Die besten Gold-/Silberminen auf der Welt

0:00 Introduction 0:53 Max Fischer Macro 6:02 Kevin Smith Macro 27:48 Quinton Hennigh Introduction 35:38 Drilling Updates 43:59 Eskay Mining Update 46:05 Core Assets Update 46:35 Goliath Resources Update 47:53 Eloro Resources Update 49:32 I-80 Gold Update 50:52 Western Alaska Minerals Update 51:44 E2 Gold Update 52:44 Kingfisher Metals Update 53:38 Tombill Mines Update 55:26 Prospector Update 56:16 Cassiar Gold Update 57:29 Lion One Metals Update 58:27 Pacific Ridge Exploration Update 59:25 Alpha Exploration Update 1:00:49 Newfound Gold & Labrador Gold Update 1:01:36 Aurion & Firefox Update 1:03:22 Bell Copper, BCM & Zacapa Updates 1:04:37 Other Junior Miner Updates 1:08:19 Conclusion

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Gold |

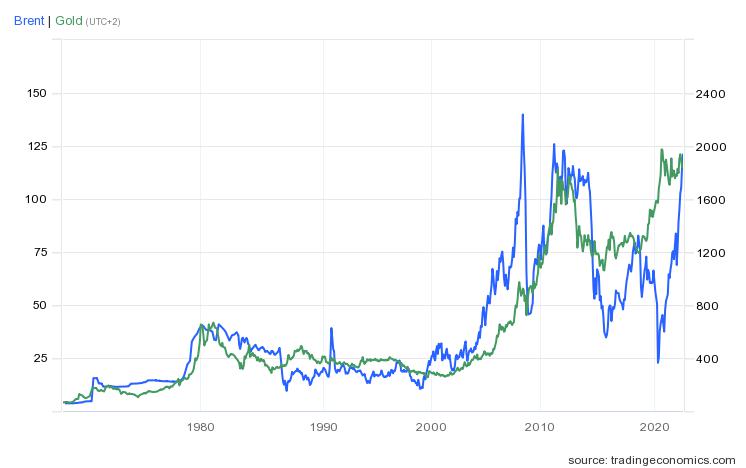

Corona hat den Ölpreis nach unten verzerrt und der Russland- Krieg jetzt nach oben- zusätzlich sind die Investitionen in die Ölförderung in den letzten Jahren zurück gegangen.

Ich denke dass wir nicht mehr unter 100$ fallen und wir in den nächten Wochen einen Höchststand für längere Zeit erreichen.

Die Ölproduzenten sind für den aktuellen Ölpreis noch sehr niedrig bewertet KGV 3, teilweise gibet es ach noch Shortquoten von bis zu 10%, was noch zusätzliches Potential bietet, falls wir noch mal massiv ansteigen.

https://ceo.ca/@newswire/...nnounces-2022-first-quarter-financial-and

https://ceo.ca/@newswire/frontera-announces-first-quarter-2022-results

https://ceo.ca/@nasdaq/...ca-oil-announces-2022-first-quarter-results

Ölfelddienstleister könnte man vielleicht einen reinnehmen.

https://money.tmx.com/en/quote/NINE:US

https://stocknessmonster.com/news/mrm.asx/

EMP konnte ihrem Gewinn nicht halten

https://hotcopper.com.au/asx/emp/?keywords=EMP

https://hotcopper.com.au/threads/...r-pesa-deal-day-brisbane.6746617/

Optionen

| Boardmail an "DasMünz" |

Wertpapier: Gold |

Angehängte Grafik:

gold_und___l.jpeg (verkleinert auf 68%)

gold_und___l.jpeg (verkleinert auf 68%)

https://goldseek.com/article/cot-gold-silver-usdx-report-june-3-2022

https://m.youtube.com/watch?v=wDwSLaaB-C0

https://www.youtube.com/watch?v=KjpfBmTkALs

Endlich mal werden konkrete Namen genannt.

