AGNICO EAGLE MINES mit 50% Potenzial

buy the dip ^^

keine Empfehlung zu irgendwas

Optionen

| Boardmail an "chivalric" |

Wertpapier: Agnico-Eagle Mines Ltd |

Grds. ist Corona überall schlecht und führt zu reduzierten Produktionen oder beeinträchtigt diese irgendwie.

Derzeit ist aber Agnico immer noch für mich das Beste, was es im Sektor gibt, weil die Minenen nicht in Dritte-Welt-Diktaturen liegen. Und insgesamt hält sich der Kurs auch unter Berücksichtigung der Übernahme ja gut. Schlussendlich ist fast nur der Goldpreis von Relevanz ...

https://www.bnnbloomberg.ca/video/...usses-agnico-eagle-mines~2364905

Ende Februar kommen erstmals konsolidierte Zahlen mit Kirkland. Das wird eine Zeitenwende.

Tiedje uund andere EW´ler sehen Gold bis 15000USD steigen. Unklar ist nur, ob Gold vorher nochmal unter 1700 absackt oder nicht. Am Ziel ändert das nichts.

Agnico Eagle Mines Limited (AEM) CEO Ammar Al-Joundi on Q4 2021 Results - Earnings Call Transcript

SeekingAlpha, heute - inkl. Tonaufnahme

has been declared (previous quarterly dividend was $0.35)" (s. News Release weiter oben)

https://www.bnnbloomberg.ca/video/...agnico-eagle-s-sean-boyd~2389992

https://www.bnnbloomberg.ca/video/...trategy-agnico-eagle-ceo~2522787

Kaufempfehlung von Taylor Dart, 28.9.

https://seekingalpha.com/article/...-smart-move-to-boost-the-pipeline

Angehängte Grafik:

agnico_20220929.png (verkleinert auf 65%)

agnico_20220929.png (verkleinert auf 65%)

https://www.bnnbloomberg.ca/video/...duction-and-cost-control~2551115

Eins steht fest: An Kryptos glaube ich nicht und

")

Auszug

"

