Die besten Gold-/Silberminen auf der Welt

Es geht um die Anzahl von Posts bzgl. von nur zwei Titeln wenn die aus überwiegend "heute geht es 10% hoch Glückwunsch an alle Investierten besteht" dann kann ich getrost darauf verzichten wenn ich am nächten Tag keine Meldung bekomme das die Aktie um die gleiche prozentuale Entwicklung wieder gefallen ist. Und die Entwicklung von Origen ist eher seitwärts die letzten 6 Monate und das für eine Aktie die hier ständig unbegründet thematisiert wird.

Soll ich jeden Tag ein Update bringen , hey guckt mal ...

NG Energy +18%

Valore Metals +10%

Andean Precious Metals +16,4%

CMC Metals +15,8% (schon lange nichts mehr dies bzgl. von Jacky gehört)

Argent Minerals +16,22% -Silberexplorer gestern in Australien aufgewacht - Sorry hatte allen investierten noch nicht gratuliert

Avidian Group +11%

Minnova +15,3%

Leviathan +15%

Jeden Tag Updates zu jedem meiner ca. 50-60 Werte ? oder nur zu den zwei ?

"Jacky liefert hier topaktuelle Informationen, teilweise aus erster Hand und auch zu anderen Werten als OPW und Origen (z.B. Volatus, Artemis, CMC)."

Das ist nicht korrekt , Volatus ist Getgo und von den anderen beiden Werten habe ich schon lange nichts gehört (Artemis und CMC). Es geht in erster Linie um die zwei Werte zu denen sie einen Draht zum CEO haben. Aber ich kann auch hier nachgucken (https://www.juniorminingnetwork.com) wenn eine vorher Gold und jetzt ist es Lithium Claim aufgenommen wurde.

"Darüber hinaus kann sich die Performance von Origen und OPW wirklich sehen lassen. "

Mhhh, seit IPO sicherlich das wäre der Kurs zu dem Jacky aufgesattelt hat danach und speziell in den letzter Zeit gibt es jede Menge anderer Werte die unsere Aufmerksamkeit bekommen sollten.Wir sind dabei im Gold und Silber auszubrechen und an meiner Liste oben seht ihr das ein Explorer nach dem anderen jetzt wieder heiß wird.Und das kann jetzt schnell gehen das wir Tage mit 10-20% in vielen Werten zu sehen bekommen.

"Und das man sich über Kurszuwächse auch öffentlich mal freuen darf, ist doch normal."

Ich kann verstehen wenn einige hier ein paar Titel im Depot haben und diese immer wieder und wieder hier unterbringen wollen (auch Goldtrust !) um diese zu pushen aber dafür ist das Forum zu klein und wenn die Nachrichten auch noch aus kurzen Freuden Bekenntnissen bestehen nur um sie hier zu nennen dann kann man das natürlich machen aber nicht über Ewigkeiten.Wie gesagt in den letzten 6 Monaten hat sich bei Origen nichts getan. Und das Forum sollte sich auf viele Titel konzentrieren.Wenn ich das machen würde bei 60 Titeln dann habt ihr jeden Tag wechselnde Titel hier zu lesen.

Ausserdem sollten wir wieder dazu übergehen aussichtsreiche Titel zu nennen , manche lesen einfach nur und geben hier weder Infos über Werte die sie haben noch über werte die sie gerne hätten ?

"Aus meiner Sicht würde der Ausschluss von JC, auch in Kombination mit Getgo, zu einem Qualitätsverlust für das Forum führen. Ich plädiere daher eindringlich für Wiederaufnahme."

Erstens Getgo ist nicht gesperrt wird sich hier wahrscheinlich trotzdem nicht mehr äußern, das hat aber nichts mit Jacky zutun (Vermutung),könnte er aber jederzeit machen.

und wenn jemand News von Jacky über die zwei Werte hören will, nichts einfacher als das

https://www.ariva.de/forum/...hstoffallrounder-576624?page=0#jumppos7

https://www.ariva.de/opawica_explor-inc-aktie

Das sind die Orte die mir am logischsten erscheinen.

Ich finde es krass wie es einige aufregt wenn es einem nicht mehr gestattet wird hier zu schreiben , aber ansonsten keine Beiträge kommen.

"Ich plädiere daher eindringlich für Wiederaufnahme."

abgelehnt !