https://www.sprottmoney.com/blog/...TAS-Games-Craig-Hemke-May-17-2022

Moderation

Zeitpunkt: 07.06.22 12:26

Aktion: Löschung des Beitrages

Kommentar: Moderation auf Wunsch des Verfassers

Zeitpunkt: 07.06.22 12:26

Aktion: Löschung des Beitrages

Kommentar: Moderation auf Wunsch des Verfassers

https://money.tmx.com/en/quote/LIO/news/...nt_Resource_at_Tuvatu_Fiji

ASX: CPO +162% für 23M AUD

https://hotcopper.com.au/threads/...ersects-173m-1-05-copper.6780061/

https://de.investing.com/equities/culpeo-minerals

Sand finden die Australier auch gut +21%

https://hotcopper.com.au/threads/...arget-and-ml-application.6780871/

https://hotcopper.com.au/asx/drx/

Auch ein tolles Bohrergebnis gab aber nur 4,7% dafür.

https://hotcopper.com.au/threads/...u-colosseum-gold-project.6780388/

Aftermath bekommt -7% für dieses Ergebnis - 65.3 metres at 408 g/t Silver, 0.91% Copper and 5.9% Mn including 18.95m at 1,162 g/t Silver, 1.1% Copper and 10.6% Mn.

Was stimmt hier nicht, außer der Standort ? Coronatief wird bald getestet, wenn es so weiter geht.

Die letzte Kapitalerhöhung lag bei 0,65 CAD, 15.6 Million CAD.

https://ceo.ca/@newsfile/...ncreases-private-placement-to-156-million

https://money.tmx.com/en/quote/AAG/news/..._Silver_at_Berenguela_Peru

Optionen

| Boardmail an "DasMünz" |

Wertpapier: Gold |

Hervorragende Längen und Grades. Dazu vom neuen Target noch 2 kleine low Abschnitte von über1 Gramm. Bin zufrieden.

Man sieht das die Liegenschaft Potential hat.

prospect.

"The 2022 drilling at Reliance is off to an excellent start with this RC intersection at the 020 Target, providing confidence in the potential for this structure to have significant exploration potential,"commented Robert T. Boyd, CEO of Endurance Gold. "A near-surface drill intersection with 202 gram-meter product is a rare privilege in an orogenic gold system and this hole RC22-062 is the eighth hole completed by Endurance Gold returning greater than 100 gram-meters

https://www.minenportal.de/artikel/...m-Reliance-2022-RC-Program.html

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://www.minenportal.de/artikel/...10m-at-the-Keats-Main-Zone.html

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

t globally. Already the leading source of low-CO2 Ti into the paint industry, in a surprise development it is now the second largest contained graphite resource globally too. Key takeaways for us are (i) global resources nearly triple to 1.8Bt, with grade rising as new higher-grade zones were added. We see this as ‘too big to ignore’, even doubling the PEA to 24Mtpa would give this a >50 year life better than the largest mines in Africa (Tronox, Rio, Kenmare). Next, (ii) high-confidence M&I resources double the 4Q21 scoping study inventory, with a high-grade (the top 4-5m) cut off 241Mt @ 1.5% rutile, both of which should drive improved economics. We double our inventory and production, which lifts our 1xNAV10% to A$1.4bn net of minority interests and staged capex, and processing only 1/3 of the MRE. Finally, (iii) being grid hydro-powered, continuous-backfill hydro-mining, on rail, gravity recovered and low-CO2 natural rutile already gave the asset world-leading ESG credentials. As a material graphite deposit, those just got stronger. The unique genesis as metamorphosed sand for high-purity Ti, but weathered for soft-surface mining / enrichment, drives this. As evidenced by the -60% share price of the largest graphite asset since 1Q18, the ‘dirty little secret’ of graphite mines (low prices on early pre-qualification production) is a non-issue here as rutile will ‘pay the bills’ early on.