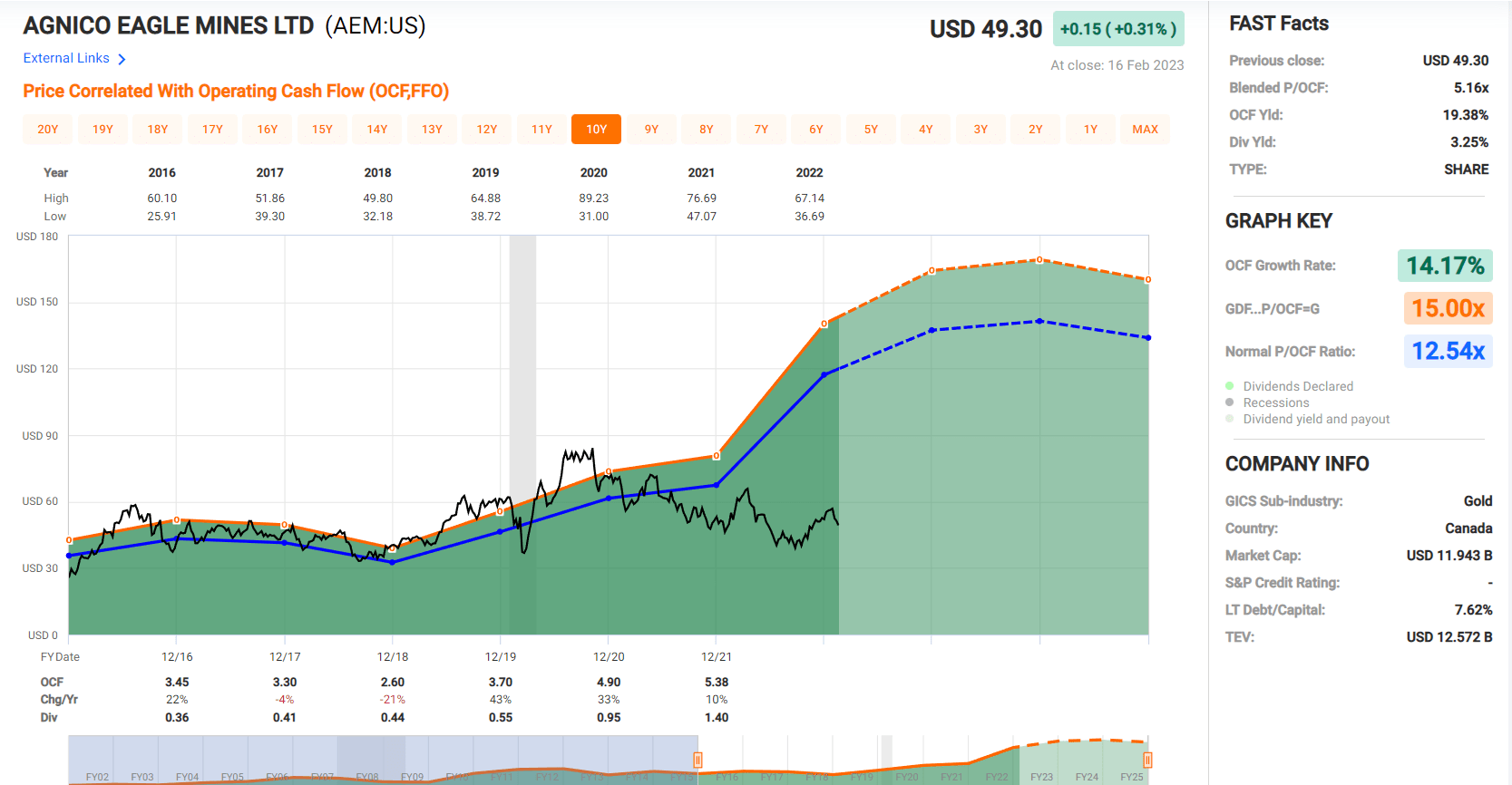

Looking at the chart above , Agnico has historically traded at 12.5x cash flow, and I would argue that a multiple of 13.0 is more than reasonable, given that it's the premier major producer with favorable jurisdictions and attractive margins. Based on conservative FY2023 cash flow estimates of $4.50, this translates to a fair value for the stock of US$58.50, pointing to 20% upside from current levels. However, this fair value estimate is based on what will be a weak year for Agnico, and it doesn't place any value on its strong development pipeline or exploration upside, where I think we can easily assign a value of $5.0+ billion (Santa Gertrudis, Upper Beaver, Wasamac, Hammond Reef, Hope Bay, San Nicolas [50%], exploration upside). It also doesn't place any value on organic growth at existing assets like Detour Lake."

"Given that valuing the stock on cash flow understates the company's long-term potential, I believe the best way to value Agnico Eagle Mines Limited stock is on a P/NAV basis. Based on an estimated net asset value of ~$23.7 billion after adjusting for G&A expenses, and assigning a 1.45x P/NAV multiple given its strong history of reserve replacement, I see a fair value for Agnico stock of ~$35.0 billion. After dividing by ~490 million shares (year-end 2023), this translates to a fair value for the stock of US$71.40, translating to a 44% upside from current levels or ~47% upside on a total return basis.

Importantly, this doesn't account for upside in the gold price, with these assumptions based on a $1,700/oz gold price, in line with the three-year average. Given its undervaluation, I continue to see Agnico as one of the best buy-the-dip candidates sector-wide."

Chart Cashflow

https://static.seekingalpha.com/uploads/2023/2/17/...38073_origin.png

{kind=link}

https://seekingalpha.com/article/...eagle-mines-a-softer-2023-outlook

******

Prognosen

https://www.marketscreener.com/quote/stock/...ITE-1408914/financials/

******

Saisonalität: Bodenbildung im März, Hoch August

https://charts.equityclock.com/...le-mines-ltd-nyseaem-seasonal-chart

Angehängte Grafik:

agnico_prognosen.jpg (verkleinert auf 63%)

agnico_prognosen.jpg (verkleinert auf 63%)

AEM ist extrem überverkauft, fundamental alles i.O., das Gap bei 54$ sollte wie ein Magnet wirken sobald die 200er bei ~48$ genommen wird. als starkes Zeichen werte ich auch, dass trotz Divi-Abschlag der Kurs gestern gestiegen ist; bin long

Optionen

| Boardmail an "chivalric" |

Wertpapier: Agnico-Eagle Mines Ltd |

Optionen

| Boardmail an "chivalric" |

Wertpapier: Agnico-Eagle Mines Ltd |

Optionen

| Boardmail an "chivalric" |

Wertpapier: Agnico-Eagle Mines Ltd |

Vorbörslicher Handel

56,71

+0,51(+0,91%)

Angehängte Grafik:

agnico_20230411.png (verkleinert auf 65%)

agnico_20230411.png (verkleinert auf 65%)