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Gold |

Blödsinn muss man auch mal aushalten! Ich muss nicht jede Meinung teilen. Don't feed the troll...

Ignore ist voellig ausreichend..

Aber ist ja dein Thread!

Schade ist es trotzdem...

Du hast es mit den posts von Brennstoffzellenfan verglichen; dies ist objektiv falsch. Wie geschrieben, meldet JC hier News von OPW und Origen und nicht nur Hurra-Kursentwicklungen. Letztere meldest auch Du und ich zu einzelnen Werten - und das ist völlig in Ordnung. Wir leiden hier zusammen, dann sollten wir uns auch gemeinsam freuen können. Zur Performance: Ich bin bei beiden Werten dick im Plus (OPW 120%; Origen + 60% - habe bei Origen die Hälfte aber schon mit 100% verkauft) und bin keineswegs zu Pre-IPO-Kursen eingestiegen.

Du glaubst doch nicht im Ernst, dass man durch die Nennung von Werten in diesem Forum den Kurs "pushen" kann. Dann sind wir ja alle "pusher" - nun gut, halt nicht so einseitig.

Ja, das Forum sollte viele Werte thematisieren; dies tut es ja auch, unabhängig von JC. Also, wo ist das Problem, wenn sich manche auf wenige Werte konzentrieren?

JC und Getgo bringen hier einen anderen, interessanten Investmentansatz rein - neben der PP-Thematik (die wir hier leider auch nicht mehr drin haben) interessiert mich zumindest immer noch, ob die Konzentration auf wenige Werte, die mit Insiderwissen ausgesucht werden, nicht weitaus erfolgsversprechender ist. Ich habe keine Lust, mich in zahllosen Spezialforen rumzutreiben, sondern schätze dieses Forum aufgrund seiner Vielfalt.

Optionen

| Boardmail an "Katzenpirat" |

Wertpapier: Gold |

Optionen

| Boardmail an "Katzenpirat" |

Wertpapier: Gold |

Wir haben nun bereits: Goldkinder, Goldkind, Golden Child, Goldinder, Child, Goldfinder, Holdkinder. Ich hoffe, du fasst das nicht als Beleidigung auf...

Optionen

| Boardmail an "Katzenpirat" |

Wertpapier: Gold |

https://www.youtube.com/watch?v=lfTYX_b3ye0

Jeder preferiert irgendwie seine eigenen Werte.

Nach ner gewissen Zeit kann man diese Beiträge ja einordnen.

Sei es steppe, origen, sienna, was auch immer.

Ob man da jetzt ne Sperre unbedingt aussprechen muss?

Im Endeffekt hat der admin sein Hausrecht in den Foren und muss das selbst entscheiden.

Schönes Wochenende euch

Trotz Kapitalerhoehung 34% plus bei den Aussies.

Der Staat Victoria gibt e einfallslos Geld...

https://www.youtube.com/watch?v=E-8FYpusTYg

AISCdeutlivj höher als im letzten Jahr.was ich gut findendes manin Zukunft auf der Plant Zinc und Leadwird verarbeiten können. Das sollte zusätzlich Einnahmen generieren und kann die AISC wieder senken .

Gran Colombia Announces Third Quarter and First Nine Months 2021 Results https://seekingalpha.com/pr/...s-2021-results?source=copyToPasteboard

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Matt Bohlsen profile picture

Matt Bohlsen

Marketplace

Bio

Follow

https://seekingalpha.com/author/matt-bohlsen#regular_articles

Portfolio Strategy, Growth At A Reasonable Price

Contributor Since 2015

I hold a Graduate Diploma in Applied Finance and Investment (similar to CFA), and a Graduate Diploma in Financial Planning.

I have 31 years of personal investing experience, and 21 years of professional financial advising experience. As a global investor I use a macro thematic approach searching for good value and/or high growth. I search the globe for great investments with a focus on "trend investing" themes. Some trends I currently follow include the rising Asian middle class, electric vehicles and the lithium/cobalt/graphite/nickel/copper/vanadium miners, battery and plastics recycling, the online data boom, 5G, IoTs, AI, cloud computing, cryptocurrency/bitcoin, renewable energy, energy storage (including vanadium), space tourism, 3D printing, personal robots, and autonomous vehicles.

I also love to invest in income producing investments that can grow over time and benefit from compounding, or help fund retirement income.

