Aixtron purpose of this thread

Free cashflow:

Aixtron hat in H1 die Vorräte stark aufgebaut, auch wegen der Exportlizenzen. Dies sollte sich in H2 m.E. normalisieren, gilt es jedoch kritisch zu beobachten. Ich halte Aixtron jedoch für ein starkes FCF Unternehmen, zudem rd. 340 Mio € Cash in der Firmenkasse (rd. 3 € je Aktie). Keine Schulden.

mit Investitionen von bis zu € 100 Millionen in das Reinraum-Forschungszentrum wird es mMn schwierig mit der FCF Erholung in Q 3 und 4 2023.

Aixtron hat übrigens einen 2D product manager im Januar 2023 eingestellt. https://www.linkedin.com/in/salim-el-kazzi-ab96b864/

Gruß

baggo-mh

baggo-mh

Optionen

vergleiche Post #1410

Innovationszentrum:

100 Millionen sind nur für die Hülle, ohne Maschinen und Techniker gedacht.

Laut Kim Schindelhauer sollen dort einmal 50 hochqualifizierte Physiker arbeiten.

Baubeginn: 2023

Fertigstellung: Ende 2024

Es sollen neue Produktgenerationen entwickelt und Schulungen (extern und intern – Servicetechniker) durchgeführt werden.

Hatte ich irgendwie anders (Ende 2023) abgespeichert.

Gruß baggo-mh

Optionen

COO - another Dr. Jochen Linck

joined in October 2020 - exit Sept. 2023. 3 Year contract not renewed.

My take on this:

If in the next 12 months he does not show up elsewhere - it was family related/personal.

Otherwise it was a disagreement on something between him and Aixtron, terms of renewal, strategy etc.

At the AGM he left a very subdued impression to me......no wonder as his demise was published on the same day.

Your info - field service technician Texas (Sherman Globitech): fits well to this info from the AGM: Kunden schließen Serviceverträge für Stand-by service technicians ab. Zum Teil 24/7 standby und onsite. 5-6 Reaktoren pro Service technician.

Still no stars from me possible as I gave you too many already

Best regards baggo-mh

Optionen

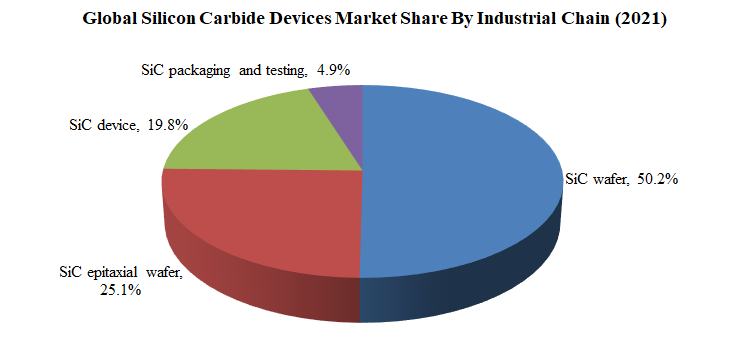

Expitaxy is or was 50% of substrate (wafer) in 2021.... in terms of value creation.

15,1% CAGR from 2022 to 2027......

https://www.hdinresearch.com/news/199

Gruß

baggo-mh

baggo-mh

Optionen

Third-generation semiconductor trend · 2023-09-19

Recently, another SiC company announced mass production and has laid out a 700 million yuan epitaxial wafer project. It is expected that SiC substrate + epitaxial revenue will increase 10 times this year.

On September 18, according to Aixtron’s official website, they have reached a cooperation with GlobiTech, a wholly-owned subsidiary of Sino-American Crystal. GlobiTech will purchase epitaxy equipment G10 to enter the SiC epitaxy field.

According to data, GlobiTech was established in December 1998 and is one of the world's largest silicon epitaxial wafer foundries. The company was originally a division of Texas Instruments, but was acquired by Sino-American Crystal many years ago

In 2008, Sino-American Crystal acquired 100% of the equity of GlobiTech for US$45 million in cash to realize the independent production process of crystal growth, slicing, grinding, polishing and epitaxial production; and in 2011, it separated the group's semiconductor business and established Globalwafers , GlobiTech is now part of Globalwafers.

According to previous reports by "Experts Say Three and a Half Generations", in the past two years, GlobiTech has begun to expand its SiC business and transition to the emerging silicon carbide market:

In March 2022, Globalwafers proposed to invest NT$100 billion to expand production. One of the plans is to expand the production of silicon carbide epitaxy at Globitech.

In May this year, GlobiTech received an investment of US$2 million (approximately RMB 13.99 million) from the Sherman, Texas (KTEN) Economic Development Corporation. This funding will help GlobiTech achieve a total investment of US$100.5 million (approximately RMB 703,000). billion) expansion plan to produce silicon carbide epitaxial wafers.

