects/sustaining capital. The below chart certainly paints what might appear to be an ugly picture of a steady uptrend in costs for Agnico Eagle, with costs rising from $741/oz in Q1 2017 to $1,079/oz in the most recent quarter.

Agnico Eagle Mines - Quarterly All-in Sustaining Costs

Agnico Eagle Mines - Quarterly All-in Sustaining Costs (Company Filings, Author's Chart)

Agnico has ~40% of its 2022 fuel hedged, which has helped the company, but given that diesel prices have continued to trend higher, some investors might be worried that costs will only worsen going forward. While it's certainly possible that FY2022 all-in sustaining costs [AISC] could come in at the top end of guidance at $1,050/oz, the company will see improved costs going forward due to synergies, as well as benefits from optimization work and organic growth at existing assets (Macassa, Detour Lake, Kittila) looking out to 2025. So, while costs may be higher in 2022 ($1,050/oz vs. $1,038/oz), I would expect this trend to reverse in 2023.

Agnico Eagle Mines - Annual Average Realized Gold Price, AISC & AISC Margins + Forward Estimates

Agnico Eagle Mines - Annual Average Realized Gold Price, AISC & AISC Margins + Forward Estimates (Company Filings, Author's Chart & Estimates)

It's also important to note that while the headlines point out that the inflationary pressures are disastrous for miners, given that the gold price has not gone anywhere in the same period (2020-2022), this view is incomplete. This is because many of these negative articles on producers omit the important point that while inflation has led to a more than $120/oz increase in AISC between H2 2020 to H2 2022 estimates sector-wide and the gold price hasn't budged, the gold price moved ahead of inflation.

This is evidenced by the above chart, showing that the gold price rose from $1,489/oz in 2019 to $1,876/oz in 2020 and should average $1,880/oz in FY2022. Hence, the gold price has offset these costs, just not in the chosen time frame, weakening the argument that producers are un-investable or seeing significant margin compression. So, while AEM's costs have increased from $938/oz in FY2019 to ~$1,050/oz in FY2022, its margins will improve from $551/oz to $830/oz, a more than 50% increase.

Looking ahead, I would not be surprised to see Agnico's costs drop to $985/oz in 2023, $955/oz in 2024, and $940/oz in 2025. Even if we assume that the gold price goes nowhere, this would still represent margin expansion vs. 2021 levels ($757/oz), with AISC margins climbing to $940/oz, or 50% AISC margins. In summary, there are reasons to be bearish on some gold producers, and I would argue that 60% of the sector is un-investable if gold prices stay below $1,900/oz. Still, one must be careful not to lump the sector laggards like Argonaut, Great Panther (GPL), Pure Gold (OTCPK:LRTNF), Iamgold (IAG), and many others in with the leaders with exceptional track records and margin expansion, like Agnico Eagle.

Long-Term Growth

If we look at the chart below, we can see that Agnico Eagle ranks highly on diversification, with multiple mines making up its current ~3.3 million-ounce production profile. This production profile that relies on more than 10 assets means that any hiccups at a single asset have a relatively limited impact across the portfolio, and for investors looking to invest in the sector without indigestion, these are exactly the types of companies they should be looking for when hunting down potential investments.

However, in addition to diversification, Agnico Eagle has meaningful organic growth across its portfolio and a development pipeline of very solid assets capable of driving significant growth as we look toward 2029/2030. In addition to growth at Detour Lake with a higher throughput rate (~32+ million tonnes per annum), an increase in throughput to ~6,250 tonnes per day at Meliadine, an increase in throughput at Kittila, and the benefits of the #4 Shaft and drifting towards Alamgamated Kirkland at Macassa, there are a few advanced opportunities in the portfolio outside of existing assets.

Kirkland Lake Camp + Holt Mill

Kirkland Lake Camp + Holt Mill (Company Presentation)

These include Upper Beaver in the Kirkland Lake Camp, a gold-copper deposit that is capable of producing up to 200,000 ounces per annum with low costs due to copper by-product credits. Another opportunity is Santa Gertrudis, a small project in Mexico that should have very high margins given its high oxide grades and underground potential. Combined, these two projects could add 325,000 ounces per annum at sub $900/oz costs. Elsewhere, there's additional upside if Agnico finds a way to combine the idle processing capacity at the Holt Mill with the Upper Canada resource base in the Kirkland Lake Mining Camp.

Between advanced projects and organic growth (existing operations), plus the potential for Hope Bay to produce 200,000-plus ounces in 2026 and grow to 275,000 ounces by the end of this decade, I see a path to ~4.3 million ounces of annual gold production by 2030 for Agnico Eagle. This would translate to a ~4% compound annual production growth rate or 30% production growth. This may seem low, but it's a country mile ahead of the declining production profiles that we've typically seen from multi-million-ounce producers.