I host a Marketplace Service called Trend Investing. Potential new subscribers can learn about my Seeking Alpha Trend Investing subscriber service from the links below:

"The Trend Investing Difference" - Click here.

"Subscriber Feedback And A Sneak Peak At My Personal Portfolio Performance From Last Year (2020) And Current Holdings" - Click here.

Summary

DLE uses various methods to accelerate the lithium extraction process, typically from lithium brines. Advantages and disadvantages of DLE.

A brief summary of some DLE companies.

A look at some of the key lithium companies trialing or planning to use DLE and my top picks.

Lithium as Element 3 of the Periodic Table 3D animation on blue background

remotevfx/iStock via Getty Images

This article first appeared in Trend Investing on October 12, 2021; but has been updated for this article.

Direct Lithium Extraction ("DLE")

DLE is the latest trend in extracting lithium and it typically competes with the traditional process of using brine ponds and an evaporation process. The large scale economics of DLE are still uncertain; however for now it appears to be carving out a niche place for lower grade brine projects, geothermal brine projects, and petroleum brine projects.

Conventional evaporation and DLE processes

Source: Lithium South Development Corp. website

The key advantages include:

Faster lithium production (takes a matter of hours/days rather than 1 year via evaporation ponds).

Much smaller environmental footprint as no need for a huge area of evaporation ponds, hence a more favorable ESG profile.

Not weather dependent.

Lower water consumption (the brine is returned to the salar after the lithium is extracted).

Potential to make low grade lithium projects economically viable.

Up to 99% lithium recovery (usually 70-90%) compared to ~40% with the conventional process.

Can potentially produce a higher purity battery grade lithium final product that sells at a premium to lower grade.

The key disadvantages include:

Not yet tested at a large scale and over a long time period. This means that the economics and effectiveness over time are still to be determined.

Technical complexity - Several choices in the type of DLE that can be used and risks involved with newer technology.

Initial CapEx may be higher and ongoing CapEx may be higher, depending upon the project. This depends on many factors (location, type of DLE process, cost of energy, any valuable by-products, geothermal benefits etc).

Source: Lithium South Development Corp. website and other sources

3 main types of DLE

Lithium bonding (Adsorption)

Ion exchange

Solvent extraction

The National Renewable Energy Laboratory (NREL) state:

DLE technologies can be broadly grouped into three main categories: adsorption using porous materials that enable lithium bonding, ion exchange, and solvent extraction. Scaling up any of these techniques to full production capability remains a challenging task. For example, developing a solid material that bonds with just lithium is a huge challenge in geothermal brine that contains many minerals and metals. Successful DLE implementation will depend on expanding innovation and creating new technologies.

Technical details of the 3 different types of DLE processes

Source: E3 Metals company presentation courtesy of Jade Cove partners

A brief summary of some Direct Lithium Extraction companies (in alphabetical order)

Adionics (private) - Some details here.

Beyond Lithium (private) - See Alpha Lithium below.

E3 Metals Corp. - See below as they also have a lithium project.

EnergySource Minerals (private) - Some details here.

Eon Minerals (private) - Some details here.

Lilac Solutions (private) - Backed by Breakthrough Energy Ventures (founded by Gates, and includes many billionaires) and others, Lilac has developed materials called ion-exchange beads for lithium extraction. Well financed and a leading contender in DLE. See Lake Resources (below) as they have a deal with Lilac.

MGX Minerals [CSE:XMG](OTCPK:MGXMF) - A very low market cap Canadian company that has a cleantech process to separates minerals, heavy metals and hydrocarbons from wastewater brine pumped to the surface during oil and gas operations. Some details here.

POSCO [KRX:005490] (PKX) - South Korea's steel giant, POSCO, plans to boost its lithium production capacity in Korea (LiOH conversion plant) and Argentina (from the Salar del Hombre Muerto, Argentina) to 220,000 tpa by 2030. They also plan to boost annual production capacity of cathodes to 100,000 tons by 2023. They have been a bit secretive regarding their DLE plans, but are definitely working in the space. POSCO has a 2021 PE of just 3.60 (div. yield of 5.60%) and a consensus price target of KRW 436,500. Note that steel making is the main source of their revenues for now and this sector is currently impacted by China property related issues.

Simbol Materials (private) - Involved with DLE at a developing geothermal power plant by the Salton Sea.