Currently, GlobiTech has begun mass production using G5WW C and G10-SiC systems, and will continue to expand installed capacity in the next few years and supply SiC substrates and SiC epitaxy to the market. Known customers include Texas Instruments and Intel.

Globalwafer's silicon carbide business model is similar to Resonac (formerly known as Showa Denko). In addition to epitaxy, they also make their own silicon carbide substrates.

In March 2022, Xu Xiulan, chairman of Sino-American Crystal, said that Globalwafer's monthly SiC substrate production capacity at that time was about 2,000 pieces. Due to very strong customer orders, they planned to expand their monthly production capacity to 5,000 pieces in 2022, which is expected to reach 5,000 pieces by the end of 2023. On 10,000 pieces.

In March 2023, SiC business only accounted for about 3% of Globalwafer's revenue. In August this year, Xu Xiulan revealed that their SiC performance this year will be at least 10 times that of last year.

https://www.hangjianet.com/topic/1695076680040

as stated n #1106, GlobalWafers is planning to eventually reach 1 million SiC epi wafers annual capacity according to the CEO.

Current 2023 FCF consensus is 89m.

If Aixtron hits a NVWC/REV ratio at 0.6, Its FCF would be about 70m.

The underlying assumption is that Aixtron's would be able to digest its inventory so the NCWC goes down from the current high level . It is certainly possible that Aixtron could at least meet a ratio of ~0.6.

The FCF model here is the classical calculation excluding some of the other factors that Aixtron uses in its FCF formula, but the key ingredients are the same. That is FCF = EBIT X (1-TAX RATE) + (DA-CAPEX) + change in NCWC.

as stated n #1106, GlobalWafers is planning to eventually reach 1 million SiC epi wafers annual capacity according to the CEO.

Not sure if you did the numbers too, but I just did. With the new G10 SiC and 6 hours per run and no down time in between it would take:

1 Millionen/4 runs per day/365 days/6 wafers 200mm per run = 76 Aixtron tools

or

1 Millionen/4 runs per day/365 days/9 wafers 150mm per run = 115 Aixtron tools

Wooow......stunning numbers.......just for one customer

Gruß baggo-mh

Optionen

https://www.deraktionaer.de/artikel/aktien/aktionaer-depotwert-aixtron-besser-als-der-wettbewerb-20339670.html

Nicht Neues nur reduzierter Gewinn seit Depotaufnahme.

Gruß baggo-mh

Optionen

Im Bereich SiC tut sich einiges.

ASM International hat LPE übernommen. Die Tabelle zeigt das aber irgendwie nicht.

Veeco hat Epiluvac einkassiert.

Zeigt wie schwierig es ist die Technology selbst zu entwicklen und wie heiß umkämpft der Markt gerade ist.

Epiluvac’s modular design of its SiC equipment will also allow Veeco/Epiluvac to compete with the major players in this area. The cluster-based approach of its machine allows up to 4 wafer reactors to be plugged in at once to increase throughput. This design element distinguishes the machine from some of its direct competitors – particularly Tokyo Electron and NuFlare, which are more “traditional” in their approach with a two-chamber type equipment while Aixtron remains the only major equipment manufacturer to offer SiC planetary reactors.

Quelle: https://www.yolegroup.com/strategy-insights/...wards-silicon-carbide/

Gruß baggo-mh

Optionen

Silicon carbide epitaxy market, the market trends we see

Original Silicon carbide core observation2023-09-19 20:55117

September 18 – AIXTRON announced that it will support GlobiTech Inc., one of the world’s largest silicon epitaxial wafer foundries, to expand its business into the silicon carbide (SiC) epitaxy field. AIXTRON's new equipment G10 will accelerate GlobiTech's increase in SiC epitaxy production to meet the growing global demand for power epitaxy wafers.

This news also quickly attracted market attention in the industry. As GlobiTech joins hands with AIXTRON to enter the silicon carbide epitaxy market, we can see that the industry is changing:

A clear signal of long-term trends in the silicon carbide

Increasing production and reducing costs will be the mainstream of the market

For a long time, the epitaxial equipment in the domestic silicon carbide market has been dominated by single-wafer furnaces with high stability and simple operation. The representative model is the Pe106/108 of the Italian LPE company. This machine can realize automatic loading and unloading of wafers at high temperatures of 900°C. The main features are high growth rate, short epitaxial cycle, good consistency within the chip and between heats, etc., and it has the highest market share in the domestic market.

In the domestic market, companies such as Jingsheng Electromechanical, China Electronics Technology Institute 48, Northern Huachuang, and Nashe Intelligence have all developed monolithic SiC epitaxy equipment with similar functions and promoted large-scale applications. The horizontal epitaxy of the above four companies The furnaces have been shipped on a large scale.