The chart below shows Agnico's potential progression in annual production per my estimates, and I have conservatively modeled Fosterville with an average production profile of 260,000 ounces per annum in case the company must employ a higher-tonnage, lower-grade model if it doesn't make new 10+ gram per tonne gold discoveries. However, my 2030 production estimate of 4.25 to 4.30 million ounces per annum is a base case (30% production growth), and the upside opportunities cannot be understated.

Agnico Eagle Mines - Annual Production & Forward Potential

Agnico Eagle Mines - Annual Production & Forward Potential (Company Filings, Author's Chart & Estimates)

In addition to the potential to see Hope Bay produce 300,000 to 400,000 ounces per annum (150,000 ounces above my estimates at the high end), which was mentioned in passing in the Q1 2022 Conference Call, there's the potential to add an another 120,000-plus ounces per annum with the Holt Mill by processing Upper Canada material. There's also the potential to add 200,000-plus ounces per annum from Hammond Reef, but this is a higher-capex project that I think will need a $2,000/oz gold price to justify, and I see it as a longer-term opportunity.

Fosterville - Quarterly Gold Production

Fosterville - Quarterly Gold Production (Company Filings, Author's Chart)

However, the biggest upside and bonus opportunity I see, which seems to be forgotten, is Fosterville. For those unfamiliar, this asset produced ~600,000 ounces of gold in FY2019 and ~640,000 ounces in FY2020 and was the world's highest-grade gold mine by a wide margin. Since then, we've seen the highest-grade reserves at the mine depleted, with the mine operating at a slightly higher throughput rate but with much lower grades, hence the decline in production. However, the best place to make an ultra-high grade gold discovery is next to where ultra-high grade gold has been mined for years. For this reason, I would not rule out another 15-25 gram per tonne discovery being made at this mine.

The good news is that under Agnico, which has growth coming from several areas and a diversified base of 10+ mines, there's no urgency to make a discovery here, and Fosterville, at 250,000 ounces to 350,000 ounces per annum at industry-leading costs, can complement the portfolio while the company works to hit another the motherlode. Suppose we were to see another major discovery. In that case, Fosterville's annual production could increase to 425,000 to 500,000-ounces per annum, boosting production materially above what I've modeled for the remainder of this decade (~260,000 ounces per annum).

It's also important to point out that while Fosterville doesn't get as much attention as it used to given that we haven't seen any holes like 16 meters of 404 grams per tonne gold drilled in 2019, recent results have still been solid. These have included 2.9 meters at 365 grams per tonne of gold near current reserve stopes, and 2.2 meters at 51.7 grams per tonne of gold in inferred resource blocks. Additionally, we saw two solid holes that included 1.4 meters of 54.5 grams per tonne of gold and 2.2 meters of 174.4 grams per tonne of gold in new sub-parallel splay structures to Swan (Ptarmigan, Pen).

Robbin's Hill Deposit - Fosterville

Robbin's Hill Deposit - Fosterville (Company Presentation)

Moving north on the property, we saw intersections of 2.5 meters of 81.3 grams per tonne of gold at nearby Robbin's Hill, and grades appear to be improving at depth, similar to what we saw at Phoenix. Obviously, these intercepts are nowhere near the grades we were seeing in 2019 that helped Kirkland Lake Gold command a massive premium over its peers from a P/NAV standpoint. Still, these solid holes that are still well above the industry average will help to build up reserves and resources, allowing Agnico to maintain a respectable production profile at Fosterville and generating meaningful free cash flow while it hunts down another major discovery.

To summarize, while I see 4.25+ million ounces of annual gold production as achievable in FY2030, I think there's some bonus upside to this production profile that could push Agnico's production profile above the 4.5 million ounce mark. This is not heavily reliant on a new discovery at Fosterville and could stem from an extra 100,000 ounces per annum at Hope Bay and an extra 100,000 ounces per annum if the company can exploit the excess processing capacity at either Holt or the Canadian Malartic Mine [CM]. This should excite both current and prospective investors. This is because in the nearly 15 years I've traded this sector, I don't recall the last time I saw an organic growth profile this attractive among a 3.0+ million-ounce producer.

Valuation

Based on ~454 million shares and a share price of $51.60, Agnico Eagle trades at a market cap of ~$23.4 billion. No matter how you slice it, this is a dirt-cheap valuation. Starting with reserves and resources, Agnico Eagle is valued at just $278/oz based on its ~84 million ounces of reserves and measured & indicated resources. This can be a tricky way to value high-cost producers, given that while a $300/oz valuation may look cheap, it isn't that cheap at all if their cost to get gold out of the ground is above $1,400/oz. However, in Agnico's case, this $278/oz figure is less than one-third of its expected FY2025 AISC margins ($940/oz) even at a $1,880/oz gold price.