Schlumberger NV (SLB) - Schlumberger New Energy (NeoLith Energy) - In March the Company announced plans to launch a DLE pilot plant in Nevada, working with Pure Energy Minerals [TSXV:PE] (OTCQB:PEMIF). Schlumberger recently announced that they were collaborating with Panasonic [TYO:6752] (OTCPK:PCRFY), who of course supply Tesla (TSLA) batteries at Giga Nevada. More details on Schlumberger New Energy here. Details on Pure Energy Minerals here. Details on Schlumberger's right to acquire 100% of Pure Energy's Clayton Valley Project here.

Tenova Advanced Technologies (private) - A top tier company with expertise in DLE. Some details here.

The above companies could be the topic of a separate article; however it should be noted that most are private and so not usually accessible for most investors.

Lithium companies trialing DLE (in alphabetical order)

Alpha Lithium [TSXV:ALLI][GR:2P62] (OTCPK:APHLF)

Alpha Lithium 100% own 27,500 hectares of the Tolillar Salar, in Argentina and has recently announced an option to acquired 985 more hectares (now have 5,072 hectares) at one of the leading salars in Argentina, Hombre Muerto. CEO & President, Brad Nichol, commented: “Following on the heels of our previous announcement, whereby we produced Lithium Hydroxide and Lithium Carbonate from the nearby Tolillar Salar, we have firmly established ourselves as a major player in Hombre Muerto." More details here.

Regarding the Tolillar Salar, Alpha Lithium state: "Concentrations were identified up to 504 mg/L in borehole samples in 2015 study....from limited previous testing on <10% of claim area."

The Company has been testing their in-house developed DLE process (developed by the principals of Beyond Lithium) and has achieved some great results including lithium concentrations of 9,474 mg/L with significant rejection of impurities. Alpha Lithium is also trialing DLE with Lilac Solutions.

The next stage will be growing a potentially sizable resource at one, or both, of their nearby salar tenements (Tolillar Salar and Hombre Muerto salar).

Alpha Lithium trades on a market cap of C$126m and as of June 2021 had C$34.2m in cash. Looks promising but very early stage and has been rather slow in developing a resource.

Alpha Lithium company presentation

Location map showing the Tolillar salar to be well located in Argentina

Source: Alpha Lithium website

E3 Metals Corp. [TSXV:ETMC] (OTCPK:EEMMF)

E3 Metals has developed their own DLE technology with an aim to use it on their flagship Clearwater Project in Alberta, Canada. E3 Metals has 3 resources across their Alberta Lithium permit area hosted in the Leduc Aquifer (Clearwater, Rocky, Exshaw), together totaling 7.0m tonnes of contained LCE with grades ranging from 52.9 to 75mg/L lithium.

E3 Metals’ Direct Lithium Extraction (DLE) technology obtains over 90% recovery and drastically increases the concentration of lithium, while reducing impurities by over 99%. More details here.

E3 Metals state:

E3’s DLE ion-exchange technology utilizes a proprietary sorbent designed to be highly selective towards lithium ions. It quickly and efficiently reduces large volumes of low-grade brine into a high-grade lithium concentrate in one step, simultaneously removing nearly all impurities.

E3 Metals DLE explained

Source: E3 Metals Corp. website

The Clearwater Project PEA resulted in a post-tax NPV8% of US$819.9m and 27% IRR, over a 20 year project life. Initial CapEx is estimated at US$602m and OpEx at US$3,656/t.

The Project is now in the pilot testing stage with a target to achieve 20,000tpa+ lithium hydroxide production by 2025-26.

Summary of the Clearwater Project PEA economics

Source: E3 Metals website

E3 Metals trades on a market cap of C$170m. Looks quite cheap, but the CapEx is high for only a 20,000tpa project.

E3 Metals company presentation

E3 Metals factsheet

Lake Resources NL [ASX:LKE] [GR:LK1] (OTCQB:LLKKF)

Lake Resources own the Kachi Lithium Brine Project in Argentina and some others (Cauchari, Olaroz, Paso, Catamarca), covering a total of 2,000 sq km (100% owned) in Argentina. Details here. Lake Resources has been working with Lilac Solutions Technology (private, and backed by Bill Gates) for direct lithium extraction and rapid lithium processing.

Lake Resources and Lilac Solutions (private) recently announced a partnership where Lilac Solutions can earn in up 25% of the Kachi Project in Argentina plus would then contribute US$50m to develop Kachi (the US$50m is equivalent to Lilac’s pro-rata share of future development costs). Lilac’s process has been found to generate lithium recovery rates of 80-90% and is able to produce a high purity 99.97% lithium carbonate product.