According to InSemi's incomplete research and comprehensive market information from various companies, with stable and reliable process performance, the domestic monolithic furnace market stock has accumulated to more than 450 units . In addition, each company still has a large number of orders to be delivered. It can be said that single-chip computers are still the mainstream in the current market.

However, with the gradual increase in downstream applications, the pace of domestic and foreign silicon carbide production capacity expansion has accelerated, and the demand for silicon carbide epitaxy expansion has further increased. There have been more than 15 epitaxy projects in the domestic market alone.

As the demand for production expansion increases, the shortcomings of the output capacity of single-chip microcomputers gradually become apparent. According to LPE, the monthly production capacity of microcontrollers is only 350 pieces/month. Therefore, the market is also constantly exploring other technical routes to improve production capacity.

G10 came into being, a new epitaxy system launched by AIXTRON in September 2022. It is understood that this high-temperature CVD system is a 150/200 mm high-throughput epitaxial equipment (dual wafer size batch reactor) for the SiC market.

So what are his advantages?

G10-SiC new platform

Supports dual wafer sizes: 150 mm and 200 mm

Highest wafer throughput/square meter on the market

Lowest cost/wafer on the market

Excellent run-to-run process performance

Highly uniform, low-defect SiC epitaxy process to achieve maximum chip yield

Efficient SiC substrate basal plane dislocation (BPD) conversion

The new platform is built around AIXTRON’s proven automated cassette-to-cassette loading solutions and high-temperature wafer transfer. Combined with high growth rate process capabilities, G10-SiC provides best-in-class wafer throughput and throughput per square meter to efficiently utilize limited cleanroom space in semiconductor fabs.

To put it simply, G10 is produced for large-scale mass production of silicon carbide epitaxial wafers.

Of course, in addition to G10, the progress of quasi-hot wall vertical CVD systems this year has also attracted market attention. According to Xinsandai, a domestic mass manufacturer of quasi-hot wall vertical CVD systems, the company has closely combined processes and equipment to develop SiC -CVD equipment is designed in aspects such as temperature field control and flow field control to achieve high productivity, 6/8-inch compatibility, COO cost, long-term continuous automatic growth control for multiple furnaces, low defect rate, maintenance convenience and reliability, etc. It has obvious advantages in all aspects.

Based on the current diversification of epitaxy technology routes, we can also see several trends:

1. Substrate costs are gradually decreasing

Previously, in the early days of the industry, the main reason why AIXTRON machines were not widely adopted by the market was not only the high price of the machines themselves, but also the fact that multi-chip machines had certain process difficulties and were difficult to operate, which easily resulted in the failure of one epitaxial wafer in a multi-chip furnace. The problem is that multiple pieces cannot be used before they grow well. At that time, the price of domestic substrates was at a high level, and domestic companies did not dare to use multi-chip machines for mass production due to cost considerations. The current resumption of G10 enthusiasm shows that the cost of domestic substrates has changed to a certain extent, and epitaxy companies can further try to use multi-chip machines for mass production.

2. Competition in extension links intensifies

Since the beginning of this year, there have been many new entrants in the extension sector. Domestic leading companies such as Hantian and Tianyu have reached a far leading level in production capacity planning focusing on horizontal machines. What subsequent new entrants will face in the future is There are multiple dimensions of competition in terms of technology, customers, products, etc., but the most important thing is cost competition. If the same technical route is gradually iterated, it will be too difficult to catch up with the gap with the industry leader. Therefore, whether it is vertical machines or multi-chip machines, the market's diversified technical routes also allow new entrants to see opportunities for misaligned competition.

3. Using multi-chip processors for epitaxy OEM may be a good business

According to GlobiTech, one of the world’s largest silicon epitaxial wafer foundries, the company has begun high-volume production with G5WW C and G10-SiC systems and will continue to expand installed capacity and supply carbonization to the market over the next few years. silicon products. According to our research information, a domestic foundry company is also verifying the stability and output of G10, which will be used for mass production on the production line.

It is understood that the current selling price of G10 machines is more than twice that of LPE and other horizontal structure machines. If the cost needs to be amortized, the company needs to have large-scale mass production capabilities. At present, epitaxy foundry companies are more capable of using multi-chip machines. rationality.

https://www.eet-china.com/mp/a252961.html

Sorry, aber mit der Aixtron stimmt was nicht. Überall positive nachrichten, aber Aixtron stürz ab. Sollte das die ruhe vor den Sturm sein???

Optionen

https://ec.ltn.com.tw/article/breakingnews/4420641

This article tells us that a G10-SiC is selling for $5m with a monthly capacity of 2000 6" wafers.

THANK YOU!!!

1.) Thank you for the Article on GlobiTech. Translation is difficult to understand, if one does not understand that monolithic computer means single wafer epitaxy equipment. LPE in the picture in Link attached by you.