It's also important to note that this $278/oz figure values all of the company's inferred resources at zero, with its inferred resource base coming in at ~30.6 million ounces. Typically, we see conversion rates on inferred resources well above 50%, so I would argue that it's ultra-conservative to value this category of the resource base at zero. Notably, this inferred resource base that I've chosen to value at zero in this reserve/resource valuation contains some very high-grade ounces, which include the following:

1.41 million ounces at ~5.07 grams per tonne gold at Hope Bay

3.05 million ounces at ~3.07 grams per tonne gold at East Gouldie

1.88 million ounces at ~3.30 grams per tonne gold at LaRonde/LZ5

0.83 million ounces at 5.98 grams per tonne gold at Robbin's Hill

Agnico Eagle Historical Cash Flow Multiple

Agnico Eagle Historical Cash Flow Multiple (FASTGraphs.com)

If we look at Agnico Eagle from a cash flow standpoint, we can see that the stock has historically traded at ~13.7x cash flow (15-year average), and closer to 19x cash flow if we were to use a 20-year lookback period. I believe it's best to be conservative and use the most recent period for trying to find a fair value for a company. Under this assumption, and using the 10-year average (12.6x cash flow), Agnico's 18-month fair value (FY2023 estimates of $5.95) would come in at $75.60.

This points to a nearly 50% upside from current levels. I would argue this price target is more than fair and even conservative, given that the gold price is trading at the high-end of its 10-year range. The other reason that this price target is conservative is that it doesn't give any value to Agnico's robust project pipeline that is not only made up of exceptional projects but these projects are located in mostly Tier-1 jurisdictions. I believe this pipeline to have an NPV (5%) of $2.7+ billion, with the main contributors being Upper Beaver/Upper Canada, Santa Gertrudis, Hammond Reef and Hope Bay.

Agnico Eagle - Advanced Pipeline Projects

Agnico Eagle - Advanced Pipeline Projects (Company Presentation)

If we divide this figure by 454 million shares, this translates to another ~$6.00 per share in value on top of the fair value based on the FY2023 cash flow price target of $75.60. Importantly, this price target based on cash flow assumes no upside in the gold price above $1,900/oz, and this price target assumes a static share count. However, Agnico Eagle recently unveiled a new tool in its planned returns to shareholders, including the approval to repurchase up to 9 million shares under its NCIB. Given where the stock is trading, I would not be surprised to see the company active on its share buyback program, suggesting some upside to the price target if all 9 million shares are repurchased before year-end 2023.

Agnico Eagle Mines - Insider Buying

Agnico Eagle Mines - Insider Buying (SEDI Filings)

Finally, it's worth noting that Agnico's Chairman, Sean Boyd, and its new CEO, Ammar Al-Joundi, have been active buying back shares this year, a nice vote of confidence. In total, we have seen share purchases valued at C$1.67 million (US$1.33 million) since February alone at an average price above US$52.00. This suggests that top management sees value in the company's shares at a value above today's levels, and I would not be surprised to see more insider buying if the stock continues to hang out near the US$50.00 level, given how bright the future is for the company.

Agnico Eagle Operations

Agnico Eagle Operations (Company Website)

Agnico Eagle didn't have the best Q1 performance from a headline standpoint, given that this was the first quarter for the company post-merger, and the company expects to see back-end weighted production (roughly 45% / 55% split). However, the future outlook could not be more exciting with continued exploration success at its two largest mines (DL and CM) that should lead to meaningful organic growth later this decade, and the company is tracking ahead of plans on its synergies. This points to continued production growth per share, improved unit costs through projects being looked at internally, and growth in reserves per share.

Most importantly, Agnico Eagle is one of the only multi-million-ounce producers with the potential to increase production by 30% this decade (3.3 million ounces to 4.3 million ounces) if it can execute successfully, all while maintaining its industry-leading Tier-1 jurisdiction profile. This differentiator is huge, given that investors that have wanted relatively low beta and diversification have had to sacrifice on growth in the past. The reason is that the largest producers sector-wide have struggled to grow production. Hence, investors previously had to go much further down on the value chain to find meaningful growth, but often at the expense of jurisdictional safety, a lack of diversification (fewer mines), and much higher share-price volatility.

Agnico Eagle Operations

Agnico Eagle Operations (Company Presentation)

Given that Agnico has this growth with a phenomenal project pipeline, the company can sit back and deliver on its plans, buy back shares, and not worry about acquiring to replace reserves/create growth like other companies have done in the past. This should translate to significant growth in cash flow per share, production per share, and reserves per share, precisely what investors should be looking for in any investment in the gold space. Based on this very bright outlook, I am hard-pressed to find a more attractive way to gain exposure to gold, and I continue to accumulate a position in AEM on weakness. Hence, I see this post-earnings swoon in the stock as a gift.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://www.goldseiten.de/artikel/...-at-the-Dukes-Ridge-Deposit.html

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Gold |

https://www.visualcapitalist.com/...mines-in-the-world-by-production/

The Top Gold Mines in 2021

The 10 largest gold mines are located across nine different countries in North America, Oceania, Africa, and Asia.

Together, they accounted for around 13 million ounces or 12% of global gold production in 2021.

Share of global gold production is based on 3,561 tonnes (114.5 million troy ounces) of 2021 production as per the World Gold Council.