We maintain our BUY rating and lift our A$1.40/sh PT to A$1.65/sh based on a 0.5xNAV multiple for Kasiya, holding the 1.2Bt of unmined material at just 0.2% in-situ. This name is catalyst heavy with (a) an updated scoping study in 2Q22 to incorporate larger resource for an SCPe doubling of production, (b) additional off-take in addition to the ~20% already released at a premium, and most importantly (c) rutile prices, where low-volume spot is over US$2,000/t against US$1,351/t last-reported market prices (themselves reflecting last year’s contracts). Effectively 2Q21 contract prices won’t be fully reported until November this year as even 2Q will have some layover of 1Q contracts, ie we already expect QoQ price rises to be reported 6M from now. One silly statistic – Sovereign now has 26Moz AuEq of free-dig zero strip ore requiring only gravity separation. Substantial engineering work is required ahead to address hydro mining, slurry pipes, mineral separation and more, but the key risk, finding the metal in the ground, is past.

Da mit 0,5 NVA aktuell gerechnet wird, gibt es noch zusätzliches Aufwärtspotential in der Zukunft.

https://sprott.com/media/5088/220405-scp-svm-mre.pdf

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Das wäre geil als Langfristianleger aus knapp 1000 Euro am Ende über20000 Euro brutto einzustreichen wenn alles hier gut klappt.

BUY rating, lift PT from A$1.40/sh to A$1.65/sh

We apply a 0.5xNAV to our A$1,390m Kasiya NPV to capture production growth ahead. As such, we maintain our BUY rating and lift our A$1.40/t price target to A$1.65/t based on a 0.5xNAV multiple on a diluted-for-options but not build basis (Table 4). To sense check our valuation, we convert our asset NPV to a group NAV by modelling an US$350m funding package (against US$775m capex). Applying 65% gearing using 10% lender IRR debt, and modelling equity dilution through to first production, gives our FF FD 1xNAV10% of A$2.99/sh at first production. Given this still accounts for Kasiya at only US$1,346/t vs spot >US$2,097/t this upside from the current share price is clear.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Nur am gleichen Tag sich diametral widersprechende Nachrichten zu verbreiten ist der Hammer.

Bekommen die jetzt Geld dafür das sie Nachrichten raushauen egal ob richtig oder falsch. Wenn dem so ist Tipp von mir immer alte Nachrichten nehmen und Datum und ein paar Namen austauschen fertig.

https://twitter.com/WallStreetSilv/status/1534022084593999872?s=19

https://www.youtube.com/watch?v=Dkop_NqxAPE

https://youtu.be/OsZQac3L3Vw

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Dazu jetzt die italienische 10 jährige. Anleihe bei weit über 3 Prozent Rendite. Die wird weiter steigen.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Ist das jetzt die neue Definition eines Bärenmarkts, wenn ein neues ATH gebildet wurde, aber wahrscheinlich nur "untergeordnet".

So langsam glaube ich, dass ich hier in einem Irrenhaus gelandet bin.

https://www.gold-eagle.com/article/...d-stay-short-side-junior-miners

Optionen

| Boardmail an "grafikkunst" |

Wertpapier: Gold |

Und der Mr. Radomsky ist ja wohl der Permabear schlechthin und hat hin und wieder recht.

Kiel Institut für Weltwirtschaft (IfW): Staus der Containerschiffe erreichen die Nordsee. „Erstmals seit Ausbruch der Pandemie stauen sich Containerschiffe auch in der Nordsee vor den Häfen Deutschlands, Hollands und Belgiens", heißt es im aktuellen Handelsindikator. „Hier stecken gegenwärtig knapp zwei Prozent der globalen Frachtkapazität fest und können weder be- noch entladen werden."

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://www.reuters.com/markets/commodities/...ium-hazard-2022-06-07/

Wenn das durch geht herzlich willkommen in der Bananen Republik bei uns sinds" Komiker" die sich Politiker nennen in Entwicklungsländern heißen sie Aborigines.