Lake Resources presentation - Lilac Solutions Partnership To Develop Kachi Lithium Project

Lilac Solutions process to be used at the Kachi Project

Source: Lake Resources presentation

The Kachi lease covers 740 sq km in Argentina. Kachi has a Total JORC resource of 4.4Mt LCE (Indicated 1.0mt & Inferred 3.4mt) at an average grade for the Indicated Resource of 289mg/L. While this is quite low, that is where the DLE comes in to more efficiently extract the lithium. Lake Resources has and an exploration target ranging between 8-17Mt of LCE at Kachi.

The Kachi PFS based on 25,000tpa LCE resulted in a post-tax NPV8% of US$1.58b and 35% IRR. Initial CapEx was estimated at US$544m and OpEx at US$4,178/t LCE.

2020 Kachi Project PFS summary (100% project share basis)

Source: Lake Resources presentation

Lake and Lilac are currently working on the pilot and demo plant at Kachi and the DFS and Environmental and Social Impact Assessment ("ESIA").

In terms of raising the US$544m initial project CapEx, Lake Resources should have ~US$50m (from the 25% project share JV with Lilac) and has a 70% debt funding 'expression of interest' for the Kachi development using a loan from the UK Export Finance (Export Credit Agency) at favorable rates.

All going well production is targeted to begin in 2024 and to scale very rapidly to 25,500tpa and then 51,000tpa LCE.

Lake Resources has a market cap of A$1.216b. Fast moving company and one to watch but looks fully priced for now.

Lithium South Development Corp. [TSXV:LIS] (OTCQB:LISMF) (formerly NRG Metals Inc.)

Lithium South has tenements of 3,287 hectares (under purchase option) known as the Hombre Muerto North ("HMN") Project which lies just north of the POSCO [KRX:005490] (PKX) and Orecobre [ASX:ORE] (OTCPK:OROCF) (from Galaxy Resources - Sal de Vida) projects, and near Livent's (LTHM) lithium mine in the Salar del Hombre Muerto, Argentina. Of note, POSCO paid Galaxy resources US$280m for the Galaxy northern tenements and resource (M&I 1.58 mt LCE).

For now the resource is not yet very big at M&I Resource of 571,000t contained LCE, but the grade of 756mg/L is very good, as is the very low Mg/Li ratio of 2.6:1. There is still plenty of potential exploration upside or as the Company recently stated: "Pending drill confirmation and resource expansion, the project size will potentially expand significantly." The salar is a proven salar with Livent producing there already.

Lithium South is trialing DLE technology in parallel with proven evaporation technology. Their environmental baseline study is also underway.

Lithium South state: "Lithium South is evaluating DLE from three different sources:

Chemphys is developing their process in Chengdu, China using an absorbent.

Eon Minerals, located in Salta, Argentina, is also developing a process using their patent pending absorbent.

Lilac Solutions of Oakland, California USA is developing an ion exchange process for rapid lithium extraction."

"All three will be testing their technology on a bulk sample of HMN Li Project brine. The technology with the best result will move forward to the pilot plant stage. Lithium South’s DLE technology potentially cuts capital and operating costs, accelerates project startup, boosts lithium recovery, and reduces the production time from years to hours. Our DLE process will be modular and can be ramped up quickly through pilot and commercial projects. The technical goal will be to lower water consumption, reduce the project footprint and thereby, potentially minimize ecological impact."

Doubling of Lithium Recovery from Brine with Chemphys Process

Lilac Solutions achieves 99% lithium recovery with Ion Exchange Process

Eon Minerals Inc. to Evaluate HMN Brine using Direct Lithium Extraction Technology

The Hombre Muerto North Project PEA (based only on the Tramo tenements of 383 hectares) resulted in a after-tax NPV8% of US$217m and 28% IRR, based on 5,000tpa lithium carbonate production over a 30 year mine life. Initial CapEx was estimated at US$93.3m and OpEx at US$3,112/t lithium carbonate.

Lithium South is currently working to expand the resource following some good TEM study results. On October 4, 2021 the Company stated:

The Tramo claim block is the most advanced and is the subject of both a resource calculation and Preliminary Economic Assessment. The balance of the property package has not been significantly evaluated to date......Management is taking a fast-track approach to moving the project to a full feasibility study, with an Environmental Impact Report currently underway. Permissions to drill have been applied for and are expected in the immediate future.