2.) Thank you for the article on Hua Hsu that verifies the price of the G10 - SiC and your comments on the run capacity. I took the 6 hours per run from the AGM meetings, but your explanation is very insight- and useful as it highlights & explains that there is not standard run time.

Thank you for sharing your knowledge with us.

Gruß

Optionen

Platz 2: AIXTRON

Aixtron (ISIN: DE000A0WMPJ6 – Symbol: AIXA – WKN: A0WMPJ – Währung: Euro) wird oft zu den Hightech-Aktien gezählt, gehört dort aber eigentlich nicht hin, sondern ist hier, bei den Nebenwerten der klassischen Branchen, richtig eingeordnet, weil es sich um einen Maschinen- und Anlagenbauer handelt, der aber die Halbleiterindustrie mit Produktionsanlagen beliefert. Die Aktie hebt sich momentan deutlich von den Trends der Chiphersteller selbst und anderer Zulieferer ab, die mehrheitlich unter Auftragsmangel und Druck auf den Unternehmensgewinn klagen. Aixtron hingegen, der Produktionsanlagen für die Chiphersteller liefern, konnte auch im Zuge der Halbjahreszahlen überzeugen und sogar die Gesamtjahresprognose anheben. Dementsprechend waren es die Aktienperformance und der beeindruckende Umsatzzuwachs, welche Aixtron die Silbermedaille in unserem Nebenwerte-Ranging einbrachten.

Quelle: https://www.lynxbroker.de/boerse/boerse-kurse/aktien/die-besten-aktien/die-besten-deutschen-nebenwerte/?a=3355991664&utm_medium=email&utm_source=newsletter&utm_campaign=newsletter-boersenblick&newsletter=true&goal=0_d93daae099-3c0a20c0e7-410831658

Gruß

baggo-mhOptionen

Coherent in talks with Japanese firms for silicon carbide investment-source

By Milana Vinn

September 22, 20231:13 PM EDTUpdated 34 min ago

NEW YORK, Sept 22 (Reuters) - Coherent Corp (COHR.N), a major U.S. supplier of materials used to make chips for the automotive industry, has attracted interest from four Japanese conglomerates for an investment in its silicon carbide business at a valuation of as much as $5 billion, according to a person familiar with the matter...

https://www.reuters.com/business/...ide-investment-source-2023-09-22/

Montag, 25.09.2023 12:41 von dpa-AFX

HAMBURG (dpa-AFX Analyser) - Die Privatbank Berenberg hat die Einstufung für Aixtron nach einer Investorenkonferenz auf "Buy" mit einem Kursziel von 40 Euro belassen. Die Umsätze mit Siliziumkarbid-Bauelementen (SiC) dürften im laufenden Jahr um fast 150 Prozent steigen, schrieb Analyst Gustav Froberg in einer am Montag vorliegenden Studie. Für den Zeitraum 2023 bis 2027 rechnet er mit einem durchschnittlichen jährlichen Wachstum des Halbleiterindustrie-Ausrüsters von 18 Prozent.

Ziel 42

LONDON (dpa-AFX Broker) - Die britische Investmentbank Barclays hat die Einstufung für Aixtron auf "Overweight" mit einem Kursziel von 42 Euro belassen. Die Erwartungen an die Drittquartalszahlen der europäischen Telekomausrüster- und Halbleiterunternehmen seien ausgewogen, schrieb Analyst Simon Coles in einer am Freitag vorliegenden Branchenstudie. Der Sektor habe einen Großteil seiner überdurchschnittlich guten Entwicklung abgegeben. Nun dürfte sich der Fokus aber auf die Ausblicke auf 2024 verschieben, bei denen er für die meisten Unternehmen negativer als der Konsens eingestellt sei. Aixtron ist sein bevorzugter Branchenwert./edh/la

Optionen

https://seekingalpha.com/article/...pportunities-and-big-expectations

Optionen

https://www.linkedin.com/company/aixtron-se/posts/?feedView=all

DB mit Kurszielbestätigung bei € 39 und das, wie die meisten anderen Analysten, nach Gesprächen mit Management in Vorfeld der Zahlen oder Besuch in Herzogenrath.

Gruß baggo-mh

Optionen

IFX held an interesting investor call last week, see presentation and replay link below.

In essence they expect 10%+ revenue growth in their Automotive Division even if the Auto market (volume) is only flat, highlighting the structural growth of SIC/GAN, which they specifically highlight.

Lots of customer wins for SIC, see slides. THey also comment on the Chinese market, threat from Chinese SIC players etc.

https://www.infineon.com/cms/en/about-infineon/...ns-conference-calls

https://www.infineon.com/dgdl/...eId=8ac78c8b8ada5179018afa2423f6000c

All underpins that demand for SIC/GAN remains solid and structural,

regards,

Fel