Lithium South trades on a market cap of C$60m. The stock looks to be cheap and a good spec buy. Their grades are very high so can choose between conventional evaporation and DLE or a combination of both. I view Lithium South as a potential takeover target given the very low market cap and strategically located asset at the HMN Project in the premium salar of Hombre Muerto. One of the very best.

Note: The 2021 stock price slide may be due to an auditor's 'ongoing concern' warning on April 30, 2021 for the period ending Dec 31, 2020; however most junior miners have this risk of needing to regularly raise capital. In March 2021 Lithium South completed the second to last property payment.

Lithium South Factsheet

Lithium South company presentation

Source: Lithium South company presentation

Standard Lithium [TSXV:SLI] (SLI)

Standard Lithium developed as a lithium extraction company with their own DLE technology and is now considered a leader.

Standard Lithium's flagship project is the 150,000+ acre Lanxess Joint Venture Arkansas Smackover Project, located in the Smackover brine region of southern Arkansas. They also own the early stage Bristol and Cadiz Dry Lake lithium brine project located in the Mojave Desert, California.

At the Arkansas Smackover Project, Standard Lithium has JV'ed with Lanxess who own the largest brine processing facility in North America (focused on bromine extraction). The Lanxess JV includes project finance, off-take and operations commitment. The 70/30 JV is in favor of Lanxess AG with an option for Standard Lithium to achieve 40% subject to attaining certain milestones.

The Project has an Indicated Resource of 3.14 million tonnes contained LCE.

The 2019 Smackover Project Preliminary Economic Assessment (100% project basis) resulted in a post-tax NPV8% of US$989m. Initial CapEx based on a 20,900 tpa project is US$437m and the OpEx is $3,107/t over a 25 year mine life. Note that the Phase 1 CapEx is just US$171m just to get the project into production.

Standard Lithium has an expansion target to reach 70,000+ tonnes/year battery quality lithium carbonate.

The Project has an operating demonstration plant and uses Standard Lithium’s proprietary technology utilizing a solid sorbent material to selectively extract lithium from Lanxess South Plant’s tail-brine. The demonstration plant is currently being used for proof-of-concept and commercial feasibility studies.

Standard Lithium is not cheap and trades on a market cap of C$1.74b.

Standard Lithium DLE extraction technology attaches next to the Lanxess brine bromine facility in Arkansas, USA

Source: Standard Lithium company presentation

The geothermal lithium miners that plan to use DLE

For details on the geothermal miners using DLE you can read my past article:

A Look At The Geothermal Lithium Sector And Some Miners

Key names include Controlled Thermal Resources (private)/ Lilac Solutions (private), Simbol Materials (private), Cornish Lithium (private) and Cornish Metals [TSXV:CUSN][AIM:CUSN], GeoLith SAS/GeoCubed (JV between Cornish Lithium Ltd and Geothermal Engineering Ltd (GEL)), and Vulcan Energy Resources [ASX:VUL] (OTCPK:VULNF).

Some companies with lithium extraction technology for lithium spodumene, other lithium hardrock or tailings

Neometals [ASX:NMT] (OTCPK:RRSSF) - Neometals (70%) and Mineral Resources [ASX:MIN] (OTCPK:MALRF) (30%) have jointly developed a patented technology to purify and electrolyse lithium chloride to produce lithium hydroxide in a direct process direct from hard rock resources. It is called the ‘ELi’ process. Neometals also 100% own their Dexter direct extraction process which can be used on lithium brine projects.

Lithium Australia [ASX:LIT] (OTCPK:LMMFF) - Developed SiLeach® for lithium extraction from a wide range of lithium feedstock (typically from lithium hardrock mica/waste).

Lepidico [ASX:LPD] - Developed L-Max technology to get lithium from lithium mica.

Risks

Macro risks. Lower EV sales. Lower lithium prices.

DLE is a new technology and the economics at scale are still uncertain. Smaller scale operations appear to work well.

DLE may prove to be a more expensive way to extract lithium than conventional evaporation. For now it does appear that the lower grade lithium projects are those that are really embracing DLE.

DLE may lead to lower lithium brine concentrations over time as the lithium-extracted brine is returned to the salar causing some dilution. More details here.

The usual mining risks (funding, exploration, development, permits, production, partner, cost blowouts etc). Plus additional risks associated with new DLE technology.

Business risks - Debt, management, liquidity, and currency risk.

Sovereign risk - Very low in Australia and Canada, moderate in Argentina.

Stock market risks - Dilution, lack of liquidity (best to buy on local exchange), market sentiment.

Further reading

Standard Lithium CEO hopes for more extraction projects in Arkansas to help U.S. EV industry (Cramer video)

Direct Lithium Extraction Technologies (long technical video)

Conclusion

DLE is a relatively new trend in the lithium mining sector. This means it is yet to be tested at large scale and the large scale economics are still to be determined. At smaller scale DLE is looking effective and quite promising. It should be noted that those most embracing DLE generally have low grade lithium resources or are geothermal lithium miners also with low lithium grades.

Investors can look to buy the companies that are developing and aiming to commercialize the DLE technology, the lithium miners that plan to use DLE, or those that have their own DLE technology plus lithium project. This article has mostly focused on the latter two categories as these companies are generally listed and have the potential to benefit if the DLE technology scales well.

The leading DLE companies with lithium projects are POSCO, Standard Lithium (JV with bromine producer Lanxess who provides the brine) and Lake Resources (JV with Lilac Solutions who provides the DLE technology). These companies already trade on rather high market caps but look to be lower risk and closer towards lithium production.

The more junior lithium companies potentially with DLE plans include Alpha Lithium, E3 Metals, Lithium South Development Corp., and Pure Energy Minerals. All have lower market caps due to their earlier stage and generally smaller resources, noting E3 Metals is an exception with 7.0m tonnes of contained LCE.

Added to this are the geothermal miners who are really primarily geothermal energy plays with some potential lithium revenues as a boost.

At this stage it is quite hard to decide on a top pick given the added layer of risk due to lower lithium grades and the uncertainties of DLE economics at scale. Given this I would view the sector as speculative and size investments accordingly.

My top picks would be one of the lower market cap DLE/lithium stocks (Alpha Lithium, E3 Metals, Lithium South Development Corp., Pure Energy Minerals) due to the high reward nature potentially balancing out the high risk. Of these four I would choose Lithium South Development Corp. as they are a low market cap junior with a quality resource location with high grade lithium. Schlumberger has some extra intrigue given the recent Schlumberger/Panasonic collaboration in Nevada, not far from Tesla's battery gigafactory.

A Look At Direct Lithium Extraction ("DLE") And Some Of The DLE Lithium Companies https://seekingalpha.com/article/...companies?source=copyToPasteboard

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Gold |

Angehängte Grafik:

febc576b-9db6-4f98-bfbc-cec1cae6b74b.jpeg (verkleinert auf 22%)

febc576b-9db6-4f98-bfbc-cec1cae6b74b.jpeg (verkleinert auf 22%)

Fortuna’s San Jose silver mine in Mexico faces closure due to expired permit

https://www.mining.com/web/...ico-faces-closure-due-to-expired-permit

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Gold |

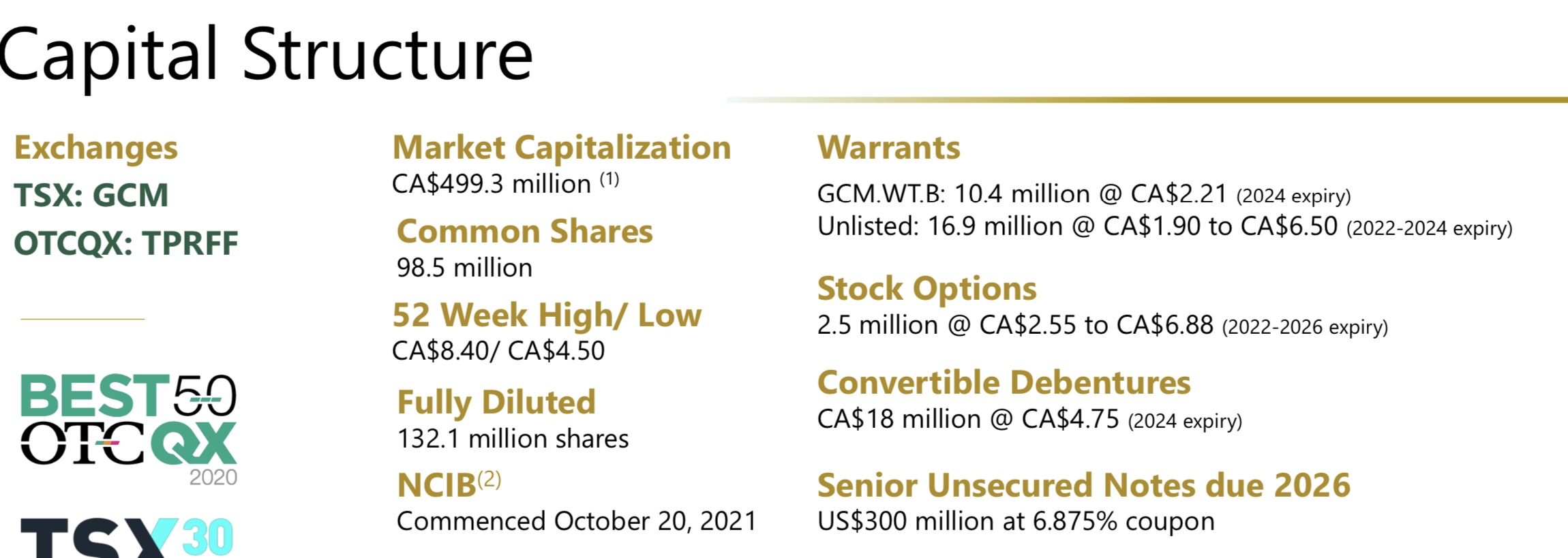

Wir dürfen nicht vergessen das mittlerweile ja immer auch Aktien zurück gekauft werden. Des weiteren dnek ich mir das wenn Sie ein Mittelgroßerproduzent sind und die Preise noch so hoch sind, Sie deutlich mehr Aktien zurück kaufen können und so die Aktienanzahl wieder Richtung 100 Millionen Sahres zurück führen können.

Des weiterenc sind die Kursziele der Analysten viel höher und reichen von 8 cad bis zu 14 cad. Davon sind wir jetzt noch meilenweit entfernt. Wir sind aktuell viel zu günstg bewertet und das auch objektiv.

Bezüglich Segovia gibt es Wachstumspotential durch eine höhere Verarbeitungsanlagein der Zukunft und dazu ist das Gebiet in Teilen immer noich unexploriert sowie gibtc es viel mehr Venen die unberührt sind.

Auch kommt in Zukunft noch die Verabeitung von Zinc und Lead dazu. Aber klar der Haupttriber sollte Toparu sein. Wenn alles einigermaßen im Plan und Budget durchgeführt wird bekommen wir automatisch eine Neubewertung.

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

Sehr ausführliche und lesenswert. Das Kursziel ist unglaublich von heute aus gesehen. Über 67 US Dollar.

Mit diesem Kursziel würde man reich werden können.

Sibanye Stillwater: Strong Upside Regardless Of Metal Prices https://seekingalpha.com/article/...al-prices?source=copyToPasteboard

Optionen

| Boardmail an "Alfons1982" |

Wertpapier: Gold |

https://themarketherald.com.au/asx-lmg/

https://seekingalpha.com/news/...eed_news_all&utm_medium=referral

Optionen

| Boardmail an "Balu4u" |

Wertpapier: Gold |

CopAur Discovers New 1000 Metre Trend of Surface Mineralization and Samples 6.88 g/t Gold

Vancouver, British Columbia--(Newsfile Corp. - November 11, 2021) - CopAur Minerals Inc. (TSXV: CPAU) ("CopAur" or the "Company") is pleased to report results from its 2021 soil program designed to confirm surface mineralization within the historic T-Bill gold zone, as well as provide reconnaissance sampling of surrounding prospective areas on its 100% owned Williams Copper-Gold Project. As a result of the reconnaissance soil and rock sampling program the Company has discovered a new north-trending zone of surface mineralization that extends ~1000 metres in strike-length and is located ~1.1 kilometres west of historic gold-in-soil anomalies (Figure 1). Within this new north-trending mineralized zone soil samples typically assayed up to 320 ppb gold (Au), with one sample assaying up to 6.88 g/t gold and that the rocks samples along the SE trending anomaly zone away from the drilling match in vein style as the TBILL.

https://ceo.ca/@newsfile/...000-metre-trend-of-surface-mineralization

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Gold |

Optionen

| Boardmail an "Bozkaschi" |

Wertpapier: Gold |